EV Charging As A Service Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

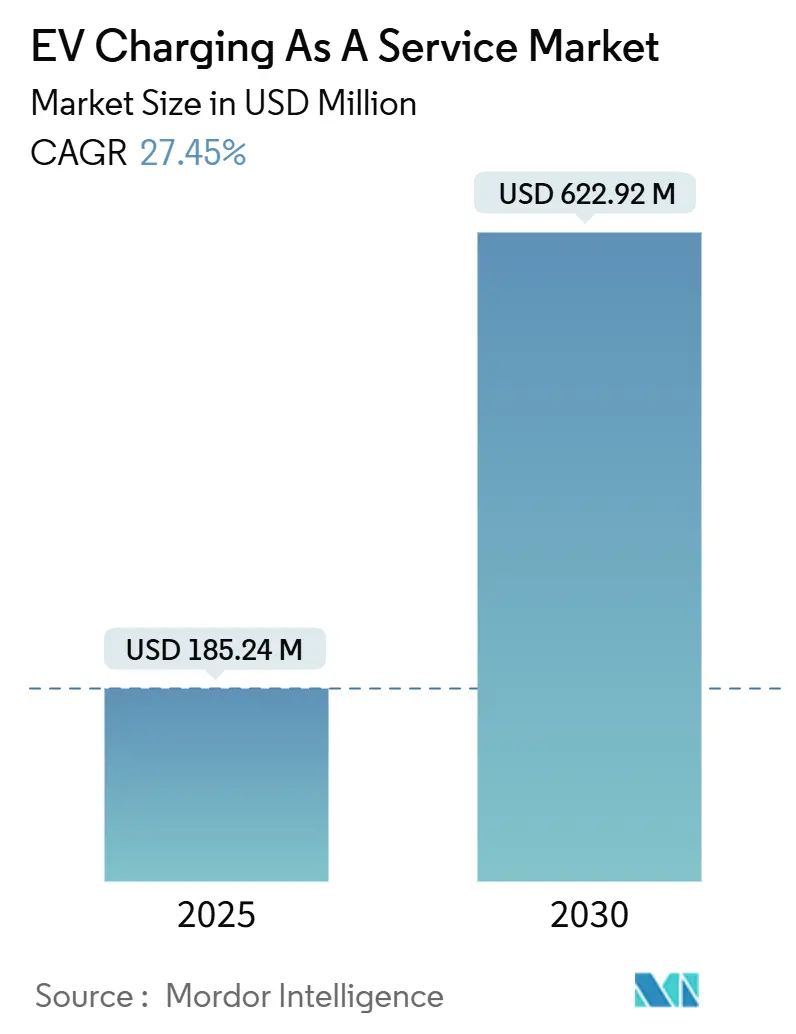

| Market Size (2025) | USD 185.24 Million |

| Market Size (2030) | USD 622.92 Million |

| Growth Rate (2025 - 2030) | 27.45% CAGR |

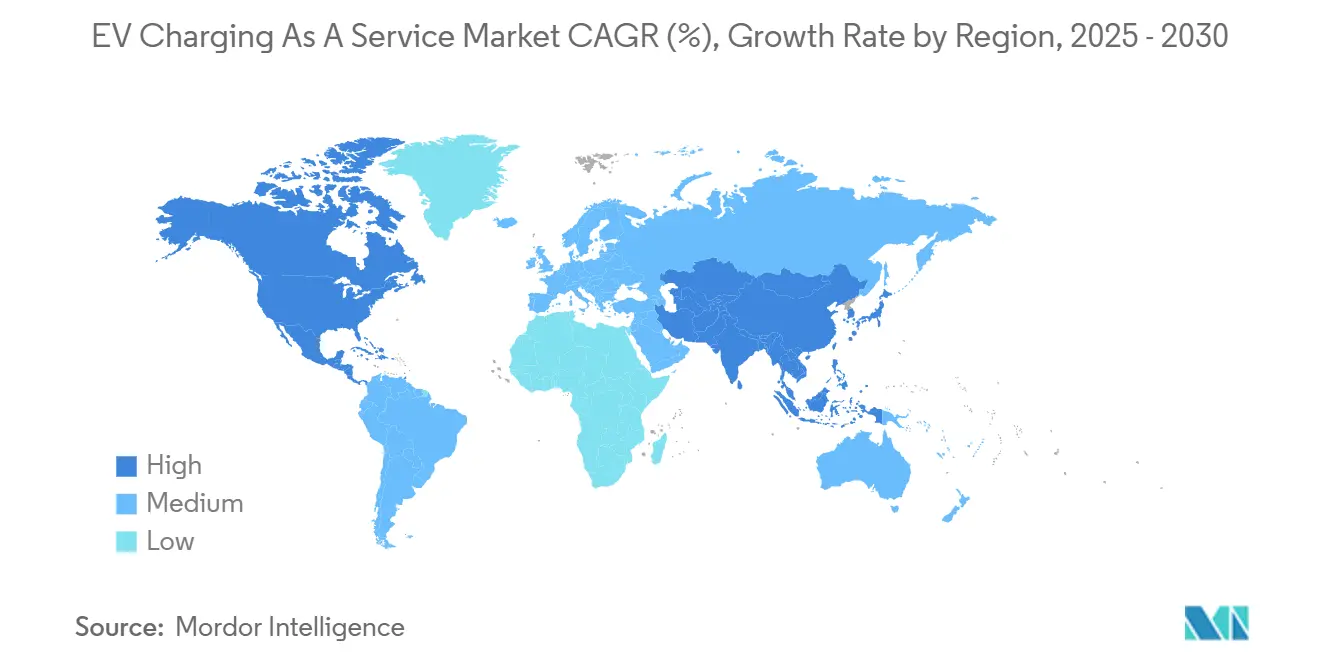

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

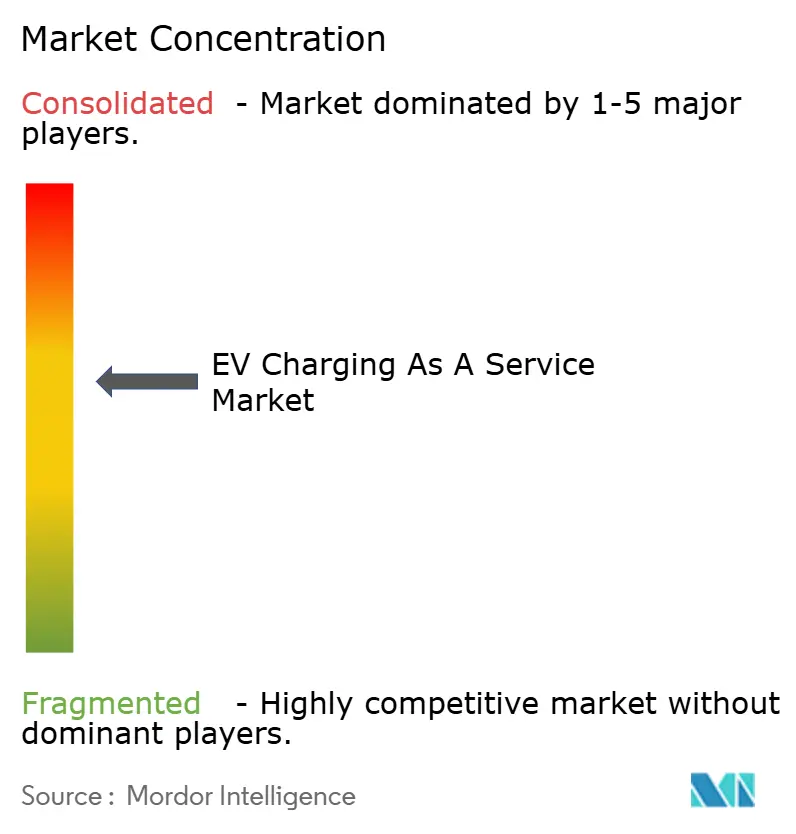

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EV Charging As A Service Market Analysis by Mordor Intelligence

The EV charging as a service market size stood at USD 185.24 million in 2025 and is projected to reach USD 622.92 million by 2030, yielding a 27.45% CAGR that reflects the growing preference for service-based charging models over outright infrastructure ownership. Federal stimulus, subscription financing, and rapid corridor build-outs steadily widen the addressable customer base, while mobile on-demand solutions remove siting constraints for early adopters. Fleet operators cite predictable operating expenses, access to the newest hardware, and risk transfer to service providers as key advantages that accelerate corporate, municipal, and logistics contract signings. At the same time, megawatt-class systems compress dwell times for heavy-duty vehicles, supporting use cases that were previously uneconomical. Consolidation is expected as capital requirements for ultra-fast assets rise, but the EV charging as a service market remains fragmented, creating room for regional specialists and technology disruptors.

Key Report Takeaways

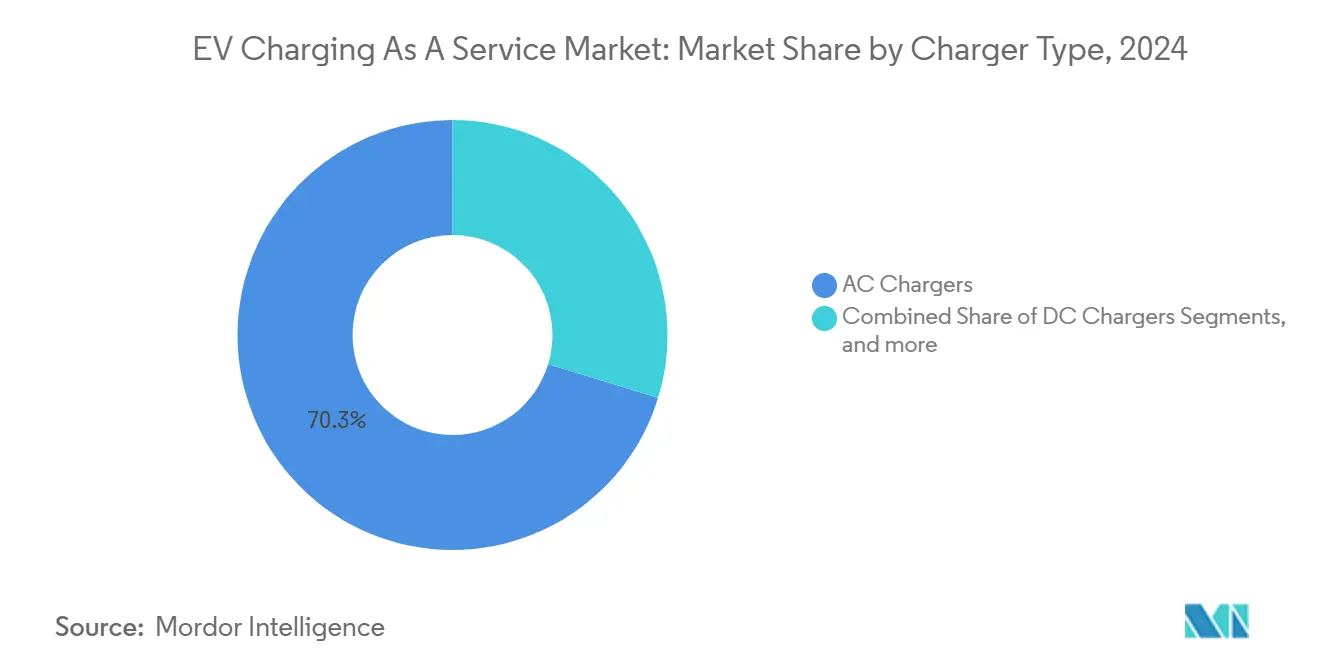

- By charger type, AC Chargers held 70.28% of the EV charging as a service market share in 2024, whereas DC Fast Chargers are projected to advance at a 28.78% CAGR through 2030.

- By fleet service type, company vehicles and motor pools accounted for the largest 29.25% share of the EV charging as a service market in 2024, while delivery and logistics fleets are growing at a market-leading 27.53% CAGR to 2030.

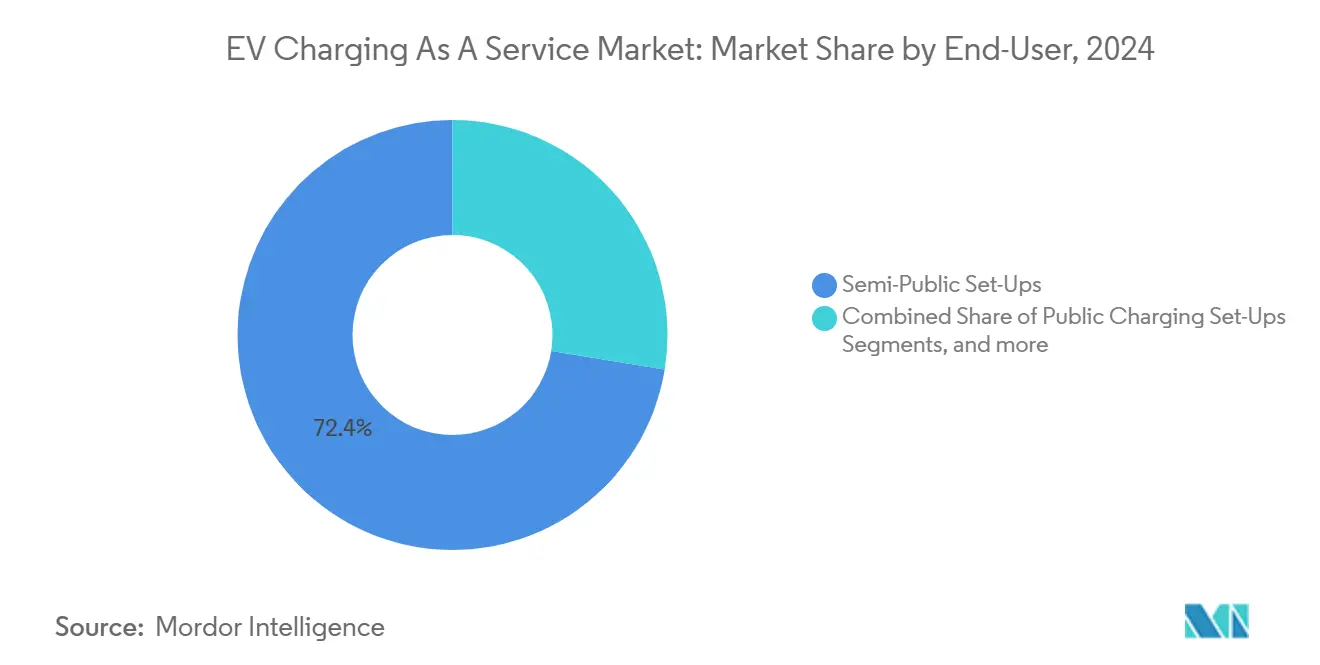

- By end-use, semi-public setups captured 72.43% of the EV charging as a service market size in 2024; mobile on-demand charging records the sharpest 27.82% CAGR through 2030.

- By power output, Level 1 ports dominated, with 79.82% of the EV charging as a service market share in 2024, yet high-power (above 150 kW) systems above 150 kW posted the strongest 28.69% CAGR over the forecast period.

- By geography, North America led with 45.38% of 2024 revenue in the EV charging as a service market, whereas Asia-Pacific is projected to expand at the highest 29.23% CAGR through 2030.

Global EV Charging As A Service Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet Electrification Pledges | +5.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Public-Charging Subsidies And Mandates | +4.2% | Global, with highest impact in North America and EU | Medium term (2-4 years) |

| DC Fast-Corridor Expansion | +3.8% | North America and EU primary, Asia-Pacific emerging | Medium term (2-4 years) |

| Subscription CaaS models | +3.4% | Global, particularly in developed markets | Medium term (2-4 years) |

| Mobile On-Demand Charging | +2.9% | Global, with early adoption in urban centers | Short term (≤ 2 years) |

| Micro-Grid + Storage Savings | +2.7% | Global, with focus on high-demand corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Fleet-Electrification Commitments

More than 120 companies in the EV100 initiative have pledged to transition to vehicles by 2030, driving predictable multi-year demand for charging subscriptions[1]“EV100 Progress and Insights Report 2025,”, The Climate Group, theclimategroup.org. In India, Zomato and Flipkart are set to roll out a significant fleet of electric two- and three-wheelers, highlighting the demand for tailored CaaS (Charging-as-a-Service) solutions that align with regional vehicle types and living habits. This initiative reflects the growing emphasis on sustainable transportation and the need for infrastructure supporting electric vehicles' unique requirements in the Indian market. By focusing on differentiated offerings, these companies aim to address challenges such as charging accessibility, vehicle compatibility, and operational efficiency, which are critical for the widespread adoption of electric mobility in the country.

Government Subsidies and Mandates For Public Charging Roll-Outs

Over the next five years, the National Electric Vehicle Infrastructure (NEVI) program will establish a nationwide fast-charging network, supporting EV adoption. These investments provide fleets with reliable charging infrastructure and service providers with stable, multiyear revenue through site leases and maintenance contracts. This initiative aims to enhance EV charging accessibility and convenience across the United States.

Similarly, Europe’s Alternative Fuels Infrastructure Regulation sets mandatory density targets to attract private investment and build a comprehensive charging network, ensuring reliable access for EV users. The regulation accelerates charging infrastructure deployment by anchoring private capital, advancing sustainable transportation. State programs like California’s Clean Transportation Program further support these efforts by funding workforce training to improve charging assets' efficiency and uptime, ensuring reliability while creating job opportunities and fostering EV ecosystem growth.

Subscription-Based CaaS Financing Models

Under typical four-to-seven-year agreements, providers absorb all installation, software, and O&M costs in exchange for a monthly service fee, eliminating upfront capital for fleet managers[2]“CaaS Financing Models Explained,”, Advanced Energy, advancedenergy.org. Volkswagen’s consolidation of its LOGPAY and Elli units into Elli Mobility GmbH shows how carmakers bundle payments, energy, and data services to lock in downstream revenue. Cooperative purchasing contracts used by United States municipalities streamline procurement and aggregate demand, giving the EV charging as a service market scalable, repeatable deal structures.

Mobile On-Demand Charging Services Gain Traction

Investor confidence in flexible models shines through with SparkCharge's latest investment. This funding propels the growth of its mobile fleet-support platform, which is designed to deliver power to vehicles, not vice versa. Such services find favor in bustling cities, where challenges like permitting, limited space, and grid upgrades hinder fixed installations. The pay-as-you-go (PAYG) pricing model allows operators to navigate the interim period before establishing permanent infrastructure. Meanwhile, premium convenience fees bolster the margins for providers. Additionally, battery-swap features minimize downtime for Asia's prevalent two- and three-wheel fleets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fast-Charger And Grid Cap-Ex | -3.8% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Plug-Standard Interoperability Gaps | -2.9% | North America primary, global implications | Short term (≤ 2 years) |

| Certified Technician Shortage | -2.1% | Global, acute in rural and emerging markets | Long term (≥ 4 years) |

| Peak-Tariff Volatility For CaaS Operators | -1.7% | Global, highest impact in deregulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex for Fast Chargers and Grid Upgrades

In cost-sensitive regions, the roll-out of single high-power sites is often delayed due to the need for significant investments in equipment and utility upgrades. These delays can hinder the adoption of advanced charging infrastructure, which is critical for supporting the growing demand for electric vehicles. By 2030, Europe will require a substantial increase in public and depot plugs to meet the truck-charging needs driven by the transition to electric fleets. However, lengthy approval processes and high interconnection fees create significant challenges, further complicating the deployment schedules. In California, the re-emergence of utility demand charges highlights the pressing need for effective load management and energy storage solutions. These measures are essential to ensure kilowatt-hour costs remain predictable and to support the economic viability of high-power charging infrastructure.

Interoperability Gaps (CCS vs NACS vs CHAdeMO)

Hardware fragmentation forces fleets to stock adapters or dual-standard dispensers. SAE’s publication of the J3400 NACS connector and Tesla’s decision to open Superchargers to others are positive steps, yet the transition period raises inventory and maintenance complexity [3]“J3400 and J3271 Standards Publication,”, SAE International, sae.org. ChargePoint’s “Omni Port” strategy seeks to future-proof sites, but procurement decisions remain fraught until one format dominates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charger Type: AC Dominance Faces High-Power Disruption

AC chargers retained a 70.28% share of the EV charging as a service market in 2024, anchored by inexpensive Level 1 units suited to overnight depot dwell times. Yet the EV charging as a service market size for DC fast solutions is expanding at a 28.78% CAGR through 2030, driven by logistics fleets that measure downtime in minutes, not hours. Static wireless pads and automated underbody couplers start appearing in transit depots, easing driver workflows and enabling nearly hands-free operations.

The EV charging as a service market is witnessing prototype megawatt dispensers such as ABB’s MCS1200 that can refuel a Class 8 truck from 20% to 80% in roughly 30 minutes. As connector standards stabilize, many depots wire for future 1 MW cabinets even when installing lower-rated posts, signaling confidence in long-term duty-cycle electrification.

By Fleet Service Type: Logistics Surge Challenges Corporate Dominance

Company vehicles and motor pools captured a 29.25% share of the EV charging as a service market in 2024 because sustainability officers could immediately leverage workplace parking to host chargers and secure internal utilization. However, the EV charging as a service market share held by delivery and logistics fleets will climb rapidly as same-day commerce explodes in urban zones, growing at a CAGR of 27.53% to 2030. Contracts increasingly bundle energy management dashboards that allocate costs by driver or route—features prized by e-commerce operators seeking transparency.

Municipal bus and refuse fleets add steady baseline demand through multi-year procurements tied to budget cycles. Asia’s two-wheeler delivery giants adopt battery-swap pods, showing that service models differ by vehicle class. Yet, all fall under the expanding umbrella of the EV charging as a service market.

By End-Use: Semi-Public Setups Drive Current Demand

Semi-public setups delivered 72.43% of the share of the EV charging as a service market in 2024, because access can be restricted to employees or paying customers, keeping utilization high and vandalism low. Still, mobile on-demand charging booked the fastest 27.82% CAGR, reflecting the draw of location-agnostic refueling for transition fleets.

While public stations are vital for corridor coverage, their utilization often lags in the initial years, posing risks for operators focused solely on them. These stations are crucial for supporting long-haul routes and ensuring widespread accessibility. Still, the slower adoption rates in the early stages can lead to underutilization, impacting profitability and operational efficiency.

In contrast, parcel carriers increasingly prefer depot-only models, allowing them to cycle trucks through a single location each night. This approach simplifies load management and facilitates the seamless integration of renewable energy sources, such as solar or wind power, into their operations. Additionally, depot-only models reduce dependency on public infrastructure, offering greater control over charging schedules and operational costs.

By Power Output: High-Power Systems Reshape Fleet Operations

Level 1 ports, cheap and grid-friendly, made up 79.82% of the share of the EV charging as a service market in 2024, a figure expected to decline as duty cycles tighten. High-power dispensers above 150 kW log the fastest 28.69% CAGR through 2030, reflecting how megawatt charging slashes dwell times for heavy freight. The EV charging as a service market size linked to 50–150 kW “fast” cabinets remains strong for regional delivery vans that need midday top-ups without full megawatt rates.

Hardware makers are designing cabinets with swappable power modules, enabling operators to start at 300 kW and scale up to 1 MW as vehicle battery technologies advance. This modular approach preserves capital by allowing incremental investments and ensures the site remains adaptable to future technological developments. By incorporating such flexibility, operators can efficiently meet evolving energy demands without requiring complete infrastructure overhauls.

Geography Analysis

North America retained a 45.38% share of the EV charging as a service market in 2024, buoyed by the Infrastructure Investment and Jobs Act, Inflation Reduction Act credits, and private collaborations such as Tesla’s opening of its Superchargers to other automakers, projected to invest in annual network fees by 2030. Corridor coverage now meets the 50-mile fast-charger spacing target on most priority highways, reducing range risk for inter-state freight and boosting transaction volumes within the EV charging as a service market.

Asia-Pacific is the fastest-growing region at a 29.23% CAGR during the forecast period, propelled by manufacturing cost advantages, national electrification mandates, and the sheer scale of two- and three-wheeler fleets. China hosts most of the world’s public chargers, giving service vendors massive load aggregation potential. Indian firms like Zomato spearhead corporate adoption of lightweight EVs that rely on compact depot chargers or battery-swap kiosks. International financiers such as HSBC have begun underwriting fleet conversions in Southeast Asia, indicating rising confidence in cash-flow visibility for the EV charging as a service market.

Europe combines mature infrastructure with ambitious targets, including Germany’s plan to enhance public transport by 2030 significantly. The Alternative Fuels Infrastructure Regulation sets uniform minimum coverage, and heavy-duty joint ventures such as Milence plan 1,700 high-power truck sites, underscoring a shift toward pan-European roaming and billing standards. Although economic headwinds may temper near-term upgrades, cross-border e-commerce keeps utilization high at established hubs.

Mordor Intelligence provides coverage of the ev charging as a service market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China, India, United States, and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

Regional fragmentation persists, yet several trends point toward consolidation. Energy majors Shell and BP are tying asset investments to power-retail portfolios, while carmakers such as Volkswagen fold mobility payments into captive charging brands to retain lifecycle revenue. ChargePoint’s “Omni Port” illustrates differentiation via hardware that accepts all mainstream connectors, mitigating transition risk for fleets.

Technology leadership is increasingly measured in peak kilowatts; ABB’s MCS1200 and Siemens’ 1 MW prototype validate commercial readiness for Class 8 trucking.

Since the top players still account for a significant portion of global revenue, partnership announcements often involve cross-licensing software or co-developing corridors, signaling a market where collaboration offsets capital intensity. Investors expect scale and uptime to be the deciding factors as contracts renew.

EV Charging As A Service Industry Leaders

ChargePoint Holdings Inc.

Shell Recharge Solutions

Tesla Inc.

ABB Ltd.

BP Pulse (Chargemaster Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SparkCharge secured USD 30.5 million to expand its mobile charging fleets. The company aims to enhance its operational capacity and cater to the growing demand for adaptable refueling services. The funding will enable the company to scale its infrastructure, improve service efficiency, and meet the increasing needs of electric vehicle users seeking convenient, flexible charging solutions.

- April 2025: ABB E-mobility unveiled the MCS1200 megawatt charger, A200/300 all-in-one units, and the ChargeDock dispenser, broadening solutions for light- and heavy-duty fleets.

- January 2025: Volkswagen merged LOGPAY Transport Services and Elli assets, forming Elli Mobility GmbH to unify charging and payment services across Europe.

Global EV Charging As A Service Market Report Scope

| AC Chargers |

| DC Fast Chargers |

| Wireless / Inductive Chargers |

| Company Vehicles & Motor Pools |

| Delivery & Logistics Fleets |

| Passenger Fleets (Ride-hail, Rental) |

| Municipal & Transit Fleets |

| Semi-Public Set-Ups (Workplace, Retail) |

| Public Charging Set-Ups (Highway, Urban) |

| Depot / Fleet-Hub Charging |

| Mobile On-Demand Charging |

| Level 1 / AC (Below 22 kW) |

| Level 2 (22 - 50 kW) |

| Fast (50 - 150 kW) |

| High-Power (Above 150 kW) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Sweden | |

| Denmark | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Morocco | |

| Rest of Middle East & Africa |

| By Charger Type | AC Chargers | |

| DC Fast Chargers | ||

| Wireless / Inductive Chargers | ||

| By Fleet Service Type | Company Vehicles & Motor Pools | |

| Delivery & Logistics Fleets | ||

| Passenger Fleets (Ride-hail, Rental) | ||

| Municipal & Transit Fleets | ||

| By End-Use | Semi-Public Set-Ups (Workplace, Retail) | |

| Public Charging Set-Ups (Highway, Urban) | ||

| Depot / Fleet-Hub Charging | ||

| Mobile On-Demand Charging | ||

| By Power Output | Level 1 / AC (Below 22 kW) | |

| Level 2 (22 - 50 kW) | ||

| Fast (50 - 150 kW) | ||

| High-Power (Above 150 kW) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Norway | ||

| Sweden | ||

| Denmark | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large is the EV charging as a service market in 2025?

It is valued at USD 185.24 million and is projected to grow to USD 622.92 million by 2030.

Which fleet segment is expanding the quickest?

Delivery and logistics fleets are growing at a 27.53% CAGR through 2030, the fastest among all segments.

What power category is gaining share the fastest?

Chargers rated above 150 kW hold the highest 28.69% CAGR as operators seek shorter dwell times

Why does North America lead in revenue?

Federal funding, corporate sustainability mandates, and corridor fast-charging coverage together delivered 45.38% of 2024 revenue in the region.

What role do subscription models play?

Four- to seven-year contracts shift installation, maintenance, and upgrade costs to providers, giving fleets predictable monthly expenses.

How are high peak tariffs mitigated?

Pairing chargers with on-site storage and smart energy management smooths load profiles and shields operators from demand charges

Page last updated on: