United States Digital Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

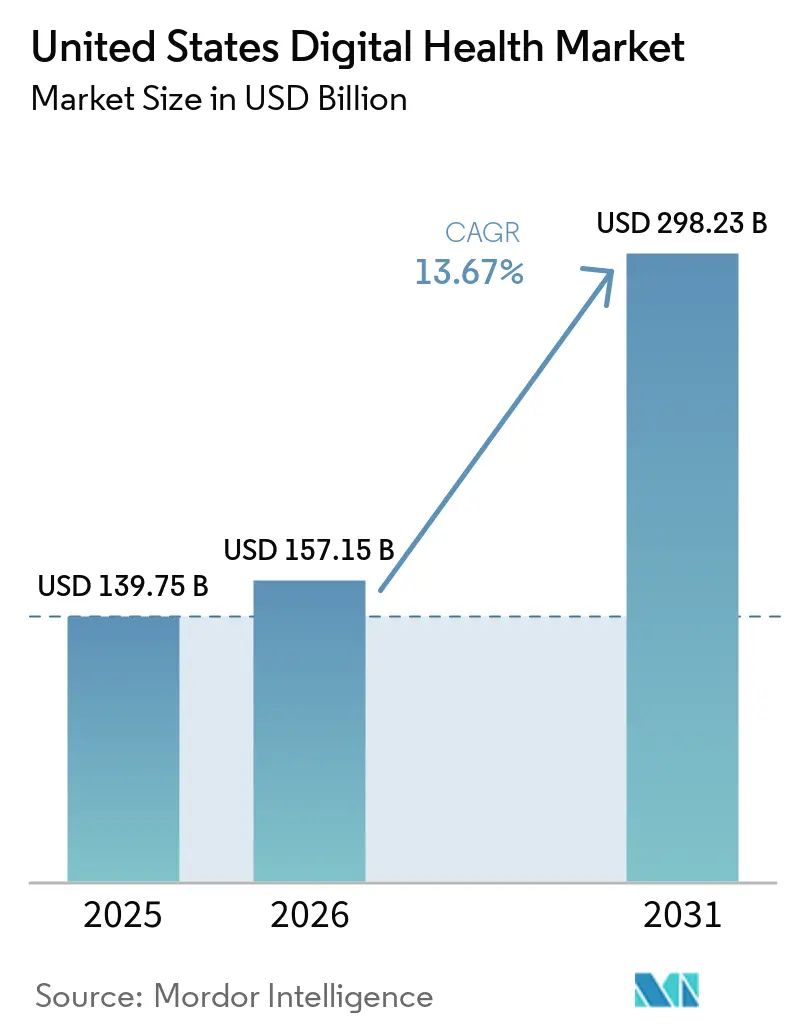

| Base Year Market Size (2025) | USD 139.75 Billion |

| Market Size (2026) | USD 157.15 Billion |

| Market Size (2031) | USD 298.23 Billion |

| Growth Rate (2026 - 2031) | 13.67% CAGR |

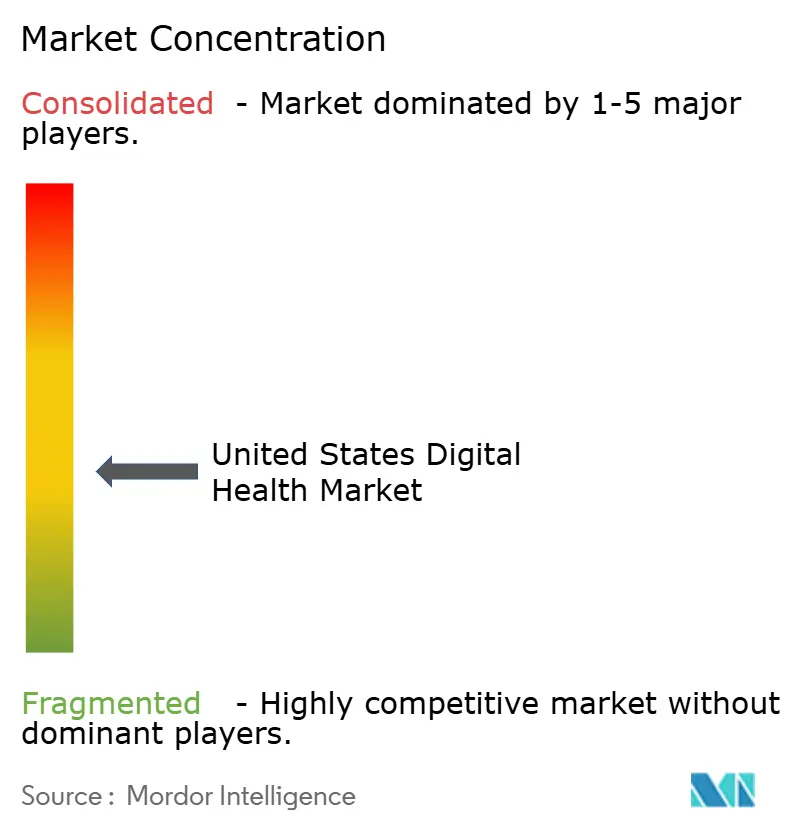

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Digital Health Market Analysis by Mordor Intelligence

The United States Digital Health Market size is expected to increase from USD 139.75 billion in 2025 to USD 157.15 billion in 2026 and reach USD 298.23 billion by 2031, growing at a CAGR of 13.67% over 2026-2031.

The United States digital health market is being reshaped by the lasting normalization of virtual care, wider use of AI in clinical workflows, and federal payment models that reward measurable outcomes rather than activity volume. The pace of adoption has shortened because health systems now see digital tools as operating infrastructure rather than optional innovation, especially in documentation, monitoring, and follow-up care. The market also benefits from stronger evidence that virtual visits often substitute for in-person care, which makes expansion easier to defend to payers and public programs. Large platform companies, EHR vendors, and clinically validated digital health specialists are all competing for the same budget pools, which is pushing the United States digital health market toward tighter integration and clearer proof of value. The main opportunity lies in solutions that can link clinical outcomes, workflow efficiency, and reimbursement in one offering, because buyers remain cautious when returns are delayed.

Key Report Takeaways

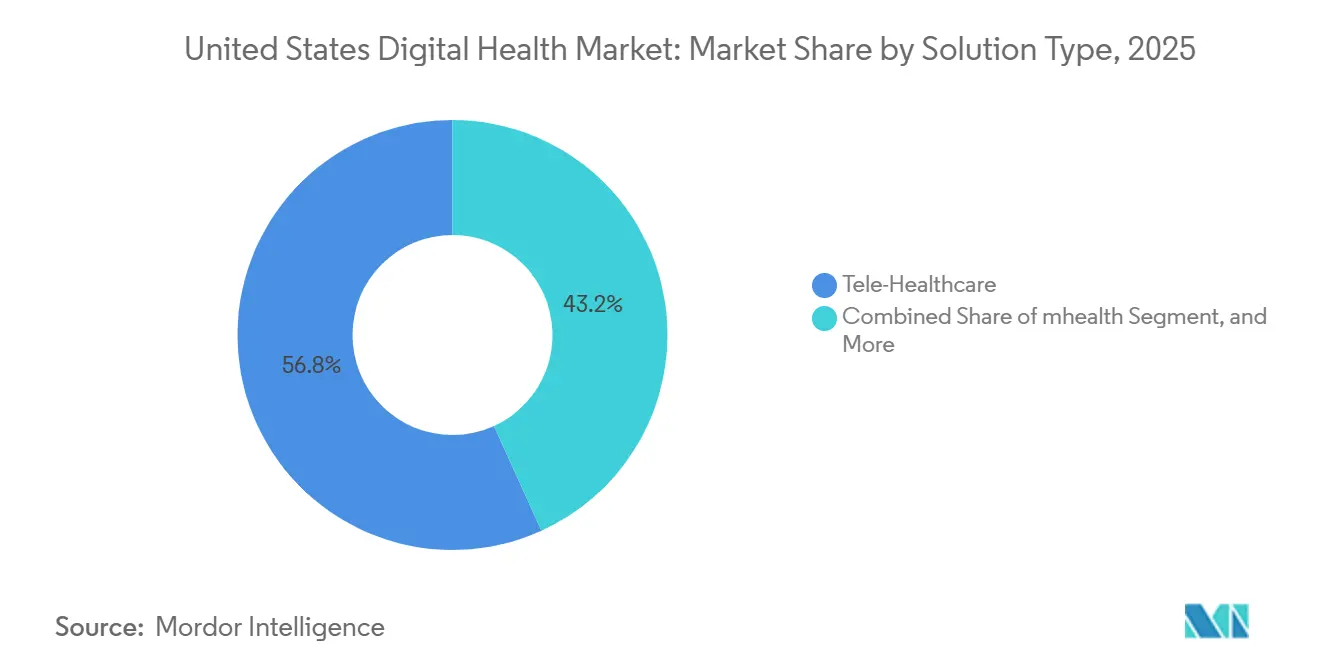

- By solution type, Tele-Healthcare led with 56.76% share in 2025, while mHealth is projected to expand at 14.49% CAGR through 2031.

- By component, Services accounted for 45.73% share in 2025, while Software is forecast to grow at 15.49% CAGR through 2031.

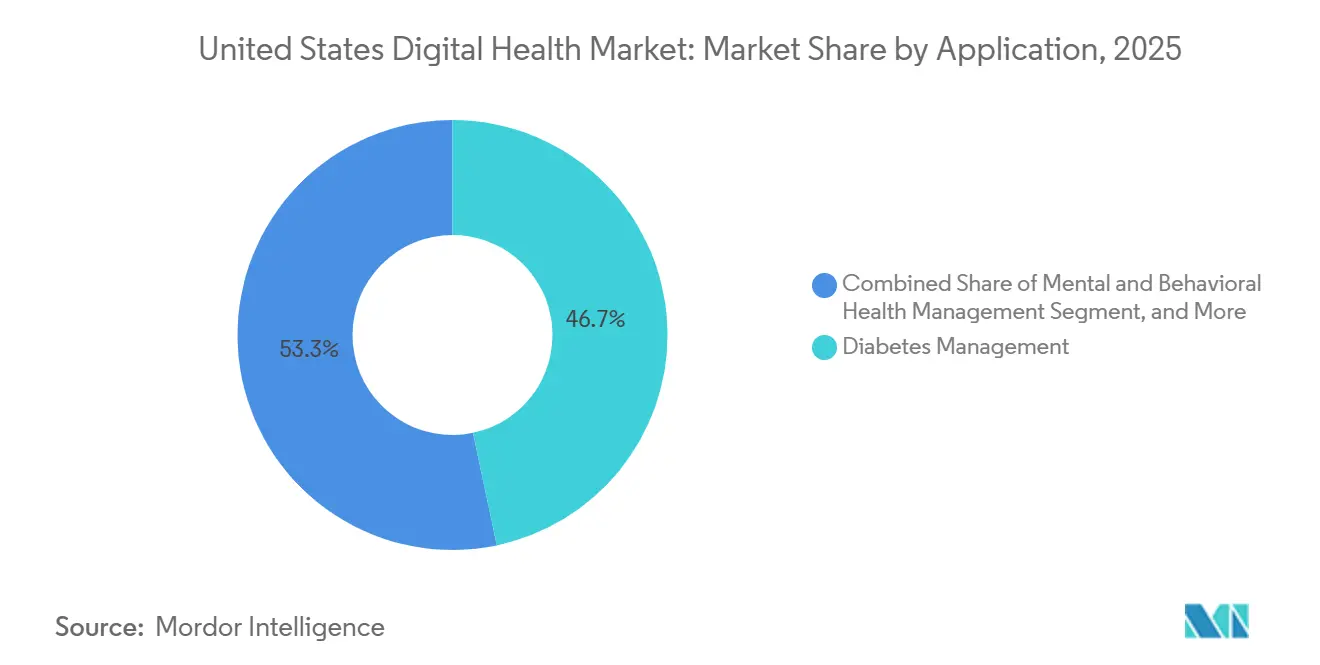

- By application, Diabetes Management held 46.73% share in 2025, while Mental and Behavioral Health Management is expected to advance at 13.72% CAGR through 2031.

- By end user, Patients and Consumers represented 61.74% share in 2025, while Healthcare Providers are projected to grow at 14.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Digital Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Telehealth Normalization Across Care Pathways | +1.9% | National, strongest in underserved rural and suburban markets | Short term (≤ 2 years) |

| Chronic Disease and Aging-Driven Remote Management Demand | +2.4% | National, amplified in Southern and Midwestern states with higher diabetes prevalence | Long term (≥ 4 years) |

| AI-Enabled Workflow Automation and Ambient Documentation Adoption | +2.8% | National, concentrated in metropolitan academic medical centers initially | Medium term (2-4 years) |

| CMS Reimbursement Expansion for RPM, RTM, and Digital Mental Health Tools | +2.1% | National, federal policy with uniform impact across payer types | Short term (≤ 2 years) |

| TEFCA-Scale Interoperability and Real-Time Prior Authorization Enablement | +1.5% | National, early gains in states with advanced HIE participation | Medium term (2-4 years) |

| ACCESS Model and TEMPO Pilot Open Outcome-Based Commercialization Paths | +1.2% | National, first cohort concentrated in Original Medicare fee-for-service markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Telehealth Normalization Across Care Pathways

The United States digital health market continues to benefit from stronger policy support for virtual care across routine care settings. Congress extended Medicare telehealth flexibilities through December 31, 2027, which removed a major near-term policy risk for providers and vendors building care models around virtual access.[1]National Association of Rural Health Clinics, “Telehealth Policy,” National Association of Rural Health Clinics, narhc.org The 2026 Medicare Physician Fee Schedule also made virtual direct supervision and unlimited subsequent inpatient telehealth visits a permanent part of Medicare coverage, which moved key provisions out of the temporary extension cycle. Evidence from the American Telemedicine Association showed a 74% substitution rate for virtual visits across 1.7 million beneficiaries in 25 states, which supports the view that telehealth is replacing a large share of physical visits rather than creating excess use. Teladoc Health’s 2025 benchmark survey also found that hospitals are redesigning virtual care around ongoing engagement instead of one-time access, which supports longer-duration payer contracts and recurring revenue models. Virtual behavioral health remains the clearest near-term use case because the 2026 rule preserved important care delivery flexibility for federally qualified and rural clinics.

Chronic Disease and Aging-Driven Remote Management Demand

The United States digital health market is also being pulled forward by the rising burden of chronic disease and by an aging population that will need more support outside traditional care settings. The Population Reference Bureau reported that the caregiver ratio for Americans aged 80 and older is expected to fall to 3 to 1 by 2040 from 6 to 1 in 2025, which points to a widening service gap that remote management tools can help fill.[2]Population Reference Bureau, “Seven Trends Reshaping the Health and Lifespans of America’s Rapidly Aging Population,” Population Reference Bureau, prb.org CMS launched the ACCESS model on July 5, 2026, and tied it to conditions that affect more than two-thirds of Medicare beneficiaries, including hypertension, diabetes, chronic musculoskeletal pain, and depression. That payment design pushes digital health vendors to show outcomes early, because reimbursement is linked to measurable results rather than simple enrollment or engagement volume. Virta Health reached a USD 200 million annualized revenue run rate in 2026 after several years of clinical evidence building, and its nutrition-based metabolic care model showed improvements in 19 of 21 inflammatory markers in peer-reviewed research. Dexcom also reported 15% year-on-year revenue growth in Q1 2026 after launching the G7 15 Day CGM in the United States, which shows how device innovation and clinical validation can reinforce each other in chronic care programs.

AI-Enabled Workflow Automation and Ambient Documentation Adoption

The United States digital health market is seeing especially fast momentum in AI tools that remove administrative burden inside provider workflows. A June 2025 study found that 62.6% of US hospitals using Epic had already adopted ambient AI documentation tools, which is unusually fast uptake for a clinical technology category.[3]AJMC Staff, “Ambient AI Tool Adoption in US Hospitals and Associated Factors,” The American Journal of Managed Care, ajmc.com A JAMA study cited by the American Hospital Association found that ambient scribes reduced total EHR time by 13.4 minutes and documentation time by 16.0 minutes per encounter, while also increasing weekly visit volume by 0.49 visits per clinician. That combination matters because it links clinician relief with throughput improvement and revenue cycle benefit in the same deployment. Mayo Clinic and Abridge extended ambient AI into nursing documentation in May 2026, which shows the category is moving beyond physician note generation into broader care team workflows. Oracle Health also made its Clinical AI Agent commercially available for inpatient and emergency note generation in March 2026 after earlier ambulatory rollout, which signals that enterprise vendors are making AI a native feature rather than an external layer. As a result, software that can prove fast labor savings is gaining budget priority even when broader IT spending remains selective.

CMS Reimbursement Expansion for RPM, RTM, and Digital Mental Health Tools

The United States digital health market is getting an added boost from reimbursement changes that widen the path from clinical use to paid deployment. CMS has expanded its support for outcome-based chronic care management through the ACCESS model, which gives digital programs a clearer route into Original Medicare for high-burden conditions. The 2026 Medicare policy cycle also advanced virtual care coverage and preserved key flexibilities that make remote delivery practical for providers serving dispersed populations. The American Telemedicine Association highlighted that the 2026 draft fee schedule expanded digital mental health treatment reimbursement to include ADHD devices, which marked a meaningful extension of Medicare payment support for software-guided care. This matters most in behavioral health, where provider shortages are deep and software can extend care capacity faster than physical networks can grow. The policy direction also supports more durable commercialization for digital therapeutics and remote management platforms, because buyers can now tie adoption decisions more closely to reimbursement readiness and clinical outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and Health-Data Breach Exposure | -1.2% | National, amplified in states with high concentration of small provider practices and independent business associates | Short term (≤ 2 years) |

| Reimbursement Variability and Proof-of-ROI Pressure | -1.0% | National, most acute in commercial and Medicare Advantage markets | Medium term (2-4 years) |

| State-by-State Privacy and Consumer Health Data Compliance Patchwork | -0.8% | National with geographic variation, most restrictive in Washington, Nevada, and Connecticut | Medium term (2-4 years) |

| Point-Solution Sprawl and EHR Integration Bottlenecks | -1.1% | National, most acute in mid-size health systems with mixed-vendor environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Health-Data Breach Exposure

Cybersecurity remains a major drag on adoption because buyers treat health data risk as both a financial and a clinical issue. The American Hospital Association reported in 2025 that more than 80% of stolen protected health information records came from third-party vendors and business associates rather than the core EHR, which shifts attention toward external integrations and vendor controls. That pattern is important in the United States digital health market because many solutions depend on multiple data exchanges across software vendors, monitoring devices, claims systems, and care delivery partners. It also means procurement cycles are becoming more security heavy, especially when health systems are evaluating smaller vendors without long operating histories. The practical effect is slower onboarding, more contract review, and higher implementation cost. Vendors that cannot support enterprise-grade security expectations are likely to face added friction even when their clinical use case is compelling.

Point-Solution Sprawl and EHR Integration Bottlenecks

The United States digital health market also faces friction from the growing number of narrow tools competing for limited implementation capacity inside health systems. TechTarget reported in 2026 that 51% of health systems were spending 11% to 25% of IT bandwidth on vendor management, integration, and implementation, which shows how much hidden cost sits behind digital adoption. This weakens the appeal of stand-alone products because many provider organizations now prefer tools that fit inside existing workflows instead of adding another management layer. The problem is more acute in mixed-vendor environments, where integration work competes directly with funding for care programs and staff support. As a result, platform-native tools from major EHR vendors and scaled operators hold an advantage over single-point offerings that still require heavy local configuration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Tele-Healthcare Anchors Revenue, mHealth Accelerates

Tele-Healthcare held 56.76% of the United States digital health market in 2025, which kept it as the largest solution segment by revenue. That position reflects long-standing investment in virtual urgent care, primary care, specialty care, and behavioral care delivery. The segment is now supported by policy continuity, because Medicare telehealth flexibilities have been extended and key virtual supervision and inpatient visit provisions have been made permanent. The United States digital health market size for Tele-Healthcare remained anchored by the depth of payer and employer benefit integration already built around virtual access in 2025. Teladoc’s BetterHelp transition toward an insurance-covered model and its targeted run rate of at least USD 125 million in insurance revenue by Q4 2026 show that behavioral telehealth is moving toward closer payer alignment. Virtual specialty care is also gaining room because it can help address shortages in endocrinology, cardiology, and psychiatry without requiring new physical capacity.

mHealth is the fastest-growing solution segment, with the United States digital health market size for mHealth projected to expand at 14.49% CAGR through 2031. Demand is being led by CGM adoption, wearable cardiac monitoring, and mobile applications that support continuous engagement instead of episodic intervention. Dexcom raised its 2026 revenue outlook to USD 5.2 billion to USD 5.3 billion after the US launch of G7 15 Day and the FDA clearance of Smart Basal, which shows continued strength in connected metabolic care. The Stelo over-the-counter platform is also broadening the addressable base beyond insulin users, and Prime Therapeutics will begin covering CGM for all people with diabetes from summer 2026, including more than 7 million type 2 non-insulin lives. In the US digital health industry, this shifts value toward solutions that can stay with patients between visits and generate usable data for both consumers and clinicians.

By Component: Services Dominant, Software Outpacing

Services accounted for 45.73% of the United States digital health market in 2025, which made it the largest component segment. This reflects the reality that implementation, workflow redesign, training, and managed support remain necessary for digital tools to deliver lasting clinical and financial value. Many provider organizations still face internal capacity limits, so service layers continue to act as the practical bridge between software purchase and real-world use. The US digital health market share in this segment stayed high because technology alone rarely solves integration, operational change, or care coordination challenges. This also explains why enterprise buyers often favor vendors that can combine product capability with deployment support.

Software is the fastest-growing component segment at 15.49% CAGR through 2031, and it is benefiting most from ambient documentation, analytics, revenue cycle automation, and patient engagement use cases. Oracle’s AI-native ambulatory EHR received ASTP/ONC certification in 2025, and the company expanded its Clinical AI Agent into inpatient and emergency settings in 2026, which shows how quickly AI is being built into core systems. Amazon One Medical also set a new benchmark for patient-facing digital engagement when it launched Health AI and later extended it to all US Amazon customers in 2026. Hardware remains supported by monitoring device volumes, but price pressure on sensors is limiting differentiation at the commodity end. In the US digital health industry, software is capturing more value because it can connect clinical evidence, workflow efficiency, and patient engagement in a single layer.

By Application: Diabetes Leads, Behavioral Health Accelerates

Diabetes Management captured 46.73% of the United States digital health market in 2025, which made it the most concentrated application segment. That share reflects both the scale of the condition and the maturity of the connected ecosystem built around CGM, insulin optimization, and software-led coaching. The American Diabetes Association’s 2026 standards recommended CGM access for all people with diabetes across payer types, which strengthens the reimbursement and coverage case for connected diabetes programs. Glooko received FDA 510(k) clearance in May 2026 for EndoTool IV Cloud, the first FDA-cleared cloud-based patient-specific insulin dosing platform for intravenous insulin management in hospitals, which extends diabetes digitization into acute care settings. Cardiometabolic and obesity management is also gaining support from the GLP-1 cycle, and Omada’s integration into Eli Lilly’s Employer Connect program shows how digital coaching and prescribing support are being paired more tightly. The US digital health market size for Diabetes Management remains larger than any other application because the condition already has validated devices, recurring engagement, and broad payer interest.

Mental and Behavioral Health Management is the fastest-growing application segment at 13.72% CAGR through 2031. Growth is being supported by persistent provider shortages and by expanding willingness to reimburse software-mediated treatment pathways. The American Telemedicine Association noted that CMS expanded digital mental health treatment reimbursement to include ADHD devices in the 2026 draft fee schedule, which widened the federal payment base for this category. Preventive wellness and fitness still carries large user volume, but its revenue quality is lower because it depends more on consumer or employer willingness to pay. In the US digital health market, behavioral health stands out because it combines high unmet need, easier virtual delivery, and growing reimbursement support. That mix is likely to keep the segment ahead of other applications where clinical value may be clear but payment pathways remain narrower.

By End User: Consumer-Led Demand, Provider-Side Growth Accelerating

Patients and Consumers represented 61.74% of the United States digital health market in 2025, which made them the largest end-user group. This reflects the scale of direct-to-consumer demand for apps, wearables, digital memberships, and self-managed chronic care tools. Amazon widened this addressable base in 2026 by extending Health AI beyond One Medical members to all US Amazon customers and by linking eligible Prime users to direct-message consultation options. Consumer demand is important because it reduces dependence on formal provider referrals and opens room for self-directed spending on prevention, monitoring, and low-friction care access. The United States digital health market share for Patients and Consumers stayed high because many tools now enter daily life through retail, subscription, and device channels rather than through traditional clinical procurement.

Healthcare Providers are the fastest-growing end-user segment at 14.68% CAGR through 2031. Provider adoption is being driven by workforce shortages, clinician burnout, and the need to manage more patients without expanding labor at the same pace. Ambient documentation, workflow automation, and chronic care monitoring are especially attractive because they address staffing constraints and value-based care goals at the same time. CMS’s ACCESS model will reinforce this shift by giving provider organizations stronger economic reason to operate tech-enabled chronic care programs inside Medicare. Payers, employers, and plan sponsors remain active buyers, but they are becoming more selective and increasingly prefer integrated platforms over narrow point solutions. This is pushing the United States digital health market toward vendors that can align clinical value, workflow fit, and measurable financial return.

Geography Analysis

Federal reimbursement policy matters everywhere, but the impact is especially visible in rural and suburban areas where telehealth fills access gaps more directly. Medicare’s extension of telehealth flexibilities and the permanence of selected virtual care provisions support continued use in communities where travel, specialist shortages, and limited clinic capacity remain common barriers. The American Telemedicine Association’s findings across 25 states also suggest that virtual care has become a normalized part of care delivery rather than a temporary supplement. This gives the US digital health market a national demand base even when local implementation speed varies.

Metropolitan academic medical centers are the earliest concentration points for advanced AI workflow tools. Ambient AI documentation adoption was already present in 62.6% of Epic-using hospitals by June 2025, and early uptake was strongest in large institutional settings with the scale to test and expand new tools quickly. The geography of chronic care demand looks different, because Southern and Midwestern states carry heavier diabetes prevalence and therefore stronger pull for CGM-linked and remote monitoring solutions. This means the US digital health market is shaped by two regional demand patterns at the same time, one tied to advanced provider infrastructure and one tied to chronic disease burden. National suppliers that can serve both patterns are likely to have a wider runway than vendors built around only one use case.

Policy and compliance variation also creates important geographic differences inside a national market. States with stronger health information exchange participation are likely to realize interoperability gains sooner, while privacy-heavy jurisdictions such as Washington, Nevada, and Connecticut can raise compliance demands for consumer-facing offerings. Original Medicare fee-for-service markets are particularly relevant for the ACCESS model, because they provide the earliest setting for outcome-aligned chronic care commercialization. The US digital health market therefore combines a national policy floor with state-level variation in data governance, care access, and implementation readiness. Over time, this should favor vendors that can adapt their deployment model to local operational conditions without changing core clinical workflows.

Competitive Landscape

The United States digital health market remains moderately fragmented, because no single company controls the full range of telehealth, monitoring, EHR, analytics, digital therapeutics, and consumer engagement. Large infrastructure vendors such as Epic Systems and Oracle Health hold a structural advantage in workflow ownership, while platform companies such as Amazon are using consumer reach to build new care access models. Oracle strengthened its position by commercializing the Clinical AI Agent for inpatient and emergency documentation in March 2026 after earlier ambulatory rollout, which moved AI deeper into core provider workflows. Amazon expanded Health AI from One Medical members to all US Amazon customers in 2026, which gave it a wider direct channel into consumer health engagement. These moves show that competition is no longer limited to one segment, because companies are building across care delivery, workflow, and engagement at the same time.

Public market activity also signals that outcome-backed specialists are regaining commercial relevance. Hinge Health guided for 2026 revenue of USD 732 million to USD 742 million, which implied 25% growth at the midpoint and showed that musculoskeletal digital care can still scale when outcomes are credible. Omada Health guided for 2026 revenue of USD 322 million to USD 330 million, and its Lilly partnership linked digital cardiometabolic support more directly with employer benefit design. Virta Health also passed a USD 200 million annualized revenue run rate in 2026 after building a long evidence base, which reinforces the market preference for vendors that can defend both outcomes and unit economics. This leaves less room for companies that still rely mainly on engagement claims without clinical or financial validation.

White space remains strongest where care coordination, senior care, and social factors intersect, because those needs cut across reimbursement categories and are still not well served by isolated products. The ACCESS model creates a more durable revenue path for tech-enabled chronic care in conditions such as diabetes, hypertension, obesity, depression, and anxiety, which could pull more vendors toward integrated, outcomes-based offerings. The main strategic divide is becoming clear. Vendors with deep integration, evidence, and reimbursement fit are gaining share of buyer attention. Vendors operating as stand-alone point solutions face more resistance because implementation cost, cybersecurity review, and ROI pressure are all rising. In the US digital health market, that dynamic favors scaled platforms, clinical evidence leaders, and companies that can fit inside enterprise workflows without adding new operational burden.

United States Digital Health Industry Leaders

athenahealth

Epic Systems Corporation

Medtronic

Oracle Health

Veradigm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Glooko received FDA 510(k) clearance for EndoTool IV Cloud, the first FDA-cleared cloud-based patient-specific intravenous insulin dosing platform for hospital settings, with commercial launch expected before year-end 2026 in the United States. This extends the connected diabetes management ecosystem from ambulatory CGM into acute inpatient care, creating a new market layer for hospital-grade digital diabetes tools.

- May 2026: Virta Health published peer-reviewed research in Endocrine Research demonstrating broad, sustained reductions in 19 of 21 inflammatory markers following one year of nutrition-based metabolic therapy, strengthening the clinical evidence base as the company prepared for a 2026 IPO at a USD 200 million annualized revenue run rate.

- May 2026: Mayo Clinic and Abridge co-developed an ambient AI documentation solution for nursing workflows, capturing nurse-patient conversations and generating structured EHR draft notes in real time, the first major extension of ambient AI from physician to nursing documentation at a flagship academic medical center.

- May 2026: Omada Health was announced as an independent program administrator in Eli Lilly's Employer Connect program, integrating its GLP-1 Care Track and prescribing capabilities into Lilly's direct-to-employer platform, signaling a new category of pharma-digital health partnerships that pair GLP-1 access with structured virtual lifestyle support.

United States Digital Health Market Report Scope

The digital health market encompasses the software platforms, connected medical devices, and services that enable remote, data-driven, and virtual delivery of healthcare. This rapidly expanding industry aims to enhance care quality, lower costs, and make healthcare systems globally more efficient.

The United States Digital Health Market is Segmented by Solution Type (Tele-Healthcare, mHealth, Digital Health Systems, Healthcare Analytics and Clinical AI, Digital Therapeutics), Component (Software, Hardware, Services), Application (Diabetes Management, Cardiometabolic and Obesity Management, Cardiovascular Monitoring, Mental and Behavioral Health, Respiratory Care, Preventive Wellness, Women's Health, Medication Management), and End User (Healthcare Providers, Payers, Patients and Consumers, Employers and Plan Sponsors). The Market Forecasts are Provided in Terms of Value (USD).

| Tele-Healthcare | Telemedicine |

| Virtual Urgent Care | |

| Virtual Primary Care | |

| Virtual Specialty Care | |

| Virtual Behavioral Health | |

| mhealth | Wearables and Connected Medical Devices |

| Mobile Health Applications | |

| Medication Adherence and Care-Navigation Apps | |

| Digital Health Systems | EHR / EMR Platforms |

| E-Prescribing Systems | |

| Health Information Exchange | |

| Patient Portals and Personal Health Records | |

| Healthcare Analytics and Clinical AI | Clinical Decision Support |

| Population Health and Risk Analytics | |

| Revenue Cycle and Administrative AI | |

| Ambient Documentation and Coding AI | |

| Digital Therapeutics | Mental and Behavioral Health Therapeutics |

| ADHD and Neurobehavioral Therapeutics | |

| Sleep and Insomnia Therapeutics | |

| Metabolic And Lifestyle Therapeutics |

| Software | Clinical Platforms |

| Patient Engagement Software | |

| Analytics and AI Software | |

| Hardware | Wearables |

| Connected Monitoring Devices | |

| Edge Devices and Gateways | |

| Services | Implementation And Integration |

| Managed Clinical Services | |

| Support And Optimization Services |

| Diabetes Management |

| Cardiometabolic and Obesity Management |

| Cardiovascular Monitoring and Management |

| Mental and Behavioral Health Management |

| Respiratory Care Management |

| Preventive Wellness and Fitness |

| Women’s Health |

| Medication Management and Adherence |

| Healthcare Providers |

| Payers |

| Patients and Consumers |

| Employers and Plan Sponsors |

| By Solution Type | Tele-Healthcare | Telemedicine |

| Virtual Urgent Care | ||

| Virtual Primary Care | ||

| Virtual Specialty Care | ||

| Virtual Behavioral Health | ||

| mhealth | Wearables and Connected Medical Devices | |

| Mobile Health Applications | ||

| Medication Adherence and Care-Navigation Apps | ||

| Digital Health Systems | EHR / EMR Platforms | |

| E-Prescribing Systems | ||

| Health Information Exchange | ||

| Patient Portals and Personal Health Records | ||

| Healthcare Analytics and Clinical AI | Clinical Decision Support | |

| Population Health and Risk Analytics | ||

| Revenue Cycle and Administrative AI | ||

| Ambient Documentation and Coding AI | ||

| Digital Therapeutics | Mental and Behavioral Health Therapeutics | |

| ADHD and Neurobehavioral Therapeutics | ||

| Sleep and Insomnia Therapeutics | ||

| Metabolic And Lifestyle Therapeutics | ||

| By Component | Software | Clinical Platforms |

| Patient Engagement Software | ||

| Analytics and AI Software | ||

| Hardware | Wearables | |

| Connected Monitoring Devices | ||

| Edge Devices and Gateways | ||

| Services | Implementation And Integration | |

| Managed Clinical Services | ||

| Support And Optimization Services | ||

| By Application | Diabetes Management | |

| Cardiometabolic and Obesity Management | ||

| Cardiovascular Monitoring and Management | ||

| Mental and Behavioral Health Management | ||

| Respiratory Care Management | ||

| Preventive Wellness and Fitness | ||

| Women’s Health | ||

| Medication Management and Adherence | ||

| By End User | Healthcare Providers | |

| Payers | ||

| Patients and Consumers | ||

| Employers and Plan Sponsors | ||

Key Questions Answered in the Report

What is the projected value of the United States digital health space by 2031?

It is forecast to reach USD 298.23 billion by 2031, rising from USD 157.15 billion in 2026 at a 13.67% CAGR.

Which solution category currently generates the most revenue?

Tele-Healthcare leads with 56.76% share in 2025, supported by deep use in virtual primary, specialty, and behavioral care.

Which part of the ecosystem is growing the fastest?

Software is the fastest-growing component at 15.49% CAGR, while mHealth leads solution growth at 14.49% CAGR through 2031.

Why is diabetes such a large use case in this space?

Diabetes Management held 46.73% share in 2025 because the category already has strong connected device adoption, validated software, and payer support.

Why are providers increasing digital tool adoption so quickly?

Providers are using these tools to reduce documentation burden, manage workforce shortages, and support value-based care models such as CMS ACCESS.

Page last updated on: