United States EV Charging As A Service Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

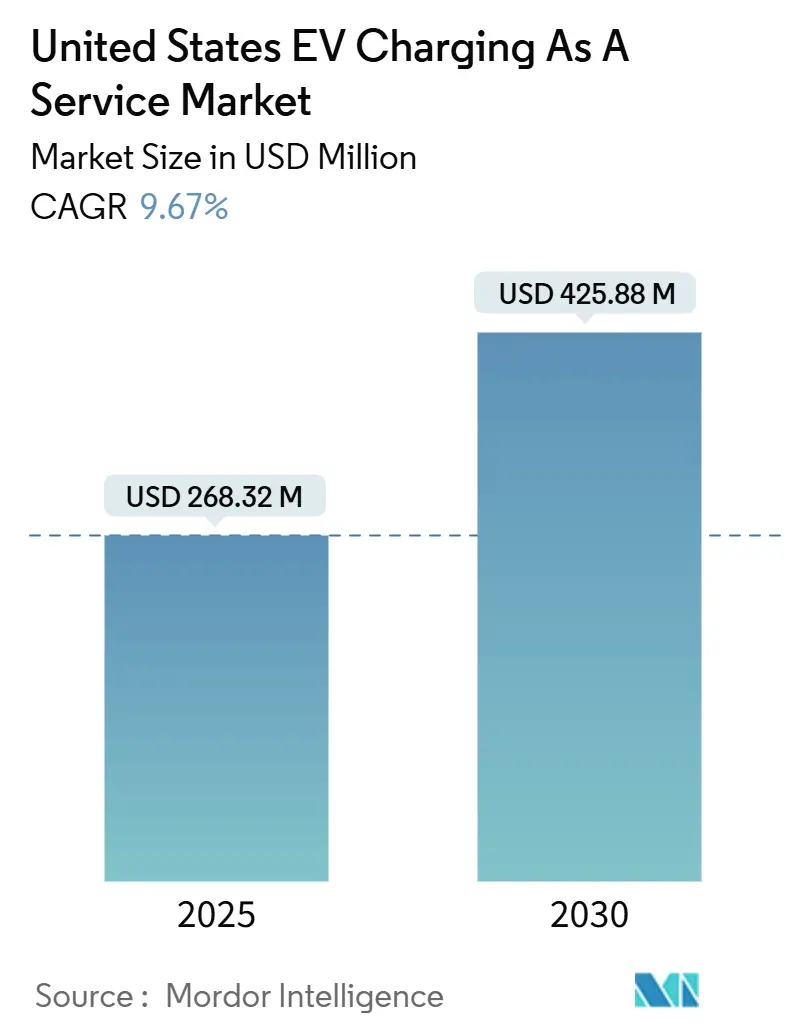

| Market Size (2025) | USD 268.32 Million |

| Market Size (2030) | USD 425.88 Million |

| Growth Rate (2025 - 2030) | 9.67% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States EV Charging As A Service Market Analysis by Mordor Intelligence

The United States EV Charging As A Service market size stands at USD 268.32 million in 2025 and is projected to reach USD 425.88 million by 2030, registering a 9.67% CAGR. Federal funding under the National Electric Vehicle Infrastructure program, fast-growing corporate electrification mandates, and tariff innovations that lower capital outlays are steering sustained demand. Rapid technology gains in predictive maintenance and plug-and-charge protocols are further reshaping operating models, while California, Texas, and New York continue to anchor network scale. The service-oriented approach converts fixed infrastructure costs into monthly fees, boosting adoption among fleet operators seeking capital-light solutions. Grid upgrade bottlenecks and payment-system fragmentation remain near-term hurdles, but nationwide connector standardization scheduled for 2025 is expected to lift user confidence.

Key Report Takeaways

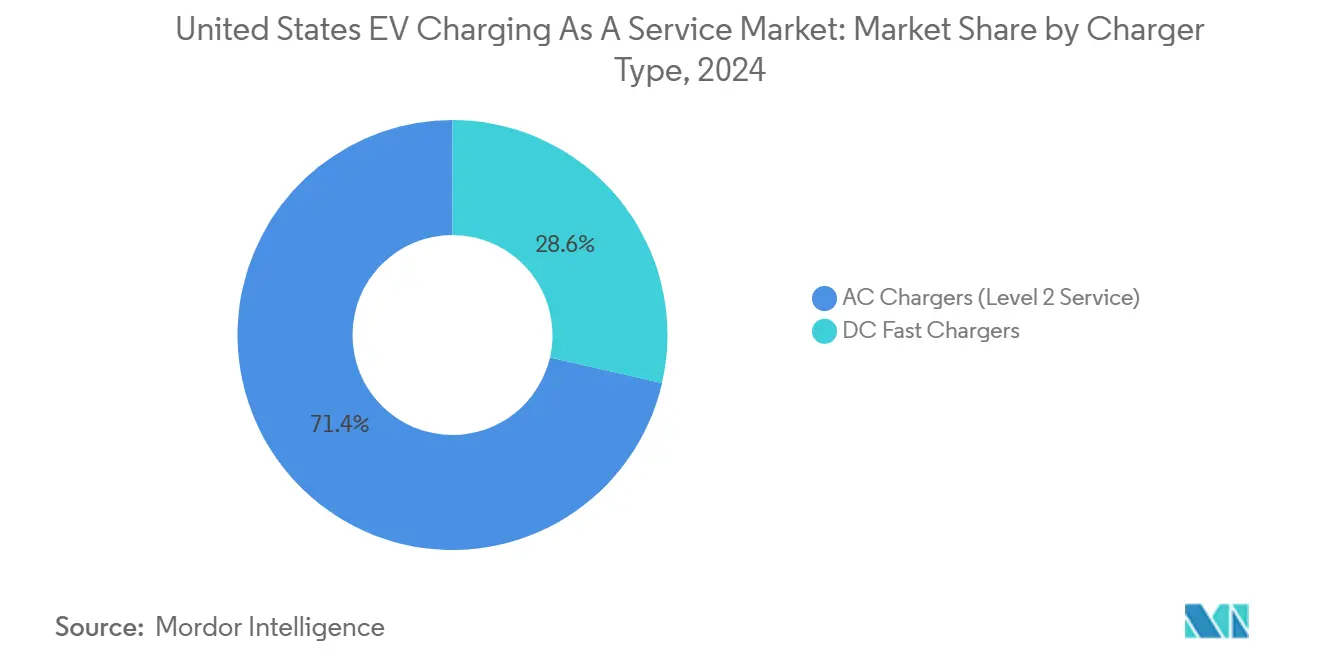

- By charger type, AC Chargers (Level 2) led with a 71.38% revenue share in 2024; DC Fast Chargers are projected to expand at a 24.76% CAGR through 2030.

- By power output, Level 2 systems captured 66.27% share of the United States EV Charging As A Service market size in 2024, while High-Power charging is advancing at a 31.14% CAGR to 2030.

- By fleet service type, company vehicles and motor pools accounted for 44.89% share of the United States EV Charging As A Service market size in 2024, whereas the delivery and logistics segment is set to grow at a 27.36% CAGR.

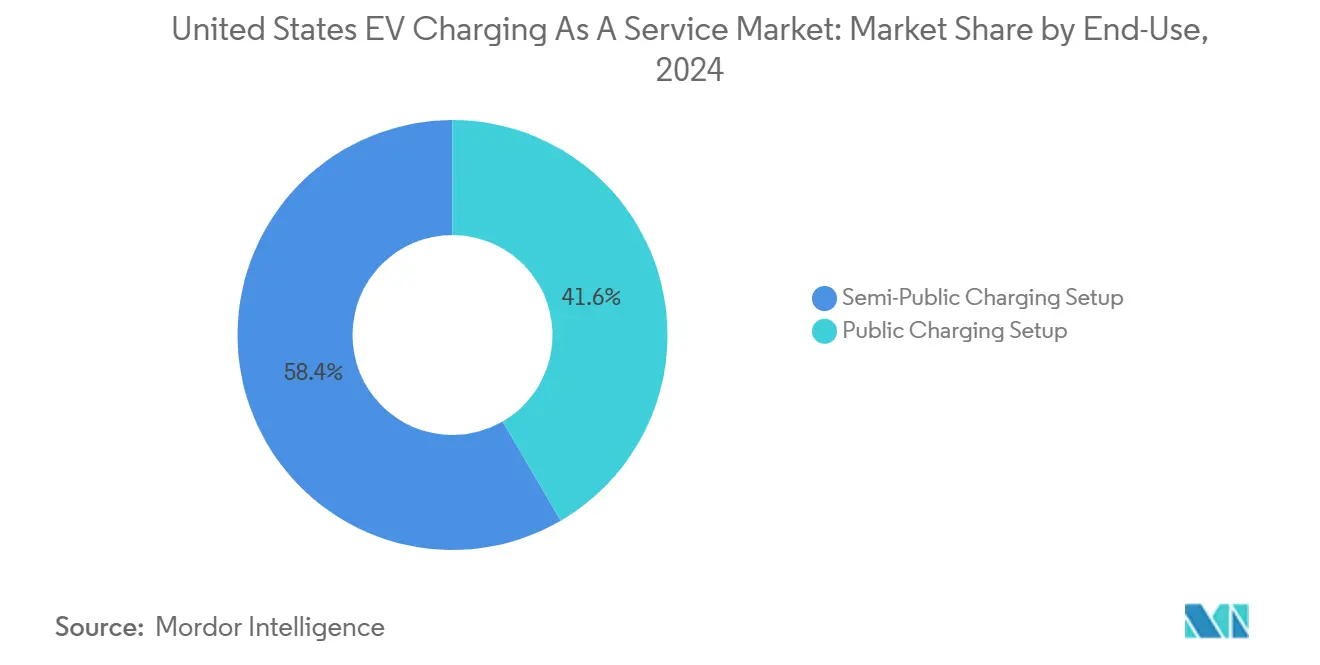

- By end-use, semi-public charging setups held 58.42% share; public charging setups are poised for a 22.61% CAGR.

- By customer business model, subscription-based Charging as a Service commanded 47.15% share in 2024; hybrid models record the top CAGR at 19.03% through 2030.

- By geography, the West secured 35.24% share in 2024, and the South presents the fastest regional CAGR of 18.08% to 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with United states being one of the contributors. Our global ev charging as a service market size represents that cumulative total.

United States EV Charging As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NEVI Federal-State Funding Roll-Out | +2.8% | Nationwide; concentrated in Texas, California, New York | Medium term (2–4 years) |

| Corporate ESG Fleet-Electrification Mandates | +2.1% | West Coast and Northeast early adopters | Short term (≤2 years) |

| Declining Battery-Pack Costs Reach TCO Parity | +1.9% | Global; accelerated on high-utilization corridors | Long term (≥4 years) |

| Utility “Subscription-Ready” Tariffs | +1.4% | California, Texas, New York utility partnerships | Medium term (2–4 years) |

| AI-Driven Predictive Maintenance | +0.8% | High-traffic urban markets | Short term (≤2 years) |

| Idle-Fee Revenue-Sharing Models | +0.7% | Congested metropolitan areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

NEVI Federal-State Funding Roll-Out

The Infrastructure Investment and Jobs Act's USD 5 billion NEVI allocation represents the most significant federal intervention in charging infrastructure development, fundamentally altering market dynamics for service providers[1]"National Electric Vehicle Infrastructure Formula Program," Federal Highway Administration, fhwa.dot.gov.. State-level deployment accelerated dramatically in 2024, with 33 states issuing solicitations and 16 states awarding contracts, generating over 170,000 public charging ports nationwide. Texas leads with USD 407.77 million in five-year funding, followed by California at USD 383.67 million, creating regional hubs that service providers can leverage for network expansion. The program's requirement for 97% uptime standards and interoperability compliance is driving service providers to invest in advanced monitoring systems and standardized protocols, elevating operational capabilities across the industry. NEVI's emphasis on Alternative Fuel Corridors with stations positioned no more than 50 miles apart creates predictable demand patterns that enable service providers to optimize route planning and capacity utilization for fleet customers.

Corporate ESG Fleet-Electrification Mandates

Corporate sustainability commitments are generating substantial demand for charging services as companies transition fleet operations to meet net-zero targets. Leading businesses have expanded their electric vehicle fleets globally. The commercial fleet electrification surge shows 81% growth among U.S. commercial fleets from 2022 to 2023, driven by companies like Walmart and Amazon committing to zero emissions by 2040[2]"'Huge Opportunity' for Last Mile, Drayage Fleets in Transition to EVs," Supply Chain Brain, supplychainbrain.com.. Ford Pro's assessment tool reveals that 53% of evaluated fleet vehicles are ready for electric conversion, indicating massive latent demand for charging services. California's Advanced Clean Fleets regulation mandates zero-emission vehicle adoption for specific fleet categories starting January 2024, creating compliance-driven demand that extends beyond voluntary corporate initiatives.

Declining Battery-Pack Costs Reach TCO Parity

Battery cost reductions are approaching the critical threshold where electric vehicle total cost of ownership matches conventional vehicles, fundamentally altering fleet economics and charging service demand patterns. While specific 2024 battery cost data varies, the trend toward TCO parity is accelerating fleet adoption decisions, particularly in high-utilization applications where fuel savings compound rapidly. Service providers benefit from this shift as fleet operators become less sensitive to charging service premiums when overall vehicle economics favor electrification. The transition creates opportunities for innovative pricing models that capture value from operational savings while providing predictable charging costs for fleet budgeting. Energy storage integration capabilities of modern EV batteries enable vehicle-to-grid services, allowing charging service providers to develop revenue streams from grid stabilization and peak shaving services.

Utility "Subscription-Ready" Tariffs Cut Capex

Utility rate structures are evolving to support charging service business models through time-of-use tariffs and demand response programs that reduce infrastructure costs and operational expenses. Synapse Energy Economics analysis demonstrates that EVs contributed approximately USD 3.12 billion more in revenues than associated costs from 2011 to 2021, enabling utilities to offer favorable rates for charging services. Xcel Energy's commitment to installing 30,000 charging ports by 2030 exemplifies utility partnerships that provide infrastructure support and favorable pricing for service providers[3]"The Proof Is in the Power: 2025 Commercial Electrification Trends," fromtheroad.ford.com.. Managed charging techniques can reduce distribution grid investment requirements by 30%, creating cost savings that utilities can pass through to charging service providers via subscription-friendly rate structures. These tariff innovations enable service providers to offer predictable monthly pricing to fleet customers while optimizing charging schedules to minimize demand charges and maximize grid benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Grid-Upgrade Costs for DC Fast Sites | -1.8% | National; acute in rural and suburban distribution upgrades | Long term (≥4 years) |

| Interoperability and Payment Fragmentation | -1.2% | National; multi-network fleet challenges | Medium term (2–4 years) |

| Soaring Demand Charges in Key Utility Territories | -1.0% | National; especially in deregulated electricity markets | Medium term (2–4 years) |

| Reliability-Penalty Clauses in NEVI Contracts | -0.9% | Nationwide; tied to federal grant recipients | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Grid-Upgrade Costs for DC Fast Sites

Distribution grid modernization requirements represent the most significant infrastructure barrier constraining charging service expansion, particularly for high-power applications serving commercial fleets. California's distribution grid upgrades alone are estimated to cost USD 20-26 billion by 2035 to support transportation electrification goals, with 67% of feeders requiring capacity enhancements. Grid connection timelines for high-powered EV charging stations extend up to 2 years due to outdated utility processes and interconnection studies, creating deployment delays that impact service provider expansion plans. Commercial EV charging survey data reveals that 75% of respondents identify grid limitations as major roadblocks, with government incentives becoming the top concern for project viability at 45% in 2024. The mismatch between charging infrastructure deployment timelines and grid upgrade schedules forces service providers to either accept higher connection costs or delay market entry in high-demand locations.

Interoperability and Payment-Standard Fragmentation

Payment system complexity and charging network incompatibilities create operational friction that constrains market growth, particularly for fleet customers requiring seamless multi-network access. The ChargeX Consortium identifies network connectivity issues, hardware robustness problems, and user interface inconsistencies as primary barriers to reliable charging experiences. Current market fragmentation requires fleet operators to maintain multiple accounts and payment methods across different charging networks, increasing administrative overhead and reducing operational efficiency. The transition to North American Charging Standard (NACS) creates temporary complexity as service providers must support both CCS and NACS connectors during the migration period, requiring dual-port installations or adapter management systems. Universal plug-and-charge protocol implementation scheduled for 2025 promises to address these issues through standardized authentication and billing processes, but deployment coordination across multiple stakeholders remains challenging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charger Type: AC Dominance Yields to DC Fast Growth

AC Chargers (Level 2 Service) maintain market leadership with 71.38% share in 2024, reflecting their cost-effectiveness for overnight fleet charging and workplace applications where vehicles remain stationary for extended periods. These systems are the backbone for depot charging operations, particularly effective for delivery fleets and company vehicle pools that return to central locations daily. DC Fast Chargers command the growth narrative with 24.76% CAGR through 2030, driven by commercial applications requiring rapid turnaround times and public charging networks prioritizing customer convenience.

The shift toward DC fast charging reflects evolving fleet operational requirements and consumer expectations for charging speed parity with conventional fueling. Significant partnerships like GM-ChargePoint's commitment to install 500 ultra-fast charging ports by the end of 2025 demonstrate industry confidence in high-power charging demand. Tesla's Supercharger network expansion to non-Tesla vehicles through partnerships with Ford and GM creates additional DC fast charging capacity while generating projected revenues of USD 6-12 billion annually by 2030. Service providers increasingly position DC fast charging as premium offerings with higher per-session revenues, while AC charging remains the volume foundation for subscription-based fleet services.

By Power Output: High-Power Charging Drives Premium Services

Level 2 (22 to 50 kW) charging systems capture 66.27% market share in 2024, serving as the workhorse for fleet depot applications and workplace charging installations where cost per port and electrical infrastructure requirements favor moderate power levels. These systems align with typical fleet dwell times and provide sufficient charging speeds for most commercial vehicle duty cycles without requiring expensive electrical upgrades. High-Power (More than 150 kW) charging represents the fastest-growing segment at 31.14% CAGR, reflecting demand for rapid charging solutions in high-throughput commercial applications and public charging networks targeting premium user experiences.

The power output segmentation reveals a bifurcated market where service providers must balance infrastructure costs against customer value propositions. Level 1/AC (Less than 22 kW) systems serve niche applications in residential and low-utilization commercial settings, while Fast (50 to 150 kW) charging occupies the middle ground for semi-public applications requiring faster turnaround than Level 2 but without the infrastructure costs of high-power installations. ChargePoint's Omni Port technology enables compatibility across multiple charging standards, allowing service providers to maximize utilization regardless of vehicle connector type. The emergence of megawatt charging systems for heavy-duty applications signals future expansion into specialized fleet segments requiring ultra-high power delivery for large battery packs and minimal charging downtime.

By Fleet Service Type: Delivery Logistics Accelerates Electrification

Company Vehicles and Motor Pools dominate with 44.89% market share in 2024, representing traditional corporate fleet applications where predictable routes and central depot charging align with current EV capabilities and charging infrastructure. These applications benefit from established operational patterns and centralized management structures, facilitating charging service integration. Delivery and Logistics emerge as the fastest-growing segment at 27.36% CAGR, driven by e-commerce expansion, last-mile delivery optimization, and regulatory pressures in urban markets requiring zero-emission vehicles.

Amazon's position as the largest private EV charging operator with over 17,000 chargers across 120 warehouses exemplifies the scale of logistics sector electrification. The company's partnership with Rivian for 13,500 custom delivery vans demonstrates integrated approaches combining vehicle procurement with charging infrastructure development. UPS and FedEx face challenges transitioning to electric vans due to battery shortages and supply constraints, creating opportunities for charging service providers to offer flexible solutions during the transition period. Passenger Transportation Fleets represent emerging opportunities as ride-sharing services and taxi operators evaluate electrification strategies. However, adoption remains constrained by utilization patterns requiring rapid charging capabilities and extensive network coverage.

By End-Use: Public Charging Gains Commercial Momentum

Semi-Public Charging Setup commands 58.42% market share in 2024, reflecting the prevalence of workplace, retail, and hospitality charging installations that serve specific customer bases while maintaining operational control over access and pricing. These installations provide predictable revenue streams for service providers while offering convenient charging options for fleet operators and employees. Public Charging Setup demonstrates strong growth at 22.61% CAGR through 2030, driven by expanding highway corridor networks, urban fast charging hubs, and retail partnerships enhancing accessibility for diverse user groups.

The end-use segmentation reflects evolving business models as traditional boundaries blur between public and semi-public applications. BP Pulse's partnership with Simon Property Group to install over 900 charging bays at 75 shopping locations exemplifies retail integration strategies that combine public accessibility with commercial partnerships. Walmart's initiative to establish fast-charging networks starting with 15 Dallas-Fort Worth locations demonstrates retail chains leveraging existing real estate for charging services. The distinction between public and semi-public installations increasingly depends on access policies and pricing structures rather than physical location characteristics, enabling service providers to optimize utilization across different customer segments.

By Customer Business Model: Hybrid Models Emerge as Flexible Solutions

Subscription-based (CaaS) models maintain 47.15% market share in 2024, providing predictable revenue streams for service providers while offering fleet operators simplified billing and budget planning capabilities. These models typically feature monthly fees around USD 200 per Level 2 station, converting capital expenditures into operational expenses while transferring maintenance and operational risks to service providers. Hybrid Models accelerate at 19.03% CAGR, combining subscription base fees with usage-based components to accommodate varying fleet utilization patterns and seasonal demand fluctuations.

Pay-per-Use models serve customers requiring occasional charging access or testing electrification strategies before committing to subscription arrangements. The evolution of the business model reflects market maturation as service providers develop sophisticated pricing strategies that capture value while providing flexibility for diverse customer requirements. Revenue diversification opportunities include idle fee structures that optimize charger utilization, demand response participation that generates grid services revenue, and advertising partnerships that monetize dwell time during charging sessions. Service providers increasingly offer customized contract terms that blend subscription guarantees with usage-based scaling, enabling fleet operators to manage electrification transitions while providing predictable revenue foundations for infrastructure investments.

Geography Analysis

The West region dominates the United States EV Charging As A Service market with 35.24% share in 2024, driven by California's aggressive electrification policies and established EV adoption patterns that create dense charging demand. California's Zero-Emission Vehicle Infrastructure Plan targets 1.01 million chargers by 2030, with USD 384 million in NEVI funding supporting network expansion. The state's reliability standards requiring 97% uptime for publicly funded chargers and 90% successful charge attempt rates by 2026 establish operational benchmarks that elevate service quality across the region. National Grid's Electric Highways Study for Massachusetts and New York demonstrates Northeast commitment to comprehensive charging infrastructure development through 2045, supporting regional market expansion.

The South region exhibits the fastest growth at 18.08% CAGR through 2030, propelled by Texas's USD 407.77 million NEVI allocation and expanding commercial fleet adoption in logistics-intensive markets. Texas Department of Transportation's comprehensive EV charging framework aims to establish statewide network coverage while supporting freight corridor electrification. The Southeast Regional Electric Vehicle Information Exchange (SE REVI) coordinates multi-state infrastructure planning and policy development, particularly focusing on rural and low-income community access. South Carolina's utility investment discussions and regulatory framework development indicate regional momentum building across traditional energy markets.

The Midwest region benefits from strategic retail partnerships and manufacturing sector electrification initiatives, exemplified by EVgo's expansion with Meijer to install 480 new fast charging stalls across six states by 2027. The region's industrial base and freight transportation networks create opportunities for fleet-focused charging services, while retail partnerships provide public charging accessibility. Northeast markets demonstrate mature adoption patterns with established policy frameworks and utility partnerships supporting charging service development, though growth rates moderate as markets mature and competition intensifies for prime locations and customer relationships.

Coverage of the ev charging as a service market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for China, India, and South Korea, each shaped by local operating conditions.

Competitive Landscape

The United States EV charging as a service market exhibits moderate concentration. Established network operators maintain competitive advantages through infrastructure scale and strategic partnerships, while specialized service providers target fleet applications and regional markets. ChargePoint leads through comprehensive service offerings and technology integration. Its AI-powered diagnostic tools enable drivers to report charging station issues through photo analysis, improving network reliability and reducing maintenance costs. Tesla's Supercharger network expansion to non-Tesla vehicles through partnerships with Ford and GM creates additional revenue streams while maintaining technological leadership in charging speed and reliability.

Strategic partnerships define competitive positioning as operators seek to expand network coverage and enhance customer value propositions without bearing full infrastructure costs. The formation of IONNA as a joint venture among major automakers signals industry consolidation around shared charging infrastructure investments. At the same time, companies like FreeWire Technologies focus on mobile and flexible charging solutions for fleet applications.

White-space opportunities exist in specialized fleet applications, rural market coverage, and integrated energy management services that combine charging with renewable energy and storage systems. Emerging disruptors leverage software-defined approaches and modular hardware designs to reduce deployment costs and improve operational flexibility. At the same time, established players defend market positions through exclusive retail partnerships and utility collaborations that create barriers to competitive entry.

United States EV Charging As A Service Industry Leaders

-

ChargePoint

-

Tesla

-

Electrify America

-

EVgo

-

Blink Charging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ionna secured over 3,000 contracted battery charging bays through strategic partnerships, including agreements with Wawa convenience stores to expand ultra-fast charging network coverage across key transportation corridors.

- May 2025: BP Pulse signed a strategic agreement with Waffle House to expand its ultra-fast EV charging network across the United States, leveraging the restaurant chain's extensive highway presence to enhance charging accessibility.

- November 2024: EVgo and Meijer announced the expansion of their partnership to install up to 480 new fast charging stalls at Meijer locations across six Midwestern states.

United States EV Charging As A Service Market Report Scope

| AC Chargers (Level 2 Service) |

| DC Fast Chargers |

| Level 1/AC (Less than 22 kW) |

| Level 2 (22 to 50 kW) |

| Fast (50 to 150 kW) |

| High-Power (More than 150 kW) |

| Company Vehicles and Motor Pools |

| Delivery and Logistics |

| Passenger Transportation Fleets |

| Semi-Public Charging Setup |

| Public Charging Setup |

| Subscription-based (CaaS) |

| Pay-per-Use |

| Hybrid Models |

| Northeast |

| Midwest |

| South |

| West |

| By Charger Type | AC Chargers (Level 2 Service) |

| DC Fast Chargers | |

| By Power Output | Level 1/AC (Less than 22 kW) |

| Level 2 (22 to 50 kW) | |

| Fast (50 to 150 kW) | |

| High-Power (More than 150 kW) | |

| By Fleet Service Type | Company Vehicles and Motor Pools |

| Delivery and Logistics | |

| Passenger Transportation Fleets | |

| By End-Use | Semi-Public Charging Setup |

| Public Charging Setup | |

| By Customer Business Model | Subscription-based (CaaS) |

| Pay-per-Use | |

| Hybrid Models | |

| By Region (United States) | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How large is the United States EV Charging As A Service market in 2025?

The market is valued at USD 268.32 million in 2025 and is forecast to reach USD 425.88 million by 2030.

What growth rate is expected for subscription-based charging services?

By 2030, hybrid models are set to grow at a robust CAGR of 19.03%.

Which region is growing fastest for charging-as-a-service deployments?

The South, led by Texas, shows the highest regional CAGR at 18.08% through 2030 due to sizable NEVI allocations and logistics-sector demand.

Why are DC fast chargers gaining popularity?

Commercial fleets and consumers favor rapid turnaround times, driving a 24.76% CAGR for DC fast infrastructure through 2030.

What is the main barrier to large-scale DC fast charging expansion?

High grid-upgrade costs and lengthy interconnection processes add significant capital hurdles, especially in rural and suburban areas.

How will standardization impact payment and connector compatibility?

The 2025 rollout of universal plug-and-charge protocols and North American Charging Standard connectors is expected to streamline authentication and reduce network fragmentation.

Page last updated on: