Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

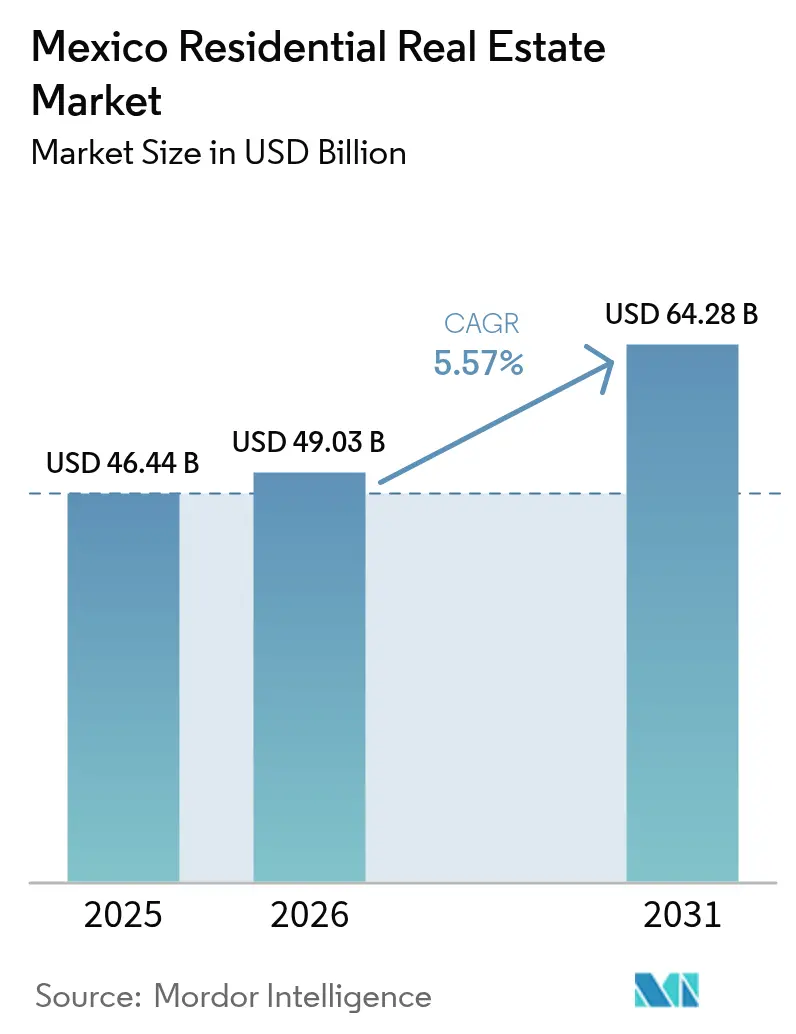

| Base Year Market Size (2025) | USD 46.44 Billion |

| Market Size (2026) | USD 49.03 Billion |

| Market Size (2031) | USD 64.28 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

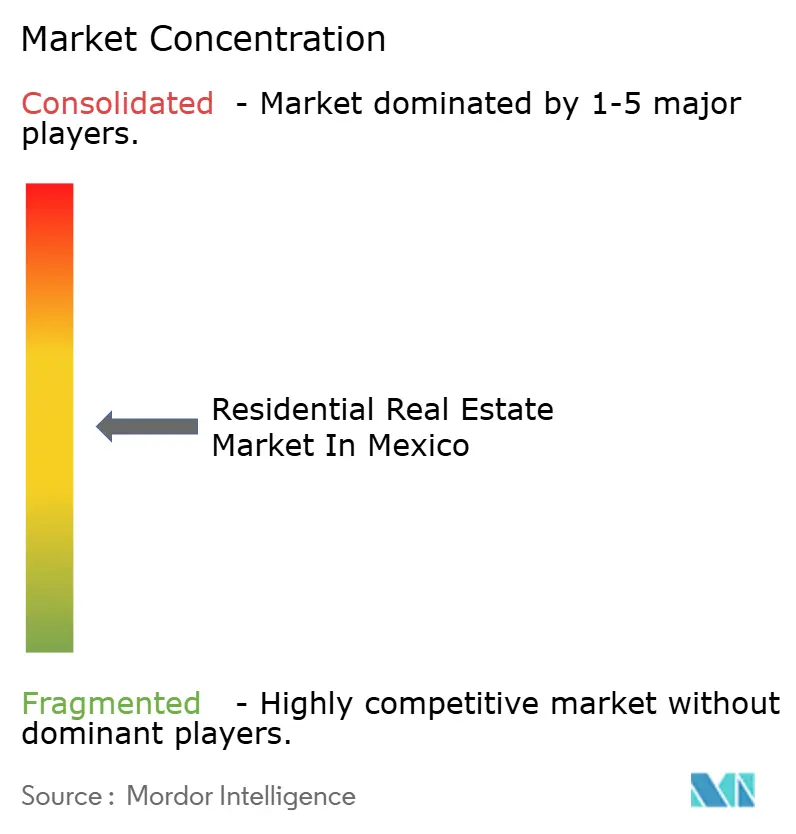

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Residential Real Estate Market Analysis by Mordor Intelligence

Mexico Residential Real Estate Market size in 2026 is estimated at USD 49.03 billion, growing from 2025 value of USD 46.44 billion with 2031 projections showing USD 64.28 billion, growing at 5.57% CAGR over 2026-2031. Robust household formation, government-backed finance reforms, and nearshoring-driven employment gains are collectively reinforcing demand despite construction-cost headwinds. President Claudia Sheinbaum’s National Housing Program, backed by MXN 600 billion (USD 32.4 billion) in federal spending, is set to inject 1 million new dwellings, strengthening affordable supply pipelines. Parallel INFONAVIT and CONAVI initiatives are widening credit access through rent-to-own schemes and capped salary deductions, nurturing both purchase and rental uptake. Developers are consolidating to scale production, while vertical projects in Mexico City, Monterrey, and Guadalajara are redefining urban living models.

Key Report Takeaways

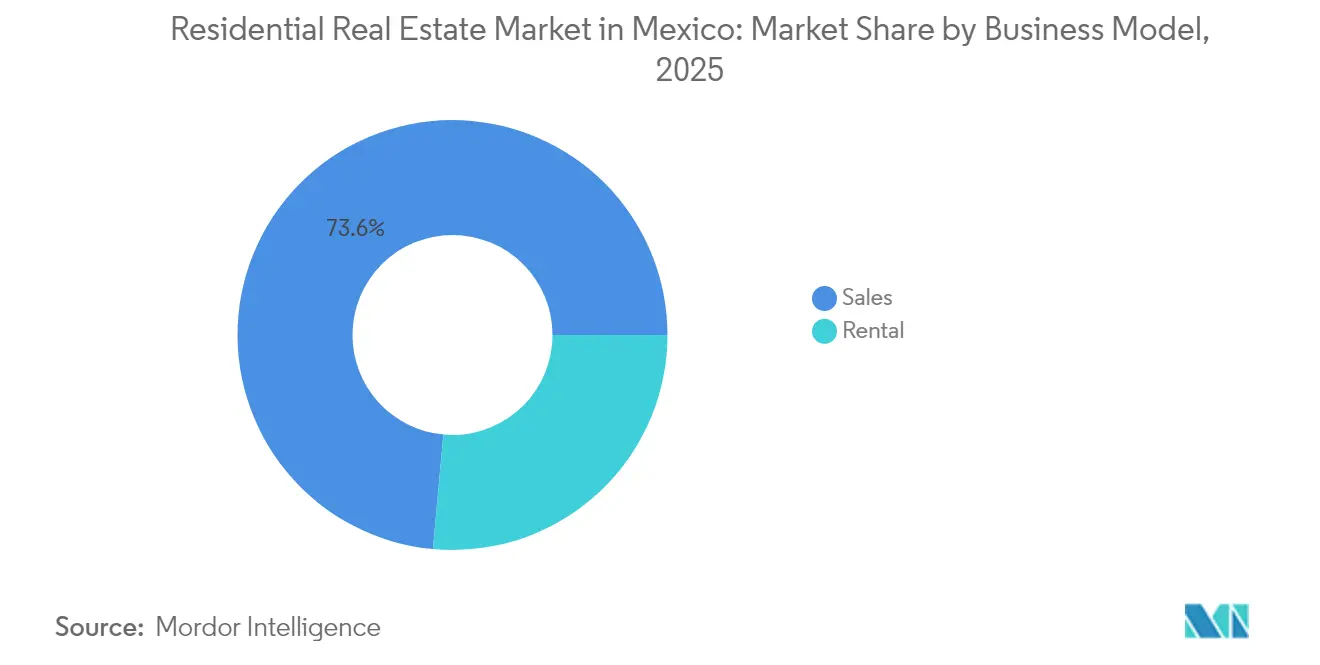

- By business model, sales held 73.55% of the Mexico residential real estate market share in 2025, whereas the rental segment is forecast to post the fastest 5.93% CAGR through 2031.

- By property type, apartments and condominiums captured 62.85% revenue in 2025; villas and landed houses are projected to expand at a 6.02% CAGR to 2031.

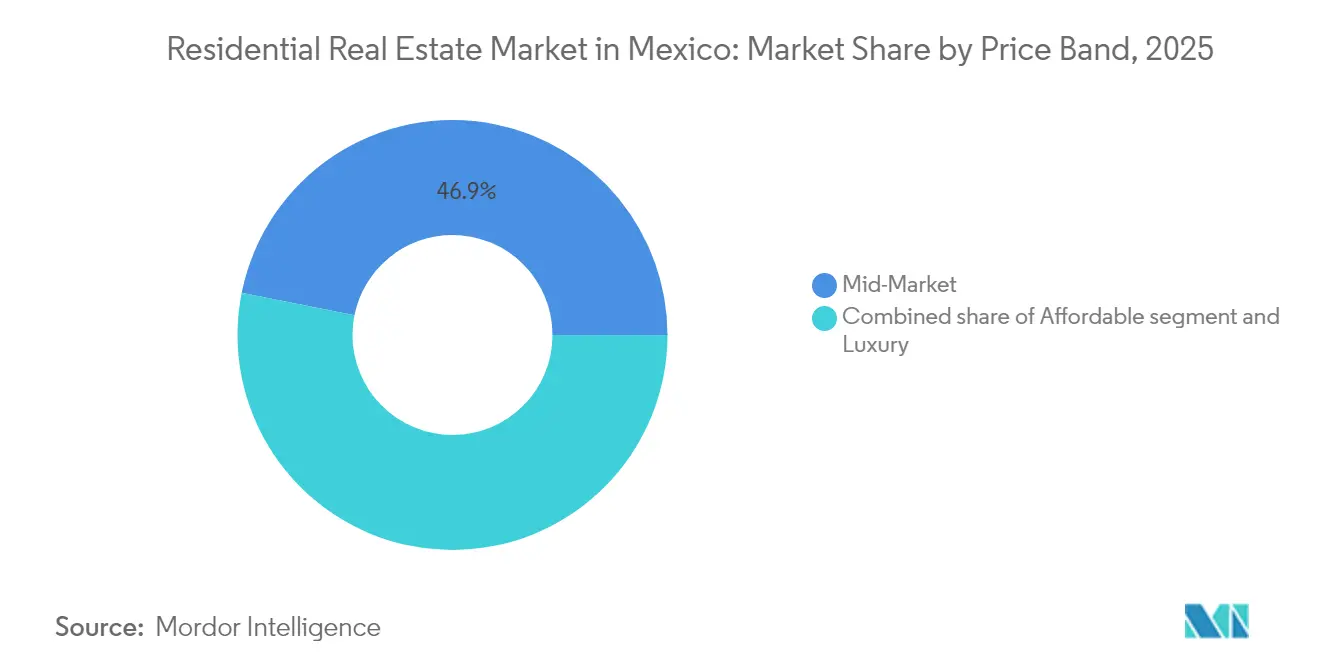

- By price band, mid-market dwellings accounted for 46.85% of the Mexico residential real estate market size in 2025, while luxury homes are advancing at a 6.28% CAGR through 2031.

- By mode of sale, the secondary segment represented a 54.05% share of the Mexico residential real estate market size in 2025 and is growing at a 6.17% CAGR through 2031.

- By state, Mexico City led with a 30.35% Mexico residential real estate market share in 2025; Querétaro is expected to record the highest 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent housing deficit sustaining long-term residential demand | +1.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Government-backed housing finance programs improving affordability and access | +1.5% | National, prioritizing marginalized areas | Medium term (2-4 years) |

| Expanding middle-class population driving demand for mid- and premium housing | +1.2% | Mexico City, Monterrey, Guadalajara metropolitan areas | Long term (≥ 4 years) |

| Urban infrastructure development creating new residential growth corridors | +0.8% | CDMX, Nuevo León, Jalisco, Querétaro | Medium term (2-4 years) |

| Growing preference for vertical and gated housing in dense urban areas | +0.6% | Major metropolitan areas and satellite cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Housing Deficit Sustaining Long-Term Residential Demand

Mexico’s structural shortage of roughly 9 million units keeps demand elevated across every income tier. More than 57.3% of the current stock remains self-built, revealing extensive quality gaps. Workers earning one to two minimum wages—about 7.3 million people—face the sharpest access barriers, prompting INFONAVIT to launch Infonavit Constructora S.A. de C.V. in 2025 to start 20,000 centrally located homes. This supply push, paired with federal subsidies, is expected to accelerate deliveries and relieve backlog pressure[1]Diego Prieto, “Encuesta Nacional de Vivienda 2024,” Instituto Nacional de Estadística y Geografía, inegi.org.mx.

Government-Backed Housing Finance Programs Improving Affordability and Access

February 2025 reforms froze balances on 2 million existing mortgages, capped salary deductions at 20% for loans and 30% for rent, and introduced social leasing that converts rent payments into equity. FOVISSSTE-INFONAVIT Unidos now lets public and private workers combine credits, lifting joint purchasing power. CONAVI’s 2025 mandate funds 100,000 new dwellings and 100,000 upgrades across 1,345 municipalities, with 20% reserved for affordable rentals. These measures collectively lower entry barriers and reshape tenure preferences[2]Alejandro Murat, “Reformas a la Ley del INFONAVIT 2025,” Diario Oficial de la Federación, dof.gob.mx.

Expanding Middle-Class Population Driving Demand for Mid- and Premium Housing

Remittances reached USD 63 billion in 2024, amplifying household budgets just as manufacturing reshoring expands salaried employment. Mid-tier homes retain the broadest buyer pool, yet luxury stock is rising fastest due to peso depreciation, attracting foreign investors. Vertical gated estates with integrated amenities meet the security and lifestyle expectations of a growing professional cohort, particularly along the Mexico City-Monterrey-Guadalajara corridor.

Urban Infrastructure Development Creating New Residential Growth Corridors

Projects such as the Mayan Train and Interoceanic Corridor are opening underserved regions, while DistritoTec in Monterrey showcases how public-private coordination can revive urban cores. Smart-city rollouts in Mexico City, Guadalajara, and Monterrey are layering IoT traffic control and air-quality systems to lift livability. Faster municipal permitting—targeted to drop from 2.6 years to 127 requirements—should further stimulate pipeline velocity.

Restraints Impact Analysis*

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction costs driven by inflation, import dependence, and supply chain disruptions | -1.1% | National, particularly border regions | Short term (≤ 2 years) |

| Lengthy permitting processes and fragmented regulatory frameworks delaying project execution | -0.9% | State and municipal levels nationwide | Medium term (2-4 years) |

| Macroeconomic volatility and peso fluctuations impacting affordability and foreign investment confidence | -0.7% | National, with higher impact in tourist and border regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Construction Costs Driven by Inflation, Import Dependence, and Supply-Chain Disruptions

Potential 25% U.S. steel and cement tariffs threaten input prices for builders reliant on cross-border trade. Although producers such as Cemex posted 6% net-sales growth and 14% EBITDA gains in 2024, project budgets remain sensitive to foreign-exchange pass-through and shipping delays. The 2021 Subcontracting Reform also raises compliance outlays but enhances labor protections, balancing cost burdens with social benefits.

Lengthy Permitting Processes and Fragmented Regulatory Frameworks Delaying Project Execution

Developers must navigate disparate municipal codes covering zoning, environment, and utilities, often stretching timelines past financial feasibility. Jalisco’s 2023 agent-licensing law signals moves toward professional standardization, yet constitutional debates slow adoption. The 2018 General Law of Better Regulation and the SINAGER platform offer process templates, but subnational compliance still represents 3.4% of GDP in regulatory costs[3]Roberto Salcedo Aquino, “Costo Regulatorio y Tramitología en la Construcción 2024,” Secretaría de la Función Pública, gob.mx.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rental Momentum Builds Within Ownership-Dominant Culture

Sales retained a 73.55% share of the Mexico residential real estate market in 2025, reflecting entrenched ownership aspirations and subsidy-backed credit lines. The rental arm, however, is primed for a 5.93% CAGR through 2031 as social leasing spreads and digital platforms streamline listings. INFONAVIT’s rent-to-own pilot links monthly rent to eventual equity, merging flexibility with long-term tenure goals. Expanded rental stock improves mobility for young professionals flocking to nearshoring hubs, enhancing labor-market efficiency.

Secondary resale homes further support liquidity, with many households favoring ready-to-occupy units in well-served districts. Nonetheless, the government’s construction push will bring fresh inventory to market, gradually balancing the mix. PropTech-enabled screening and e-signatures are also shrinking vacancy times for landlords, underscoring the rental segment’s structural tailwinds.

By Property Type: Vertical Stock Dominates Yet Ground-Oriented Homes Accelerate

Apartments and condominiums secured 62.85% Mexico residential real estate market share in 2025 as density regulations and land scarcities channeled capital into high-rise formats. Tower complexes bundle green areas, retail, and coworking nodes, meeting modern lifestyle standards. Villas and landed houses, though smaller today, are slated for a 6.02% CAGR owing to expanding middle-class budgets and post-pandemic outdoor-space preferences.

Hybrid gated communities mixing towers and townhouses illustrate how developers are optimizing footprints while catering to diverse household structures. The government’s emphasis on well-located sites with transit links continues to favor vertical infill, yet suburban parcels in Querétaro and Mérida are gaining traction for low-rise build-to-sell projects.

By Price Band: Luxury Upswing Amid Mid-Market Scale Leadership

Mid-range units captured 46.85% of the Mexico residential real estate market size in 2025 by serving households earning multiple minimum wages. Remittance-boosted liquidity and INFONAVIT credit ceilings sustain this core. Conversely, the luxury tier is on track for a 6.28% CAGR, buoyed by expatriate inflows and dollar-denominated buyers capitalizing on currency discounts. Coastal resorts and Mexico City’s Polanco district headline high-end absorption, with concierge amenities and ESG-certified designs differentiating projects.

Affordable stock remains undersupplied after sub-MXN 550,000 homes slid from 51% to 15% of output between 2016 and 2024. Vinte-Javer’s merger explicitly targets this gap, planning units from MXN 500,000 (USD 27,000) upward while leveraging IFC backing to keep margins viable.

By Mode of Sale: Secondary Listings Thrive as New-Build Pipelines Tighten

Resale transactions accounted for 54.05% of the Mexico residential real estate market share in 2025 and will likely post a 6.17% CAGR given faster closings and bank-valuation familiarity. Cash-heavy remittance purchases favor existing properties in legacy neighborhoods, bypassing construction-completion risk. Primary sales face rising material costs and permitting drag, yet public-sector land banks and direct-build schemes are expected to ease bottlenecks over the medium term.

Developers adopting phased pre-sale models and escrow safeguards are rebuilding buyer trust, especially in metros where stalled projects once dented confidence. Government streamlining of approval workflows should eventually shorten launch-to-delivery cycles, invigorating primary-market competitiveness.

Geography Analysis

Mexico City led with 30.35% of the Mexico residential real estate market size in 2025, leveraging its 30 million-resident metropolitan economy and extensive transit network. Highland prices spur vertical redevelopment, while municipal incentives for social housing aim to anchor affordability within the urban core. Near-zero vacancy in prime corridors is encouraging adaptive reuse of aging office stock into loft-style apartments, adding depth to supply choices.

Nuevo León, centered on Monterrey, benefits from nearshoring inflows and the DistritoTec revitalization, which cut local vacancy to single digits and lifted property values. Industrial payroll expansion fuels both entry-level and premium demand, with cross-border executives gravitating toward gated vertical enclaves that parallel U.S. lifestyle formats.

Querétaro is the fastest-growing node at a projected 6.74% CAGR through 2031. Its strategic location on the Mexico City-Monterrey axis, plus aerospace and automotive clusters, magnetizes skilled labor. Affordable land reserves and agile permitting processes are luring national developers, with mixed-use communities sprouting along new bypass highways.

Guadalajara’s tech ecosystem supports steady absorption of mid-to-high-end condos, aided by smart-city upgrades under the Ciudad Creativa Digital program. Enhanced fiber networks and co-living inventory cater to digital-nomad segments, expanding the city’s residential appeal.

Government mandates ensure CONAVI funding reaches 1,345 municipalities, dispersing development toward secondary cities and rural towns. Southeastern states tied to the Mayan Train and Interoceanic Corridor now exhibit speculative land trades as investors anticipate tourism and logistics spillovers.

Regulatory Landscape

Mexico's housing and residential development framework is anchored in the Ley de Vivienda. Under it, the Federal Executive sets national housing policy through SEDATU, with CONAVI executing key federal housing programs and INSUS leading land regularization. On the consumer-facing side, NOM-247-SE-2021 sets mandatory requirements for how residential real estate is marketed and advertised by developers and providers, which raises compliance expectations around disclosures and sales practices.

In 2026, the policy direction was formalized through publication of the Programa Nacional de Vivienda (PNV) 2026-2030, aligned with national territorial planning instruments, including the 2026-2030 planning framework for land use and urban development. In parallel, PROY-NOM-007-SEDATU-2024 advanced criteria around housing habitability certification, linking access to government-backed credits and subsidies. This reinforces the need for developers to meet defined habitability and sustainability thresholds to participate in public support channels.

Value Chain Analysis

Mexico's residential real estate value chain spans land origination and regularization (including INSUS-linked processes), planning and permitting at state and municipal levels, development and construction (developers, general contractors, and specialized trades), and materials supply (cement, steel, blocks, wiring, and finishing products). It also covers sales and brokerage (agents and digital platforms), financing (INFONAVIT, FOVISSSTE, banks, and developer credit), and post-sale services (property management, maintenance, and facility operations). Self-production remains a defining feature, with autoproduccion representing 55.6% of total housing sector economic activity and residential construction activity tied to building, expansion, and improvement contributing 68% to housing GDP in 2024, which shapes demand for technical assistance, materials retail, and incremental-build solutions alongside formal developer-delivered stock.

On the supply side, the residential building construction industry counted 4,857 registered economic units as of 2025, concentrated in states such as Jalisco, Yucatan, and Nuevo Leon. Input-cost dynamics stay a bottleneck: construction material inflation was 3.93% year-on-year as of December 2025, with outsized increases in specific items such as wires (17.4%), nitrogen/oxygen (14.6%), and concrete blocks/bricks (7.6%). CMIC also reported housing construction as the highest material-inflation segment within construction (4.52% annual as of December 2025). Public programs are shaping upstream demand as well, since CONAVI's Vivienda para el Bienestar program moved into 2026 execution after late-2025 allocation lotteries. The 2026 build target of 400,000 homes concentrates purchasing needs for core materials and contractor capacity, influencing procurement cycles and subcontractor availability.

Competitive Landscape

Mexico's residential real estate industry consolidation accelerated when COFECE approved the May 2024 Vinte-Javer merger. The combined group can deliver 16,000 units annually, anchoring scale advantages in procurement and land banking. IFC financial participation provides patient capital, facilitating deeper penetration into sub-USD 30,000 price points.

INFONAVIT’s new construction arm introduces quasi-public competition, particularly in the social-interest bracket where private margins are thin. Its inaugural 20,000-home batch scheduled for April 2025 could recalibrate pricing benchmarks and spur efficiency drives among private peers.

Grupo ARA resumed projects across Puebla, Veracruz, and Nayarit after hurricane disruptions, projecting an 80% revenue rebound in Acapulco under Line III loan packages. Smaller regional builders are aligning with PropTech platforms for sales outreach, yet rising compliance costs from the Subcontracting Reform may push further mergers or exits, lifting market concentration progressively.

Mexico Residential Real Estate Industry Leaders

Ruba Residencial

ARA Consortium

Grupo Jomer

Grupo GP

Grupo GP

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale federal housing execution creates addressable whitespace across affordable delivery, rental, and self-production support services. The Vivienda para el Bienestar agenda carries a stated 2026 construction target of 400,000 homes, and the PNV 2026-2030 reframes housing policy to include rental, self-construction, and land access as core pillars alongside ownership. That broadens the product and service mix that can be financed or supported through public channels.

Digitization is a second opportunity pocket as market participants aim for faster sales cycles and better risk controls under fragmented local processes. PropTech expansion is visible in moves such as Habi's March 2026 acquisition of broker-technology firm Pulppo to deepen digital brokerage capabilities in Mexico, complementing wider adoption of digital tools across real estate operations. As public programs scale and compliance expectations tighten, including NOM-247-SE-2021 for marketing, platforms and service providers that streamline documentation, verification, customer qualification, and post-sale management can support both primary developers and the growing resale and rental ecosystems. Platforms that can also align with emerging habitability certification criteria may be better placed to serve projects tied to INFONAVIT and CONAVI-linked affordability channels.

Recent Industry Developments

- May 2026: Ruba expanded its residential operating footprint to 17 cities across 13 Mexican states, highlighting ongoing geographic diversification by large-scale homebuilders. The move includes project activity in Monterrey, Nuevo Leon (such as Semillero Mediterraneo) developed in partnership with Fraterna, aligning supply with nearshoring-driven employment hubs and demand for organized housing formats.

- July 2025: INFONAVIT announced an increase in its housing construction target for the presidential term to 1.2 million homes, up from an earlier 500,000-home goal. The larger public pipeline reinforces long-dated demand for developers, contractors, and materials suppliers that can deliver at scale and meet affordability-linked program requirements.

- May 2024: COFECE approved the Vinte-Javer merger, accelerating consolidation in Mexico's residential development landscape. The combined platform strengthened scale advantages in land banking and procurement, increasing competitive pressure on smaller builders in the affordable and mid-market segments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of residential property activity in Mexico, including homes that are bought, sold, or rented, across both apartments and landed houses.

Scope exclusions: It does not include commercial real estate, industrial properties, or public infrastructure projects.

Segmentation Overview

- By Business Model

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

We start by building the Mexico housing demand and supply picture from public datasets that are consistent year to year, which helps avoid one-off headline bias. Core references include sources such as INEGI housing, population, and construction statistics, Banco de Mexico macro and interest-rate series, CONAVI housing program indicators, and INFONAVIT origination and credit performance data.

To round out the model inputs, we also use sources such as OECD and World Bank demographic and income series, local property registry and municipal permitting disclosures where available, and official inflation and exchange-rate series for currency normalization. General secondary sources like listed-company filings, investor presentations, association websites, and reputed press coverage are used to sanity-check pricing direction, launches, and absorption. A paid subscription for company financials and news, and a patent database for construction and housing-related materials signals, are used selectively to support validation, and this list is not exhaustive because many other sources were consulted for collection, cross-checking, and clarification.

Primary Interviews and Surveys

To make sure the model reflects what is happening on the ground, we validate assumptions through expert interviews and structured surveys with developers, brokers, lenders, valuers, and local market advisors. Coverage is spread across key demand centers and supply corridors in Mexico so pricing moves, absorption, and buyer behavior can be cross-checked, and then the findings are used to tighten variables where public data is slower to update.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 56% | Functional/Unit leaders: 32% | |

| Smaller Players: 16% | Managers: 56% |

Market-Sizing & Forecasting

Sizing is built mainly through a top-down model where housing activity and value are reconstructed from Mexico-level indicators, then converted into market value using pricing and mix assumptions. In practice, we track signals such as household formation and migration into major metros, mortgage origination and interest rate direction, residential building permits and starts, price per square meter movements, and the sales-versus-rental mix, since these drivers explain most of the year-to-year change.

After the initial total is produced, it is corroborated with selective bottom-up approximations, such as sampled unit volumes by major state markets multiplied by observed price bands, and reasonableness checks using publicly visible developer project launches. Where bottom-up visibility is thin for informal or fragmented brokers, gaps are handled through penetration assumptions that are first anchored in official housing and credit series and then adjusted using interview feedback.

For forecasting, scenario analysis is used around mortgage affordability, construction cost pressure, and employment-driven demand (including nearshoring-linked job creation), and then a simple regression-style sensitivity is applied to keep growth tied to the key variables. Final outputs are produced in USD using consistent currency timing so the trend is not distorted by short-term FX swings.

Data Validation & Update Cycle

Outputs are checked in more than one step so obvious mismatches do not pass through, and we look for breaks versus independent signals like housing finance growth, construction activity, and reported price trends. When a variance looks large, assumptions are revisited, outliers are tested, and interviewees may be re-contacted to confirm whether a shift is real or just a timing difference in available data.

Before sign-off, another analyst reviews the logic, inputs, and calculations so the estimate is repeatable, and major assumptions are traceable to a source or an expert check. Reports are refreshed annually, with interim updates triggered by material events such as policy changes in housing finance, rate shocks, or major macro disruptions, and a final pre-delivery pass is completed to keep figures current.

Mordor Intelligence's Mexico Residential Real Estate Market Size Versus Other Published Estimates

Published market sizes for Mexico residential real estate can look far apart, mainly because authors do not always count the same revenue pool or use the same timing for prices and currency conversion. Differences also show up when one estimate leans heavily on macro growth and another leans on housing transaction activity, which can move in different directions in the same year.

Commercial real estate, industrial properties, and land-only transactions sit outside Mordor Intelligence's scope, which removes adjacent value pools that some publications blend into a broader "real estate" total. The gaps in the table also reflect how some sources apply a single national price growth rate to all regions, or use a long forecast window without re-checking mortgage availability and absorption conditions in key states.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 46.44 B (2025) | |

| Trade Journal A | USD 13.93 B (2024) | Uses a smaller implied value pool that appears closer to selected corridors and buyer cohorts rather than a full national sales and rental view, and the base year and FX timing differ. |

| Industry Publisher B | USD 168.90 B (2025) | Represents a broader real estate total that can include non-residential categories and land-led value, so the reported figure expands beyond strictly residential transactions and rentals. |

Taken together, the spread is mostly explained by scope and by how price levels are applied across regions and property types. By keeping inputs tied to observable housing activity, financing signals, and realistic price progression, the resulting market size stays traceable to clear drivers and can be repeated when new public data arrives.

Key Questions Answered in the Report

What is the size of Mexico Residential Real Estate in 2026 and 2031?

The Mexico residential real estate market size reached USD 49.03 billion in 2026 and is forecast to touch USD 64.28 billion by 2031.

What annual growth is expected through 2031?

The sector is projected to post a 5.57% CAGR, sustained by housing-finance reforms and steady household formation.

Which Mexican state is expanding fastest in home sales?

Querétaro is poised for a 6.74% CAGR through 2031, driven by aerospace and automotive industry growth.

What impact will INFONAVIT’s new builder arm have?

Infonavit Constructora plans 500,000 social-interest homes, adding affordable stock and heightening competition for private developers.

How are construction-cost pressures being managed?

Domestic suppliers like Cemex raised 2024 net sales by 6% despite tariff risks, while builders streamline designs and seek volume discounts.

Page last updated on: