Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

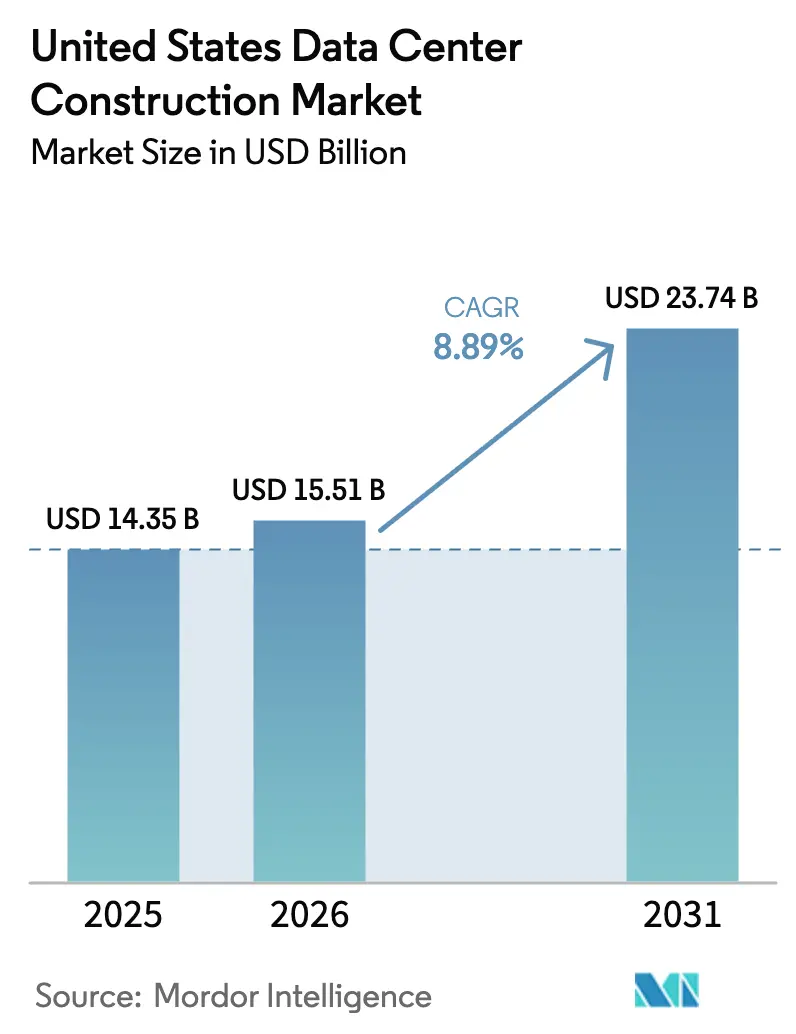

| Base Year Market Size (2025) | USD 14.35 Billion |

| Market Size (2026) | USD 15.51 Billion |

| Market Size (2031) | USD 23.74 Billion |

| Growth Rate (2026 - 2031) | 8.89% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Data Center Construction Market Analysis by Mordor Intelligence

The United States (US) data center construction market size was valued at USD 14.35 billion in 2025 and is estimated to grow from USD 15.51 billion in 2026 to reach USD 23.74 billion by 2031, at a CAGR of 8.89% during the forecast period (2026-2031). Hyperscaler self-build pipelines now exceed 10 gigawatts, steering capital toward higher-density campuses that require liquid-cooling retrofits and on-site power generation. Electrical infrastructure captured 40.17% of 2025 spending, yet mechanical infrastructure is growing fastest at 9.87% as average rack power climbs from 8 kilowatts in 2024 to 15 kilowatts in 2026. Power-grid interconnection delays, multi-year transformer lead times, and land prices topping USD 1 million per acre in tier-1 hubs are redirecting projects to secondary metros that offer shorter utility queues and richer incentives. Environmental, social, and governance rules are pushing operators toward closed-loop liquid cooling and small modular reactors that decouple load growth from strained grids.

Key Report Takeaways

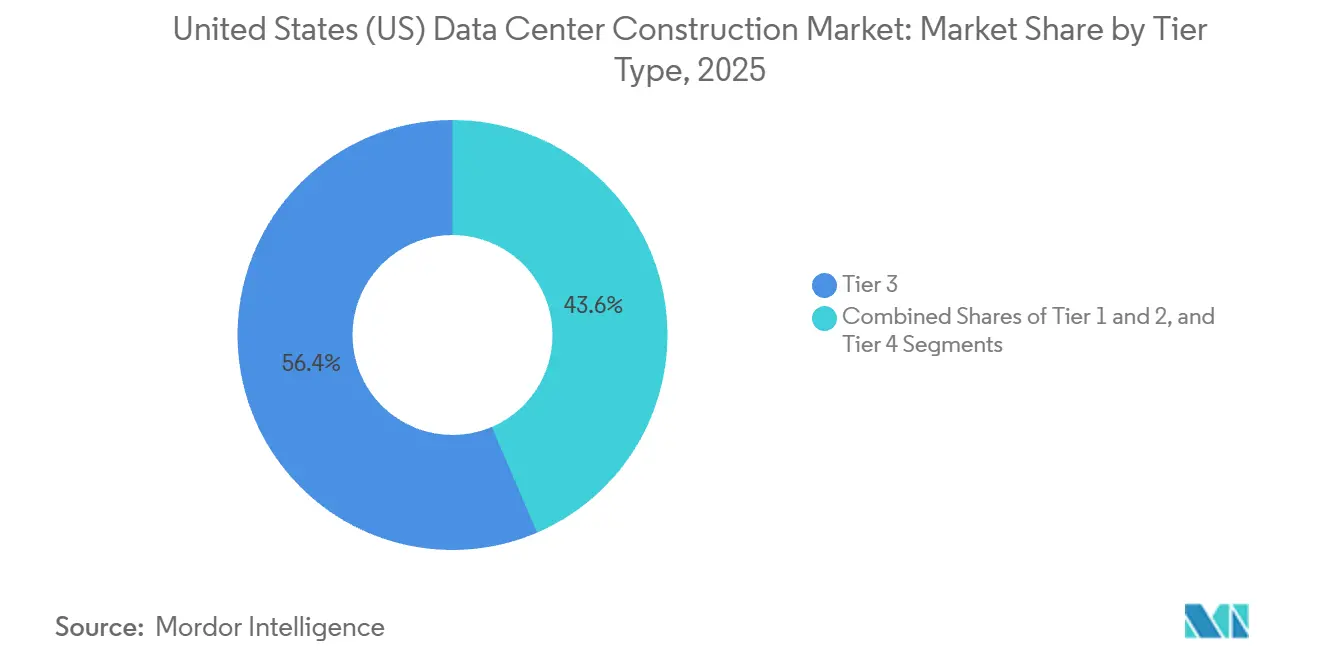

- By tier type, Tier 3 facilities led with 56.43% of the United States data center construction market share in 2025, while Tier 4 builds are positioned for a 9.12% CAGR through 2031.

- By data center size, hyperscale installations accounted for 64.31% of the United States data center construction market share in 2025 and are projected to advance at a 9.45% pace through 2031.

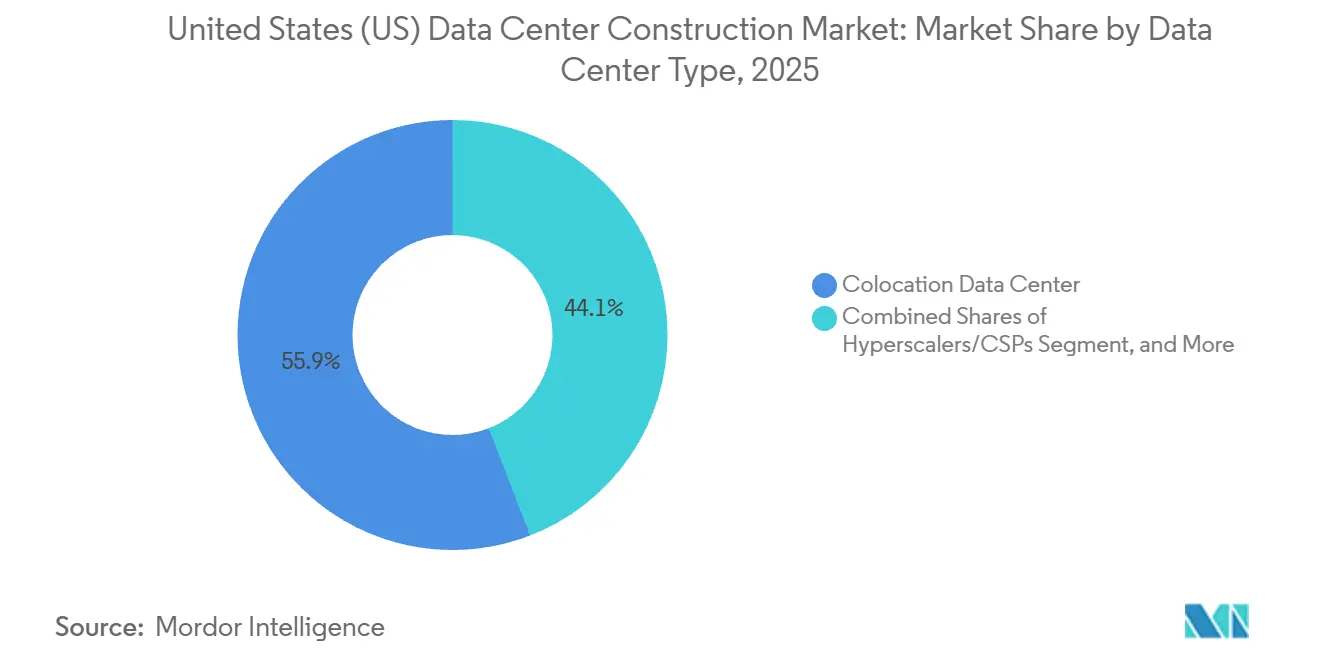

- By data center type, colocation providers accounted for 55.88% of 2025 spending, while hyperscalers were the fastest-growing segment at 9.75% as they internalize capacity.

- By infrastructure, electrical infrastructure accounted for 40.17% of 2025 outlays, whereas mechanical infrastructure is projected to post the strongest 9.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud, AI and Big-Data Workload Boom | +2.4% | Nationwide, focus on Northern Virginia, Silicon Valley, Phoenix, Dallas-Fort Worth | Medium term (2-4 years) |

| Hyperscale Self-Build Pipelines Above 10 GW | +2.1% | Nationwide, led by Virginia, Texas, Mississippi, Louisiana | Long term (≥ 4 years) |

| AI-Optimized Liquid-Cooling Retrofits Drive Rebuild Spend | +1.6% | Nationwide, early adoption in Northern Virginia, Silicon Valley, Chicago | Short term (≤ 2 years) |

| Edge and 5G Densification of Metro Clusters | +1.3% | Nationwide, early gains in New York, Los Angeles, Miami, Seattle | Medium term (2-4 years) |

| Federal and State Tax-Incentive Packages | +0.9% | Virginia, Texas, Ohio, Georgia, North Carolina | Short term (≤ 2 years) |

| On-Site Micro-Nuclear SMR Approvals Accelerate Greenfield Sites | +0.6% | Pennsylvania, Ohio, Virginia, emerging in Texas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud, AI and Big-Data Workload Boom

Generative AI inference clusters have doubled average rack loads, pushing design densities to 15 kilowatts in 2026 and an expected 25 kilowatts by 2028. Operators are retrofitting rear-door heat exchangers and direct-to-chip loops, which add USD 1.5 million to USD 2 million per megawatt to budgets. Amazon Web Services committed USD 11 billion to Pennsylvania sites, and Microsoft reserved USD 80 billion globally for AI-optimized campuses, illustrating hyperscaler capital redeployment.[1]Editorial Board, “Thermal Guidelines for Data Processing,” ASHRAE, ashrae.org With the United States hosting more than half of the world’s hyperscale inventory, demand is bifurcating between 100-megawatt campuses for training and sub-1-megawatt edge nodes for low-latency inference.

Hyperscale Self-Build Pipelines Above 10 GW

Amazon Web Services, Microsoft Azure, Google Cloud, and Meta together hold over 10 gigawatts of active projects. Meta confirmed a USD 10 billion Louisiana campus, and Google added USD 1 billion in Texas expansion, signaling migration to secondary markets where land and utility interconnection costs are up to 60% lower than tier-1 hubs. Hyperscalers now self-perform civil work, hire specialists for mechanical and electrical scopes, and compress schedules from 24 months to 18 months, reducing general-contractor addressable value by roughly 25%.

AI-Optimized Liquid-Cooling Retrofits Drive Rebuild Spend

Rack densities above 20 kilowatts make raised-floor air cooling thermodynamically inefficient. Direct-to-chip manifolds and rear-door heat exchangers are standard in new builds, and the legacy air-cooled base represents a USD 4-6 billion retrofit opportunity through 2031. Vertiv and Schneider Electric offer skid-mounted liquid-cooling units that cut downtime in half, while Microsoft and Meta piloted immersion-cooled racks in Arizona and Oregon. ASHRAE raised allowable inlet temperatures to 27 °C for liquid systems, reducing chiller capacity requirements by up to 20%.[2]Federal Energy Regulatory Commission, “Interconnection Reform Notice,” ferc.gov

Edge and 5G Densification of Metro Clusters

Latency-sensitive services require compute within 10 milliseconds of users, driving demand for 100-kilowatt to 2-megawatt edge nodes colocated with 5G hubs and retail points of presence. The Infrastructure Investment and Jobs Act allocates USD 65 billion to broadband backhaul that enables edge economics in rural markets. Verizon targets 100 edge locations by 2027, and AT&T plans 75 by 2026, each using prefabricated containers that install in six weeks, versus the 18-month timeline of conventional halls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-Grid Interconnection Delays (3-6 Years) | -1.8% | Nationwide, acute in Northern Virginia, Phoenix, Silicon Valley, Atlanta | Long term (≥ 4 years) |

| Transformer and Switch-Gear Supply-Chain Choke Points | -1.2% | Nationwide | Medium term (2-4 years) |

| Soaring Land Prices Around Tier-1 Metros | -0.7% | Northern Virginia, Silicon Valley, Phoenix, Dallas-Fort Worth | Short term (≤ 2 years) |

| ESG-Driven Municipal Moratoria on Water-Intensive Cooling | -0.5% | Mesa, Arizona; Prince William County, Virginia; emerging in California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power-Grid Interconnection Delays (3-6 Years)

National queues exceed 2,600 gigawatts, stretching median approvals to five years. Dominion Energy alone lists 47 gigawatts of pending data-center load in Northern Virginia. Arizona Public Service froze new data-center hookups in late 2024, redirecting projects to Texas and Ohio. Developers are funding on-site peaker plants and small modular reactors that add USD 3 million to USD 5 million per megawatt but avoid queue risk, while Federal Energy Regulatory Commission reforms, slated for 2027, aim to streamline approvals.[3]Staff Author, “Microsoft Announces USD 80 Billion AI Data Center Plan,” microsoft.com

Transformer and Switch-Gear Supply-Chain Choke Points

Lead times for >100 megavolt-ampere transformers range from 24 to 30 months as electric-vehicle and renewable-energy projects compete with data-center demand. ABB and Siemens backlogs push delivery into 2027, forcing developers to pre-order 18 months ahead of groundbreaking. Some operators deploy multiple smaller transformers in parallel to reduce wait times, but this approach increases footprint and maintenance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Fault Tolerance Fuels Tier 4 Momentum

Tier 3 sites held 56.43% share in 2025, favored for concurrent maintainability at a 20%-30% cost discount versus Tier 4 designs. However, fault-tolerant Tier 4 builds are on track for a 9.12% CAGR, the fastest within the United States data center construction market size. Banking, healthcare, and government tenants demand 99.995% uptime, prompting colocation operators to retrofit Tier 3 halls with dual utility feeds and 2N uninterruptible power supply racks. Uptime Institute’s 2024 survey showed 38% of U.S. builds sought Tier 4 certification, up from 29% in 2022, a jump driven partly by cyber-insurance underwriters.

Colocation leaders Equinix and Digital Realty are layering Tier 4 features onto existing campuses to secure premium workloads, while Amazon Web Services included multiple Tier 4 campuses in its USD 11 billion Pennsylvania program to support GovCloud clients. As more enterprises require fault-tolerant hosting, contractors focused on redundant electrical paths and liquid-cooled backup modules stand to gain the largest share of Tier 4 spending.

By Data Center Size: Hyperscale Dominance Redefines Economics

Hyperscale campuses above 10 megawatts controlled 64.31% of 2025 build volume and are projected to grow at 9.45% annually, underscoring their weight in the United States data center construction market. Economies of scale in power procurement, modular cooling, and labor reduce per-megawatt costs by as much as 40% against medium-sized halls, prompting cloud providers to favor 100-200 megawatt master-planned sites.

Medium facilities between 1 megawatt and 10 megawatts still serve hybrid colocation tenants but face slower growth as workloads shift to cloud. Small sub-1 megawatt facilities bifurcate into decommissioned enterprise rooms and rising edge nodes. Broadband subsidies and 5G densification make edge builds financially viable in tier-2 and rural metros, a niche where modular specialists like Mortenson and Balfour Beatty deliver turnkey enclosures in under 45 days.

By Data Center Type: Vertical Integration Compresses Colocation Margins

Colocation operators retained 55.88% share in 2025, yet hyperscalers are pacing the fastest 9.75% growth as they bring capacity in-house to manage latency, security, and cost. Amazon Web Services, Microsoft Azure, Google Cloud, and Oracle Cloud collectively added more than 3 gigawatts of owned footprint during 2024-2025, outstripping the expansion rate of the top five colocation firms.

Consolidation is underway: Digital Realty acquired Teraco and Equinix purchased MainOne in 2024 to bolster interconnection density and regional reach. Colocation players are differentiating through edge nodes, renewable-linked campuses, and hybrid-cloud on-ramps. Enterprise data centers continue to retire, yet compliance and latency needs keep retrofit budgets intact. Edge builds capture telecom interest as Verizon and AT&T deploy containerized compute near 5G radios.

By Infrastructure: Mechanical Spend Surges on Liquid Cooling

Electrical systems absorbed 40.17% of 2025 construction outlays, but mechanical systems are slated for the highest 9.87% CAGR through 2031 as liquid-cooling uptake accelerates. Tier 3 and Tier 4 designs demand redundant switchgear and dual utility feeds, keeping power distribution the largest electrical sub-segment. Battery energy storage modules are incrementally replacing diesel-only ride-through, while hydrogen fuel-cell pilots surface in select campuses.

Cooling leads mechanical growth. Vertiv’s 2024 results showed liquid-cooling revenue up 65% year-over-year, and Schneider Electric launched 42U racks rated at 50 kilowatts. Servers, racks, and storage increasingly ship in prefabricated data-hall modules that compress site labor by up to 30%, though this shift narrows general-contractor margins. Design-build firms that master prefabrication workflows and liquid-cooling integration capture outsized value.

Geography Analysis

Northern Virginia maintained roughly 25%-30% of 2025 national builds, yet five-year queue delays and USD 1 million-per-acre land costs are steering projects to states such as Pennsylvania, Mississippi, and Ohio. Amazon Web Services’ USD 11 billion Pennsylvania and USD 10 billion Mississippi commitments exemplify this diversification. Phoenix ranked second in 2025, but an Arizona Public Service moratorium and Mesa’s ban on water-cooled permits threaten future growth.

Silicon Valley expansion is cooling as land scarcity and environmental regulations are driving build costs to USD 15 million per megawatt, a 40% premium over the United States data center construction market average. Dallas-Fort Worth and Atlanta absorb displaced demand with competitive power rates, fiber density, and state tax exemptions. Google’s USD 1 billion Texas addition and Meta’s USD 10 billion Louisiana build highlight Gulf Coast momentum.

The Pacific Northwest leverages hydroelectric rates below USD 0.025 kWh, yet wildfire and transmission constraints cap growth. Emerging markets such as Indiana, North Carolina, and Ohio attract hyperscalers through proactive utility planning and decade-long sales-tax holidays on equipment. Edge densification clusters in New York, Los Angeles, Chicago, and Miami, where Verizon and AT&T deploy containerized compute within 10 milliseconds of end users.

Competitive Landscape

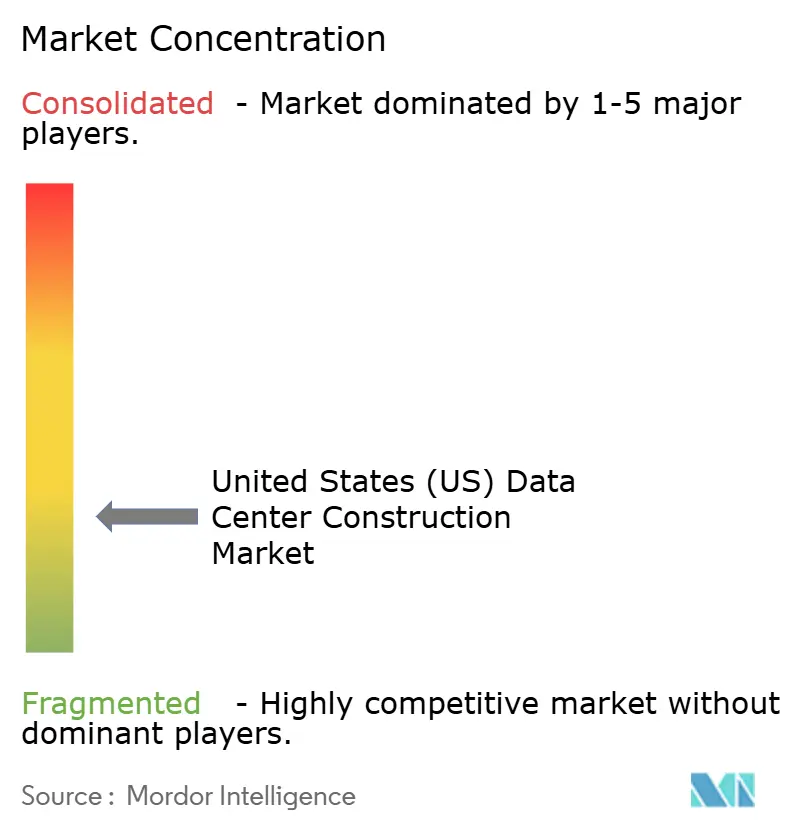

Market fragmentation persists despite billion-dollar project sizes. Turner Construction, DPR Construction, and AECOM hold the inside track on hyperscale awards thanks to mission-critical credentials and deep benches of specialized subcontractors. Hyperscalers self-perform civil work, outsource mechanical and electrical scopes, and favor prefabricated modules that cut onsite labor by 30% and shrink commissioning from 18 months to 12 months. Digital Realty’s modular data-hall template and QTS Realty Trust’s power-skid strategy illustrate this shift.

Mechanical-electrical specialists such as Jacobs Solutions and Black & Veatch earn higher margins on liquid-cooling retrofits and power upgrades that demand deep domain knowledge. Small modular reactor integration opens white space for contractors with nuclear licensing expertise, as shown by Amazon Web Services’ 5-gigawatt partnership with X-energy and Talen Energy’s 960-megawatt nuclear campus.

Edge projects favor regional firms able to deliver containerized halls in under six weeks, a niche filled by Balfour Beatty US and Mortenson Construction. Contractors investing in building information modeling, digital twins, and off-site fabrication secure 15%-20% cost advantages, winning repeat hyperscaler contracts and expanding market share.

United States Data Center Construction Industry Leaders

AECOM

Turner Construction

DPR Construction

Holder Construction

Skanska USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amazon Web Services closed on land parcels for its USD 11 billion Pennsylvania program and commenced substation upgrades, with phase-one capacity expected online in 2028.

- January 2025: Amazon Web Services unveiled a USD 10 billion Mississippi build plan aimed at leveraging low-cost power and state incentives, with initial hall delivery set for 2027.

- October 2024: Google announced a USD 1 billion Texas campus expansion, adding 300 megawatts of capacity and on-site solar plus battery storage to meet 90% carbon-free energy by 2027.

- September 2024: QTS Realty Trust accelerated a 30 megawatt Atlanta-Metro expansion featuring prefabricated power skids and rear-door heat exchangers, trimming build time by six months.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States data center construction market as the spending associated with planning, designing, building, and fitting out purpose-built facilities that host IT equipment and the supporting electrical, mechanical, and general construction systems required to meet prescribed availability tiers. It captures greenfield campuses as well as major brownfield expansions across colocation, hyperscaler self-build, enterprise, and emerging edge formats.

Scope Exclusions: We do not count routine facility maintenance, modular container rentals, server procurement, or multi-tenant lease revenues.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Size

- Small

- Medium

- Large

- Hyperscale

- By Data Center Type

- Colocation Data Center

- Hyperscalers/Cloud Service Provider (CSPs)

- Enterprise and Edge Data Center

- By Infrastructure

- Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Services - Design and Consulting, Integration, Support and Maintenance

- Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed design-build contractors, hyperscale development managers, specialist equipment vendors, and regional economic development officials across Northern Virginia, Texas, Ohio, and Arizona. These discussions validated construction costs per megawatt, supply chain lead times, and the practical adoption pace of liquid cooling and on-site generation.

Desk Research

We opened the analysis with structured reviews of public datasets from the U.S. Census Bureau Construction Put-in-Place survey, Energy Information Administration power statistics, and Bureau of Labor Statistics cost indices. Trade bodies such as the Uptime Institute, AFCOM, and the Data Center Coalition provided tier certificate volumes and project pipelines, while SEC filings from listed real estate trusts and utility interconnection queues illustrated capacity and cost trends. Paid resources, notably D&B Hoovers for contractor financials and Dow Jones Factiva for deal flow, complemented these open sources. The list is illustrative; many additional references underpin our database.

Market-Sizing & Forecasting

We used a top-down reconstruction that begins with annual construction spending reported by federal statistics, which is then split by facility type using penetration ratios from utility queue data and building permits, followed by tier level allocation informed by Uptime certificate logs. Bottom-up checks, via sampled contractor revenues and average selling price per MW audits, refined totals. Key variables in our forecast model include hyperscale CAPEX announcements, transformer lead time inflation, rack power density progression, utility capacity availability, and state level tax incentives. A multivariate regression coupled with scenario analysis projects 2025-2030 values and aligns with consensus ranges gathered during primary interviews. Data gaps on privately funded projects were bridged by conservative imputation anchored to disclosed power capacity builds.

Data Validation & Update Cycle

Outputs pass three-layer peer review, variance tests against external cost indices, and reconciliation with newly issued building permits. We refresh the model each year and trigger interim updates when cumulative variance exceeds five percent or a marquee project over one gigawatt reaches financial close.

Why Mordor's United States Data Center Construction Baseline Is Dependable

Published estimates often differ because firms track dissimilar expenditure buckets, apply varied cost per megawatt assumptions, or freeze models for several years before refreshing. Our disciplined scope alignment, annual update cadence, and dual path validation give decision makers a balanced, transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.35 B | Mordor Intelligence | NA |

| USD 48.18 B (2024) | Global Consultancy A | Includes IT equipment procurement and counts announced projects without probability weighting |

| USD 88.09 B (2024) | Industry Association B | Aggregates North American spend and converts at list price build costs |

| USD 67.00 B (2025) | Regional Consultancy C | Omits edge builds under 5 MW and applies aggressive cost inflation multipliers |

These comparisons show that Mordor's carefully scoped, frequently refreshed approach delivers a transparent, decision ready view that clients can trace to verifiable spending streams.

Key Questions Answered in the Report

What annual growth rate is forecast for United States data center construction?

Spending is anticipated to rise at an 8.89% CAGR from 2026 to 2031.

Which tier category is expanding fastest?

Tier 4 facilities, designed for 99.995% uptime, are expected to grow at 9.12% per year through 2031.

Why are hyperscalers choosing to self-build?

Self-builds let hyperscalers control latency, security, and power sourcing while reducing per-megawatt costs by up to 40%.

What supply-chain bottleneck most affects project schedules?

Large power transformers face 24-30-month lead times, often delaying project kick-off.

How are operators cooling higher-density racks?

Direct-to-chip and immersion systems are standard in new halls, whereas legacy sites add rear-door heat exchangers during retrofits.

Which regions are attracting new mega-campuses?

Pennsylvania, Mississippi, Texas, and Ohio lead due to shorter utility queues, lower land costs, and sizeable tax incentives.

Page last updated on: