United States and Canada Skin Cancer Dermatology Tests Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

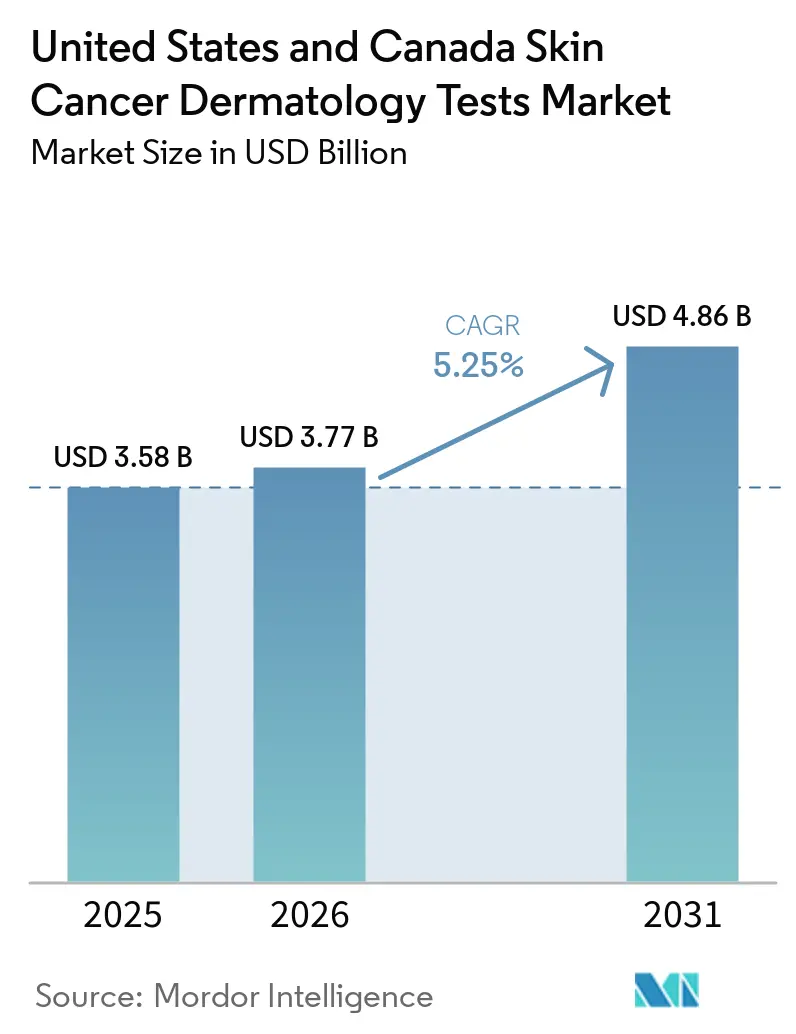

| Base Year Market Size (2025) | USD 3.58 Billion |

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 4.86 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

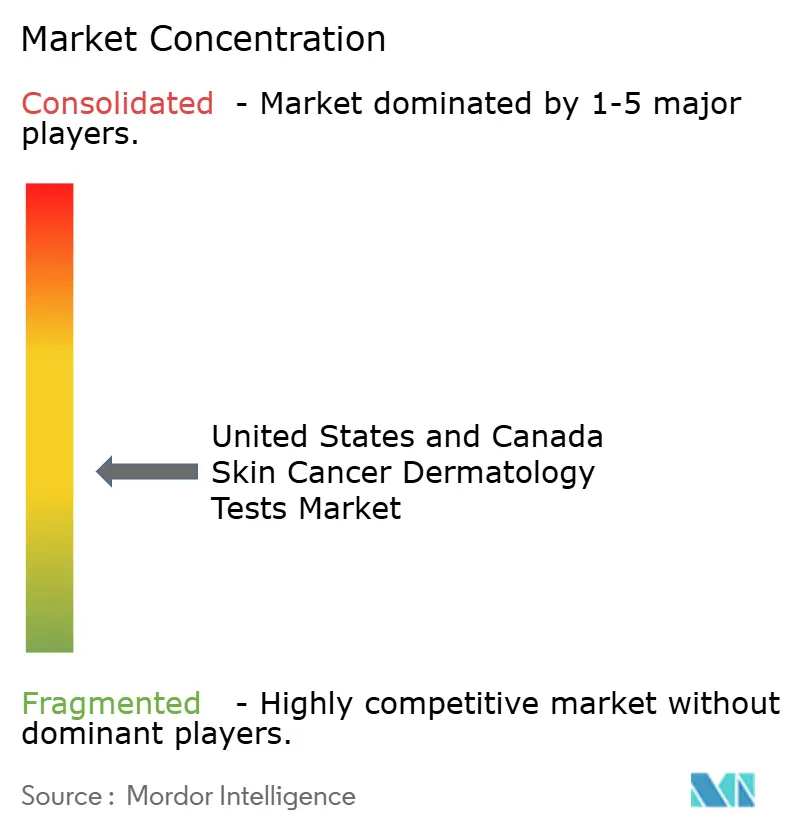

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States and Canada Skin Cancer Dermatology Tests Market Analysis by Mordor Intelligence

The United States And Canada Skin Cancer Dermatology Tests Market size was valued at USD 3.58 billion in 2025 and is estimated to grow from USD 3.77 billion in 2026 to reach USD 4.86 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

The growth base for the skin cancer dermatology tests market remains firm because the United States is expected to record 112,000 new invasive melanoma cases in 2026, while skin cancer treatment spending in the country had already reached USD 8.9 billion, including USD 4.8 billion tied to non-melanoma disease, which keeps diagnostic activity concentrated in high-volume outpatient settings. The United States and Canada skin cancer dermatology tests market is also widening beyond conventional biopsy because genomic assays, AI-assisted dermoscopy, and spectroscopy tools are being used earlier in the diagnostic pathway as pre-biopsy decision aids. A major competitive shift is now underway after the FDA moved optical melanoma diagnostic devices and electrical impedance spectrometers from Class III to Class II, which lowers entry barriers for device developers and should expand the field of AI-adjunctive platforms in the skin cancer dermatology tests market. At the same time, CMS continues to actively maintain reimbursement rules for melanoma molecular testing, which supports commercialization for covered assays but keeps payer engagement central to growth for newer test formats. This combination of strong disease burden, device liberalization, and selective molecular reimbursement keeps the skin cancer dermatology tests market on a steady growth path while creating clear openings for companies that can combine clinical evidence, workflow fit, and reimbursement execution.

Key Report Takeaways

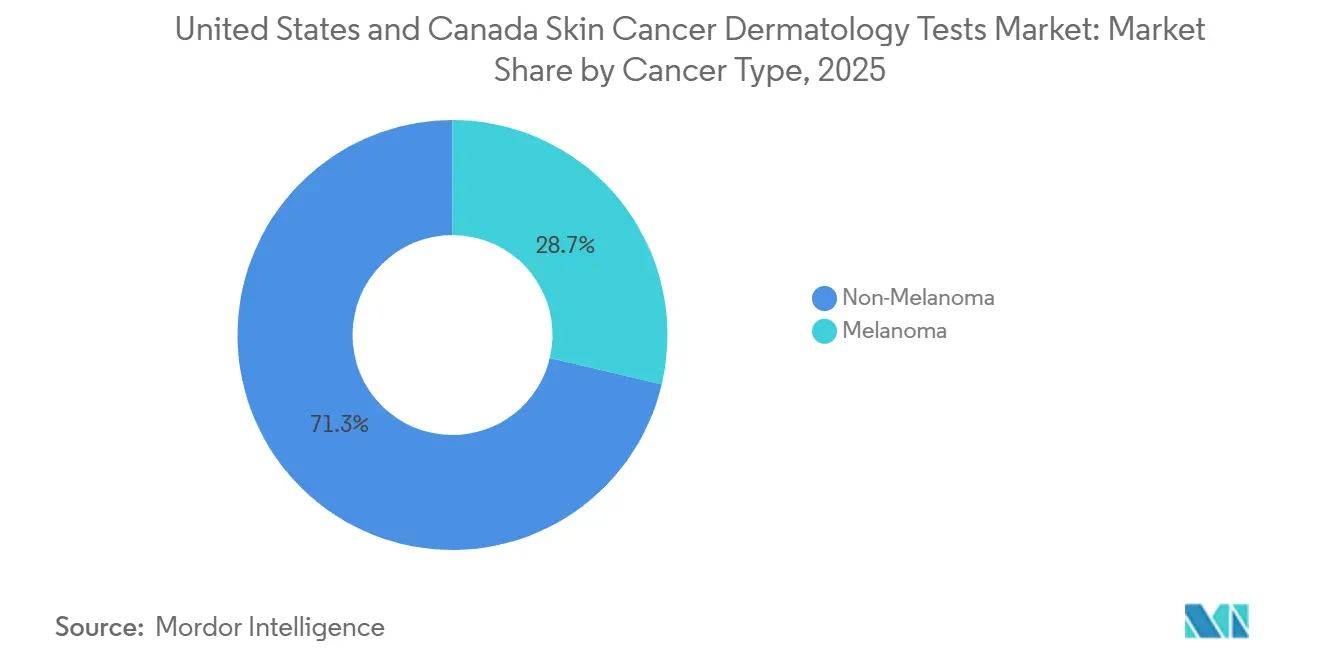

- By cancer type, non-melanoma skin cancer held 71.31% revenue share in 2025, while melanoma is projected to expand at a 6.38% CAGR through 2031.

- By test type, skin biopsy accounted for 32.24% of revenue in 2025, while imaging tests are forecast to grow at a 7.52% CAGR through 2031.

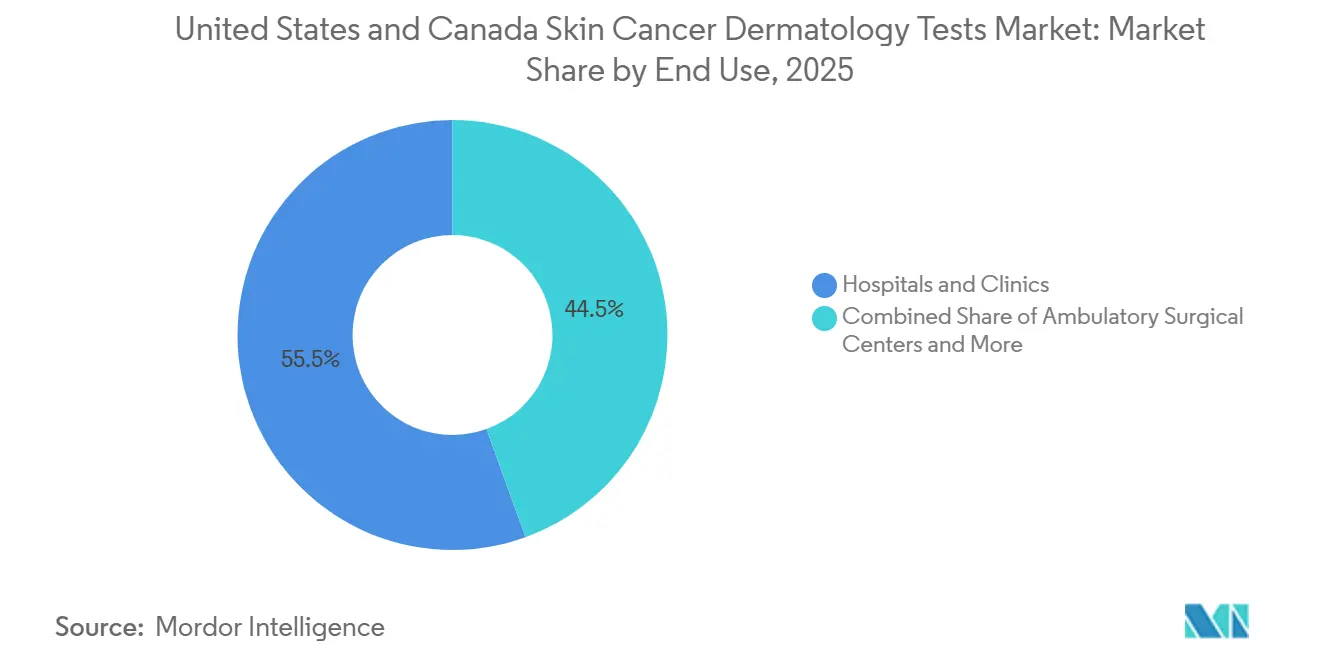

- By end use, hospitals and clinics captured 55.52% of revenue in 2025, while ambulatory surgical centers are projected to record the highest CAGR at 7.25% through 2031.

- By country, the United States represented 85.54% of combined revenue in 2025, while Canada is projected to advance at a 6.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States and Canada Skin Cancer Dermatology Tests Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Melanoma Screening Intensity In High-Risk Populations | +1.2% | United States primary, Canada secondary with spill-over to Atlantic provinces | Medium term (2-4 years) |

| Faster Adoption Of AI-Assisted Dermoscopy And Spectroscopy | +1.0% | National across the United States and Canada, with early concentration in academic and metropolitan centers | Short term (≤ 2 years) |

| Expansion Of Teledermatology Triage Into Diagnostic Pathways | +0.8% | Rural United States and underserved Canadian provinces including Alberta, Saskatchewan, and the Maritime provinces | Medium term (2-4 years) |

| Reimbursement Support For Medically Necessary Diagnostic Workups | +0.7% | United States Medicare and commercial payers nationally, Canadian provincial formularies | Medium term (2-4 years) |

| Increased Use Of Non-Invasive Pre-Biopsy Assessment Tools | +0.5% | National across the United States and Canada, with highest penetration in high-volume dermatology practices | Short term (≤ 2 years) |

| Employer And Payer Focus On Earlier Stage Detection Economics | +0.4% | United States employer-sponsored plans, concentrated in large metropolitan self-insured employers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Melanoma Screening Intensity in High-Risk Populations

Melanoma incidence in the United States has been rising at an average of 1.1% per year over 2014-2023, with age-adjusted new case rates near 22.3 per 100,000 and 112,000 new invasive cases projected in 2026, which keeps referral volumes elevated across the United States and Canada skin cancer dermatology tests market. This sustained rise is translating into stronger demand for risk stratification, lesion assessment, and confirmatory testing among people aged 50 and older, outdoor workers, and other groups with high cumulative UV exposure. Another layer of demand is coming from melanoma-in-situ, which reached an estimated 107,240 cases in 2025 and requires differentiation from benign lesions even when it does not follow the same downstream procedural path as invasive disease[1]American Cancer Society, “Cancer Facts & Figures 2025,” American Cancer Society, cancer.org. In Canada, melanoma accounts for 1 in 24 new cancer diagnoses, and Nova Scotia and Prince Edward Island report incidence levels above the national average, which points to localized areas where screening expansion can lift testing demand faster than the national averageG. The result is a structural increase in specialist referrals that supports multi-year growth in the United States and Canada skin cancer dermatology tests market even before any single platform change is considered.

Faster Adoption of AI-Assisted Dermoscopy and Spectroscopy

The January 2024 FDA clearance of DermaSensor expanded the diagnostic setting for the United States and Canada skin cancer dermatology tests market because the device was cleared for use by primary care physicians to help detect melanoma, basal cell carcinoma, and squamous cell carcinoma. The company’s pivotal study later published in 2025 reported 95.5% sensitivity across skin cancer types and showed that physician cancer prediction accuracy improved by 12.5%, which strengthens the clinical case for front-end triage use. In practice, AI spectroscopy does not remove downstream testing from the skin cancer dermatology tests market because lesions flagged as suspicious still move into biopsy or specialist review, which means the tool can add an upstream triage layer without replacing confirmatory testing[2]DermaSensor, “Published FDA Pivotal Studies Find DermaSensor Has 96% Sensitivity and Cuts Physician’s Missed Skin Cancers by Half,” DermaSensor, dermasensor.com. The FDA’s March 2026 reclassification of OYD and ONV device classes from Class III to Class II further changes the economics by replacing the premarket approval route with a 510(k) pathway for eligible products. That policy reset should accelerate launches, widen competition, and reinforce the strong outlook for imaging within the United States and Canada skin cancer dermatology tests market.

Expansion of Teledermatology Triage Into Diagnostic Pathways

Teledermatology is becoming a permanent triage layer in the United States and Canada skin cancer dermatology tests market because it is moving suspicious lesions into specialist review faster than traditional referral pathways. A 2025 review reported that photo-triage reduced median time to first specialist clinic from 24 days to 14 days, which shortens lead time in melanoma workups and moves more lesions through structured diagnostic review. In rural U.S. settings and underserved Canadian provinces, store-and-forward teledermoscopy is also helping primary care physicians route only higher-risk lesions to biopsy or in-person specialist care. This selective routing can lower biopsy use in clearly benign cases while improving biopsy yield and preserving lab capacity for lesions with stronger malignant potential. A separate meta-analysis reported 98.9% sensitivity for teledermatology melanoma diagnosis in countywide rollouts, which gives providers stronger confidence to embed digital triage tools inside the skin cancer dermatology tests market rather than treat them as a temporary access solution.

Reimbursement Support for Medically Necessary Diagnostic Workups

Reimbursement remains a strong growth support for the United States and Canada skin cancer dermatology tests market because CMS maintains structured Medicare coverage for melanoma molecular testing under LCD L38016 and for the Pigmented Lesion Assay under LCD L38153. These policies matter beyond Medicare because private payers often use CMS decisions as a benchmark when evaluating new diagnostics, which gives covered melanoma assays a clearer route into broader reimbursement. A U.S. payer model referenced by Blue Cross Blue Shield of Michigan showed annual net savings of USD 0.54 per member per month over 3 years when the Pigmented Lesion Assay was integrated into the melanoma diagnostic pathway, which supports the view that some tests can be positioned as cost offsets rather than pure added expense. CMS also delayed Clinical Laboratory Fee Schedule reporting requirements into a January-March 2026 collection window, while payment reductions for non-advanced diagnostic laboratory tests were capped at 0% in 2025, which temporarily eased immediate price pressure on established tests. Together, these policies make reimbursement a practical enabler for the skin cancer dermatology tests market even as newer platforms still need ongoing payer engagement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Sensitivity For Advanced Diagnostic Workups | -0.8% | United States nationally, amplified in high-deductible plan populations and uninsured segments | Short term (≤ 2 years) |

| Variable Clinical Adoption Across Non-Specialist Settings | -0.5% | Rural United States and remote Canadian provinces, with lower adoption in primary care than specialist settings | Medium term (2-4 years) |

| Limited Reimbursement Clarity For Novel Adjunctive Tests | -0.6% | United States nationally, Canada with provincial formulary variability | Medium term (2-4 years) |

| Workflow Friction From Confirmatory Biopsy Capacity Constraints | -0.4% | High-volume urban dermatopathology labs in the United States, concentrated in Northeast and Pacific Coast hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Sensitivity for Advanced Diagnostic Workups

High cost sharing remains a real constraint on the market because complex workups can combine dermoscopy, molecular testing, and confirmatory biopsy for a single suspicious lesion. The American Cancer Society reported that cancer-related out-of-pocket costs in the United States reached USD 16.2 billion in 2025, while total time and financial costs to patients were estimated at USD 21.1 billion, which shows the broader affordability pressure around cancer care decisions. In the United States and Canada skin cancer dermatology tests market, that pressure can cause patients to delay a biopsy even after a suspicious triage result, which directly reduces realized test volumes and slows treatment initiation. The problem is sharper for advanced molecular assays because patient cost sharing can become substantial even when the clinical need is high. This creates a gap between clinical value and completed utilization, especially in older and lower-income patient groups that already carry elevated disease risk.

Limited Reimbursement Clarity for Novel Adjunctive Tests

Reimbursement policy remains uneven across the market, and that unevenness is most visible between melanoma and cutaneous squamous cell carcinoma testing. CMS has maintained defined coverage pathways for melanoma molecular testing, yet it classifies molecular biomarker tests for cutaneous SCC risk stratification as non-covered because clinical validity and utility have not been established beyond existing clinicopathological criteria. That matters because non-melanoma disease held 71.31% of revenue in 2025, so the largest disease category in the United States and Canada skin cancer dermatology tests market still has a ceiling on reimbursable molecular expansion. The same policy uncertainty can slow adoption for newer adjunctive imaging and assessment tools when providers are not yet certain how broadly payers will reimburse them. As a result, technically capable products can still face long commercialization cycles while clinical evidence, payer policy, and utilization behavior move at different speeds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Non-Melanoma Volume Anchors the Market While Melanoma Drives Value Intensity

Non-melanoma skin cancer accounted for 71.31% of revenue in 2025 and remained the largest disease segment in the United States and Canada skin cancer dermatology tests market because of the very large annual volume of basal cell carcinoma and squamous cell carcinoma cases. The Skin Cancer Foundation reports 3.6 million annual U.S. basal cell carcinoma diagnoses and 1.8 million squamous cell carcinoma diagnoses, which supports a steady flow of biopsies and histopathology work in dermatology clinics and diagnostic laboratories[3]Skin Cancer Foundation, “Skin Cancer Facts & Statistics,” Skin Cancer Foundation, skincancer.org. This gives non-melanoma disease a stable volume base because the pathway from lesion review to biopsy and pathology remains familiar, repeatable, and widely used across care settings. At the same time, CMS non-coverage for molecular biomarker testing in cutaneous SCC limits how much the non-melanoma segment can lift value per patient despite its dominant role in testing volumes.

Melanoma is the fastest-growing cancer type segment and is projected to advance at a 6.38% CAGR through 2031, which makes it the value-intensive growth engine inside the market size by disease category. The segment is benefiting from broader use of gene expression profiling, stronger policy support for medically necessary melanoma assays, and rising detection of melanoma-in-situ lesions that need better pre-biopsy discrimination from benign lesions. Coverage of melanoma risk stratification testing and the Pigmented Lesion Assay also supports a broader diagnostic mix, since testing can now inform biopsy decisions and downstream management rather than serving only as a post-biopsy add-on. That mix shift explains why melanoma remains smaller in volume but stronger in revenue intensity within the skin cancer dermatology tests market.

By Test Type: Skin Biopsy Dominates Volume While Imaging Accelerates at the Frontier

Skin biopsy held 32.24% of revenue in 2025 and retained the leading position in the skin cancer dermatology tests market share by test type because histopathological confirmation remains the definitive basis for treatment-guiding diagnosis. The practical role of biopsy is reinforced by the high and recurring volume of suspicious lesions generated by non-melanoma disease, which keeps physician offices, outpatient settings, and pathology labs closely tied to biopsy-led workflows. Lymph node biopsy continues to matter in melanoma staging, while molecular tests are being added around the biopsy pathway to support risk assessment and decision making. Quest Diagnostics reinforced this part of the test landscape with the February 2024 launch of MelaNodal Predict, a gene expression assay intended to personalize melanoma risk prediction and help inform decisions around invasive surgery.

Imaging tests are projected to grow at a 7.52% CAGR through 2031, making them the fastest-expanding test category in the skin cancer dermatology tests market. Growth is being driven by reflectance confocal microscopy, line-field confocal optical coherence tomography, and AI-enhanced dermoscopy, all of which aim to improve lesion assessment before biopsy. A 2024 multicenter study found that adjunctive reflectance confocal microscopy delivered 97.8% sensitivity and 86.8% specificity for basal cell carcinoma, compared with 93.2% sensitivity and 51.7% specificity for dermoscopy alone, which supports stronger use of imaging as a pre-biopsy filter. The FDA reclassification that took effect in April 2026 should support more launches and sharper pricing competition in this category, while conventional dermatoscopy will continue to anchor lower-cost screening and teledermatology workflows across the skin cancer dermatology tests market.

By End Use: Hospitals Lead Volume While Ambulatory Centers Capture Efficiency-Driven Share

Hospitals and clinics represented 55.52% of revenue in 2025 and led the skin cancer dermatology tests market size by end use because complex diagnostic workups still cluster where specialist access, imaging platforms, and downstream pathology coordination are strongest. These settings remain central for cases that require multi-modal imaging, lymph node biopsy, or molecular profiling, especially when oncology and dermatology teams need to coordinate around higher-risk lesions. Diagnostic laboratories form the second operational layer of this end-use structure by processing biopsy and molecular samples generated upstream in clinics and hospitals. Quest Diagnostics illustrates that scale through its Dermpath Diagnostics network of more than 75 dermatopathologists, which shows how specialized lab infrastructure is embedded in the broader workflow of the skin cancer dermatology tests market.

Ambulatory surgical centers are projected to record the fastest end-use CAGR at 7.25% through 2031, which points to a gradual migration of suitable procedures into lower-cost outpatient settings. The shift reflects the fact that skin biopsies and minor excisions can often be performed in focused procedural environments without the overhead tied to hospital outpatient departments. That makes ambulatory centers well positioned to benefit as providers look for faster throughput and more efficient site-of-care models. Even so, hospitals and integrated clinics should remain the main channel for the most complex cases in the skin cancer dermatology tests market because they retain deeper imaging access, oncology links, and specialist support.

Geography Analysis

The United States accounted for 85.54% of combined revenue in 2025 and remained the core geography in the skin cancer dermatology tests market size because it combines the highest absolute melanoma burden with the broadest reimbursement and device adoption infrastructure. The country also benefits from a dense network of academic dermatology centers and specialized labs that can absorb biopsy, imaging, and molecular workflows at scale. Age-adjusted melanoma death rates in the United States declined by an average of 2.2% per year over 2015-2024, which supports the view that earlier detection and structured workups are already improving clinical outcomes. Large employer-sponsored plans are adding to this demand base because Business Group on Health has explicitly encouraged stronger cancer prevention and screening coverage design, including skin cancer screening, as part of cost-control and early detection strategies.

Canada is projected to grow at a 6.25% CAGR through 2031 and is the faster-growing geography in the skin cancer dermatology tests market, even though it starts from a smaller base. The Canadian Cancer Society projected 11,300 new melanoma diagnoses in 2026, which keeps the need for diagnostic access expansion high. A 2025 population-based study also noted that the economic burden from skin cancer in Canada is approaching USD 1 billion, which supports the health system case for earlier lesion assessment and faster diagnostic triage. Melanoma incidence is not evenly distributed across the country because Prince Edward Island, Nova Scotia, and coastal New Brunswick report rates above the national average, which points to localized pockets of unmet diagnostic demand. Teledermatology has extra relevance in Canada because remote triage can help underserved provinces move suspicious lesions into specialist review faster without waiting for full in-person access.

Competitive Landscape

The United States and Canada skin cancer dermatology tests market remains moderately fragmented because revenue is spread across large diagnostic laboratories, specialist molecular companies, and AI-enabled device developers rather than controlled by a small group of dominant suppliers. Quest Diagnostics and Laboratory Corporation of America hold structural advantages in biopsy-linked lab services because scale, physician relationships, and dermatopathology capacity are hard to replicate quickly. Specialist companies such as DermTech, Castle Biosciences, and DermaSensor are competing in narrower areas of the United States and Canada skin cancer dermatology tests market where non-invasive assessment, molecular profiling, and AI-supported lesion review matter more than broad lab footprint. In this setting, competitive differentiation depends more on clinical evidence, reimbursement progress, and workflow fit than on simple test menu breadth.

Competition is becoming sharper because the FDA’s 2026 device reclassification reduced the regulatory burden for melanoma optical diagnostic devices and electrical impedance spectrometers, which should encourage more entrants in the AI-adjunctive segment. Quest Diagnostics strengthened its position in melanoma-related molecular testing through the February 2024 launch of MelaNodal Predict, which supports more personalized decisions around invasive surgery. Quest also broadened its oncology diagnostics platform in June 2025 through an agreement with the University of Texas MD Anderson Cancer Center to develop a Multi-Cancer Stratification blood test based on circulating protein biomarkers. Roche made the largest strategic move in the supplied material when it entered a definitive agreement in May 2026 to acquire PathAI for USD 750 million, with up to USD 300 million in milestone payments, which shows how major diagnostics groups are using acquisition to accelerate digital pathology and AI capability. These actions suggest that leading companies increasingly want multi-modal portfolios that combine pathology, molecular insight, and software-enabled interpretation inside the United States and Canada skin cancer dermatology tests market.

There is still open space in the United States and Canada skin cancer dermatology tests market for point-of-care spectroscopy, stronger molecular tools for SCC risk stratification, and platforms that can combine imaging outputs with molecular decision support. That white space exists because reimbursement clarity is stronger in melanoma than in SCC, which leaves part of the largest disease category less developed for higher-value adjunctive testing. It also means companies with physician access, evidence generation capability, and payer negotiation strength should stay better positioned than firms that rely on technical performance alone. The competitive pattern therefore remains balanced between incumbents that control core workflow infrastructure and specialists that are trying to expand specific diagnostic steps across the skin cancer dermatology tests market.

United States and Canada Skin Cancer Dermatology Tests Industry Leaders

Castle Biosciences, Inc.

DermaSensor, Inc.

Canfield Scientific, Inc.

FotoFinder Systems GmbH

DermTech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The US FDA issued a final order reclassifying optical diagnostic devices for melanoma detection (product code OYD) and electrical impedance spectrometers (product code ONV) from Class III to Class II (special controls), effective April 24, 2026. The reclassification introduces a 510(k) pathway for these AI-adjunctive diagnostic devices, substantially reducing market entry barriers for device developers.

- June 2025: Quest Diagnostics entered an agreement with the University of Texas MD Anderson Cancer Center to develop and validate a Multi-Cancer Stratification (MCaST) blood test based on circulating protein biomarkers, targeting 10 cancer types. The partnership extends Quest's precision oncology capabilities into multi-cancer detection.

United States and Canada Skin Cancer Dermatology Tests Market Report Scope

As per the scope of the report, skin cancer dermatology tests are medical examinations and procedures used to detect, diagnose, and evaluate skin cancer. These tests help dermatologists identify abnormal skin growths, moles, or lesions that may be cancerous or precancerous.

The segmentation of the United States and Canada skin cancer dermatology tests market is categorized by cancer type, test type, end use, and country. By cancer type, the market is divided into melanoma and non-melanoma. By test type, it includes dermatoscopy, skin biopsy, lymph node biopsy, imaging tests, and genetic and molecular tests. By end use, the market is segmented into hospitals and clinics, diagnostic laboratories, dermatology clinics, and ambulatory surgical centers. By country, the segmentation covers the United States and Canada. For each segment, the market size and forecast are provided in terms of value (USD).

| Melanoma |

| Non-Melanoma |

| Dermatoscopy |

| Skin Biopsy |

| Lymph Node Biopsy |

| Imaging Tests |

| Genetic and Molecular Tests |

| Hospitals and Clinics |

| Diagnostic Laboratories |

| Dermatology Clinics |

| Ambulatory Surgical Centers |

| United States |

| Canada |

| By Cancer Type | Melanoma |

| Non-Melanoma | |

| By Test Type | Dermatoscopy |

| Skin Biopsy | |

| Lymph Node Biopsy | |

| Imaging Tests | |

| Genetic and Molecular Tests | |

| By End Use | Hospitals and Clinics |

| Diagnostic Laboratories | |

| Dermatology Clinics | |

| Ambulatory Surgical Centers | |

| Country | United States |

| Canada |

Key Questions Answered in the Report

What is driving growth in United States and Canada skin cancer dermatology testing through 2031?

Growth is being supported by a rise in melanoma burden, large non-melanoma case volumes, broader use of AI-assisted and molecular tools, and a forecast increase from USD 3.77 billion in 2026 to USD 4.86 billion by 2031 at a 5.25% CAGR.

Which cancer category generates the largest testing demand?

Non-melanoma skin cancer leads demand because it held 71.31% of revenue in 2025 and is supported by very high annual basal cell carcinoma and squamous cell carcinoma volumes in the United States.

Which test format is expanding the fastest?

Imaging tests are projected to grow at a 7.52% CAGR through 2031 as reflectance confocal microscopy, LC-OCT, and AI-enhanced dermoscopy gain wider use as pre-biopsy assessment tools.

Why do hospitals and clinics still lead end-use revenue?

Hospitals and clinics held 55.52% of revenue in 2025 because they remain the main setting for complex diagnostic workups that require specialist access, imaging, pathology coordination, and molecular testing support.

Why is Canada growing faster than the United States?

Canada is projected to expand at a 6.25% CAGR through 2031 because melanoma diagnoses remain significant, some provinces show above-average incidence, and teledermatology can improve access in underserved areas.

What is the main commercial risk for newer molecular and adjunctive tests?

The main risk is reimbursement inconsistency, since melanoma assays have clearer CMS pathways while molecular biomarker tests for cutaneous SCC remain non-covered, which limits expansion in the largest disease segment.

Page last updated on: