Human Nutrition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 486.99 Billion |

| Market Size (2031) | USD 665.72 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Nutrition Market Analysis by Mordor Intelligence

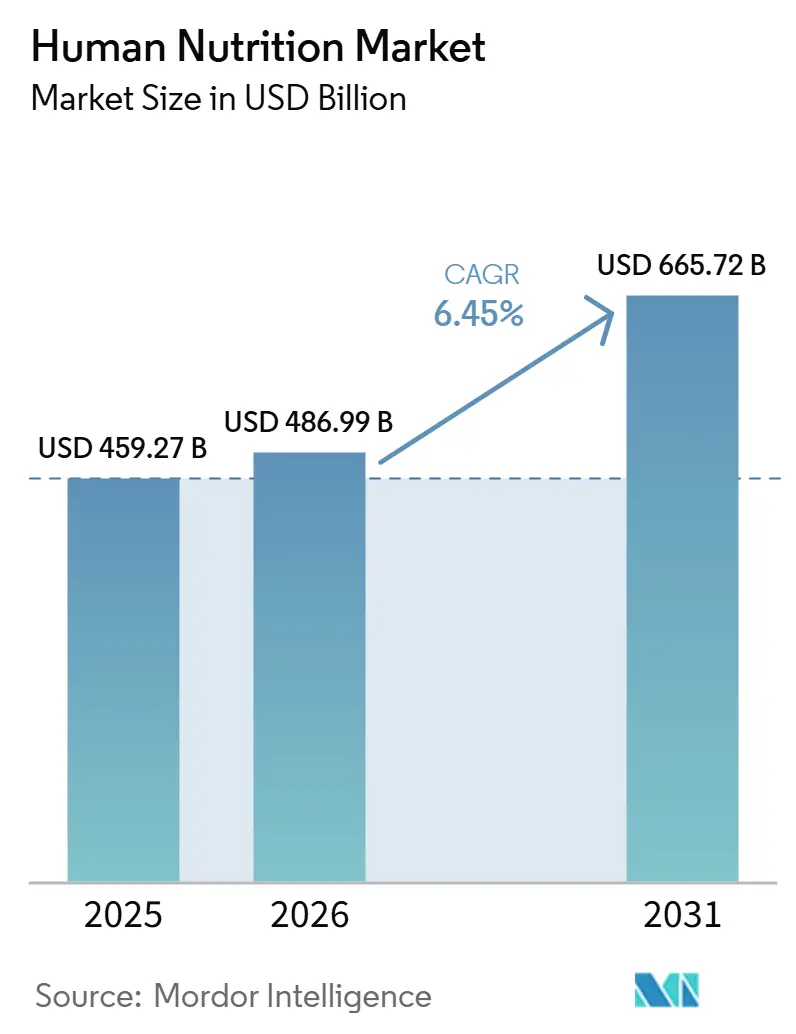

The human nutrition market is expected to increase from USD 459.27 billion in 2025 to USD 486.99 billion in 2026 and reach USD 665.72 billion by 2031, growing at a CAGR of 6.45% over 2026-2031. The human nutrition market is expanding as consumers place more value on daily health maintenance and use nutrition earlier in the care journey rather than after symptoms worsen. This demand is also supported by aging populations, higher out-of-pocket health costs, and broader interest in strength, mobility, immunity, and metabolic health. The human nutrition market is also benefiting from a wider product set, with supplements, medical nutrition, fortified foods, and functional beverages serving different use cases across retail and clinical settings. Digital commerce is widening product access and helping brands build repeat purchasing through subscriptions, direct communication, and personalized recommendations, while pharmacy-led channels still hold strong trust in many countries. At the same time, the human nutrition market faces tighter pressure from raw material volatility, differing regulatory standards across major regions, and growing consumer scrutiny around claims, purity, and scientific support.

Key Report Takeaways

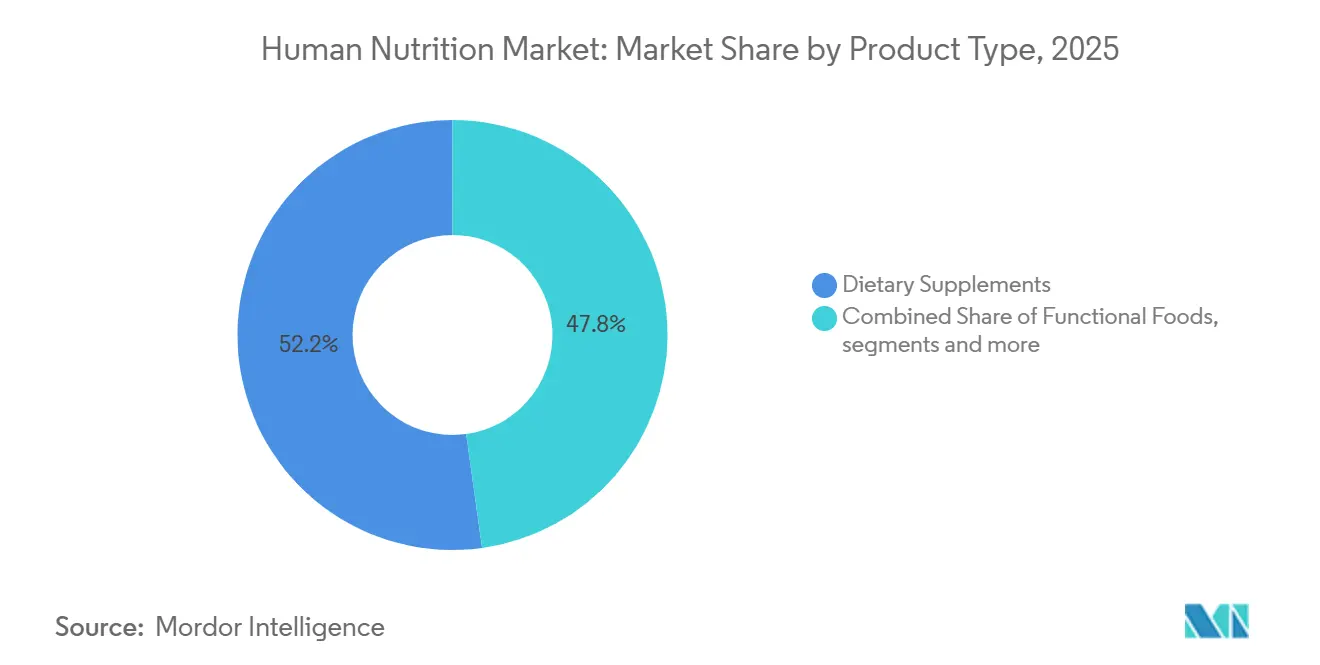

- By product type, dietary supplements led with 52.16% revenue share in 2025, while medical nutrition is forecasted to expand at a 6.55% CAGR through 2031.

- By ingredient type, vitamins and minerals held 42.22% share in 2025, while proteins and amino acids are projected to grow at a 6.71% CAGR through 2031.

- By dosage form, powder held 40.31% share in 2025, while gummies are projected to grow at a 7.26% CAGR through 2031.

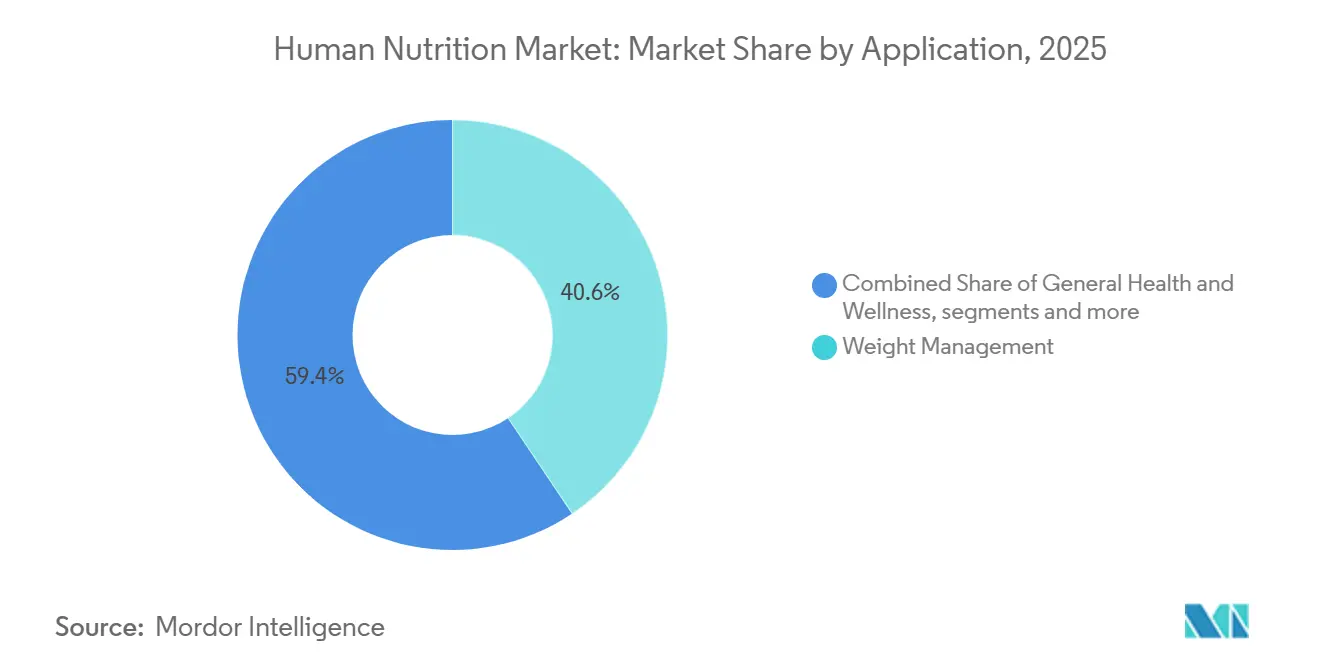

- By application, weight management accounted for 40.62% share in 2025, while general health and wellness is expected to advance at a 7.14% CAGR through 2031.

- By distribution channel, pharmacies and drug stores held 47.58% share in 2025, while online retailers and e-commerce are forecasted to grow at a 6.69% CAGR through 2031.

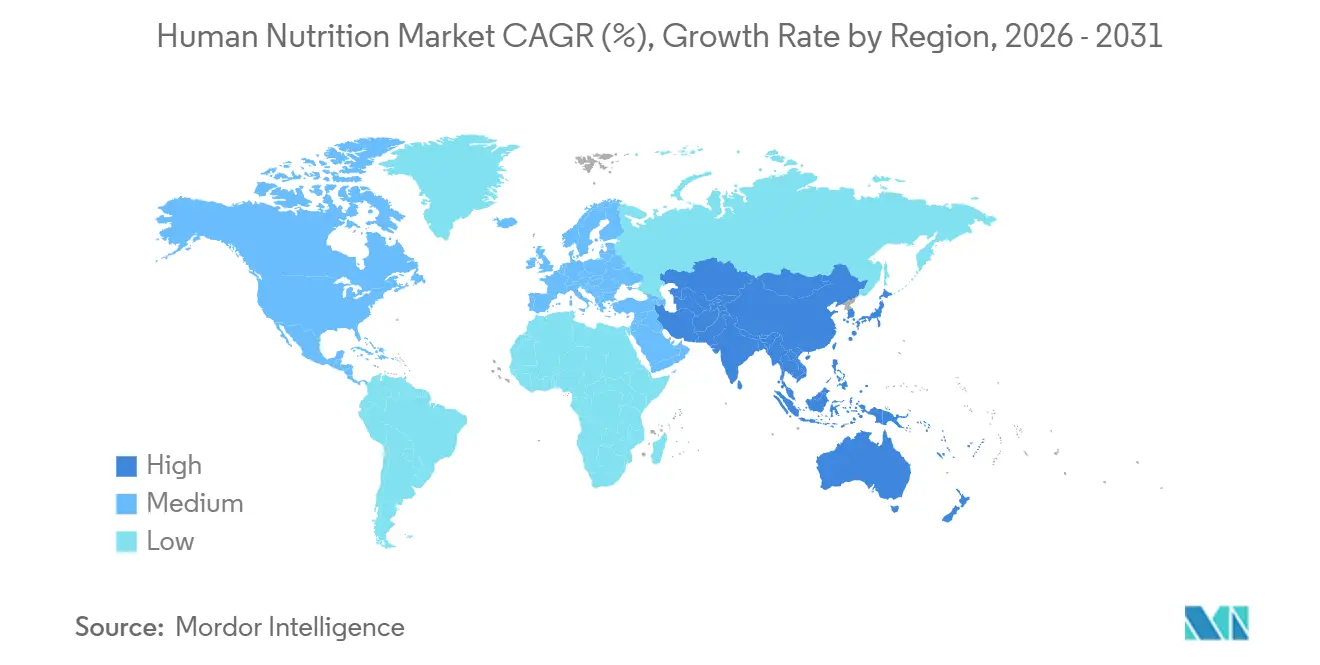

- By geography, North America held 50.27% share in 2025, while the Asia-Pacific is projected to expand at a 7.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Human Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Preventive Nutrition and Micronutrient Replenishment | +1.6% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Expansion of Personalized Nutrition and Omics-Based Formulations | +0.9% | North America, Europe, APAC urban centers | Long term (≥ 4 years) |

| Growth of E-Commerce, D2C, and Subscription Replenishment Models | +0.8% | Global, with highest penetration in North America and APAC | Short term (≤ 2 years) |

| Rising Adoption of Functional Foods and Fortified Beverages | +0.6% | APAC and Europe, with spillover to MEA | Medium term (2-4 years) |

| Aging Population and Life-Stage Specific Nutrition Demand | +1.4% | Global, acute in Japan, Germany, Italy, and South Korea | Long term (≥ 4 years) |

| Bioavailability and Format Innovation, Gummies, Powders, Shots, and Shelf-Stable Formats | +0.5% | Global, led by North America and EU R&D centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Preventive Nutrition and Micronutrient Replenishment

Preventive healthcare remains one of the most durable supports for the human nutrition market because chronic disease exposure is pushing consumers toward daily nutritional management. The shift is not limited to older consumers, since younger adults are also buying products for energy, sleep, recovery, mental focus, and long-term vitality. The human nutrition market is also gaining from wider clinical acceptance, as nutrition counseling is increasingly appearing alongside broader health management rather than sitting outside it. Demand linked to GLP-1 treatment is adding another layer, because appetite suppression raises concern around protein adequacy, micronutrient intake, and lean-mass preservation during weight reduction.[1]S. Makhija et al., “Nutritional Approaches to Enhance GLP-1 Analogue Therapy in Obesity: A Narrative Review,” Nutrients, mdpi.com That change makes preventive nutrition more practical and more routine, which supports repeat use across supplements, fortified products, and clinically positioned formulations. In the human nutrition market, this steady movement from occasional use to ongoing use is helping support category depth across several product formats.

Expansion of Personalized Nutrition and Omics-Based Formulations

Personalized nutrition is moving from a premium concept into a broader commercial model within the human nutrition market. Consumer interest is being shaped by digital tools that connect food intake with glucose response, microbiome information, activity patterns, and broader lifestyle data. This makes product selection feel more specific to need, which can improve retention and raise acceptance for higher-value formulations. The human nutrition market is therefore seeing a gradual move away from generic vitamin bundles and toward more targeted solutions for condition, life stage, and performance goal. This trend also favors brands that can combine evidence, formulation skill, and digital recommendation systems in a single customer journey. Over time, the human nutrition market is likely to give stronger pricing power to companies that can connect personalized advice with measurable outcomes and reliable replenishment.

Growth of E-Commerce, D2C, and Subscription Replenishment Models

E-commerce has become a structural growth engine for the human nutrition market rather than a temporary channel shift. Online platforms widen reach, support subscription purchasing, and allow brands to explain benefits, ingredients, and use cases in more detail than shelf labels usually permit. iHerb reported record net sales of USD 2.9 billion in fiscal 2025, and the company opened new fulfillment centers in Dallas-Fort Worth and Riyadh in 2026 to support further growth.[2]iHerb Corporate, “iHerb Achieves Record $2.9 Billion Net Sales in Fiscal 2025,” iHerb Corporate Communications, corporate.iherb.com That scale shows that digital health retail can now compete with established pharmacy and mass-market formats in both volume and consumer trust. The human nutrition market also benefits because online channels reach younger consumers who may not shop regularly in traditional health retail environments. As a result, the human nutrition market is adding new demand through digital discovery rather than simply shifting sales from one channel to another.

Aging Population and Life-Stage Specific Nutrition Demand

Aging populations are creating a long-duration demand base for the human nutrition market, especially where muscle preservation, mobility, cognition, and chronic disease management are becoming more urgent. Kerry noted that by 2030, 1 in 6 people globally will be over 60, which will raise demand for nutrition linked to mobility, cognitive function, and microbiome resilience. This demographic shift is important because it supports recurring use rather than one-time trial, especially in categories tied to daily function and quality of life. Abbott’s December 2025 launch of Ensure Max Protein 42 gm also shows how major suppliers are framing protein intake around muscle health and aging rather than only general wellness.[3]Abbott Mediaroom, “Abbott Launches Two New Ensure Max Protein Shakes,” Abbott Press Release, abbott.mediaroom.com India’s National Institute of Nutrition has also highlighted geriatric nutrition as a public health concern, which supports formal attention to age-linked deficiency and diet quality. In the human nutrition market, these shifts support demand across supplements, medical nutrition, and fortified foods aimed at maintaining independence later in life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Pressure from Clinical Validation, Claims Substantiation, and Quality Assurance | -1.0% | Global, most acute in North America and Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Regulatory Fragmentation Across Health Claims, Labels, and Ingredient Permissibility | -0.8% | EU, US, India, and Brazil | Medium term (2-4 years) |

| Consumer Skepticism Toward Efficacy, Purity, and Overlapping Claims | -0.6% | North America and Western Europe | Short term (≤ 2 years) |

| Supply Chain Volatility for Specialty Inputs, Bioactives, and Botanical Raw Materials | -0.7% | APAC-sourced ingredients with global freight exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Pressure from Clinical Validation, Claims Substantiation, and Quality Assurance

Raw material inflation is limiting margin expansion in the human nutrition market because many products depend on ingredients that are exposed to dairy cycles, agricultural variation, trade friction, and freight costs. Whey proteins, amino acid inputs, and botanical extracts remain especially sensitive because supply build-out often trails demand growth. When those costs rise quickly, companies must either absorb the hit, reduce promotional activity, or push higher prices into channels that may resist them. This pressure is especially difficult for mid-sized brands, since they often have less buying power and less ability to spread compliance and sourcing costs across a broad portfolio. The human nutrition market is also seeing stronger private-label pressure when retailers respond to inflation with lower-priced alternatives that narrow the premium space for brands without strong scientific equity. That means the human nutrition market is still growing, but not every player is benefiting equally from that growth.

Regulatory Fragmentation Across Health Claims, Labels, and Ingredient Permissibility

Regulatory fragmentation remains a meaningful brake on the human nutrition market because product claims, ingredient rules, and label expectations still vary sharply across major regions. The European framework on vitamins, minerals, and other added substances remains detailed and prescriptive, which raises the cost of multi-country portfolio management. In the United States, the FDA’s current priorities continue to stress food labeling, ingredient oversight, and stronger program delivery, which keeps compliance expectations visible for nutrition suppliers. These differences force companies in the human nutrition market to manage parallel formulation, substantiation, and packaging paths instead of using a single global model. The burden falls hardest on smaller manufacturers that lack dedicated regulatory teams and formal systems for frequent adaptation. For the human nutrition market, this does not stop growth, but it does slow product rollout and favor better-capitalized operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dietary Supplements Lead, Medical Nutrition Fastest Growing

Dietary supplements captured 52.16% of the human nutrition market share in 2025, which shows how central they remain to everyday consumer nutrition decisions. Their lead reflects broad accessibility, wide format choice, and the ability to address goals such as immunity, energy, healthy aging, metabolic support, and active living within one category. In the human nutrition market, supplements also act as the most common starting point for consumers who are entering formal nutrition spending for the first time. They are sold across pharmacies, food retail, specialty outlets, and online channels, which gives them much wider reach than more specialized categories.

Medical nutrition is forecasted to grow at a 6.55% CAGR through 2031, which makes it the fastest-growing product type in the human nutrition market. The category is moving forward as nutrition becomes more integrated into oncology care, metabolic disorder support, recovery pathways, and home-care routines. Functional foods remain important because they place health benefits into everyday eating occasions, which reduces dependence on pill-based routines. Sports nutrition is still smaller by volume, yet its buyer base is broadening well beyond competitive athletes, which gives the human nutrition industry more room to expand premium protein, hydration, and recovery formats.

By Distribution Channel: Pharmacies Retain Volume as Online Channels Scale

Pharmacies and drug stores accounted for 47.58% share of the human nutrition market size in 2025, which kept them as the largest distribution channel. Their strength comes from a combination of trust, health-led positioning, and the presence of staff or healthcare touchpoints that can guide purchase decisions. In the human nutrition market, this matters because many consumers still prefer to buy nutrition products in settings that feel medically credible. Pharmacies also support premium pricing better than many food retail formats, especially for condition-linked, high-protein, or age-targeted products. This gives the channel continued importance even as digital options grow quickly.

Online retailers and e-commerce channels are projected to grow at a 6.69% CAGR through 2031, which makes them the fastest-expanding route in the human nutrition market. The channel is winning share because it combines convenience with easy product comparison, automatic replenishment, and stronger access to education and reviews. Online growth also helps the human nutrition market reach consumers who prefer self-directed research and repeat digital ordering rather than store visits. Over time, the strongest brands are likely to be those that protect pharmacy credibility while also building direct digital engagement.

By Dosage Form: Powder Leads, Gummies Fastest Growing

Powder accounted for 40.31% of the human nutrition market share in 2025, reflecting its widespread use across dietary supplements, sports nutrition, functional foods, and medical nutrition products. Its leading position is driven by formulation flexibility, longer shelf life, ease of storage, and the ability to deliver higher concentrations of proteins, vitamins, minerals, and other functional ingredients. In the human nutrition market, powders are commonly used in meal replacements, protein supplements, infant nutrition, and clinical nutrition, making them a preferred dosage form for both consumers and healthcare professionals.

Gummies are projected to grow at a 7.26% CAGR through 2031, making them the fastest-growing dosage form in the human nutrition market. Their rapid growth is supported by increasing consumer preference for convenient, palatable, and easy-to-consume nutritional products, particularly among children, adults, and older populations who may have difficulty swallowing tablets or capsules. Liquids continue to maintain strong demand due to their rapid absorption, suitability for pediatric and geriatric populations, and use in ready-to-drink nutritional beverages and clinical nutrition. Capsules remain a widely accepted dosage form because they offer precise dosing, portability, and compatibility with a broad range of nutritional ingredients. Other dosage forms, including tablets, softgels, nutrition bars, and chewables, continue to diversify the market by addressing specific consumer preferences, lifestyles, and targeted nutritional needs.

By Application: Weight Management Anchors Demand, General Health Accelerates

Weight management accounted for 40.62% share of the human nutrition market size in 2025, which kept it as the largest application area. This leadership reflects many years of concentrated spending on calorie control, metabolism, body composition, and, more recently, lean-mass preservation. As a result, the application retains scale while also opening room for more specialized and higher-value products.

General health and wellness are forecasted to grow at a 7.14% CAGR through 2031, which makes it the fastest-growing application in the human nutrition market. This reflects a wider consumer focus on feeling well across the day, with stronger interest in energy, sleep quality, resilience, immunity, and daily function. The category benefits because it is broad enough to support frequent use, yet specific enough to allow targeted positioning around age, lifestyle, and health objective. Immune, digestive, and cognitive health products are all gaining from better ingredient awareness and more evidence-based communication. Bone and joint health, along with healthy aging applications, also carry strong value potential as older consumers spend more on quality-of-life support in the human nutrition market.

By Distribution Channel: Pharmacies Retain Volume as Online Channels Scale

Pharmacies and drug stores accounted for 47.58% share of the human nutrition market size in 2025, which kept them as the largest distribution channel. Their strength comes from a combination of trust, health-led positioning, and the presence of staff or healthcare touchpoints that can guide purchase decisions. In the human nutrition market, this matters because many consumers still prefer to buy nutrition products in settings that feel medically credible. Pharmacies also support premium pricing better than many food retail formats, especially for condition-linked, high-protein, or age-targeted products. This gives the channel continued importance even as digital options grow quickly.

Online retailers and e-commerce channels are projected to grow at a 6.69% CAGR through 2031, which makes them the fastest-expanding route in the human nutrition market. The channel is winning share because it combines convenience with easy product comparison, automatic replenishment, and stronger access to education and reviews. Online growth also helps the human nutrition market reach consumers who prefer self-directed research and repeat digital ordering rather than store visits. Over time, the strongest brands are likely to be those that protect pharmacy credibility while also building direct digital engagement.

Geography Analysis

North America held 50.27% of the human nutrition market share in 2025, which kept it as the leading regional block. This position reflects high supplement penetration, strong retail depth across pharmacies and e-commerce, and a consumer base that is already comfortable with routine nutrition spending. The human nutrition market in North America also benefits from early adoption of new formats and strong interest in protein, healthy aging, and metabolic support. Regulatory visibility under the U.S. food oversight system supports product development, even though compliance expectations remain active and can add cost.

Asia-Pacific is forecasted to grow at a 7.51% CAGR, which makes it the fastest-expanding part of the human nutrition market size by region through 2031. Urban income growth, a wider middle class, and stronger interest in science-backed nutrition are supporting demand across South Asia, Southeast Asia, and major East Asian markets. The human nutrition market in the region also benefits from food fortification programs and a rising shift from informal remedies toward standardized branded products. Japan and South Korea remain important for premium and age-linked nutrition, while India and Southeast Asia offer faster volume expansion and wider first-time adoption. India’s National Institute of Nutrition has pointed to geriatric nutritional deficiency as a public health concern, which supports continued attention to age-focused nutrition needs.

Europe holds a significant position in the human nutrition market because consumers are highly engaged with preventive health and functional food use. Demand is supported by established habits around supplements, digestive support, healthy aging, and everyday wellness products. The region also has a strong pharmacy and specialty channel base, which helps premium and evidence-led products maintain credibility. At the same time, the human nutrition market in Europe faces heavier formulation and labeling discipline because ingredient additions and related rules remain closely regulated. South America and the Middle East and Africa remain smaller in absolute size, but the human nutrition market is gaining opportunity there as urban retail, e-commerce, and preventive health messaging improve. These regions are likely to stay attractive for companies that can balance affordability, local relevance, and channel development.

Competitive Landscape

The human nutrition market shows moderate concentration at the top and broad fragmentation below that level. Large multinational suppliers hold structural advantages because they can fund research, manage regulatory work across several regions, and support many brands or product lines at the same time. The human nutrition market therefore rewards companies that combine evidence, supply reliability, and distribution breadth instead of relying on one product trend. Nestlé, Abbott, Danone, DSM-Firmenich, Herbalife, Glanbia, and other large operators remain prominent because they can move across supplements, medical nutrition, functional foods, and ingredient platforms. Smaller firms still play a role, but they usually compete through niche positioning, local formulation preferences, or focused digital communities rather than scale alone.

Recent company actions show that competition in the human nutrition market is not based only on price or brand recognition. iHerb expanded fulfillment capacity in 2026 after reporting record fiscal 2025 sales, which highlights how digital infrastructure has become a competitive asset in the human nutrition market. Kerry also released its 2026 Supplements Taste Charts to help manufacturers align flavor and format choices with regional preferences, which shows that sensory execution is becoming part of nutrition competition rather than a secondary issue.

Ingredient science and platform capabilities are also shaping competition in the human nutrition market. DSM-Firmenich reported FY2025 net sales of EUR 9 billion (USD 9.72 billion) and outlined a performance acceleration plan through 2027, which indicates continued selective investment despite wider macro pressure. Companies with stronger regulatory systems are also in a better position because the burden of evidence, labeling discipline, and portfolio adaptation is rising across major regions. This means the human nutrition market still offers room for specialists, but it increasingly favors firms that can scale trust as well as product volume. Over the next several years, the clearest white space is likely to remain around healthy aging, treatment-support nutrition, targeted proteins, and digital personalization tied to repeat purchasing in the human nutrition market.

Human Nutrition Industry Leaders

Nestlé S.A.

Abbott Laboratories

Danone S.A.

Bayer AG

Herbalife Nutrition Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nestlé and biotechnology company Helaina announced a partnership to advance novel bioactive proteins derived from human-milk bioactives, combining Nestlé's decades of early-life nutrition science with Helaina's precision fermentation platform. The collaboration targets gut health, immunity, and women's wellness, advancing a category of biotechnology-derived functional ingredients with high differentiation potential and barriers to replication

- May 2026: Danone expanded its Oikos Protein Shakes line with two new flavors, including Mocha Latte, delivering 30 g of protein, 5 g of prebiotic fiber, and 95 mg of caffeine, targeting the growing "profee" (protein plus coffee) functional occasion. The launch reflects Danone's accelerating push into high-protein RTD nutrition alongside its EUR 1 billion (~USD 1.1 billion) Huel acquisition.

- March 2026: Danone announced a definitive agreement to acquire Huel, a complete nutrition and meal replacement brand, for EUR 1 billion (USD 1.1 billion), currently under review by the UK Competition and Markets Authority. The transaction extends Danone's position in functional, digitally distributed nutrition and adds a direct-to-consumer subscription business with strong UK, European, and US brand equity.

- March 2026: Herbalife announced a planned USD 55 million acquisition of Bioniq, a personalized supplement company, to expand personalized nutrition capabilities globally, complementing prior acquisitions of Pro2col and Link BioSciences. The transaction is expected to close in Q2 2026, with Bioniq products to be offered through Herbalife's distributor network in Europe and the US later in 2026.

Global Human Nutrition Market Report Scope

According to the report’s scope, the human nutrition market encompasses products and solutions designed to support dietary health and nutritional well-being, including dietary supplements, functional foods, clinical nutrition, and fortified food and beverage products aimed at improving overall human health.

The human nutrition market is segmented into product type, ingredient type, dosage form, application, distribution channel, and geography. By product type, the market is segmented into dietary supplements, functional foods, medical nutrition, and sports nutrition. By ingredient type, the market is segmented into vitamins and minerals, proteins and amino acids, probiotics, fiber and specialty carbohydrates, and phytochemicals and botanical extracts. By dosage form, the market is segmented into powder, liquid, capsules, gummies, and other dosage forms. By application, the market is segmented into weight management, general health and wellness, digestive health, immune health, cognitive health, bone and joint health, and anti-aging and healthy longevity. By distribution channel, the market is segmented into pharmacies and drugstores, supermarkets and hypermarkets, and online retailers and e-commerce. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Dietary Supplements |

| Functional Foods |

| Medical Nutrition |

| Sports Nutrition |

| Vitamins and Minerals |

| Proteins and Amino Acids |

| Probiotics |

| Fiber and Specialty Carbohydrates |

| Other Ingredient Types |

| Powder |

| Liquid |

| Capsules |

| Gummies |

| Other Dosage Forms |

| Weight Management |

| General Health and Wellness |

| Digestive Health |

| Immune Health |

| Cognitive Health |

| Bone and Joint Health |

| Other Applications |

| Pharmacies and Drugstores |

| Supermarkets and Hypermarkets |

| Online Retailers and E-Commerce |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Dietary Supplements | |

| Functional Foods | ||

| Medical Nutrition | ||

| Sports Nutrition | ||

| By Ingredient Type | Vitamins and Minerals | |

| Proteins and Amino Acids | ||

| Probiotics | ||

| Fiber and Specialty Carbohydrates | ||

| Other Ingredient Types | ||

| By Dosage Form | Powder | |

| Liquid | ||

| Capsules | ||

| Gummies | ||

| Other Dosage Forms | ||

| By Application | Weight Management | |

| General Health and Wellness | ||

| Digestive Health | ||

| Immune Health | ||

| Cognitive Health | ||

| Bone and Joint Health | ||

| Other Applications | ||

| By Distribution Channel | Pharmacies and Drugstores | |

| Supermarkets and Hypermarkets | ||

| Online Retailers and E-Commerce | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the human nutrition market?

The human nutrition market is estimated at USD 459.27 billion in 2025 to reach USD 486.99 billion in 2026 and is projected to reach USD 665.72 billion by 2031 at a 6.45% CAGR.

Which product type leads global demand in human nutrition?

Dietary supplements remain the largest product type, with 52.16% share in 2025, reflecting their broad accessibility and routine use across health goals.

Which application area is growing fastest in human nutrition?

General health and wellness is the fastest-growing application, with a projected 7.14% CAGR through 2031, as demand expands beyond weight control into energy, sleep, and resilience.

Which region dominates the global human nutrition landscape?

North America led with 50.27% share in 2025, supported by high supplement use, strong pharmacy and e-commerce networks, and a mature consumer base.

Page last updated on: