United States Digital Twin Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

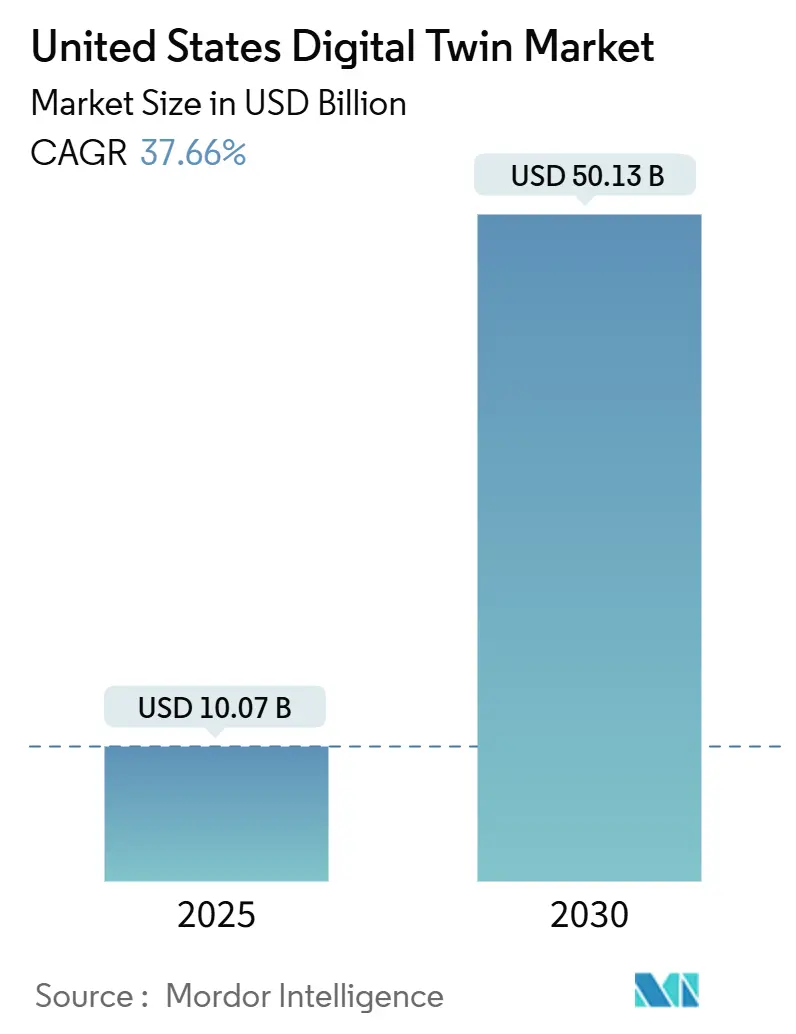

| Market Size (2025) | USD 10.07 Billion |

| Market Size (2030) | USD 50.13 Billion |

| Growth Rate (2025 - 2030) | 37.66% CAGR |

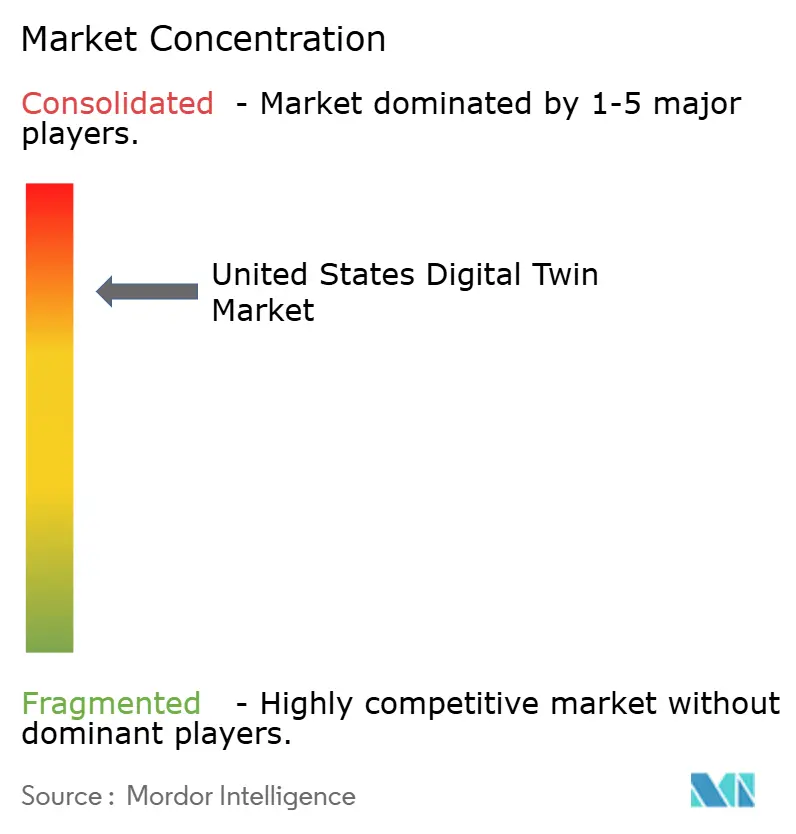

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Digital Twin Market Analysis by Mordor Intelligence

The United States digital twin market size is USD 10.07 billion in 2025 and is projected to reach USD 50.13 billion by 2030, reflecting a 37.66% CAGR. Growth stems from federal infrastructure mandates, semiconductor-fab subsidies and fast-track medical regulations that reposition twins as strategic infrastructure rather than optional analytics tools. Manufacturing adoption remains strong, but rapid uptake in smart-city, healthcare and utility projects is broadening demand. Cloud hyperscalers continue to bundle twin-ready Internet-of-Things (IoT) suites, compressing deployment timelines while creating data-gravity lock-ins. At the same time, hybrid architectures are expanding quickly as enterprises balance latency, compliance and cybersecurity requirements. GPU tariffs that raise simulation costs, together with brownfield integration complexity, temper the market’s near-term trajectory but do not offset its structural momentum.

Key Report Takeaways

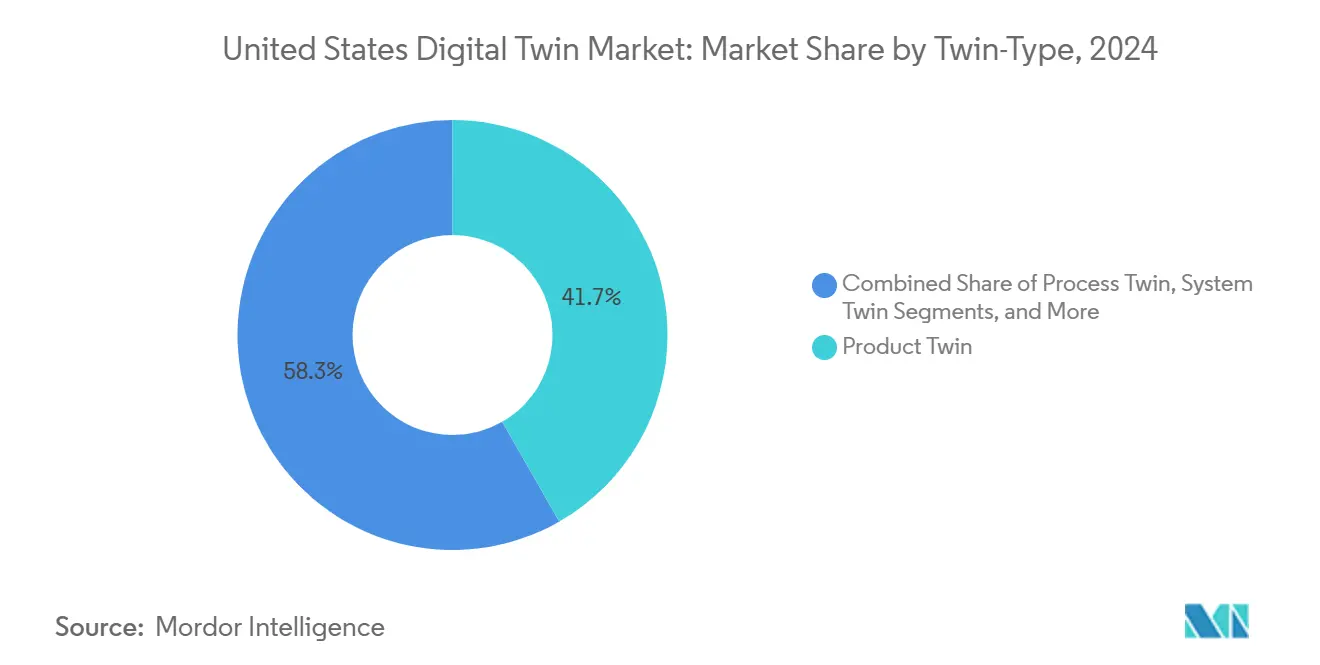

- By twin-type, product twins held 41.73% of the US digital twin market share in 2024; system twins are advancing at a 38.44% CAGR through 2030.

- By application, predictive maintenance accounted for 38.85% share of the US digital twin market size in 2024, while business workflow optimization is forecast to grow at a 38.11% CAGR to 2030.

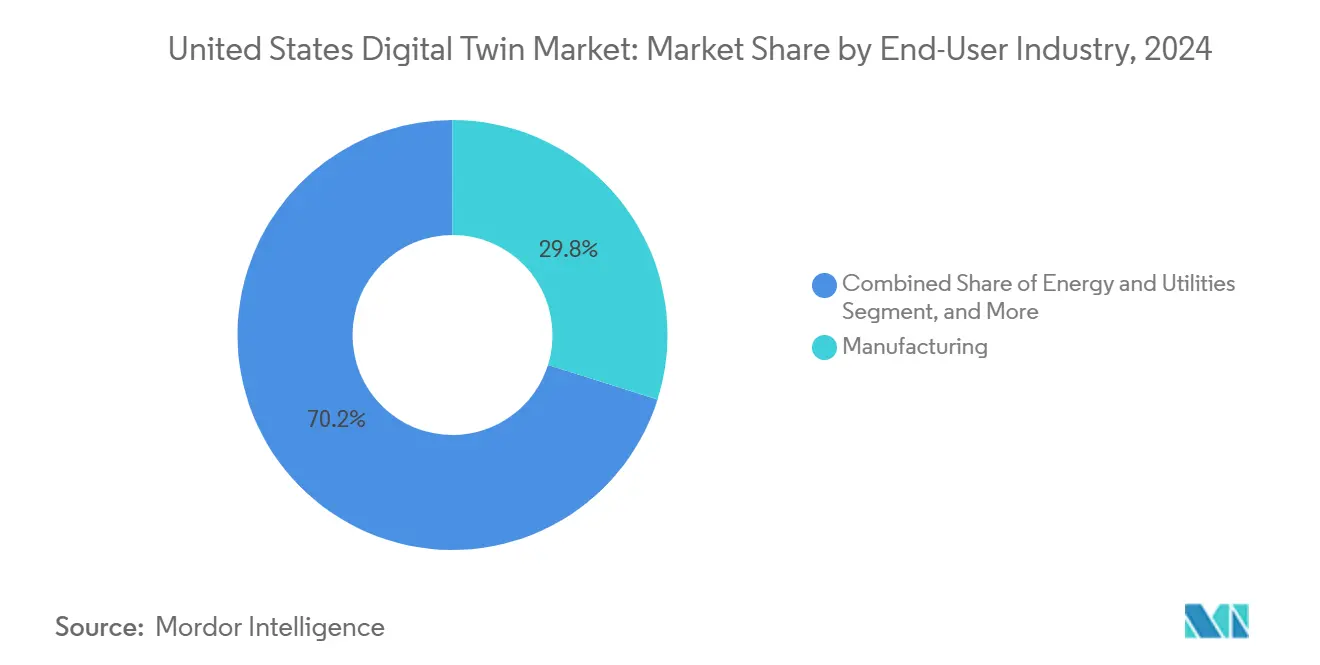

- By end-user industry, manufacturing led with 32.83% share of the US digital twin market size in 2024 and is expanding at a 37.99% CAGR between 2025-2030.

- By deployment model, cloud deployment captured 70.62% revenue share in 2024 in the US digital twin market; hybrid architectures record the highest projected CAGR at 39.11% through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on digital twin (dt) market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Digital Twin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of predictive-maintenance twins across US manufacturing | +6.2% | National, concentrated in Midwest industrial belt | Medium term (2-4 years) |

| Cloud hyperscalers bundling twin-ready IoT suites | +4.8% | National, with early gains in tech hubs | Short term (≤ 2 years) |

| Federal infrastructure and smart-city funding mandates twin deliverables | +3.1% | National, prioritizing underserved communities | Long term (≥ 4 years) |

| FDA fast-track pathways for patient-specific surgical-planning twins | +2.9% | National, concentrated in medical device clusters | Medium term (2-4 years) |

| US semiconductor-fab subsidies requiring digital twins for yield optimization | +2.7% | Southwest and Northeast fab locations | Long term (≥ 4 years) |

| Insurer discounts for facilities using energy-efficiency twins | +1.8% | National, emphasis on high-risk climate zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Predictive-Maintenance Twins Across US Manufacturing

Unplanned downtime costs in automotive and aerospace facilities reach USD 50,000 per hour, motivating the shift from reactive to prescriptive maintenance. Digital twins simulate multiple failure modes and sequence repairs during production gaps, cutting maintenance expenses by 30% when integrated with enterprise resource planning systems. Declining IoT-sensor prices, falling 40% annually, extend these capabilities to mid-market manufacturers, widening the US digital twin market’s addressable base. Early adopters then refine proprietary algorithms that synchronize asset health with delivery schedules, creating durable competitive moats. National rollouts concentrate in the Midwest, where suppliers cluster around automotive and heavy-machinery OEMs.

Cloud Hyperscalers Bundling Twin-Ready IoT Suites

Microsoft Azure Digital Twins and Amazon IoT TwinMaker embed modeling, visualization and data-ingestion functions into existing cloud subscriptions, reducing integration work and elevating switching costs. Pre-configured industry templates shorten deployment timelines to six months and attract small-to-medium enterprises that lack dedicated IT teams. As workloads accrue, data gravity encourages broader cloud migration, deepening platform stickiness and lifting lifetime customer value. Hyperscalers also partner with industrial-automation vendors to embed edge services inside factory hardware, further weaving the US digital twin market into core operational technology stacks.

Federal Infrastructure and Smart-City Funding Mandates Twin Deliverables

The Infrastructure Investment and Jobs Act ties funding for projects above USD 50 million to the delivery of interoperable digital twins.[1]U.S. Department of Transportation, “Biden Administration Announces Nearly $5 Billion Available to States and Communities,” transportation.gov The stipulation injects long-term demand into the US digital twin market, especially for water, transit and energy projects in underserved communities. Cities increasingly favor end-to-end platforms over point solutions, elevating vendors with proven government-contracting credentials. States such as California augment federal directives with their own mandates for water-infrastructure twins, creating a cascade of compliance-driven projects across utilities. Smaller software firms without public-sector experience face higher bid-participation costs, nudging market consolidation.

FDA Fast-Track Pathways for Patient-Specific Surgical-Planning Twins

The 2024 FDA guidance shortens approval cycles from 24 months to eight months, encouraging medical-device firms to embed twins in surgical workflows.[2]U.S. Food and Drug Administration, “Digital Twins for Medical Devices,” fda.gov Early clinical studies show a 25% fall in operative complications when surgeons plan procedures with anatomical twins. Vendors able to validate outcomes through real-world evidence gain a regulatory edge, and platforms with large patient-outcome datasets command premium valuations. Cardiovascular and orthopedic specialties are the immediate beneficiaries, but oncology and neurology are slated for inclusion as validation frameworks mature. The policy cements healthcare as a high-growth node inside the wider US digital twin market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and IP-protection concerns | -2.7% | National, acute in defense and healthcare sectors | Short term (≤ 2 years) |

| Integration complexity with brown-field legacy systems | -1.8% | National, concentrated in mature industrial regions | Medium term (2-4 years) |

| Shortage of "model-governance" auditors slowing regulated deployments | -1.4% | National, particularly Northeast financial and healthcare hubs | Medium term (2-4 years) |

| Rising GPU tariffs inflating compute costs for high-fidelity twins | -1.2% | National, with higher impact on compute-intensive applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and IP-Protection Concerns

Connected twins enlarge attack surfaces, and 67% of industrial firms reported related incidents in 2024.[3]Cybersecurity and Infrastructure Security Agency, “Cybersecurity Advisory AA24-102A,” cisa.gov Defense contractors must isolate sensitive data under International Traffic in Arms Regulations, leading many to favor on-premises or hybrid deployments despite cloud cost advantages. Smaller vendors often lack dedicated security teams, adding compliance overhead that narrows their competitive field. These pressures shape purchasing criteria, with certifications such as FedRAMP becoming gating factors for public-sector opportunities and for high-risk industries inside the expanding US digital twin market.

Integration Complexity with Brown-Field Legacy Systems

Plants averaging 15-20 years of service rely on diverse protocols and proprietary data formats. Integrating legacy programmable-logic controllers (PLCs) with real-time twin platforms inflates project costs by up to 60% relative to greenfield builds.[4]National Institute of Standards and Technology, “NIST Releases Framework for Digital Twin Manufacturing Systems,” nist.gov Vendors capable of delivering end-to-end hardware, middleware and services become preferred partners as buyers seek single-throat accountability. Mid-market companies with limited IT resources gravitate toward pre-assembled gateway kits and low-code interfaces, but sustained demand still leans toward mature providers with extensive installed bases. This dynamic underpins the US digital twin market’s moderate fragmentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Twin-Type: System Twins Accelerate Holistic Optimization

System twins account for 38.44% CAGR from 2025-2030 as enterprises pivot from component monitoring to asset orchestration. A leading wind-farm operator lifted overall energy output by 10% after coordinating turbine controls through a system-level twin, a return that justifies premium software fees. Meanwhile, product twins retain the largest 2024 share at 41.73%, especially in aerospace and automotive where geometric precision guides high-tolerance fabrication. Process‐level twins gain traction in continuous operations such as chemical blending, optimizing recipes against fluctuating input costs. Asset- and component-level models remain valuable for niche maintenance but risk commoditization as sensor prices fall and analytics libraries standardize.

System twins elevate the US digital twin market by creating network effects: each new connected machine multiplies potential operational combinations, raising the marginal utility of the platform. Early adopters use this connectivity to simulate scheduling scenarios, production routing and energy loads simultaneously, boosting enterprise-wide efficiency. Vendors that can translate real-time telemetry into actionable system-level insights therefore gain durable pricing power, widening the performance gap between integrated suites and standalone visualization tools.

By Application: Business Optimization Redefines Operational Intelligence

Predictive maintenance held 38.85% share of the US digital twin market size in 2024 thanks to clear cost-avoidance value. However, business workflow optimization is climbing at 38.11% CAGR through 2030 as firms extend simulation beyond equipment health to supply-chain resilience and inventory allocation. Performance-monitoring twins often serve as an entry step, delivering visibility before broader decision support. Product-design twins shorten time-to-market by virtualizing prototypes, allowing engineers to iterate digitally rather than through costly physical testing.

The shift toward enterprise-scale optimization underscores digital twins’ maturation from descriptive dashboards to prescriptive engines. Consulting partners package domain models, such as discrete factory sequencing or energy-grid balancing, into reusable libraries. As these libraries accumulate real-world feedback, recommendation engines improve, weaving continuous-improvement cycles directly into operations. This evolution embeds twin technology at the strategy layer of organizations, escalating its centrality to the US digital twin market.

By End-User Industry: Manufacturing Sustains Dual Leadership

Manufacturing commanded 32.83% revenue share in 2024 and remains the fastest-expanding vertical at 37.99% CAGR, illustrating both scale and speed. Aerospace primes demand for high-fidelity simulation, while automotive OEMs deploy twins to synchronize just-in-time logistics with plant automation. Healthcare accelerates on the back of FDA clarity; hospitals model patient flows, surgical outcomes and equipment utilization. Utilities deploy grid twins to manage renewable intermittency and forecast maintenance windows for aging transmission assets.

Manufacturing’s integrative posture, spanning product lifecycle, production, quality and after-sales service, creates sticky ecosystems that favor full-suite suppliers. Large enterprises integrate twins into enterprise resource planning and manufacturing execution systems, establishing cyber-physical loops that automatically refine production parameters. These embedded feedback cycles embed twin solutions deeply into corporate DNA, reinforcing the segment’s dominance within the broader US digital twin market.

By Deployment Model: Hybrid Architectures Blend Performance With Control

Cloud platforms hold 70.62% share in 2024 due to hyperscaler economics and managed services that slash total cost of ownership for smaller firms. Hybrid solutions outpace all others at 39.11% CAGR thanks to the need for on-site latency management and data-sovereignty compliance. High-value production lines process control loops at the edge while delegating AI model training and long-term analytics to the cloud. Defense and pharmaceutical operators maintain strictly on-premises clusters to meet regulatory safeguards, showing that deployment choices map closely to risk tolerance.

Major vendors now ship converged offerings, Azure Stack for Microsoft, Outposts for Amazon, that extend identical application programming interfaces from core cloud to customer edge. This consistency reduces integration friction and accelerates project rollout. As 5G private networks proliferate, edge nodes acquire greater compute density, paving a migration path for even more twin workloads. The resulting architectural flexibility underpins widening adoption across multiple industries, sustaining momentum in the US digital twin market.

Geography Analysis

The South dominates current installations, buoyed by aerospace clusters in Texas, Alabama and Florida plus energy-infrastructure upgrades tied to federal grid-modernization grants. Semiconductor fabs in Arizona and Texas, financed under the CHIPS Act, embed yield-optimization twins during tool-install phases, creating anchor projects that ripple across supplier ecosystems. Favorable state incentives and right-to-work statutes accelerate new plant construction, concentrating early demand for system-level twins that orchestrate greenfield operations.

The Northeast retains research heft and domain expertise. Massachusetts hosts medical-device innovators and university labs that prototype algorithmic twins for personalized medicine [MIT.EDU]. New York financial institutions experiment with operational-risk twins that stress-test transaction flows against cyber or market shocks. Brownfield industrial bases in Pennsylvania and New Jersey require deep integration services, permitting higher professional-services margins for vendors. FDA headquarters in Maryland accelerates clinical validation workflows, reinforcing healthcare’s regional prominence.

The Midwest, rooted in automotive and heavy machinery, drives discrete-manufacturing use cases. Michigan, Ohio and Illinois refit stamping and assembly lines with asset-level twins, moving steadily toward plant-wide system models. Clustering of Tier-1 suppliers promotes data-sharing standards that streamline multi-enterprise simulations. The West concentrates platform development: Silicon Valley startups design twin engines, while Washington’s aerospace giants implement large-scale operational twins. Cross-regional collaboration emerges as vendors headquartered on the coasts partner with manufacturing customers in the interior, propagating best practices throughout the US digital twin market.

Competitive Landscape

Competition falls into three tiers. Industrial-automation incumbents, General Electric, Siemens, Rockwell Automation, leverage deep domain expertise and installed hardware to upsell twin-enabled software extensions. Cloud hyperscalers Microsoft and Amazon pursue platform economics; their bundled services expand total contract value while reducing per-unit compute costs, eroding standalone providers’ price advantages. Specialist firms such as PTC, Ansys and Materialise defend vertical niches through proprietary algorithms and regulatory track records.

Strategic convergence is visible: GE’s purchase of Bentley Systems’ infrastructure-twin assets merges operational data with civil-engineering models, while Microsoft’s USD 3.2 billion Azure Digital Twins expansion embeds generative AI that auto-creates models from minimal data inputs. NVIDIA’s Omniverse Cloud democratizes GPU-powered simulation, unlocking high-fidelity twins for small manufacturers without local high-performance computing clusters. Remaining white-space includes simplified offerings for mid-sized enterprises and packaged integrations for brownfield plants, both of which vendors increasingly address through low-code interfaces and pre-validated hardware kits.

Moderate fragmentation persists, yet platform stickiness is rising. Once a twin anchors critical decision workflows, production planning, energy balancing or surgical scheduling, organizations hesitate to migrate, cementing incumbents’ footholds. The need for cybersecurity certifications and government-vendor qualifications further narrows the viable supplier pool for federally funded projects, gradually lifting entry barriers within the US digital twin market.

United States Digital Twin Industry Leaders

General Electric Company

Siemens AG

Microsoft Corporation

IBM Corporation

Dassault Systèmes SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft committed USD 3.2 billion to extend Azure Digital Twins with generative-AI model automation and sector templates.

- December 2024: General Electric acquired Bentley Systems’ infrastructure-twin portfolio for USD 1.8 billion, integrating civil-works capabilities.

- November 2024: Amazon Web Services released IoT TwinMaker Edge for sub-10 millisecond industrial-control loops.

- October 2024: Siemens invested USD 2.1 billion in new US twin R&D centers focused on automotive and aerospace.

United States Digital Twin Market Report Scope

| Product Twin |

| Process Twin |

| System Twin |

| Asset/Component Twin |

| Predictive Maintenance |

| Performance Monitoring |

| Product Design and Development |

| Business / Workflow Optimization |

| Manufacturing |

| Aerospace and Defense |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Other End-user Industries |

| Cloud |

| On-premise |

| Hybrid / Edge-Cloud |

| By Twin-Type | Product Twin |

| Process Twin | |

| System Twin | |

| Asset/Component Twin | |

| By Application | Predictive Maintenance |

| Performance Monitoring | |

| Product Design and Development | |

| Business / Workflow Optimization | |

| By End-user Industry | Manufacturing |

| Aerospace and Defense | |

| Healthcare and Life Sciences | |

| Energy and Utilities | |

| Other End-user Industries | |

| By Deployment Model | Cloud |

| On-premise | |

| Hybrid / Edge-Cloud |

Key Questions Answered in the Report

What is the current size of the U.S. digital twin market?

The US digital twin market size stands at USD 10.07 billion in 2025 and is forecast to reach USD 50.13 billion by 2030.

Which segment holds the largest share among twin types?

Product twins lead with 41.73% share in 2024, reflecting their dominance in high-precision aerospace and automotive applications.

Why are hybrid deployments growing so quickly?

Hybrid architectures combine on-site latency control with cloud-based analytics, driving a 39.11% CAGR as firms balance performance and data-sovereignty needs.

How are federal mandates influencing adoption?

Infrastructure and CHIPS Act requirements make digital twins mandatory for large smart-city projects and subsidized semiconductor fabs, strongly accelerating adoption.

What are the main barriers to implementation?

Cyber-security risk and the complexity of integrating brownfield legacy systems remain the two primary constraints on near-term deployment velocity.

Page last updated on: