North America Clinical Nutrition Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

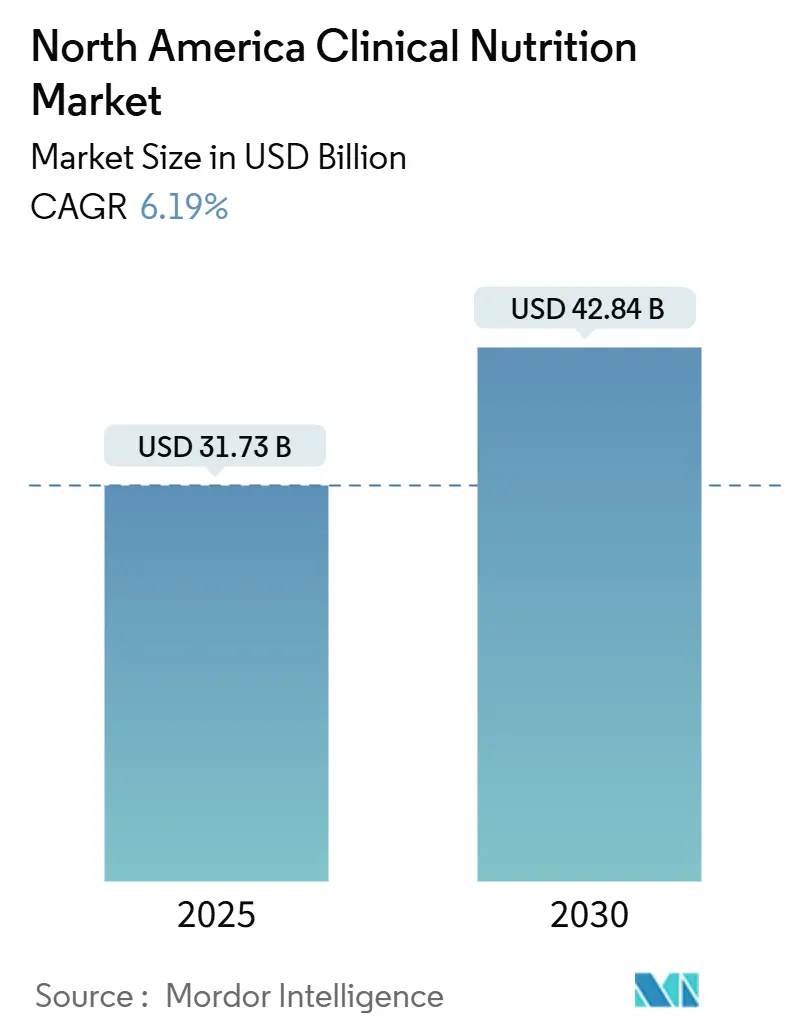

| Market Size (2025) | USD 31.73 Billion |

| Market Size (2030) | USD 42.84 Billion |

| Growth Rate (2025 - 2030) | 6.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Clinical Nutrition Market Analysis by Mordor Intelligence

The North America clinical nutrition market is valued at USD 31.73 billion in 2025 and is projected to reach USD 42.84 billion by 2030, registering a 6.19% CAGR through the forecast period. Demographic aging, higher survival rates for chronic-disease patients, and telehealth adoption are the main growth catalysts. Remote dietitian consultations have expanded home enteral programs, while AI-based decision support is improving parenteral protocols. Regulatory modernization, such as the FDA’s first full review of infant-formula nutrients since 1988, is encouraging product innovation. Supply-chain resilience also rebounded after 2023 shocks, helped by a 34% surge in fish-oil output that stabilized lipid raw-material costs, further supporting the clinical nutrition market.

Key Report Takeaways

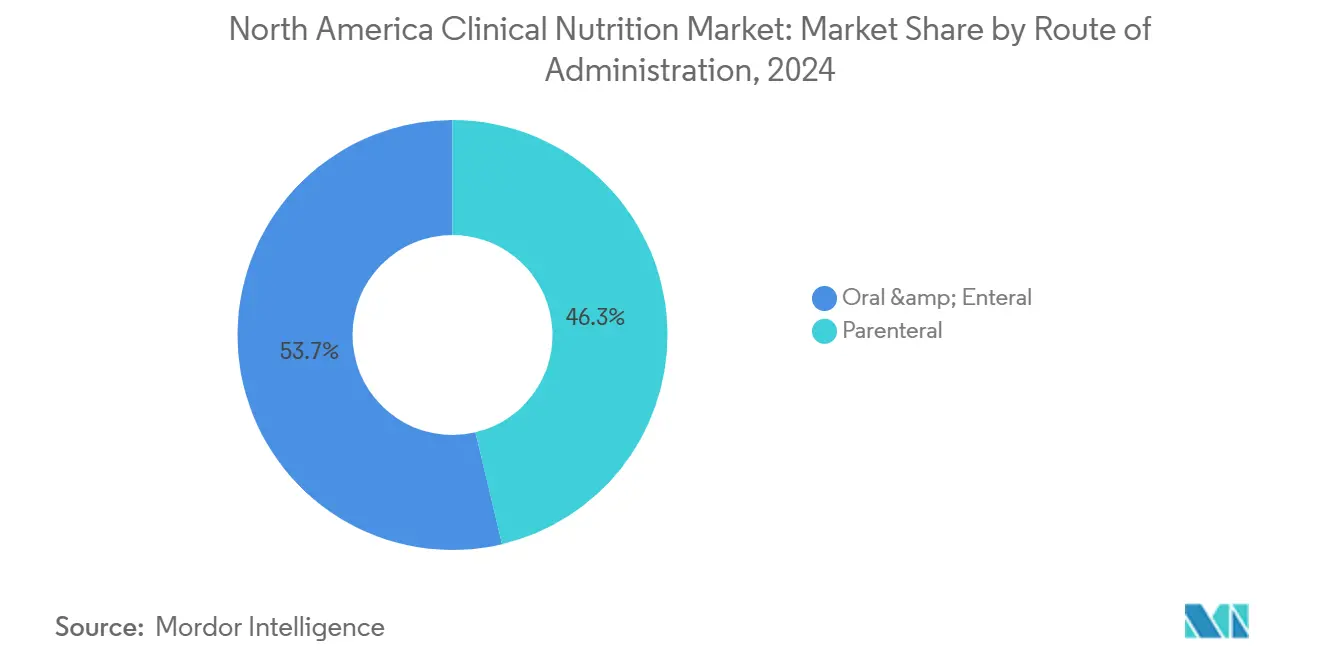

- By route of administration, oral & enteral routes commanded 53.7% of the clinical nutrition market share in 2024, whereas parenteral routes are expanding at a 6.4% CAGR to 2030.

- By product type, infant nutrition held 42.1% revenue share in 2024; adult nutrition are forecast to grow at 7.7% CAGR.

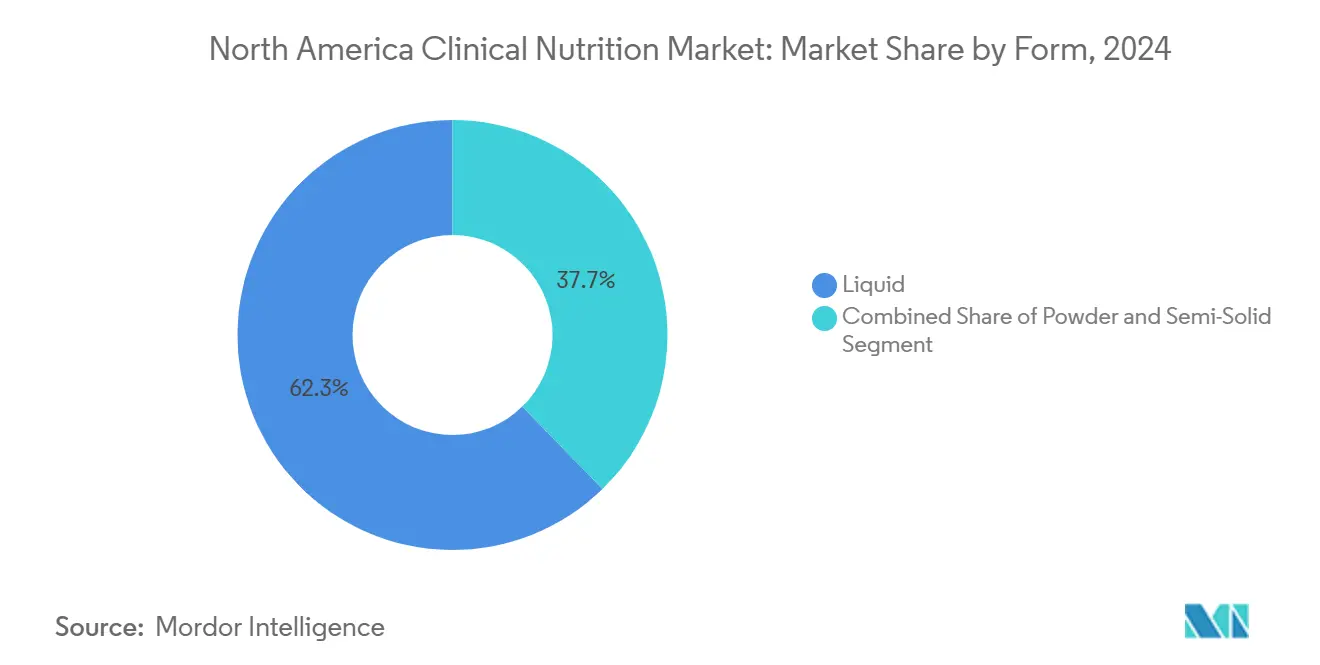

- By form, liquid products led with 62.3% share in 2024; semi-solid formats are projected to rise at a 7.8% CAGR.

- By application, nutritional support for malnutrition accounted for 31.8% of the clinical nutrition market size in 2024, while cancer nutrition is projected to advance at a 7.2% CAGR.

- By distribution channel, hospital pharmacies held a 57.4% share in 2024, and online pharmacies are poised for an 8.2% CAGR growth.

- By geography, the United States contributed 81.4% of regional revenue in 2024, with Mexico registering the fastest 6.7% CAGR outlook.

North America Clinical Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic & metabolic disorder prevalence | 1.80% | United States urban hubs | Long term (≥ 4 years) |

| Aging population growth | 1.50% | United States and Canada | Long term (≥ 4 years) |

| High healthcare spending | 1.20% | United States focus | Medium term (2–4 years) |

| Pre-term births and pediatric malnutrition | 0.90% | North American NICUs | Medium term (2–4 years) |

| Home-enteral expansion via telehealth | 0.70% | United States and Canada | Short term (≤ 2 years) |

| Fast-track lipid emulsions | 0.40% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic & Metabolic Disorders

The rise in diabetes, cardiovascular disease, and obesity is lifting baseline demand for medical nutrition therapy. Close to half of U.S. adults live with diet-related conditions requiring intensive dietary management. Specialized formulas designed for patients using GLP-1 medications address micronutrient depletion and lean-muscle loss risks, and companies are bundling these products with virtual coaching to improve adherence. Abbott and Nestlé Health Science each introduced targeted lines in 2024, signaling deeper alignment between pharmaceutical and nutrition strategies. Hospitals now include nutrition screening in chronic-care pathways, acknowledging cost offsets from reduced readmissions. Consequently, the clinical nutrition market is seeing faster uptake of disease-specific enteral products in outpatient settings.

Growing Aging Population Across North America

Adults aged 65 and older are forecast to account for one-fifth of the U.S. population by 2030. Sarcopenia and dysphagia are common geriatric challenges, prompting demand for texture-modified, high-energy formulas[1]Nature Editorial Team, “Expansion of the Aging Population,” nature.com . Ensure surpassed USD 3 billion in global sales in 2024 as older consumers increased discretionary spending on preventive nutrition. Nursing-home malnutrition prediction models can now identify at-risk residents with 90% accuracy, enabling earlier intervention. Economically, malnutrition among older adults costs the United States USD 51.3 billion each year, strengthening the case for reimbursable nutrition solutions. These trends create sustainable tailwinds for the clinical nutrition market.

High Healthcare & Insurance Spending Levels

U.S. healthcare spending exceeds USD 4 trillion annually, ensuring relatively attractive reimbursement for enteral and parenteral products. Medicare’s 2025 expansion of preventive nutrition benefits includes intensive counseling for obesity and cardiovascular risk[2]CMS, “Medicare Preventive Services Update 2025,” cms.gov. Private insurers are broadening coverage of medical foods for inherited metabolic disorders, although variability persists due to the absence of dedicated FDA regulation. In Canada, universal coverage structures have different cost-sharing mechanics; nevertheless, Health Canada’s CAD 4.4 billion dental-care program indirectly supports better nutrition by improving oral health barriers[3]Health Canada, “Canadian Dental Care Plan Announcement,” canada.ca . Payer scrutiny also drives manufacturers to collect stronger outcomes data, reinforcing evidence-based positioning across the clinical nutrition market.

Rising Incidence of Pre-Term Births & Pediatric Malnutrition

Neonatal ICUs rely heavily on customized amino-acid and lipid regimens for very-low-birth-weight infants. Baxter’s Clinolipid label expansion to neonates in 2024 provided a soybean-olive-oil blend that reduces essential fatty-acid deficiency risk. FDA GRAS clearance for lutein fortification addresses cognitive and visual development gaps in standard formulas. Human-milk fortifiers and elemental formulas remain essential for cow’s-milk-protein allergy and short-bowel syndrome. Fresenius Kabi advanced its Peditrace Novum trace-element solution in Europe, illustrating ongoing innovation. As a result, the pediatric segment remains a key contributor to clinical nutrition market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-agency regulatory approvals | -0.80% | United States, spillover to Canada & Mexico | Medium term (2–4 years) |

| Clinician & patient misperceptions | -0.60% | Region-wide, heightened in rural zones | Long term (≥ 4 years) |

| Declining birth rates | -0.40% | United States & Canada | Long term (≥ 4 years) |

| Fish-oil supply volatility | -0.30% | Global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Agency Regulatory Approvals

Manufacturers must navigate separate frameworks from the FDA, Health Canada, and COFEPRIS, each with unique dossiers and labeling rules. The FDA’s sweeping infant-formula nutrient review adds complexity by updating quantitative targets for numerous micronutrients. Health Canada is simultaneously modernizing its special-diet regulations to close gaps exposed during the 2022 formula shortage. Divergent timelines and documentation raise launch costs and slow cross-border rollouts, constraining velocity in the clinical nutrition market.

Misperceptions Among Clinicians & Patients

Knowledge gaps can deter optimal usage of tube feeding or parenteral therapy. Canadian surveys report that home enteral users face high out-of-pocket costs and limited dietitian contact, undermining compliance. In the United States, CVS Health showed that dedicated dietitian support resolved feeding intolerances in 91% of cases by day 60. Without structured education, physicians may delay initiation, and patients might discontinue early, placing a drag on clinical nutrition market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Telehealth Drives Enteral Expansion

Oral & Enteral solutions generated 53.7% of the clinical nutrition market size in 2024. Demand reflects clinicians’ preference for less invasive feeding when gastrointestinal function remains intact. Telehealth monitoring platforms now allow dietitians to titrate formulas remotely, reducing hospital revisits and reinforcing payer confidence in home care. Hospitals are integrating smart pumps that transmit real-time metrics, enabling early troubleshooting and lowering aspiration pneumonia incidents.

Parenteral products represent a smaller base but are climbing at 6.4% CAGR as mixed-oil emulsions receive broad formulary acceptance. AI engines such as TPN 2.0 calculate individualized macronutrient ratios, cutting compounding errors in NICUs. Home parenteral therapy, once limited by sepsis fears, is expanding as remote monitoring and antimicrobial lock solutions improve safety. Together, these dynamics position both modalities as complementary pillars within the clinical nutrition market.

By Product Type: Adult Nutrition Lead Innovation

Infant Nutrition commanded 42.1% of regional sales in 2024, buoyed by ongoing formula upgrades that add lutein, DHA, choline, and human milk oligosaccharides. Regulatory scrutiny following the 2022 contamination crisis accelerated investments in redundancy and quality controls.

Adult nutrition products are forecast to outpace the overall clinical nutrition market at 7.7% CAGR. Growth stems from oncology, renal, hepatic, and diabetes-tailored formulas that align with value-based care incentives. Weight-management drives also foster GLP-1 companion drinks fortified with high leucine content. Standard enteral continues to serve broad medical-surgical wards, while total parenteral nutrition components innovate through novel trace-element blends that lower cholestasis risk.

By Form: Semi-Solid Gains Traction

Liquid offerings held a 62.3% share of the clinical nutrition market in 2024. Ready-to-use packaging cuts medication-room labor and reduces contamination risk, explaining hospital loyalty. Shelf-stable aseptic technology further benefits disaster stockpiling needs.

Semi-Solid formats are growing fastest at 7.8% CAGR because texture-modified gels help dysphagic seniors maintain dignity by using spoonable meals rather than tube feeds. Japan’s pioneering research inspired North American manufacturers to refine viscosities that flow through narrow feeding tubes yet resist pulmonary aspiration. Powder forms remain vital where long storage and flexible dosing matter, particularly in rural clinics that rely on mail-order supply chains.

By Application: Cancer Nutrition Accelerates

Nutritional support for malnutrition represented 31.8% of the clinical nutrition market share in 2024. Hospitals continue to screen inpatients for involuntary weight loss on admission, triggering protocolized high-protein interventions that shorten length of stay.

Cancer care is projected to expand at a 7.2% CAGR because immunonutrition regimens rich in arginine, omega-3s, and nucleotides reduce postoperative complications. Enhanced recovery after surgery pathways now embed pre-op carbohydrate loading and post-op sip feeds. Metabolic disorders benefit from low-phenylalanine powders and branched-chain amino acid modules, whereas gastrointestinal indications use elemental feeds that bypass pancreatic stimulation, easing symptom burden.

By Distribution Channel: Online Pharmacies Surge

Hospital pharmacies supplied 57.4% of purchases in 2024 because formulary controls tether most inpatients to institutional supply. Group-purchasing contracts reinforce volume discounts and ensure pharmacovigilance data capture.

Online pharmacies will rise at an 8.2% CAGR as consumer comfort with direct-to-home delivery grows. Platforms integrate telehealth consultations, insurance adjudication, and automatic reorder scheduling, lifting persistency. Retail chains expand shelf space for disease-specific powders, while specialty infusion centers bundle nursing visits with product dispensing, smoothing transitions from hospital to home.

Geography Analysis

The United States dominates the clinical nutrition market, contributing 81.4% of regional revenue in 2024. A large elderly population, extensive ICU capacity, and a robust reimbursement apparatus sustain demand. The FDA’s fast-track pathway for innovative lipids and its sweeping infant-formula nutrient review illustrate an enabling yet rigorous regulatory climate. Around 437,882 Americans rely on home enteral nutrition, and Medicare’s widened preventive-nutrition benefits reinforce growth.Canada accounts for a smaller but strategically important share. Universal healthcare shifts procurement power to provincial formularies, fostering price discipline yet guaranteeing baseline access. Recent regulatory modernization simplified cross-provincial distribution standards, and new vitamin-D fortification rules in yogurt and kefir target population deficiencies. However, high out-of-pocket spending for enteral supplies and limited dietitian coverage can suppress adherence among home-care patients. Mexico exhibits the fastest 6.7% CAGR outlook through 2030. The government’s strict front-of-pack labeling to curb sugar and sodium intake is raising health literacy. COFEPRIS issued clearer import guidelines that improve transparency but still require costly documentation, favoring global incumbents with regulatory scale. The USMCA agreement reduced tariffs on dairy proteins, supporting local manufacturing of high-protein enteral blends. Consumer awareness campaigns and rising private insurance penetration further unlock potential, positioning Mexico as an emerging pillar of the clinical nutrition market.

Competitive Landscape

Three multinationals, such as Abbott Laboratories, Nestlé Health Science, and Fresenius Kabi, collectively controlled significant market share in 2024, underscoring moderate consolidation. Abbott leverages integrated R&D and sprawling distribution, recording USD 955 million in U.S. nutrition revenue in Q1 2025 on the strength of Ensure and Glucerna. Nestlé broadens its therapeutic footprint through acquisitions such as VOWST, a microbiota-based capsule for recurrent C. difficile infection, complementing its peptide-based tube feeds.Fresenius Kabi differentiates with vertical supply-chain investments that earned the 2024 Trailblazer Award from Premier Inc., highlighting risk-mitigation capabilities valued by hospital systems. Mid-tier participants focus on niche disease states: Alcresta markets enzyme-activated formulas for exocrine pancreatic insufficiency, while Kate Farms targets plant-based hypoallergenic feeds for pediatric allergy management. Start-ups deploy AI to tailor macronutrient ratios based on genomics or microbiome profiles, creating data-heavy moats that challenge traditional product-only models.Digital service overlays are becoming decisive. Nestlé’s GLP-1 nutrition portal offers symptom triage and dietitian chat, aiming to secure lifetime customer value as anti-obesity drugs proliferate. Abbott invests in continuous glucose-monitoring tied to nutrition algorithms, a bridging device, and formula lines. Contract manufacturing organizations, especially in lipid emulsions, expand high-purity fish-oil facilities in Canada to hedge climate-driven supply swings. Competitive intensity, therefore, balances product innovation, integrated services, and supply-chain robustness across the clinical nutrition market. Source: https://www.mordorintelligence.com/industry-reports/north-america-medical-clinical-nutrition-market-industry

North America Clinical Nutrition Industry Leaders

Abbott Laboratories (Abbott Nutrition)

Nestlé SA

Baxter

Danone Nutricia

Fresenius Kabi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: OmniActive received FDA GRAS clearance for Lutemax Free Lutein in infant-formula applications, enabling brain and eye development support.

- April 2025: Abbott Laboratories launched a new immunonutrition formula specifically designed for oncology patients undergoing chemotherapy.

- March 2025: Nestlé Health Science completed the acquisition of a specialized pediatric nutrition company for USD 1.2 billion, expanding its portfolio of products for children with rare metabolic disorders.

- February 2025: Fresenius Kabi received FDA approval for a next-generation parenteral nutrition solution featuring an improved lipid emulsion with enhanced stability and reduced inflammatory potential.

- December 2024: Danone (Nutricia) launched a comprehensive digital platform for healthcare professionals to monitor patients on home enteral nutrition, featuring remote adjustment capabilities and integration with electronic health records.

North America Clinical Nutrition Market Report Scope

Mordor Intelligence defines the North American clinical nutrition market as the aggregate spending on science-based oral, enteral, and parenteral nutrition products that are prescribed or recommended to manage disease-related malnutrition, metabolic disorders, or recovery-critical conditions across hospitals, long-term care, and home-care settings. All figures are recorded at manufacturer selling price and expressed in constant 2024 US dollars.

Scope exclusion: Sports nutrition powders, standard multivitamin tablets, and over-the-counter wellness drinks not marketed for clinical use are kept outside the model.

| Oral & Enteral |

| Parenteral |

| Infant Nutrition |

| Adult Nutrition |

| Geriatric Nutrition |

| Powder |

| Liquid |

| Semi-Solid |

| Nutritional Support for Malnutrition |

| Metabolic Disorders |

| Gastrointestinal Diseases |

| Cancer |

| Neurological Diseases |

| Other Diseases |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Homecare & Specialty Clinics |

| United States |

| Canada |

| Mexico |

| By Route of Administration | Oral & Enteral |

| Parenteral | |

| By Product Type | Infant Nutrition |

| Adult Nutrition | |

| Geriatric Nutrition | |

| By Form | Powder |

| Liquid | |

| Semi-Solid | |

| By Application | Nutritional Support for Malnutrition |

| Metabolic Disorders | |

| Gastrointestinal Diseases | |

| Cancer | |

| Neurological Diseases | |

| Other Diseases | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| Homecare & Specialty Clinics | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North American clinical nutrition market?

The clinical nutrition market stands at USD 31.73 billion in 2025 and is forecast to rise to USD 42.84 billion by 2030.

Which route of administration holds the largest share?

Oral & Enteral nutrition products command 53.7% of the clinical nutrition market share, supported by telehealth expansion and patient preference for less invasive feeding.

Why are disease-specific enteral formulas growing faster than standard products?

Precision nutrition needs in oncology, renal, and metabolic disorders push demand for tailored macronutrient and micronutrient profiles, driving a 7.7% CAGR for this sub-segment.

How important is telehealth to clinical nutrition growth?

Telehealth enables real-time monitoring and dietitian consultations, lowering complications and scaling home enteral therapy, thereby adding a 0.7% CAGR uplift.

Which country in North America shows the fastest market growth?

Mexico leads with a projected 6.7% CAGR through 2030, helped by rising healthcare access and regulatory initiatives aimed at obesity and metabolic disease management.

Who are the leading players in the market?

Abbott Laboratories, Nestlé Health Science, and Fresenius Kabi collectively hold more than half of regional revenue, using product diversification and supply-chain strength to defend their positions.

Page last updated on: