United States Enteral Nutrition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

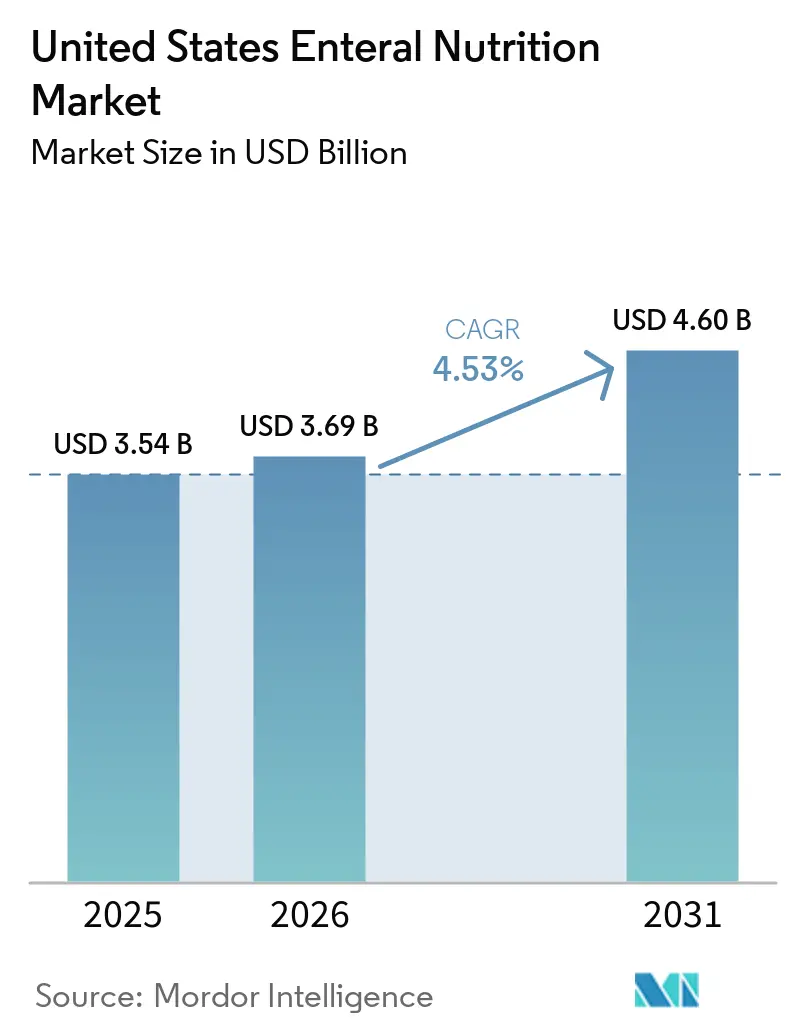

| Base Year Market Size (2025) | USD 3.54 Billion |

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 4.60 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Enteral Nutrition Market Analysis by Mordor Intelligence

The United States Enteral Nutrition Market size was valued at USD 3.54 billion in 2025 and is estimated to grow from USD 3.69 billion in 2026 to reach USD 4.60 billion by 2031, at a CAGR of 4.53% during the forecast period (2026-2031).

Growth in the United States enteral nutrition market rests on two durable demand sources: a rapidly aging patient base with higher dysphagia and multi-morbidity rates, and a care system that is moving nutrition support from hospitals into home and long-term care settings. The demand base remains resilient because enteral nutrition is tied to clinical need, so usage patterns are less exposed to broad consumer spending cycles than adjacent nutrition categories. The United States enteral nutrition market is also being reshaped by the normalization of home enteral nutrition as a standard post-acute pathway, which is reducing the relative weight of inpatient use while expanding the treated patient pool through discharge continuity. Competition in the United States enteral nutrition market remains moderately high because Abbott Nutrition, Nestlé Health Science, Danone/Nutricia, and Fresenius Kabi USA still control most institutional formulary positions, yet Danone’s 2025 deals for Functional Formularies and a majority stake in Kate Farms have materially changed the strategic balance. Product discontinuations announced by Abbott in March 2025 and Nestlé in February 2025 have also created selective white space, which is allowing mid-tier suppliers to pursue new hospital and homecare placements.

Key Report Takeaways

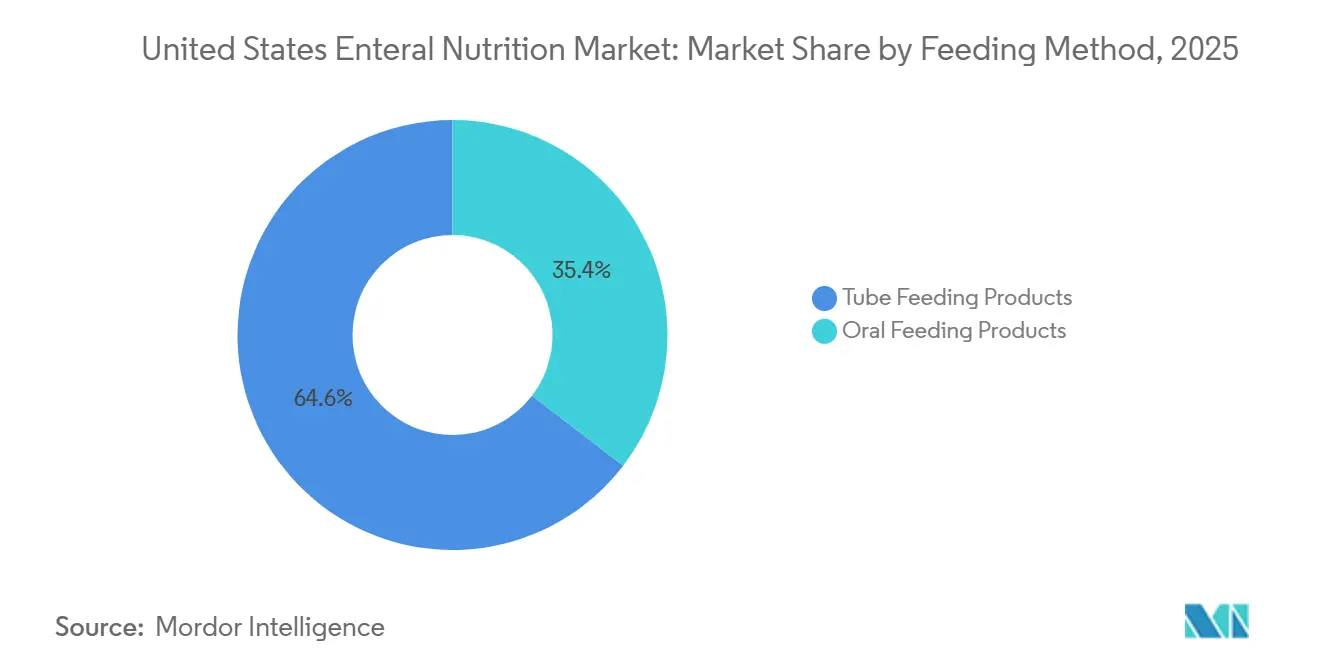

- By feeding method, tube feeding products led with 64.57% revenue share in 2025, while oral feeding products are projected to expand at a 5.46% CAGR through 2031.

- By formula type, standard/polymeric formulas held 56.81% revenue share in 2025, while disease-specific formulas are forecast to grow at a 5.27% CAGR through 2031.

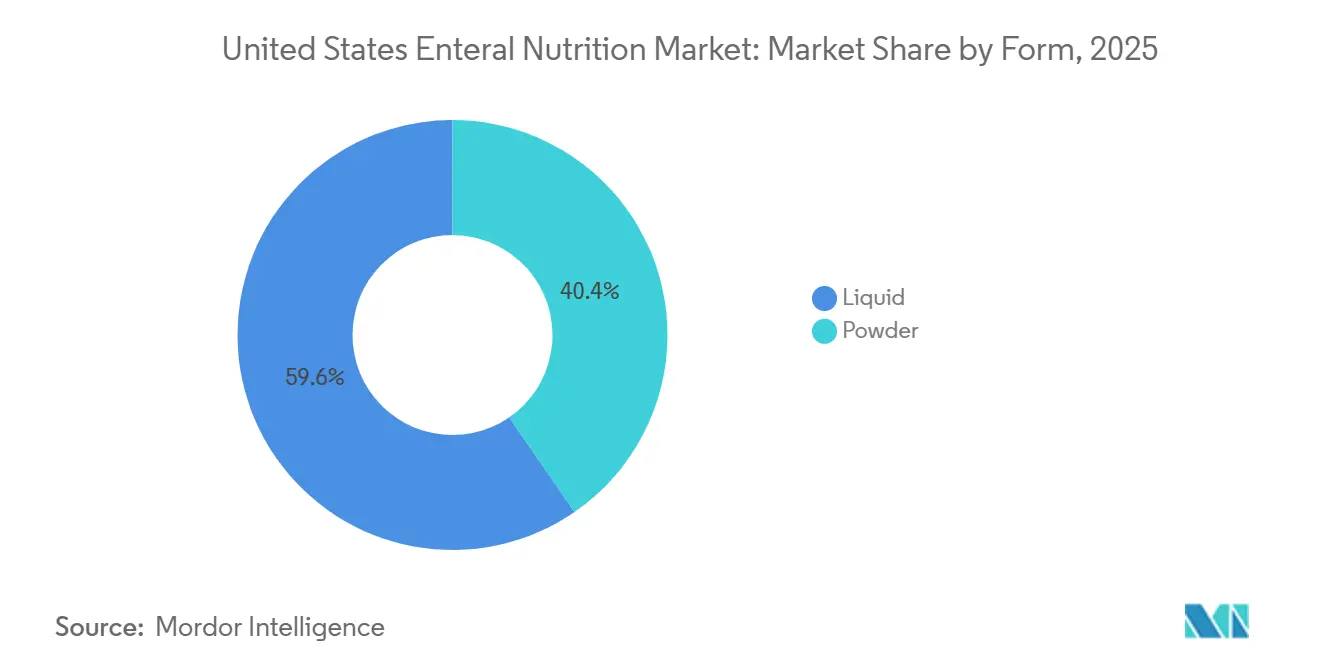

- By form, liquid formulas accounted for 59.57% revenue share in 2025 and are also projected to record the fastest growth at a 5.88% CAGR through 2031.

- By age group, adults represented 52.71% revenue share in 2025, while pediatrics is projected to advance at a 6.65% CAGR through 2031.

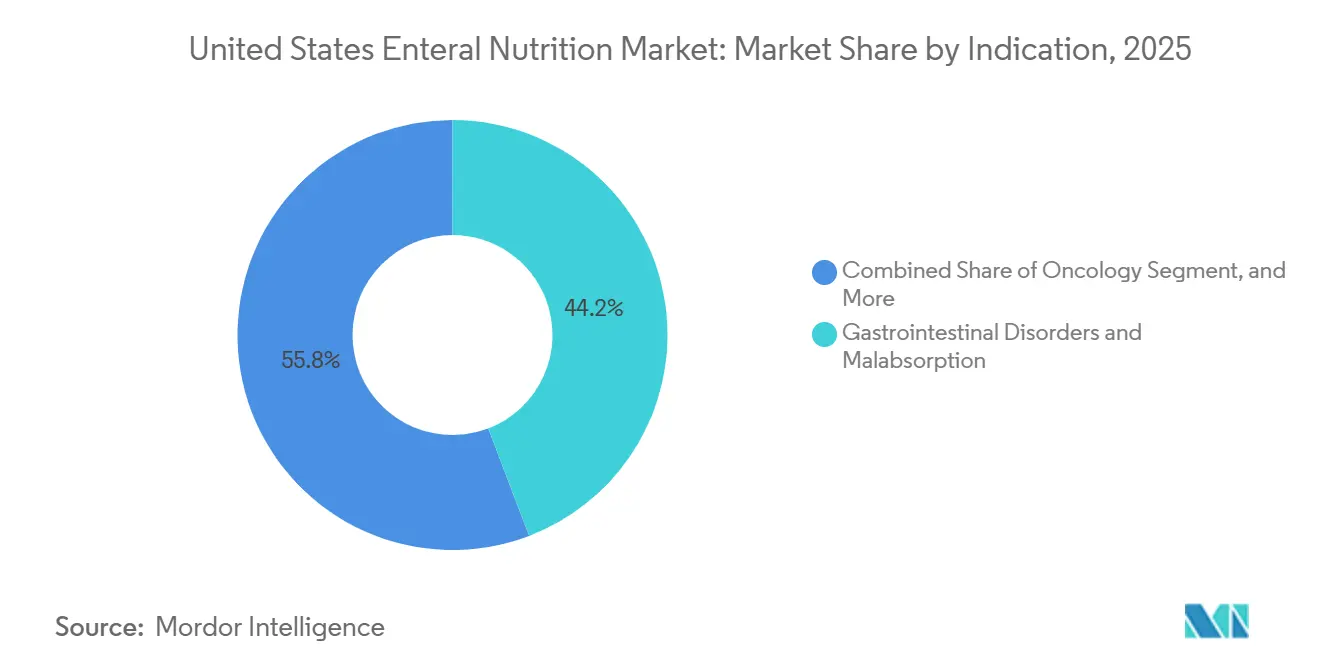

- By indication, gastrointestinal disorders and malabsorption held 44.21% revenue share in 2025, while oncology is forecast to grow at a 6.0% CAGR through 2031.

- By end user, hospitals accounted for 56.12% revenue share in 2025, while home care settings are projected to expand at a 5.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Enteral Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-Related Dysphagia and Chronic Disease Burden | +1.2% | US National, concentrated in Southeast and Sun Belt states | Long term (≥ 4 years) |

| Home-Enteral Care Expansion Across Post-Acute Pathways | +0.9% | US National, with accelerated adoption in Medicare Advantage markets | Medium term (2-4 years) |

| Disease-Specific Formula Adoption in Diabetes, Renal, and GI Care | +0.8% | US National, with early concentration in outpatient clinics and integrated health systems | Medium term (2-4 years) |

| Real-Food and Blenderized Tube-Feeding Innovation | +0.5% | US National, with market leadership in pediatric specialty centers and homecare | Short term (≤ 2 years) |

| ENFit-Compatible Convenience Formats Improving Home Adherence | +0.4% | US National | Short term (≤ 2 years) |

| Pediatric Elemental and Metabolic Nutrition Demand Expansion | +0.4% | US National, concentrated in tertiary pediatric centers and metabolic specialty clinics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging-Related Dysphagia and Chronic Disease Burden

The aging of the U.S. population continues to create a durable demand floor for the United States enteral nutrition market through the end of the decade. This demand is not driven by age alone, because dysphagia often overlaps with dementia, stroke, Parkinson’s disease, chronic kidney disease, and head and neck cancer, which raises both treatment complexity and formula intensity. The U.S. Census Bureau projects that 73 million Americans will be age 65 or older by 2030, and that scale materially enlarges the patient base that can require oral thickened support, specialized oral nutrition, or tube feeding therapy.[1]United States Census Bureau, “Population Projections,” U.S. Census Bureau, census.gov The United States enteral nutrition market, therefore, benefits not only from higher patient numbers but also from a richer case mix where renal, oncology, and neurologic needs push demand toward more specialized products. That pattern helps explain why disease-specific formulas are expanding faster than broad polymeric products even while the standard base remains large.

Home-Enteral Care Expansion Across Post-Acute Pathways

The center of gravity in the United States enteral nutrition market is moving from inpatient use toward the home as hospitals seek lower-cost recovery pathways and shorter lengths of stay. CMS reimbursement codes for eligible enteral products and supplies give providers a structured payment route, which makes home enteral nutrition easier to operationalize after discharge.[2]Centers for Medicare & Medicaid Services, “National Coverage Determination, Enteral and Parenteral Nutritional Therapy (NCD 180.2),” Medicare Coverage Database, cms.gov Medicare Advantage growth is also raising plan-level formulary gatekeeping, so companies that win preferred supplier status can secure lasting distribution advantages across discharge networks. Portable pump technology and continued ENFit-compatible system adoption have narrowed the usability gap between hospital delivery and home administration, which lowers the barrier to starting patients on home regimens. As the homecare channel expands, spending also shifts toward ready-to-hang liquids and closed systems that reduce the handling burden for caregivers.

Disease-Specific Formula Adoption in Diabetes, Renal, and GI Care

Disease-specific formulas are taking share from generic products because clinicians now have a stronger evidence base for matching nutrition to metabolic and organ-specific needs in diabetes, renal disease, and gastrointestinal care. A 2025 paper in Nutrients found that low-glycemic enteral formulas improved postprandial glucose control versus standard polymeric alternatives in hospitalized patients with diabetes, which supports the clinical case for targeted products.[3]F. Bozzetti et al., “Diabetes-Specific Enteral Nutrition Formulas, Clinical Evidence Review,” Nutrients, mdpi.com The CDC reported that 38.4 million Americans were living with diabetes in 2024, which leaves a very large eligible pool for glycemic-optimized enteral support across hospitals, outpatient settings, and eventually the home. Abbott Nutrition’s Suplena with CARBSTEADY and Nestlé’s NOVASOURCE Renal show how leading suppliers are structuring renal offerings around both protein and glycemic needs rather than simple calorie replacement. The same migration is visible in gastrointestinal care, where malabsorption, short bowel syndrome, and inflammatory bowel disease keep demand elevated for peptide-based and elemental nutrition that standard polymeric formulas cannot reliably replace.

Real-Food and Blenderized Tube-Feeding Innovation

Commercial real-food tube feeding has become a meaningful growth layer in the United States enteral nutrition market because it now competes on both clinical and caregiver preference grounds. ASPEN’s 2024 Blenderized Tube Feedings Practice Recommendations gave health systems a clearer framework for risk management and implementation, which reduced one of the main institutional barriers to adoption. A 2026 prospective study reported 0% emesis in blenderized tube feeding recipients compared with 41.1% in the semi-elemental formula group, which gives the category a stronger clinical footing as well as a practical adherence benefit. Families often respond better to products with recognizable food-origin ingredients, and that response can improve adherence, reduce waste, and support more consistent calorie delivery in the home. Danone strengthened its position in this part of the United States enteral nutrition market through its 2025 Functional Formularies acquisition and its majority investment in Kate Farms, which together expanded its reach across both medical and consumer-facing pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement and Documentation Barriers for Home Enteral Nutrition | -0.8% | US National, disproportionately affecting independent HEN suppliers | Short term (≤ 2 years) |

| High Affordability Pressure on Specialized Formulas | -0.5% | US National, with amplified impact in lower-income and rural communities | Medium term (2-4 years) |

| Supplier Attrition and Access Gaps in HEN Distribution | -0.4% | US National, with significant rural access disparity | Short term (≤ 2 years) |

| Product Shortages and SKU Discontinuations in Critical Formulas | -0.3% | US National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement and Documentation Barriers for Home Enteral Nutrition

Reimbursement remains the most important structural constraint on the United States enteral nutrition market because administrative friction directly affects supplier willingness to serve home patients. CMS reported a 23.8% improper payment rate for enteral nutrition suppliers in its 2024 compliance review, and insufficient documentation accounted for 48.8% of denials, which shows how much revenue can be exposed even when clinical need is real. CMS LCD L38955 requires detailed and current proof of medical necessity, and that burden is harder for smaller homecare providers to manage without dedicated compliance teams. As those costs rise, independent distributors face tighter margins, and some exit the space, which narrows the supply base even as patient need grows. The result is a clear mismatch in the United States enteral nutrition market, because a broader eligible population is being served through a reimbursement channel that still favors scale and administrative depth.

High Affordability Pressure on Specialized Formulas

Affordability remains another meaningful brake on the United States enteral nutrition market because specialized formulas can be hard to sustain for uninsured, underinsured, or Medicaid-reliant patients. Elemental and amino acid-based products are among the highest-cost therapies in the category, and coverage has historically varied widely across states, even when clinical need is clear. Louisiana Healthcare Connections expanded Medicaid coverage for amino acid-based elemental formulas from January 1, 2026, and the policy now includes eosinophilic disorders, FPIES, multiple food protein allergies, and severe gastrointestinal malabsorption. That move shows how state action can open new demand, but it also shows how uneven access remains across the country when federal coverage is not standardized. Until broader coverage or stronger manufacturer assistance programs are in place, many patients will continue to cycle back to lower-cost formulas that may not fit their clinical needs as well.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feeding Method: Oral Feeding Momentum Challenges Tube Dominance

Tube Feeding Products accounted for 64.57% of the United States enteral nutrition market share in 2025, which confirms that tube-based delivery still anchors demand across acute care and institutional settings. This position reflects persistent use in intensive care, neurology, oncology, and post-surgical recovery, where the oral route is often unavailable or insufficient for maintaining nutritional status. The United States enteral nutrition market still depends on nasogastric, nasoduodenal, and PEG-based regimens because they remain the standard of care when aspiration risk, swallowing impairment, or severe weakness limit oral intake. Hospitals and long-term care providers also value tube feeding because it provides predictable calorie and protein delivery in high-acuity patients.

Oral Feeding Products, however, are projected to grow at a 5.46% CAGR through 2031, which gives this segment the growth premium within the broader United States enteral nutrition market. Post-discharge nutrition protocols are using more oral nutritional supplements for patients leaving acute care, especially when they can transition from full tube dependence to partial or complete oral support. Managed care models are also encouraging earlier discharge, and that favors portable sip-feed formats that fit community recovery better than prolonged inpatient tube feeding. This does not weaken the clinical importance of tube products, but it does shift incremental demand toward oral supplementation as patient recovery moves outside the hospital. The result is a stable base in tube feeding and a faster expansion path for oral products, which mirrors the broader channel shift from institutional care to home and outpatient support.

By Formula Type: Disease-Specific Formulas Outpace the Polymeric Base

Standard/Polymeric Formulas accounted for 56.81% of the United States enteral nutrition market size in 2025, while Disease-Specific Formulas are projected to expand at a 5.27% CAGR through 2031. Polymeric products still dominate because they are broadly applicable across age groups, indications, and care settings, and they remain the cost-effective workhorse of many hospital formularies. The United States enteral nutrition market retains this large polymeric base because standard formulas are easier to deploy across mixed patient populations where highly specialized composition is not required. That broad role helps preserve volume leadership even as newer categories take a larger share of incremental growth.

Disease-specific formulas are gaining ground because diabetes, renal disease, oncology, and gastrointestinal care increasingly demand nutrition profiles designed for defined metabolic or organ-related needs. Fresenius Kabi’s 2026 launch of Renalive HP shows how suppliers are targeting clinical gaps left by competitor portfolio reductions and pushing deeper into renal-specific nutrition. Peptide-based and semi-elemental formulas remain essential for patients with impaired digestion or absorption, while elemental and amino acid-based products serve the highest-complexity cases such as eosinophilic gastrointestinal disorders and inborn errors of metabolism. A 2025 review in Nutrients also supported the expanding role of amino acid-based formulas in pediatric eosinophilic esophagitis and related food protein-mediated disorders, which strengthens the reimbursement case for these products in state Medicaid programs. The United States enteral nutrition industry, therefore, continues to rely on polymeric formulas for scale, while specialized products carry the higher-value growth layer.

By Form: Liquid Format Advantages Reinforce Market Leadership

Liquid formulas accounted for 59.57% of the United States enteral nutrition market size in 2025 and are projected to advance at a 5.88% CAGR through 2031. That combination of leading share and fastest growth shows how strongly the United States enteral nutrition market favors formats that reduce preparation burden and support safer administration. Ready-to-use liquids lower the risk of reconstitution errors and reduce contamination concerns, which matters in intensive care, neonatal care, and immunocompromised patient groups. These practical benefits have made liquid products the preferred choice in many hospitals and an increasingly strong option in homecare.

The home enteral channel reinforces this position because caregivers can manage closed-system liquids more easily than powders in day-to-day use. That advantage becomes more important as discharge pathways expand and more complex patients receive long-duration feeding support outside the hospital. Powder formulas still retain value in cost-sensitive settings, in pediatric metabolic care where clinicians need custom caloric density, and in cases where longer shelf life or concentration adjustment is useful. Institutional practices also favor validated, ready-to-use liquids because hospitals must manage preparation controls carefully and avoid unnecessary handling steps. The balance within the United States enteral nutrition market, therefore, continues to favor liquids for convenience, safety, and workflow reasons, while powders remain relevant in selected clinical and economic settings.

By Age Group: Pediatric Growth Outpaces the Adult Base

Adults accounted for 52.71% of United States enteral nutrition market share in 2025, while Pediatrics is projected to expand at a 6.65% CAGR through 2031. Adult leadership remains tied to the large patient census across oncology, neurologic disease, surgical recovery, and geriatric care, which keeps this cohort at the center of revenue generation in the United States enteral nutrition market. The adult base is especially important because absolute patient volume remains high even as faster growth appears in more specialized pediatric uses. Older adults also raise the average value per patient when dysphagia overlaps with kidney disease, dementia, stroke, or cancer, and pushes prescribing toward tailored nutrition.

Pediatric growth is stronger because rare metabolic disorders, pediatric oncology, eosinophilic gastrointestinal disease, and food protein-related conditions all require specialized formula pathways. The National Cancer Institute projected 14,690 childhood and adolescent cancer diagnoses in 2025, which supports a persistent need for nutrition intervention in pediatric oncology care. A 2025 Nutrients review also supported the growing use of elemental and semi-elemental formulas in pediatric eosinophilic esophagitis, multiple food protein intolerance, and short gut syndrome. These factors explain why pediatrics is the fastest-growing age segment, even though adults still generate the largest revenue base. The US enteral nutrition industry, therefore, combines a mature adult core with a pediatric segment that is more specialized, faster growing, and increasingly important for innovation.

By Indication: Oncology Accelerates While GI Disorders Anchor Demand

Gastrointestinal Disorders and Malabsorption accounted for 44.21% of United States enteral nutrition market size in 2025, while Oncology is projected to grow at a 6.09% CAGR through 2031. GI-related demand stays largest because enteral nutrition is directly relevant in short bowel syndrome, inflammatory bowel disease, severe malabsorption, and related disorders where the gut remains the preferred route but nutrient absorption is impaired. This makes gastrointestinal care the anchor indication in the United States enteral nutrition market, especially for peptide-based, elemental, and disease-specific formulas. The breadth of GI needs also supports consistent consumption across both hospital and home settings.

Oncology is expanding faster because nutrition intervention is moving earlier in the care pathway and is being used more consistently during treatment. ASPEN’s 2025 practice tool for oncology patients recommends enteral support when intake falls below 60% to 75% of needs for 7 to 14 days, which places nutrition therapy more firmly inside routine cancer care. Neurology remains another large and durable use case because stroke, dementia, and cerebral palsy often create long-duration tube feeding dependence. Diabetes and CKD continue to drive disease-specific formula uptake, while food allergy, eosinophilic GI disease, and inborn errors of metabolism support high-value elemental and specialty products. Specialist manufacturers such as Ajinomoto, Cambrooke, and Vitaflo USA benefit from this narrower but highly defended niche because clinical switching barriers remain high in complex metabolic care.

By End User: Homecare Settings Rise as Hospital Formulary Share Stabilizes

Hospitals accounted for 56.12% of United States enteral nutrition market size in 2025, while Homecare Settings are projected to expand at a 5.77% CAGR through 2031. Hospital leadership remains strong because acute care still handles the highest-acuity cases, and formulary decisions made there shape product use across intensive care, oncology, surgery, and neurology. In the United States enteral nutrition market, dietitians and pharmacy committees continue to influence brand access, which gives incumbents with established clinical evidence and supply reliability a clear advantage. Once hospital placement is secured, suppliers can often hold volume for long periods through standard protocols and purchasing relationships.

Homecare is growing faster because post-surgical, oncology, and neurologic patients are increasingly discharged with ongoing nutrition support needs. CMS coverage under NCD 180.2 and related documentation rules shapes how providers structure supply, education, and follow-up for patients outside the hospital. Long-term care centers and skilled nursing facilities remain a stable middle layer because they serve chronically institutionalized older adults who often require routine polymeric or disease-specific feeding support. Specialty clinics and outpatient sites also matter more now, especially for pediatric metabolic patients and oncology patients who need ongoing tube feeding or oral nutrition support alongside treatment. Providers that invest in documentation systems and payer compliance are better placed to keep serving these channels as the center of demand shifts beyond hospital walls.

Geography Analysis

The United States enteral nutrition market is defined as a single-country market, but demand is not evenly distributed across regions because age mix, provider density, and payer structures vary sharply from state to state. The Southeast and Sun Belt carry an outsized role in the United States enteral nutrition market because they combine large elderly populations with growing homecare needs and high exposure to chronic disease. Florida, Texas, and Arizona stand out within this pattern, especially for geriatric-adapted formulas and home enteral services that support post-acute patients outside hospital settings. Florida had 4.7 million residents age 65 or older in 2024, which makes it one of the clearest demand nodes for age-linked enteral care in the country. Texas and California, by contrast, are also important for pediatric nutrition because large pediatric specialty hospital networks and greater absolute case volumes support elemental, metabolic, and oncology-related formula demand.

The Northeast and Mid-Atlantic form another distinct center because they host dense clusters of academic medical centers and children’s hospitals that shape protocol adoption. Boston, Philadelphia, and New York often serve as early reference points for complex enteral practices, including blenderized tube feeding, amino acid-based formulas, and specialty pediatric nutrition. This gives manufacturers an advantage when they can build evidence, medical affairs ties, and clinical partnerships inside these institutions before broader rollout. The same regions also show an access gap, because rural communities in parts of the Northeast, Appalachia, and the rural Midwest face lower provider density, fewer dietitians, and weaker home enteral coverage infrastructure. ASPEN’s 2025 shortage tracker showed that product disruptions affected programs nationwide, and rural and critical-access facilities faced heavier substitution pressure because they had thinner supply networks and fewer backup options.

The Midwest remains important because integrated health systems and large skilled nursing networks provide stable institutional demand for standard and geriatric-focused polymeric formulas. The Pacific and Mountain West are also becoming more relevant as telehealth-assisted home enteral programs and digitally supported pump management gain traction in health systems that are more open to care technology adoption. Medicaid policy differences between states create a real product-mix effect because fee-for-service states often preserve broader access to specialty formulas, while managed Medicaid structures can push prescribing toward lower-cost polymeric options. Louisiana’s January 2026 coverage expansion for amino acid-based elemental formulas is a clear example of how one state decision can change access for high-value categories and alter regional demand patterns. Companies with strong state-level market access capabilities, therefore, hold a practical advantage over peers that rely mainly on national contracting.

Competitive Landscape

The United States enteral nutrition market shows moderate-to-high concentration because Abbott Nutrition, Nestlé Health Science, Danone/Nutricia, and Fresenius Kabi USA still control most institutional formulary positions and major homecare relationships. This structure gives the category a stable incumbent layer, but it does not eliminate competition because product shortages, channel shifts, and differentiated formula design continue to create openings. The United States enteral nutrition market is increasingly split between large multinationals that compete on evidence depth, supply scale, and formulary reach, and smaller challengers that compete on ingredient transparency, real-food positioning, and caregiver preference. Danone made the clearest strategic move in 2025 when it acquired Functional Formularies and took a majority stake in Kate Farms, which combined medical-channel strength with a faster-growing plant-based and real-food platform. That repositioning has been especially important because it gave Danone stronger access to the parts of the United States enteral nutrition market that are growing through homecare, pediatric specialty demand, and caregiver-led formula choice.

The ENFit transition has also created a fresh competition point in delivery systems. Facilities replacing or upgrading pump platforms must often make linked decisions on accessories, compatibility, and workflow, so pump suppliers can influence broader enteral purchasing at the same time. Moog Medical and B. Braun have been active in this opening because the move toward ISO 80369-3 compatible systems creates switching windows that do not appear often in more stable installed bases. This matters because delivery systems do not sit outside formula competition, and bundle decisions can shape how easily a brand holds or expands a formulary position.

Shortage-led disruption has added another layer of redistribution inside the United States enteral nutrition market. Abbott’s March 2025 discontinuation of products, including Glucerna 1.2 Cal, Jevity 1.5 Cal, and EleCare Jr, along with Nestlé’s February 2025 withdrawal of Vivonex RTF, Peptamen Junior with Prebio1, and Glutasolve, opened immediate substitution opportunities for other suppliers. Fresenius Kabi’s 2026 Renalive HP launch directly fits this environment because it targets renal nutrition needs that became more exposed after competitor rationalization. At the niche end, Ajinomoto, Cambrooke, and Vitaflo USA remain difficult to displace in metabolic nutrition because proprietary compositions and specialist clinic ties create strong switching barriers. White space still exists in adult ketogenic therapy formulas, adolescent-focused blenderized products, and digital platforms that combine home enteral management with remote dietitian supervision.

United States Enteral Nutrition Industry Leaders

Abbott Nutrition

Danone

Fresenius Kabi USA

Nestlé Health Science

Vitaflo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Fresenius Kabi disclosed in its Q1 2026 earnings presentation the global commercial launch of Fresubin PRO Fibre and Renalive HP, with Renalive HP specifically targeting high-protein needs in renal patients, a segment experiencing supply gaps following competitor SKU rationalizations. The launch signals Fresenius Kabi's strategy to capture formulary share opened by Abbott and Nestlé portfolio contractions.

- March 2026: Louisiana Medicaid expanded coverage for amino acid-based elemental formulas effective January 1, 2026, covering eosinophilic disorders, FPIES, multiple food protein allergies, and severe GI malabsorption. The policy sets a state-level precedent and opens a commercial pathway for elemental formula manufacturers in Medicaid-reliant patient populations.

- July 2025: Danone announced the acquisition of a majority stake in Kate Farms, a plant-based enteral nutrition company distributed across more than 1,400 US hospitals, for an undisclosed consideration. The transaction substantially expands Danone/Nutricia's clinical distribution footprint in the United States and positions it as the dominant force in real-food and plant-based enteral nutrition.

- March 2025: Abbott Nutrition issued a product discontinuation notice covering Glucerna 1.2 Cal, Jevity 1.5 Cal, EleCare Jr, and related variants, creating immediate substitution pressure for hospital pharmacy teams and HEN distributors managing patients dependent on these SKUs. The action reflected Abbott's broader medical nutrition portfolio rationalization strategy.

United States Enteral Nutrition Market Report Scope

The Enteral Nutrition Market is defined as the healthcare industry segment focused on delivering essential nutrients directly into the gastrointestinal (GI) tract via feeding tubes when patients cannot consume food orally but have a functioning digestive system. It covers specialized formulas, devices, and services designed to maintain or improve nutritional status in clinical and home settings.

The United States Enteral Nutrition Products Market is defined and segmented across several key dimensions. By feeding method, it includes both tube feeding and oral feeding. By formula type, the market covers polymeric, peptide-based, elemental, and disease-specific formulations. In terms of form, products are available as liquid or powder. By age group, the market serves both adults and pediatrics. Segmentation by indication highlights usage in gastrointestinal (GI) disorders, oncology, neurology, diabetes, chronic kidney disease (CKD), allergy, and inborn errors of metabolism (IEM). The end users include hospitals, homecare, long-term care facilities, and specialty clinics. Geographically, the scope is focused on the United States, with market forecasts provided in terms of value (USD), reflecting the financial scale and growth potential of these product categories.

| Tube Feeding Products |

| Oral Feeding Products |

| Standard / Polymeric Formulas |

| Peptide-Based / Semi-Elemental Formulas |

| Elemental / Amino Acid-Based Formulas |

| Disease-Specific Formulas |

| Liquid |

| Powder |

| Adults | Adult 18-64 |

| Geriatric 65+ | |

| Pediatrics | Infants |

| Children | |

| Adolescents |

| Gastrointestinal Disorders and Malabsorption | Short Bowel Syndrome |

| Inflammatory Bowel Disease | |

| Severe Malabsorption / Diarrhea | |

| Oncology | |

| Neurology | Stroke Recovery |

| Dementia / Alzheimer’s Disease | |

| Cerebral Palsy and Neurodevelopmental Disorders | |

| Diabetes | |

| Chronic Kidney Disease | |

| Food Allergy and Eosinophilic GI Disorders | |

| Inborn Errors of Metabolism / Ketogenic Therapy | |

| General Malnutrition / Surgical Recovery / Critical Care |

| Hospitals | ICU / Critical Care |

| Med-Surg / Oncology Units | |

| Neonatal / Pediatric Units | |

| Homecare Settings | |

| Long-term Care Centers / Skilled Nursing Facilities | |

| Specialty Clinics / Outpatient Care |

| By Feeding Method | Tube Feeding Products | |

| Oral Feeding Products | ||

| By Formula Type | Standard / Polymeric Formulas | |

| Peptide-Based / Semi-Elemental Formulas | ||

| Elemental / Amino Acid-Based Formulas | ||

| Disease-Specific Formulas | ||

| By Form | Liquid | |

| Powder | ||

| By Age Group | Adults | Adult 18-64 |

| Geriatric 65+ | ||

| Pediatrics | Infants | |

| Children | ||

| Adolescents | ||

| By Indication | Gastrointestinal Disorders and Malabsorption | Short Bowel Syndrome |

| Inflammatory Bowel Disease | ||

| Severe Malabsorption / Diarrhea | ||

| Oncology | ||

| Neurology | Stroke Recovery | |

| Dementia / Alzheimer’s Disease | ||

| Cerebral Palsy and Neurodevelopmental Disorders | ||

| Diabetes | ||

| Chronic Kidney Disease | ||

| Food Allergy and Eosinophilic GI Disorders | ||

| Inborn Errors of Metabolism / Ketogenic Therapy | ||

| General Malnutrition / Surgical Recovery / Critical Care | ||

| By End User | Hospitals | ICU / Critical Care |

| Med-Surg / Oncology Units | ||

| Neonatal / Pediatric Units | ||

| Homecare Settings | ||

| Long-term Care Centers / Skilled Nursing Facilities | ||

| Specialty Clinics / Outpatient Care | ||

Key Questions Answered in the Report

What is the size of the United States enteral nutrition market in 2025 and 2031?

The United States enteral nutrition market was valued at USD 3.54 billion in 2025 and is forecast to reach USD 4.60 billion by 2031, with a 4.53% CAGR over 2026-2031.

Which feeding method leads revenue in U.S. enteral nutrition products?

Tube Feeding Products led in 2025 with 64.57% share, but Oral Feeding Products are growing faster at a 5.46% CAGR through 2031.

Why is homecare becoming more important for enteral nutrition in the United States?

Homecare is growing because hospitals are moving patients into lower-cost post-acute settings, and CMS coverage pathways support ongoing nutrition delivery outside inpatient care.

Which formula category is growing fastest in the United States enteral nutrition products space?

Disease-Specific Formulas are the fastest-growing formula type, with a projected 5.27% CAGR through 2031, supported by stronger use in diabetes, renal, oncology, and GI care.

What is driving pediatric demand for enteral nutrition products in the United States?

Pediatric demand is rising because of rare metabolic disorders, pediatric oncology, and eosinophilic GI conditions, which together are pushing the segment to a 6.65% CAGR through 2031.

Page last updated on: