Digital Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

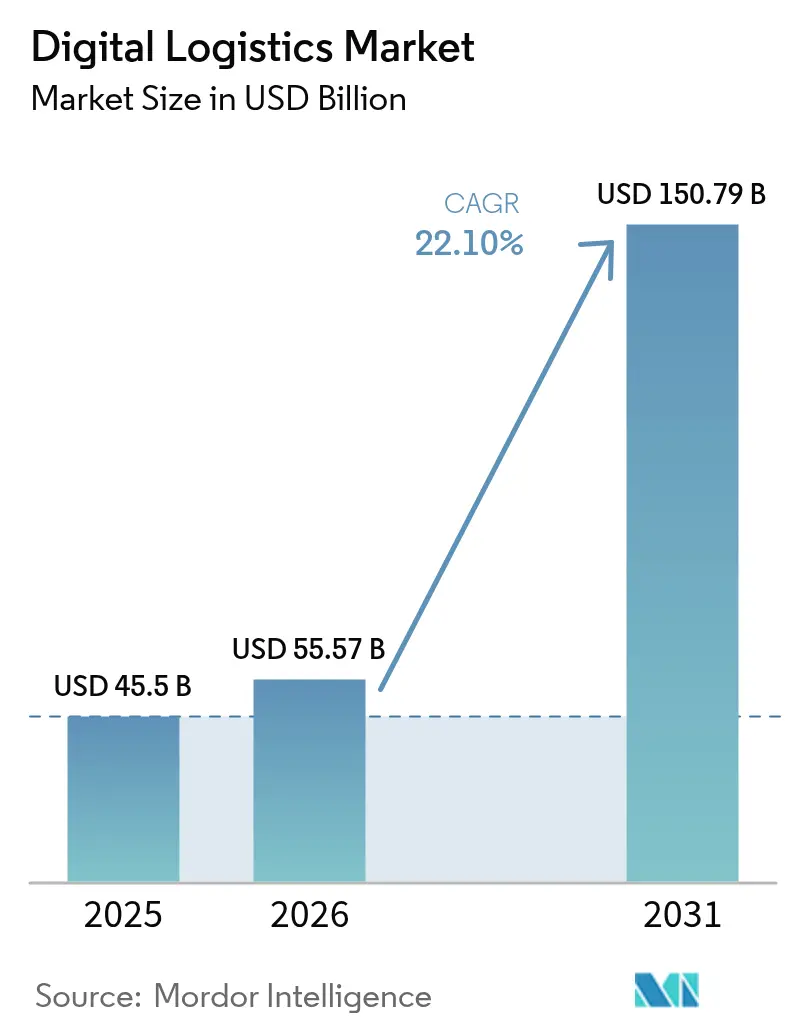

| Market Size (2026) | USD 55.57 Billion |

| Market Size (2031) | USD 150.79 Billion |

| Growth Rate (2026 - 2031) | 22.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Logistics Market Analysis by Mordor Intelligence

Digital Logistics Market size in 2026 is estimated at USD 55.57 billion, growing from 2025 value of USD 45.5 billion with 2031 projections showing USD 150.79 billion, growing at 22.1% CAGR over 2026-2031. Rapid e-commerce expansion, the convergence of AI, IoT, and blockchain, and the pivot toward cloud-native architectures are accelerating enterprise adoption. Predictive analytics is enhancing inventory accuracy and reducing waste, while real-time IoT telematics is lowering fleet fuel consumption and supporting sustainability targets. Enterprises increasingly treat digital logistics as a source of competitive advantage; 71% of automotive OEMs now favor direct-to-consumer distribution, forcing logistics providers to rethink last-mile models. Heightened cyber-threat levels and regional infrastructure gaps temper the pace of transformation; yet, sustained investment by retailers, pharmaceutical firms, and governments underscores the market’s long-term momentum.

Key Report Takeaways

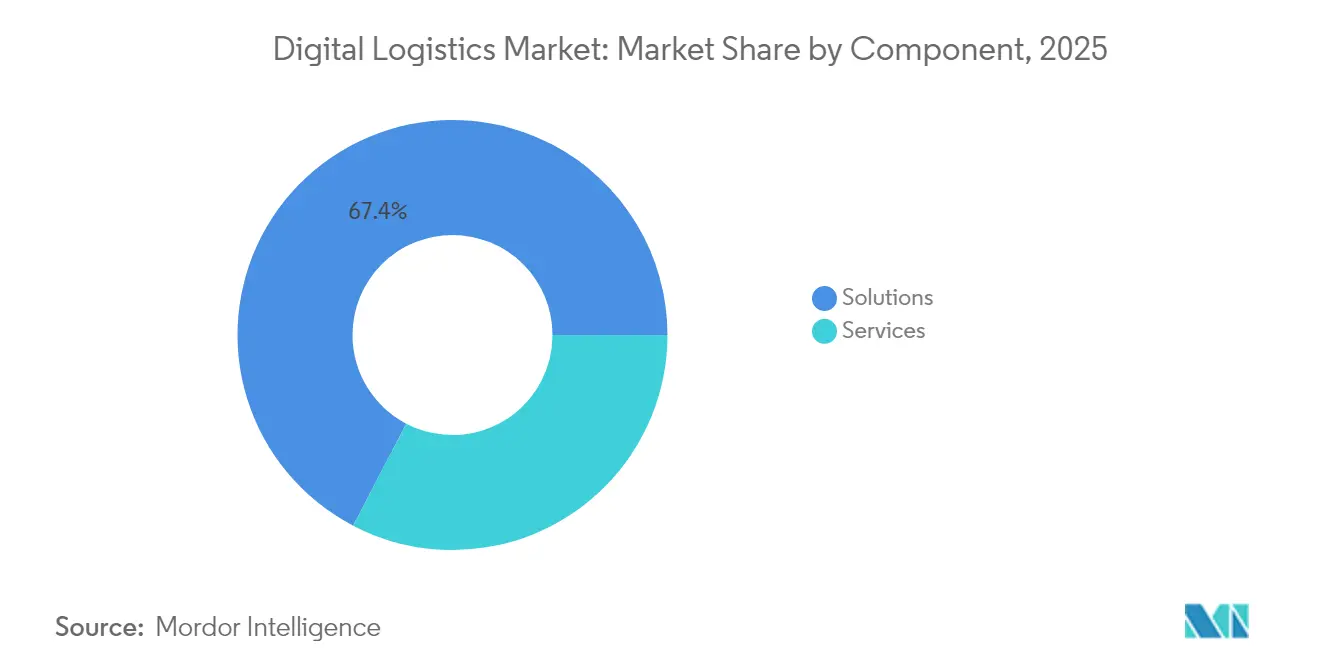

- By component, solutions led with 67.35% of the digital logistics market share in 2025, while Services are projected to expand at a 23.55% CAGR through 2031.

- By deployment mode, cloud platforms commanded a 57.60% share of the digital logistics market size in 2025; cloud-led spending is forecast to rise at a 22.93% CAGR between 2026-2031.

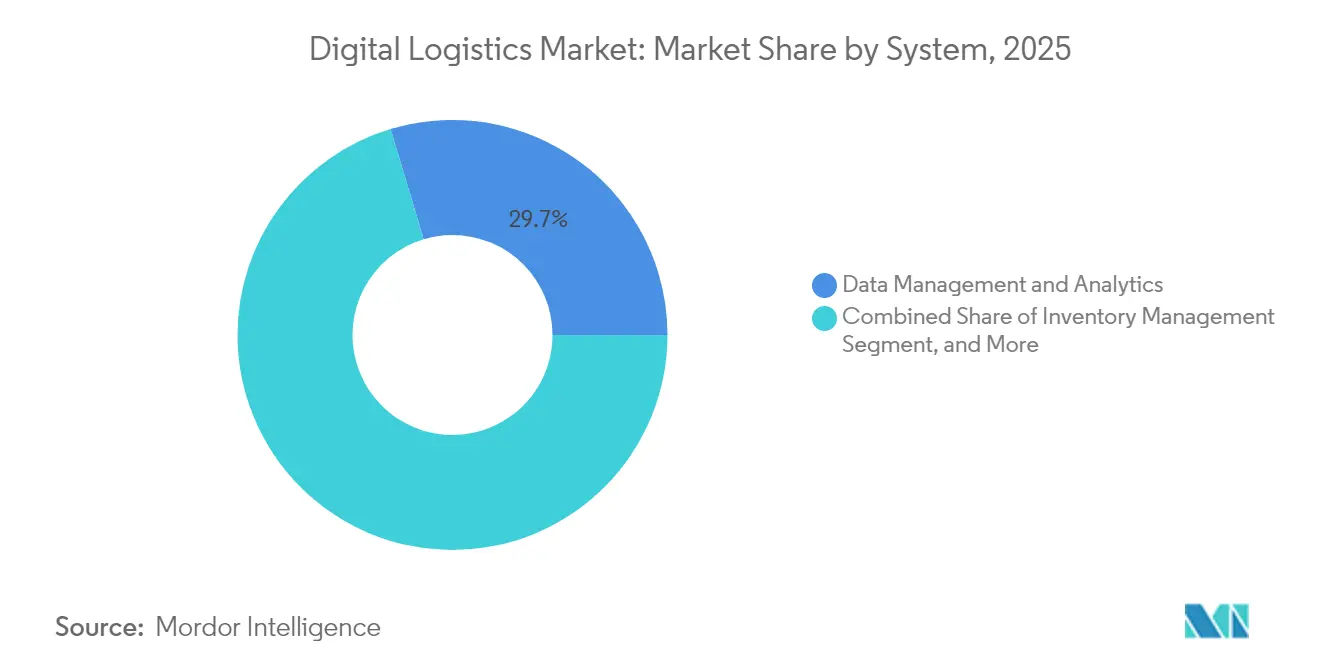

- By system type, data management and analytics captured a 29.65% revenue share in 2025, whereas fleet management is projected to advance at a 22.65% CAGR through 2031.

- By end-user vertical, retail and e-commerce held 24.60% of the digital logistics market in 2025; pharmaceuticals and life Sciences is the fastest-growing vertical, with a 23.64% CAGR from 2025 to 2031.

- By geography, North America dominated with a 37.55% share in 2025, while the Asia Pacific is expected to expand at a 23.58% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Real-time IoT Fleet Telematics in North America | +4.20% | North America, spillover to Europe | Medium term (2–4 years) |

| AI-powered Predictive Warehouse Analytics Adoption by European 3PLs | +5.80% | Europe, North America | Medium term (2–4 years) |

| Surge in Same-day E-commerce Fulfilment Across Asia | +6.10% | Asia-Pacific, spillover to North America | Short term (≤ 2 years) |

| National Green-Freight Digitalization Incentives (Middle East) | +3.50% | Middle East, spillover to Europe | Long term (≥ 4 years) |

| Automotive-OEM Direct-to-Consumer Digital Logistics Programs | +4.60% | North America, Europe, Asia | Medium term (2–4 years) |

| Post-COVID Pharma Cold-Chain Digitization Mandates in Europe | +3.90% | Europe, spillover to North America and APAC pharma hubs | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Expansion of real-time IoT fleet telematics in North America

Connected telematics devices now stream engine health, driver behavior, and cargo data in real-time, enabling predictive maintenance that cuts downtime by 30% and fuel consumption by 15-20%. Logistics providers translate these gains into premium, guaranteed delivery windows that raise service levels while shrinking emissions. With IoT logistics spending expected to top USD 114.7 billion by 2032, fleet telematics has become a boardroom priority, particularly for carriers seeking to differentiate on sustainability.[1]Cisco Systems, “Cisco IoT in Logistics,” cisco.com

AI-powered predictive warehouse analytics adoption by European 3PLs

European 3PLs combine machine-learning algorithms and computer vision to create digital twins of warehouses, unlocking inventory reductions of 20-30% without compromising fill rates. Scenario modelling helps operators pre-empt labor bottlenecks and reroute pick paths in minutes rather than hours. These capabilities underpin new value-added contracts that bundle demand forecasting with fulfillment, helping 3PLs move up the margin curve.

Surge in same-day e-commerce fulfillment across Asia

Same-day delivery spending is on track to quadruple between 2024 and 2031, spurring micro-fulfillment buildouts in dense cities such as Shanghai and Jakarta. Retailers deploy AI route-optimization to navigate complex traffic patterns and autonomous sorting lines to manage SKU proliferation. Hybrid hub-and-spoke networks strike a balance between cost and speed, positioning the Asia-Pacific region to capture 57% of global e-commerce logistics growth by 2025.

National green-freight digitalization incentives (Middle East)

Saudi Arabia’s Vision 2030 allocates USD 2.7 billion in grants and tax credits to logistics projects that prove measurable carbon reductions. Providers deploy IoT sensors linked to blockchain ledgers for tamper-proof carbon accounting, cutting empty miles up to 40% through real-time load matching. Early movers secure lower financing costs and priority access to government contracts, accelerating regional adoption of low-emission fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Under-investment in 5G Corridors across Africa | −2.8% | Africa, spillover to Middle East | Long term (≥ 4 years) |

| Fragmented Data-standards Blocking Cross-Border APAC Trade | −2.3% | Asia-Pacific | Medium term (2–4 years) |

| Cyber-insurance Premium Spikes for Cloud-Logistics Platforms | −2.1% | Global – strongest in North America and Europe | Short to medium term (1–3 years) |

| Skilled WMS (Warehouse Management System) Talent Shortage in Latin America | −1.9% | Latin America, emerging logistics hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Under-investment in 5G corridors across Africa

Only 7% of key transport corridors have 5G coverage, limiting real-time visibility for cross-border hauls. Customs clearance averages 48-72 hours, compared to 4-6 hours in well-connected regions, which prolongs dwell times and increases inventory carry costs. Closing the gap requires an estimated USD 4.7 billion, a figure that exceeds current public-private commitments, though pilot corridors are starting to demonstrate productivity uplifts.[2] Development Bank of Southern Africa, “Transport Infrastructure Investment Needs,” dbsa.org

Fragmented data standards blocking cross-border APAC trade

Multiple, country-specific data formats compel carriers to maintain redundant systems, inflating compliance costs by 15-20%. Initiatives such as the ASEAN Single Window have streamlined customs data, yet shipment tracking, safety stock, and product classification standards remain inconsistent. The lack of harmonization deprives regional shippers of end-to-end visibility and hinders the rollout of digital logistics, particularly for small exporters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services capture growth momentum

Digital logistics services contributed 32.65% to 2025 revenue, but their stronger 23.55% CAGR points to a growing preference for outsourced expertise. Companies short on in-house talent increasingly contract managed services to orchestrate system integration, data cleansing, and continuous optimization. Solutions still generate the remaining 67.35% of 2025 revenue and anchor many transformation roadmaps, yet buyers now expect modularity and open APIs rather than monolithic suites. Vendor success hinges on coupling a robust core platform with curated partner ecosystems that address specialized functions such as cold-chain validation or customs brokerage. Mid-market adopters illustrate the shift; 72% now favor service contracts over direct software ownership to avoid capex and accelerate ROI. Providers such as Tech Mahindra bundle low-code accelerators and AI toolkits, allowing clients to reconfigure workflows in days rather than quarters. This flexibility is crucial as regulations, demand patterns, and sustainability targets evolve. Solution vendors respond by unbundling modules and offering pay-as-you-scale commercial models, ensuring the digital logistics market continues to diversify.

By Deployment Mode: Cloud maintains decisive lead

Cloud platforms accounted for a 57.60% share of the digital logistics market in 2025 and are expected to grow at a 22.93% CAGR through 2031. Scalability, rapid deployment, and global accessibility make cloud architectures the default choice for omnichannel logistics networks. Companies report deployment cycles 35% faster and total cost of ownership 42% lower than on-premise alternatives, underscoring the economic rationale for migration. Security once hindered adoption, but enterprise-grade encryption, zero-trust frameworks, and sovereign cloud options have alleviated most concerns. Hybrid models persist in highly regulated verticals where data-residency rules apply, yet edge-to-cloud architectures now satisfy real-time processing demands without relinquishing governance. North America leads with 67% cloud adoption, closely followed by Europe at 63%. Emerging markets are catching up as bandwidth improves and hyperscalers launch new regional zones. On-premise deployments will continue to serve niche use cases involving ultra-low-latency robotics or proprietary legacy hardware, but their share of the digital logistics market size is projected to contract steadily.

By System/Type: Analytics anchors decision intelligence

Data Management and Analytics held a 29.65% share of the digital logistics market size in 2025, thanks to its role in converting raw data into tactical and strategic insights. Users report 18-25% logistics cost reductions after embedding predictive models that fine-tune replenishment, carrier selection, and dock scheduling. Cloud-based data fabrics ingest IoT, ERP, and telematics feeds, enabling AI engines to surface anomalies in near real time. Fleet Management is the fastest-growing system, with a 22.65% CAGR from 2026 to 2031. The proliferation of on-vehicle sensors, driver-assistance tech, and emissions regulations forces carriers to digitize fleet operations. Warehouse Management Systems retain a 22% share and benefit from robotics integration that reduces travel time and boosts pick accuracy. Tracking and Monitoring platforms experience adoption spikes in the pharmaceutical and food industries, where regulators demand end-to-end visibility of conditions. Meanwhile, niche modules for customs, return,s and reverse logistics gain traction as cross-border e-commerce scales.

By End-user Vertical: Pharma accelerates digital adoption

Retail and E-commerce led 2025 revenue, accounting for a 24.60% share of the digital logistics market. The sector’s customer-promise focus turns delivery performance into a direct sales lever, which in turn fuels investments in last-mile route optimization and micro-fulfillment automation. Same-day and instant delivery propositions now extend to tier-2 urban areas, raising the digital baseline across the retail landscape. Pharmaceuticals and Life Sciences is the standout growth sector, tracking a 23.64% CAGR through 2031, as biologics and cell- and gene-therapies impose strict cold-chain mandates. IoT loggers with blockchain validation create immutable audit trails, satisfying the needs of post-pandemic regulators and insurers. The automotive sector, driven by the direct sales of electric vehicles, demands white-glove handover and battery condition assurance, while the Food and Beverage sector taps blockchain traceability to validate provenance. Manufacturing and Oil and Gas explore digital twins and condition monitoring to minimize downtime, ensuring the digital logistics industry addresses a broadening array of vertical pain points.

Geography Analysis

North America commanded 37.55% of the digital logistics market revenue in 2025. Deep e-commerce penetration, widespread 5G rollouts and abundant venture funding nurture a vibrant ecosystem of SaaS providers, robotics firms and freight-tech start-ups. Eight in ten logistics operators plan to embed AI in at least one workflow by 2025, while regulators steadily open corridors for autonomous trucking trials.

Asia-Pacific is the growth engine, expanding at a 23.58% CAGR through 2031. China, India, and Southeast Asia underpin this trajectory with surging online consumption and ambitious national logistics corridors. Cross-border sellers benefit from duty-paid models and smart lockers, yet fragmented data standards inflate costs and curb small-business participation. Urban congestion prompts micro-fulfillment build-outs and two-wheel deliveries, whereas remote islands adopt drones to bridge infrastructure gaps. Europe blends advanced infrastructure with policy-driven sustainability. Carbon-linked road tolls and low-emission zones amplify demand for routing software and electric last-mile fleets. The region’s 3PLs pioneer predictive warehouse analytics to counter labor shortages and rising wage bills. The Middle East channels sovereign funds into smart ports and rail links to diversify beyond oil. Africa’s potential remains tied to 5G and customs modernization, while South America contends with talent deficits that inflate WMS implementation costs by 40%.

Regulatory Landscape

Digital logistics regulations are shifting from enabling guidance to compliance-led digitization of freight information and transport documentation. In the European Union, the eFTI framework advanced through Implementing Regulation (EU) 2024/1942 (common procedures for competent-authority access to electronic freight transport information) and Implementing Regulation (EU) 2025/2243 (functional requirements for eFTI platforms), which increases expectations for interoperability, authentication, and auditability across cross-border freight flows.

In 2026, several large markets introduced national-level programs that affect platform architecture, data governance, and document workflows. Japan approved the Comprehensive Physical Distribution Policy Outline (FY2026-FY2030) with an explicit focus on logistics DX and supply-chain strengthening. Russia issued Government Decree No. 139 establishing the National Digital Transport and Logistics Platform "GosLog" effective March 1, 2026, and China finalized multi-ministry rules to promote and standardize electronic documents in trade and transport, effective September 1, 2026. In the United States, the Department of Transportation initiated a 2026 Request for Information to define a National Strategy for Transportation Digital Infrastructure, reflecting continued federal emphasis on freight data and digital infrastructure alignment.

Value Chain Analysis

The digital logistics value chain spans data capture and connectivity (IoT devices, telematics, mobile scanning, edge gateways), cloud and platform infrastructure, and application layers such as WMS, TMS, fleet management, analytics, and tracking/monitoring, delivered via solutions and managed services. Integrators, consulting and IT services firms, and logistics operators (carriers, 3PLs, forwarders, and terminal operators) translate these capabilities into implementation, workflow redesign, cybersecurity, and ongoing optimization, while shippers in retail and e-commerce, manufacturing, automotive, and pharmaceuticals drive requirements for real-time visibility, compliance, and exception handling.

Recent ecosystem moves show ports and trade networks taking on a larger role as high-value nodes in the chain. Partnerships such as Kale Logistics with Tech Mahindra (ports and airports digitalization), Altana with Maersk (digital trade network connecting importers and customs authorities), and APSEZ with Kaleris (AI-augmented terminal operating systems across 15 container terminals) indicate that value is increasingly created through shared data layers and interoperable platforms, rather than isolated point systems. Bottlenecks remain concentrated in data fragmentation across stakeholders, integration limits of legacy ERP landscapes, and security and governance requirements as electronic documentation and traceability become operational necessities.

Competitive Landscape

The digital logistics market is moderately fragmented, with ERP majors, freight-tech specialists, and incumbent forwarders vying for wallet share. Cloud migration and API-first strategies lower entry barriers, enabling niche providers to attack specific pain points such as container visibility or cold-chain compliance. Incumbents counter by acquiring specialists or launching venture studios; DHL’s purchase of IDS Fulfillment exemplifies the push to strengthen e-commerce depth.

Platform playbooks dominate recent strategy. Vendors court third-party developers with open SDKs, aiming to create network effects that lock in customers. White spaces still exist in high-value verticals, such as pharma, EV delivery, and sustainable urban freight, where domain expertise trumps generic functionality. Funding flows confirm the trend, with 61.2% of recent logistics-tech capital targeting AI-centric propositions that deliver hard ROI.

Despite prolific innovation, the usage of capabilities lags behind their potential. A Here Technologies survey shows half of logistics professionals rely solely on descriptive analytics, while only one-quarter employ AI for decisions. This gap underscores the importance of change management and upskilling, domains where consulting-led service models find receptive audiences.

Digital Logistics Industry Leaders

IBM Corporation

Advantech Corporation

Oracle Corporation

Cisco Systems Inc.

FedEx Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ports, terminals, and trade corridors are becoming a key adoption surface for digital logistics platforms because they concentrate multimodal data, regulatory documentation, and operational control. In Europe, COM(2026) 112 positions CEF Digital as a support instrument for 5G in ports within the 2028-2034 budget framework, linking connectivity upgrades with digital freight workflows. This creates more defined whitespace for vendors that combine edge-to-cloud visibility with the governance, identity, and interoperable data exchange capabilities needed for cross-border movements.

Operational digitization is also being funded through large, named projects that embed AI, terminal operating systems, and digital twin capabilities into new capacity and expansion programs. Examples include APSEZ announcing a USD 100 million investment phase with Kaleris to deploy AI-augmented terminal operating systems across 15 container terminals, TTI Algeciras signing with CyberLogitec to implement OPUS Terminal and digital twin solutions for the B1 terminal expansion, and RSGT Bangladesh commencing full operations at the Patenga Container Terminal after a USD 170 million investment that included digital automation. India’s Logistics Port Performance Index for FY2024-25 and its additional maritime digital initiatives further support demand for platforms that can standardize performance monitoring, incident and grievance handling, and ship and cargo data flows across stakeholders.

Recent Industry Developments

- June 2026: Oracle announced four new Fusion Agentic Applications in Oracle Fusion Cloud Supply Chain and Manufacturing to improve inventory visibility and manufacturing efficiency. The additions extend agentic AI into day-to-day execution workflows, shifting digital logistics toward proactive exception handling and decision automation within enterprise suites.

- May 2026: FedEx expanded its strategic collaboration with ServiceNow, embedding FedEx Dataworks logistics intelligence into ServiceNow Source-to-Pay and Supply Chain Management workflows. The integration aims to streamline procurement-to-logistics coordination by reducing context switching and bringing carrier and network insights closer to enterprise process owners.

- April 2026: FedEx announced a strategic collaboration with Viettel Post Joint Stock Corporation to strengthen end-to-end logistics connectivity in Vietnam, effective April 26, 2026. The partnership supports more integrated cross-border and domestic shipping workflows, reinforcing Asia-Pacific as a key arena for visibility and platform-led service differentiation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services used to plan, execute, and monitor logistics flows digitally, such as transportation, warehousing, inventory, and fleet activities, where value is captured as spending on these digital logistics capabilities.

Scope exclusions: We exclude manual-only logistics operations and general IT hardware spending that is not purchased as part of a digital logistics solution.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud-based

- On-premise

- By System / Type

- Inventory Management

- Warehouse Management System (WMS)

- Fleet Management

- Data Management and Analytics

- Tracking and Monitoring

- Other Types

- By End-user Vertical

- Retail and E-commerce

- Manufacturing

- Automotive

- Pharmaceuticals and Life Sciences

- Food and Beverage

- Oil and Gas and Energy

- Consumer Packaged Goods

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a demand map for digital logistics, then connecting that to public signals on freight activity and supply chain investment. We referenced non-paywalled sources such as the World Bank logistics indicators, UN trade and freight statistics, OECD transport data, and US Census Bureau measures tied to inventory and e-commerce activity. For technology adoption cues, we also used sources such as peer-reviewed logistics and supply chain journals and patent databases, which help indicate where innovation and deployment are rising.

To make the model practical, we also reviewed company annual reports, investor presentations, earnings call transcripts, and credible press coverage to understand solution mix, pricing direction, and buyer priorities. In a few cases, paid subscriptions that compile company financials and news were used to fill gaps around revenue splits and recent product launches, and shipment-level trade databases were used as a cross-check for macro volume movements. The desk sources listed here are illustrative, and many other public materials were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with shippers, logistics service providers, and digital solution teams who work around transportation, warehousing, and inventory operations. Since this is a global market, feedback was intentionally balanced across APAC, EMEA, and the Americas to confirm adoption pace, typical buying bundles, and the share of spending that is truly tied to digital logistics outcomes. Where desk sources were unclear, we used re-contacts to lock assumptions on pricing ranges, deployment shifts, and the portion of services attached to solutions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 19% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 21% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where the top-down view reconstructs the spend pool using logistics activity signals and IT-to-operations digitization intensity by region. We then corroborated totals with selective bottom-up checks, such as rolling up sampled revenues from solution and service providers, and validating implied spend using ASP ranges multiplied by installed and incremental deployments for core systems.

Key inputs that shaped the model included global freight and trade momentum, warehouse automation and WMS adoption trends, cloud versus on-premise deployment mix, average contract lengths and renewal patterns, and the attach rate of services (implementation, integration, and managed services) to solution deals. For areas where supplier disclosures were limited, gaps were handled using peer-group ratios and channel feedback, followed by conservative adjustments when assumptions did not match what users reported. Forecasts were developed using scenario analysis supported by short-cycle indicators like e-commerce volumes, inventory turns, and transportation capacity tightness, and then stress-tested with what interviewees expect for pricing progression and rollout timing.

Data Validation & Update Cycle

Before sign-off, outputs are triangulated against independent indicators like logistics activity, cloud spend direction in operations, and the implied penetration of digital systems in warehouses and fleets. Variance checks are run at the region and solution level, and any outliers trigger a deeper review of unit assumptions, currency timing, or double counting between solutions and services. When conflicts show up, follow-up calls are done so the final view reflects how the market is actually purchased and delivered.

Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, sharp freight cycle shifts, or step changes in enterprise spending. Right before delivery, a fresh analyst pass is completed to ensure the latest public data and market signals are reflected in the final numbers.

Mordor Intelligence's Digital Logistics Market Size Measured Against Other Published Estimates

It is normal to see different published market sizes for digital logistics because firms do not always count the same revenue streams and they also use different base-year assumptions. Differences can come from what gets included as digital logistics, how services are treated, and whether the estimate follows current deployment realities or a more aggressive adoption curve.

In our checks, the biggest gap driver is scope, especially whether adjacent areas like broad supply chain software suites or non-logistics enterprise IT are bundled into the total. Another driver is pricing logic, where some estimates apply straight-line ASP increases without testing them against contract terms and the fast shift toward cloud subscriptions. The table reflects these issues, since the figure that counts only solutions and explicitly linked services, with cloud versus on-premise split validated in interviews, lands higher than one estimate and below another, which is a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 45.50 B (2025) | |

| Industry Publisher A | USD 37.64 B (2025) | This estimate appears to apply a narrower inclusion set, which can undercount service revenue attached to deployments and omit some enterprise-grade logistics systems beyond transportation-only use cases. |

| Industry Publisher B | USD 48.20 B (2025) | This estimate seems to use a broader scope that can pull in adjacent supply chain software functions, and it may assume a faster near-term ramp in adoption that increases the base-year spend. |

Across the three figures, the spread mainly comes from what is counted as digital logistics spend, plus how services and subscription pricing are treated in the base year. By keeping the scope tied to logistics execution systems and their directly linked services, and then cross-checking with adoption and contract signals, the final number stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the digital logistics market?

The digital logistics market stands at USD 55.57 billion in 2026 and is projected to reach USD 150.79 billion by 2031.

Which region leads the digital logistics market?

North America leads with 37.55% revenue share in 2025, benefiting from advanced infrastructure and high cloud adoption.

Which deployment model is growing fastest in digital logistics?

Cloud-based platforms grow at a 22.93% CAGR, delivering lower ownership cost and quicker deployments than on-premise systems.

Which region has the biggest share in Digital Logistics Market?

In 2025, the North America accounts for the largest market share in Digital Logistics Market.

What technological driver has the highest impact on market CAGR?

Same-day e-commerce fulfillment across Asia carries a +6.1% impact, pushing investments in micro-fulfillment and route optimization.

How fragmented is the competitive landscape?

The market is moderately fragmented: the top 10 firms capture under 40% revenue, and new entrants continually emerge in niche segments.

Page last updated on: