South Korea EV Charging As A Service Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

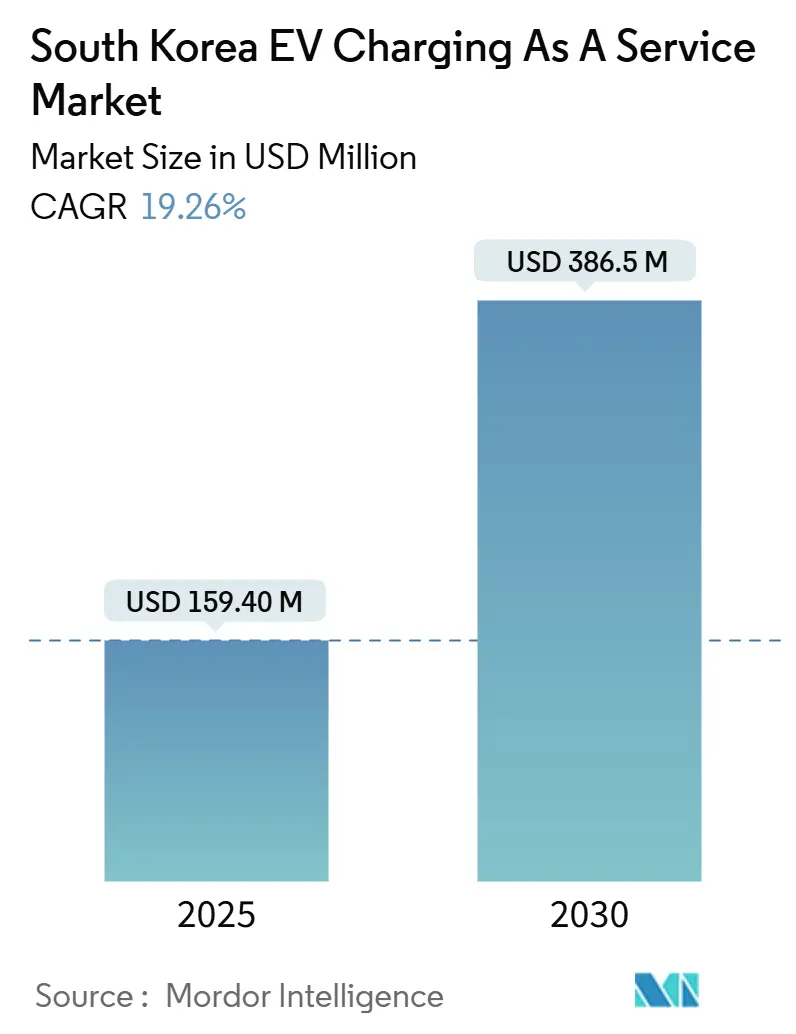

| Market Size (2025) | USD 159.40 Million |

| Market Size (2030) | USD 386.5 Million |

| Growth Rate (2025 - 2030) | 19.26% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea EV Charging As A Service Market Analysis by Mordor Intelligence

The South Korea EV Charging as a Service market size is poised to be at USD 159.4 million in 2025 and is projected to reach USD 386.50 million by 2030, expanding at a 19.26% CAGR. Demand is propelled by generous national subsidies that favor rapid chargers, the rapid electrification of delivery fleets, and the willingness of oil refiners to repurpose fuel stations into mobility hubs. Healthy charger utilization stems from the country’s 1.7:1 EV-to-charger ratio, which exceeds global benchmarks and accelerates operator revenue payback. At the same time, grid congestion risks and a dip in 2023 EV sales temper short-term growth, encouraging providers to optimize site selection, adopt AI-based load balancing, and explore depot-centric business models. Heightened mergers and acquisitions activity, led by SK, GS Caltex, and PlugLink, signals a pivot from infrastructure rollout toward profitability management and scale efficiencies. Innovative trials, ranging from megawatt-class systems for trucks to AI-guided charging robots, indicate that South Korea's EV charging as a service market will continue to test advanced concepts before larger global deployment.

Key Report Takeaways

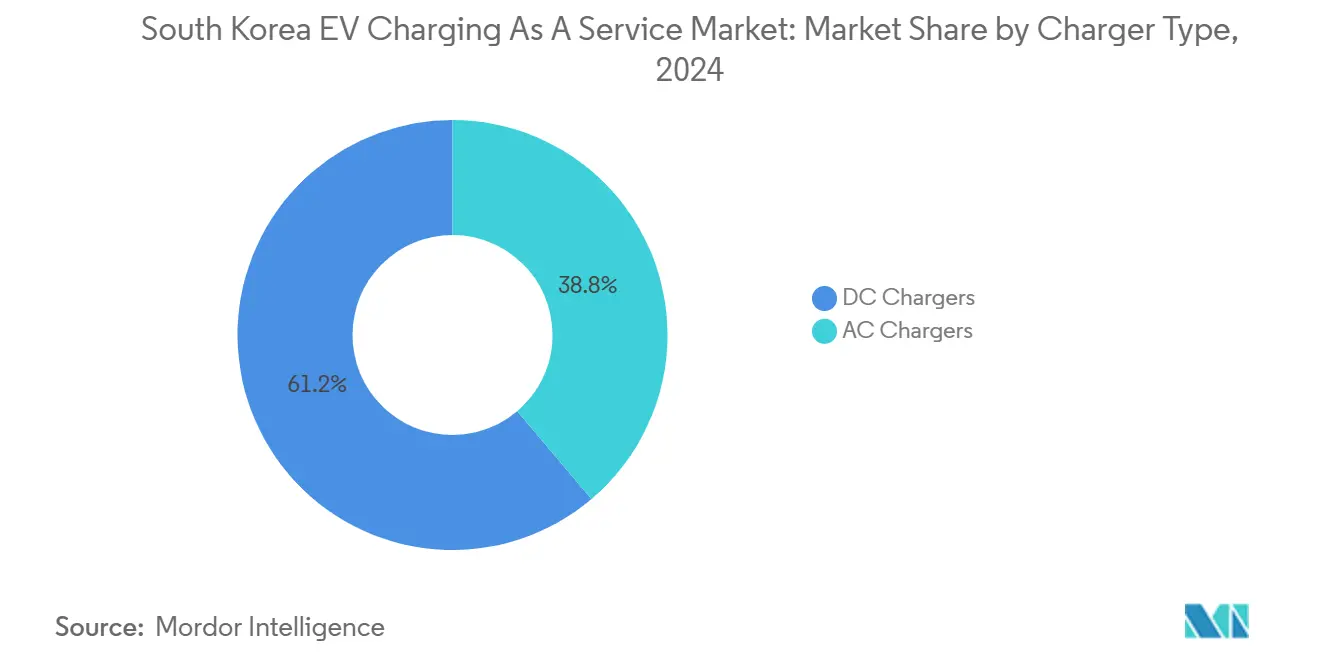

- By charger type, DC units held 61.23% of the South Korea EV Charging As A Service market share in 2024, while DC Chargers are expected to grow at a 28.42% CAGR through 20230.

- By power output, fast chargers (50 to 150 kW) accounted for 47.54% of the South Korea EV Charging as a Service market size in 2024, while ultra-fast systems above 150 kW are on track for a 37.01% CAGR through 2030.

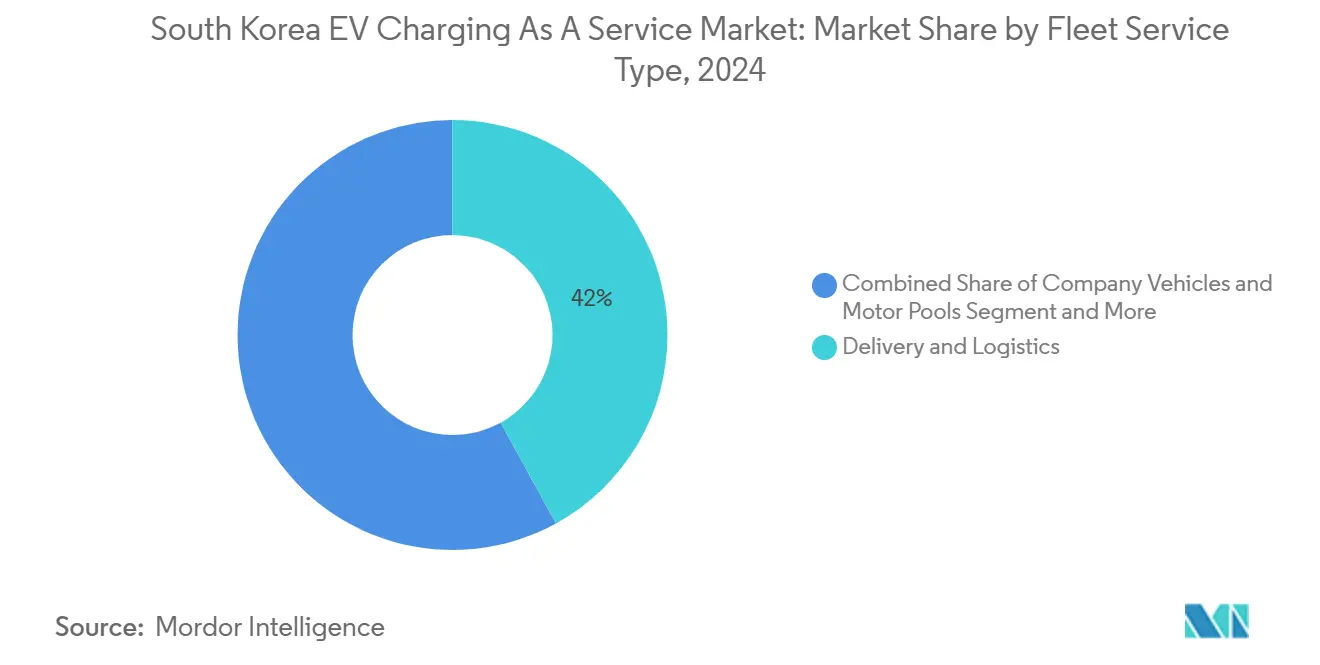

- By fleet service type, delivery and logistics represented 42.08% revenue share in 2024 and are forecast to expand at a 25.26% CAGR to 2030.

- By end-use, public charging captured 64.17% revenue share in 2024 and is advancing at a 24.53% CAGR through 2030.

Competitive positioning in South korea includes both locally based firms and those operating across multiple regions. The market landscape in the global ev charging as a service industry research shows how these players are arranged internationally.

South Korea EV Charging As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Government CAPEX Subsidies for Rapid Chargers | +4.2% | National, with Seoul metropolitan area priority | Short term (≤ 2 years) |

| Corporate Zero-Emission Logistics Mandates | +3.8% | National, concentrated in industrial corridors | Medium term (2–4 years) |

| Oil-Refiner Conversion of Forecourts into EV Hubs | +2.9% | National, highway and urban gas station networks | Medium term (2–4 years) |

| EV-to-Charger Ratio of Less Than 2:1 Boosts Utilisation Economics | +2.1% | National, particularly urban centers | Short term (≤ 2 years) |

| AI-Optimised Dynamic Load-Balancing Pilots | +1.7% | Seoul, Busan, and smart city demonstration zones | Long term (≥ 4 years) |

| Megawatt-Charging-System (MCS) Trials for Heavy Fleets | +1.4% | Industrial logistics hubs and highway corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Government CAPEX Subsidies for Rapid Chargers

Korea's Ministry of Environment increased charging facility support by 43% in 2025, allocating KRW 3.757 billion (USD 2.8 million) for rapid chargers and KRW 2.43 trillion (USD 1.8 billion) for smart control systems. This represents a strategic shift from broad EV adoption incentives to targeted infrastructure density improvements. The subsidy structure now prioritizes urban rapid charger installations and includes CCTV installation costs, addressing safety concerns following high-profile EV fire incidents. Government support reached KRW 371 billion (USD 278 million) in 2024, demonstrating sustained commitment despite fiscal pressures. The policy evolution reflects recognition that charging infrastructure availability directly correlates with EV adoption rates, creating a multiplier effect on service demand.

Corporate Zero-Emission Logistics Mandates

Korea's K-EV100 campaign has enrolled 56 major corporations, including Samsung SDI, Lotte Chemicals, and SK Innovation, committing to fleet electrification targets. CJ Logistics' commitment to replace all vehicles under 1 ton with EVs by 2030 exemplifies the scale of transformation, targeting 37% GHG emission reductions[1]"From Fossil Fuels to Electric Vehicles: A Green Shift in Transportation and Logistics," perspectives.se.com.. This corporate mandate creates predictable, high-utilization demand for charging services, particularly during business hours when public infrastructure experiences lower usage. The logistics sector's electrification timeline aligns with charging service providers' capacity expansion plans, reducing investment risk. Fleet electrification mandates drive demand for specialized charging solutions, including depot charging and route optimization services that enhance service provider revenue streams.

Oil-Refiner Conversion of Forecourts into EV Hubs

HD Hyundai Oilbank operates 2,500 gas and charging stations across Korea, positioning traditional fuel retailers as mobility infrastructure leaders[2]HD Hyundai Oilbank, hd-hyundaioilbank.co.kr.. GS Caltex's partnership with Kakao Mobility for electric bicycle charging demonstrates refiners' strategy to transform forecourts into comprehensive mobility hubs rather than simple fuel dispensing locations. This conversion leverages existing real estate assets and customer traffic patterns while addressing the declining gasoline demand trajectory. Shell's global strategy to divest 1,000 retail sites for EV charging expansion provides a template for Korean refiners' transformation. The forecourt conversion model creates high-visibility charging locations with established customer convenience infrastructure, enhancing charging service economics.

EV-to-Charger Ratio of Less than 2:1 Boosts Utilization Economics

Korea maintains a 1.7:1 EV-to-charger ratio as of January 2025, significantly better than global averages, with 405,000 chargers supporting the EV fleet[3]"Korea has one charger for every 1.7 electric cars," The Korea Herald, koreaherald.com.. This ratio creates optimal utilization conditions for charging service providers, reducing idle capacity costs that plague over-deployed markets. The annual addition of approximately 100,000 chargers since 2021 demonstrates infrastructure scaling aligned with EV adoption curves. However, concerns emerge over decreased usage rates in some locations, suggesting market maturation and the need for demand-responsive deployment strategies. The favorable ratio enables charging service providers to achieve profitability thresholds more rapidly than in oversupplied markets, supporting sustainable business development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Profit Squeeze from Charger Over-Installation | -2.8% | Urban centers and highway corridors | Short term (≤ 2 years) |

| 2023 EV Sales Dip Undermines Demand Visibility | -1.9% | National, particularly premium EV segments | Medium term (2–4 years) |

| Urban Grid-Congestion Fee Proposals | -1.4% | Seoul metropolitan area | Medium term (2–4 years) |

| Shrinking Per-Charger Subsidy Quantum | -1.1% | National, affecting new installations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Profit Squeeze from Charger Over-Installation

Despite Korea's favorable EV-to-charger ratio, localized over-installation creates profitability challenges for charging service providers, with some operators experiencing decreased usage rates and financial struggles. The rapid deployment of 100,000 annual charger additions has created capacity imbalances in certain locations, particularly highway rest areas and urban centers where multiple operators compete. PlugLink's ability to achieve profitability in 2024 despite market stagnation demonstrates the importance of operational efficiency and strategic site selection. The introduction of occupancy fees by operators like Daeyoung Chaevi, charging KRW 100 per minute after 10 minutes post-charging, represents attempts to optimize utilization and revenue per charger. Market consolidation through acquisitions like PlugLink's purchase of Hanwha's charging business reflects efforts to achieve economies of scale and reduce competitive pressure.

2023 EV Sales Dip Undermines Demand Visibility

Korea's EV penetration rate declined from 10% to 9% in 2023, creating uncertainty for charging service providers' capacity planning and investment decisions. The sales decline, attributed to rising charging prices and reduced subsidies, challenges the predictable demand growth assumptions underlying charging infrastructure investments. Major battery manufacturers SK On, LG Energy Solution, and Samsung SDI reported significant sales declines, with SK On experiencing a 51% revenue drop to KRW 6.27 trillion (USD 4.33 billion). This upstream supply chain stress signals potential continued EV market volatility. However, government commitments to achieve 4.2 million EVs by 2030 and expand charging infrastructure to 1.2 million points provide long-term demand anchors for service providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charger Type: DC Dominance Drives Service Economics

DC Chargers captured 61.23% market share in 2024, reflecting their superior revenue generation potential and alignment with Korea's ultra-fast charging infrastructure priorities. The 28.42% CAGR for DC Chargers through 2030 stems from their ability to serve high-turnover applications and command premium pricing for rapid charging services. While representing the remaining 38.77% share, AC Chargers serve primarily workplace and residential applications where longer dwell times enable different service models. The DC segment's dominance reflects Korea's strategic focus on public and semi-public charging infrastructure rather than home charging solutions, driven by the country's apartment-dominant housing structure.

SK Signet's development of 80kWh charging solutions capable of full vehicle charging in 12 minutes exemplifies the technological advancement driving DC charger adoption. LS Cable & Systems' mass production of Korea's first liquid-cooled hyper-charging cables addresses thermal management challenges in high-power DC applications, enabling chargers exceeding 400kW with twice the charging speed of air-cooled alternatives. The technological evolution toward megawatt-class charging systems positions DC infrastructure as the foundation for heavy-duty fleet electrification, creating new service opportunities beyond passenger vehicle applications.

By Power Output: Ultra-Fast Charging Reshapes Service Models

Ultra-fast chargers exceeding 150 kW demonstrate the highest growth trajectory at 37.01% CAGR, driven by their ability to reduce charging session times and increase station throughput. Fast chargers (50-150 kW) maintain the largest 2024 market share at 47.54%, representing the current sweet spot between charging speed and infrastructure cost. Level 2 chargers (22-50 kW) and Level 1/AC systems (less than 22 kW) complement workplace and residential applications where extended dwell times enable different economic models. The power output segmentation reflects the evolution from convenience charging to rapid refueling paradigms that mirror traditional gasoline station experiences.

Hyundai's development of 350kW ultra-fast chargers through Hyundai Kefico Corp. represents automaker integration into the charging infrastructure, creating vertically integrated service ecosystems. The Hyundai EV Station Gangdong features eight 350kW ultra-fast chargers, enabling vehicles to charge from 10% to 80% in under 18 minutes, demonstrating the commercial viability of ultra-fast charging services. Hyundai Mobis' plans to mass-produce integrated charging control units (ICCU) by the end of 2025, doubling charging speeds from 11kW to 22kW, illustrate the automotive industry's commitment to charging infrastructure advancement.

By Fleet Service Type: Logistics Sector Drives Predictable Demand

The Delivery and Logistics segment commands 42.08% market share in 2024 and exhibits the highest growth rate at 25.26% CAGR, reflecting corporate electrification mandates and the sector's operational efficiency requirements. Passenger Fleets (Taxi/Ride-hailing) and Company Vehicles and Motor Pools represent complementary segments with distinct charging patterns and service requirements. The logistics sector's dominance creates predictable, high-utilization demand during business hours, enabling charging service providers to optimize capacity planning and pricing strategies. Fleet applications drive demand for specialized services, including depot charging, route optimization, and fleet management integration.

CJ Logistics' commitment to electrify all vehicles under 1 ton by 2030, targeting 37% GHG emission reductions, exemplifies the scale of logistics sector transformation. The company's pioneering liquefied hydrogen transportation service, operating from SK E&S's Incheon plant, capable of producing 90 tons daily, demonstrates diversification across alternative fuel technologies. Korea's K-EV100 campaign enrollment of 56 major corporations creates a pipeline of fleet electrification demand that charging service providers can target with specialized offerings. The logistics sector's operational requirements for rapid charging and high reliability create opportunities for premium service tiers and long-term contract arrangements.

By End-Use: Public Infrastructure Dominates Service Revenue

Public Charging infrastructure captures 64.17% market share in 2024, reflecting Korea's apartment-dominant housing structure and the government's strategic focus on accessible charging networks. The 24.53% CAGR for Public Charging through 2030 demonstrates sustained highway, retail, and urban charging application growth. Semi-public Charging (Workplace/Commercial) represents 35.83% of the market, serving office buildings, shopping centers, and corporate facilities where extended dwell times enable different service models. The end-use segmentation highlights the importance of location strategy and customer experience in charging service provider success.

Seoul's initiative to establish a '5-minute living zone' for convenient EV charging, supporting 400,000 electric vehicles by 2026, demonstrates municipal commitment to public charging accessibility. The city's plan includes various charger types: rapid (100kW), slow (7-11kW), and outlet (3- 3.5kW) installations across residential, commercial, and public facilities. Hyundai and Incheon Airport's trial of AI-powered EV charging robots represents innovation in public charging user experience, potentially reducing operational costs and improving service reliability. The public charging segment's growth trajectory aligns with Korea's urban development patterns and supports the broader transition from private vehicle ownership to mobility-as-a-service models.

Geography Analysis

Seoul and its satellite cities anchor charger density, driven by high EV ownership and local subsidies that cover grid upgrades. The corridor linking Seoul to Busan hosts 350 kW stations, cutting inter-city travel anxiety. Incheon International Airport is a technology test bed, housing AI-guided robots that maneuver charging cables for precise vehicle alignment.

Busan’s port complex, Korea’s largest, pilots megawatt chargers to electrify short-haul drayage trucks. Ulsan’s Hydrogen Green Mobility zone illustrates regional diversification, offering hydrogen and battery charging side by side to meet mixed-fuel fleet needs. Jeju Island, once an EV adoption leader, now tightens charger permits to prevent visual clutter, signaling that future deployment must balance density and aesthetics.

Grid constraints vary by province. KEPCO faces KRW 202.5 trillion in debt, prompting connection queuing and legal disputes by independent power firms. Providers with standby battery storage receive faster approvals, nudging the South Korea EV Charging as a Service market toward integrated energy-plus-storage designs. Compact geography, extensive highways, and strong telecom coverage allow operators to manage networks nationally while tailoring offerings to local traffic patterns.

Mordor Intelligence tracks the ev charging as a service market across other major regions such as Europe, with additional country-level coverage spanning China, India, and United States, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The South Korea EV Charging As A Service market exhibits moderate consolidation with increasing competitive intensity as traditional energy companies, technology firms, and specialized charging operators compete for market share. Korean conglomerates like SK Signet and Hyundai Engineering leverage their resources and strategic locations to dominate the market, while smaller players focus on technological differentiation and specialized services. The competitive landscape reflects a transition from infrastructure deployment to service optimization, with companies investing in AI-driven load balancing, user experience improvements, and integrated mobility solutions. Market consolidation accelerates through strategic acquisitions, as demonstrated by PlugLink's purchase of Hanwha's charging business and SK E&S's acquisition of U.S.-based EverCharge.

White-space opportunities emerge in specialized applications, including megawatt charging for heavy-duty vehicles, wireless charging technology, and integrated energy storage solutions. Witz's development of wired/wireless hybrid chargers showcased at EV Trend Korea 2025 exemplifies charging flexibility and space optimization innovation. The company's technology partnership with KG Mobility demonstrates how smaller players can compete through specialized solutions and strategic alliances. Emerging disruptors include startups like Bionever, selected for Korea Credit Guarantee Fund's 'First Penguin' program, focusing on ISO 15118-based intelligent control charging and AI-based operation platforms. Technology integration becomes a key competitive differentiator, with companies leveraging AI for demand forecasting, dynamic pricing, and grid optimization to improve service economics and customer experience.

South Korea EV Charging As A Service Industry Leaders

-

SK Signet

-

LG CNS

-

Chaevi

-

Korea Electric Power Corp. (KEPCO)

-

GS Caltex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Korea ST Trading signed a business agreement with Chargein to promote token securities (STO) in EV charging infrastructure, linking digital assets with eco-friendly charging network expansion and providing investment opportunities for general investors.

- May 2025: Hyundai Motor and Incheon Airport initiated trials of AI-powered EV charging robots, aiming to enhance the charging experience, automation, and operational efficiency at major transportation hubs.

South Korea EV Charging As A Service Market Report Scope

| AC Chargers (Less than 22 kW) |

| DC Chargers (More than 22 kW) |

| Level 1/AC (Less than 22 kW) |

| Level 2 (22 to 50 kW) |

| Fast (50 to 150 kW) |

| Ultra-fast (More than 150 kW) |

| Company Vehicles and Motor Pools |

| Delivery and Logistics |

| Passenger Fleets (Taxi/Ride-hailing) |

| Semi-public Charging Set-up (Workplace/Commercial) |

| Public Charging Set-up (Highway/Retail) |

| By Charger type | AC Chargers (Less than 22 kW) |

| DC Chargers (More than 22 kW) | |

| By Power Output | Level 1/AC (Less than 22 kW) |

| Level 2 (22 to 50 kW) | |

| Fast (50 to 150 kW) | |

| Ultra-fast (More than 150 kW) | |

| By Fleet Service Type | Company Vehicles and Motor Pools |

| Delivery and Logistics | |

| Passenger Fleets (Taxi/Ride-hailing) | |

| By End-use | Semi-public Charging Set-up (Workplace/Commercial) |

| Public Charging Set-up (Highway/Retail) |

Key Questions Answered in the Report

What is the 2025 value of South Korea’s EV charging-as-a-service sector?

The South Korea EV Charging As A Service market is valued at USD 159.40 million in 2025.

How fast is the sector growing through 2030?

The market expands at a 19.26% CAGR, reaching USD 386.50 million by 2030.

Which charger type leads revenue?

DC chargers held 61.23% market share in 2024, driven by high utilization and ultrafast roll-outs.

Why are logistics fleets important customers?

Delivery and logistics fleets supply 42.08% of 2024 revenue and have the highest 25.26% CAGR because corporate mandates ensure predictable usage.

What restrains near-term profitability?

Over-installation in some corridors reduces session counts, prompting idle-fee policies to protect margins.

Where is public investment focused?

Seoul and major highways receive priority subsidies, ensuring rapid-charger availability within a five-minute drive for most residents.

Page last updated on: