Banking And Financial Services ERP Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

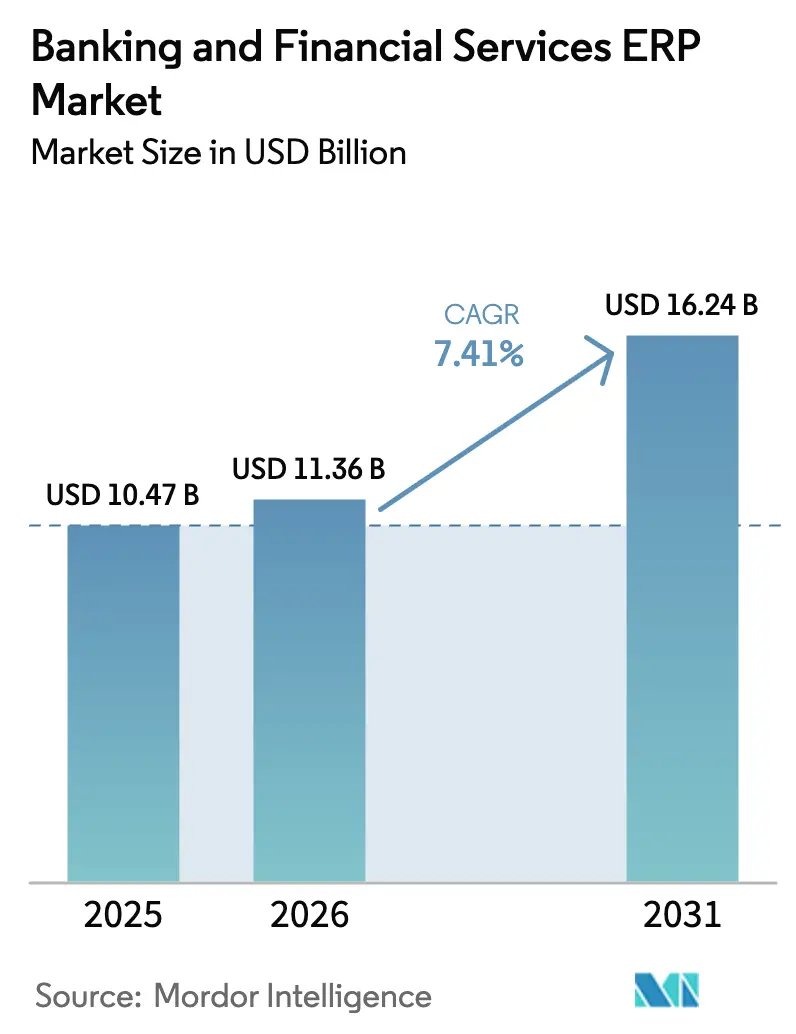

| Market Size (2026) | USD 11.36 Billion |

| Market Size (2031) | USD 16.24 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

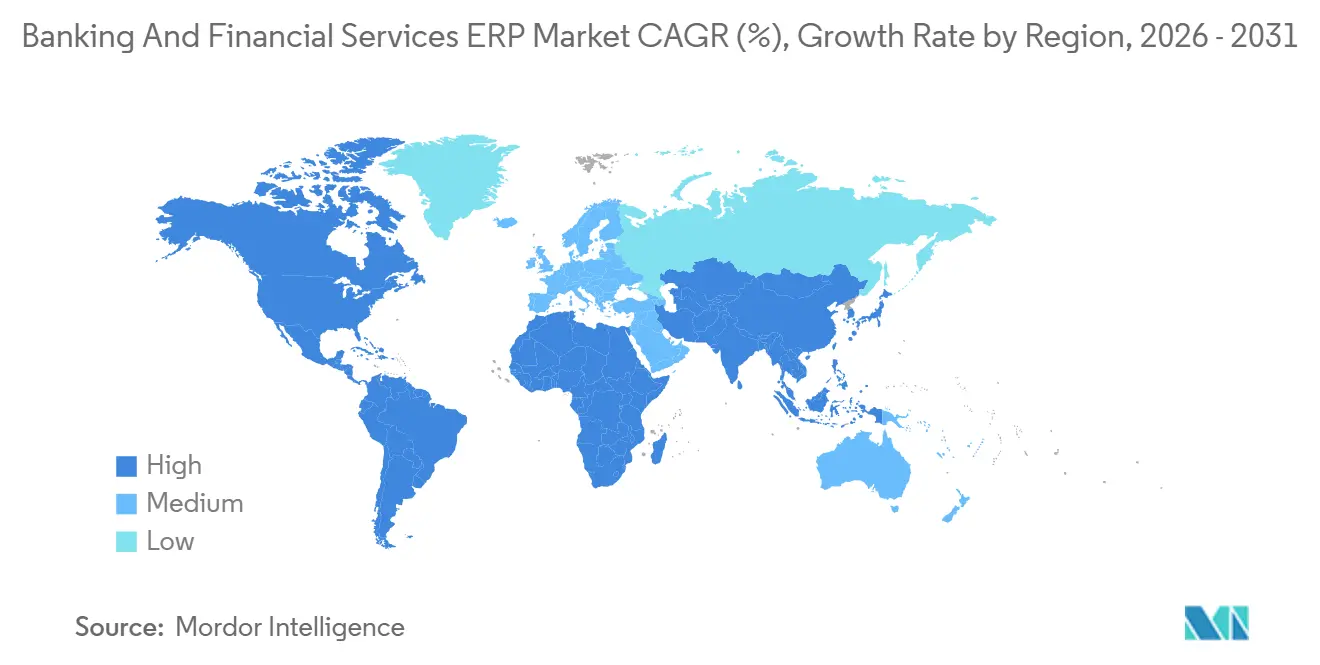

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Banking And Financial Services ERP Market Analysis by Mordor Intelligence

The Banking and Financial Services Enterprise Resource Planning Market size was valued at USD 10.47 billion in 2025 and is estimated to grow from USD 11.36 billion in 2026 to reach USD 16.24 billion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031). Mainstream banks are replacing monolithic, on-premise cores with cloud-native, API-first suites that embed artificial intelligence for predictive liquidity management, real-time regulatory reporting, and automated compliance controls. The confluence of Digital Operational Resilience Act timelines in the European Union, Basel Committee guidance on technology outsourcing, and the global shift to ISO 20022 payment messaging continues to steer investments toward modular platforms that can be updated without prolonged downtime. Intensifying cyber-resiliency mandates, the availability of sovereign-cloud regions, and growing demand for consumption-based pricing are reshaping buyer expectations, while the promise of lower total cost of ownership is drawing mid-tier banks and credit unions into the banking and financial services ERP market. Competitive activity centers on embedded banking APIs, fraud-detection add-ons, and climate-risk analytics, signaling that specialized functionality has become a primary differentiator rather than generic financials alone.

Key Report Takeaways

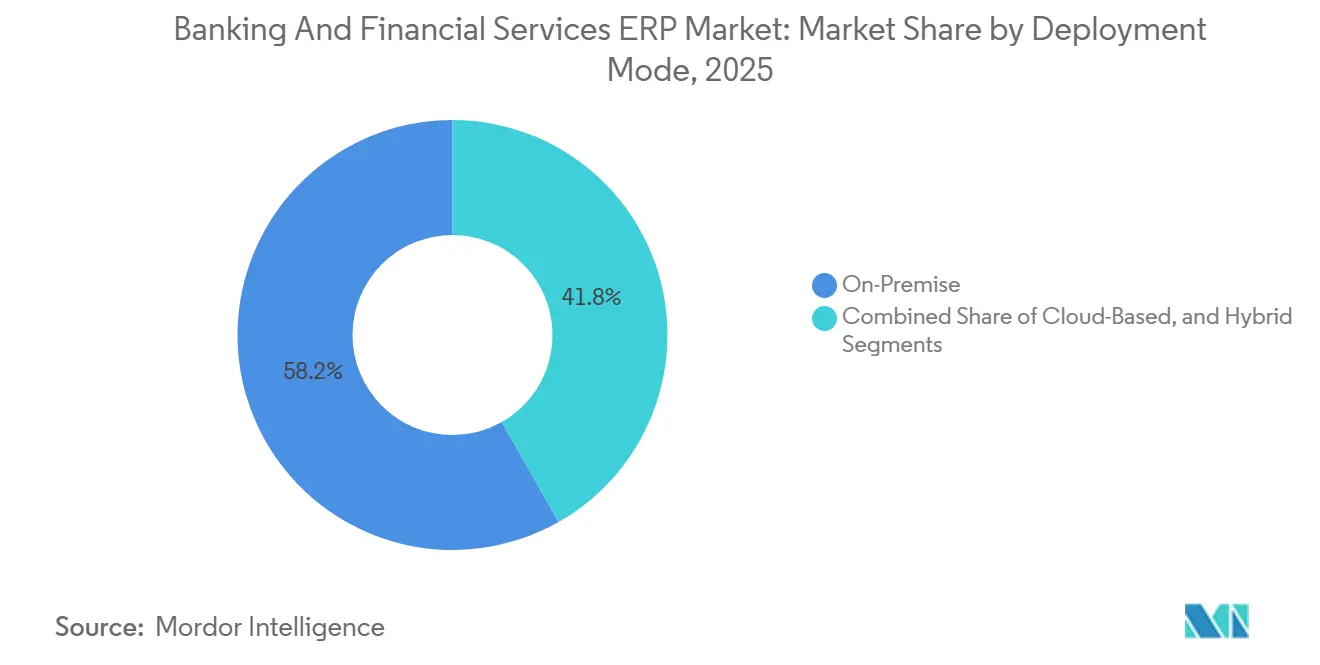

- By deployment mode, on-premises installations accounted for 58.21% of 2025 revenue, while cloud deployments are advancing at a 7.83% CAGR through 2031.

- By application, payment management led with a 42.57% revenue share in the banking and financial services enterprise resource planning market in 2025, whereas risk and compliance management is projected to expand at an 8.23% CAGR through 2031.

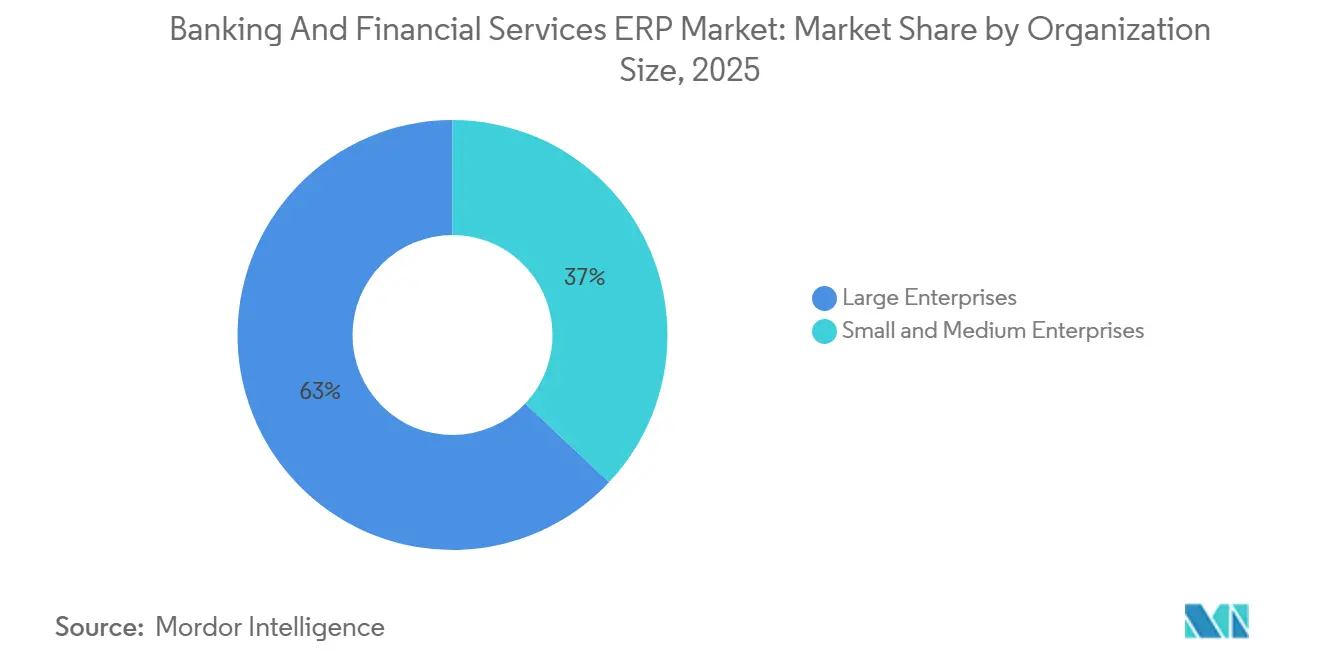

- By organization size, large enterprises held 62.98% of 2025 revenue, yet small and medium enterprises are set to record a 7.63% CAGR during 2026-2031.

- By component, software accounted for 68.89% of the 2025 value, but services are pacing ahead at a 7.98% CAGR across the banking and financial services ERP market.

- By geography, North America captured 37.37% market share in 2025, while Asia-Pacific is positioned for the fastest 8.48% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Banking And Financial Services ERP Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Real-Time Regulatory Reporting and Compliance Automation | +2.1% | Global, with peak intensity in European Union and North America | Medium term (2-4 years) |

| Integration of AI-Driven Predictive Analytics within ERP Suites | +1.8% | Global, early adoption in North America and Asia-Pacific core markets | Medium term (2-4 years) |

| Accelerating Cloud-Native Adoption in Regulated Financial Institutions | +1.5% | Global, led by European Union, United Kingdom, and Singapore | Long term (≥ 4 years) |

| Cyber-Resiliency Mandates Driving ERP Modernization | +1.2% | European Union, North America, with spillover to Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Growing Preference for Modular and Composable ERP Architectures | +0.9% | Global, concentrated in mid-market and challenger banks | Long term (≥ 4 years) |

| Rise of Embedded Banking APIs Extending ERP Value Chains | +0.7% | North America, European Union, and Asia-Pacific fintech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Real-Time Regulatory Reporting and Compliance Automation

Supervisors now expect granular, event-driven filings rather than monthly or quarterly batches, pushing institutions to embed real-time data pipelines directly into core finance processes. DORA incident-notification windows and Basel capital calculations for cryptoasset exposures require daily mark-to-market valuations that legacy batch architectures cannot support. Modern ERP suites offering ready-made XBRL taxonomy validation and central-bank connectors shorten submission cycles, reduce manual reconciliation, and lower non-compliance risk. Tier-1 banks in Germany and the United States are already running parallel production pilots that deliver live exposure data to regulators within four-hour windows, illustrating how regulatory pressure is steering budgets into the banking and financial services enterprise resource planning market. Early adopters report 30%-plus reductions in regulatory-reporting effort, freeing capacity for strategic analytics.

Integration of AI-Driven Predictive Analytics Within ERP Suites

Embedding machine-learning engines into day-to-day workflows lets treasury teams model forward liquidity buffers, fraud-ops units detect anomalous behavior, and credit officers surface early warning signs of covenant breaches. Recent product releases from the top three vendors provide natural-language interfaces that allow non-technical staff to query cash positions and scenario outcomes with conversational prompts. Pilot programs show 40%-60% declines in manual reconciliation tasks and materially sharper accuracy in cash-flow forecasts, yet the compute intensity of large-language-model inference introduces incremental subscription layers that smaller institutions must carefully budget. As predictive capabilities mature, institutions see tangible proof that AI functionality is no longer a nice-to-have but a core selection criterion, deepening penetration of the banking and financial services enterprise resource planning market.

Accelerating Cloud-Native Adoption in Regulated Financial Institutions

Clarified outsourcing rules from the European Banking Authority, the Monetary Authority of Singapore, and other regulators have reduced uncertainty about the use of public cloud for critical workloads.[1]Monetary Authority of Singapore, “Technology Risk Management Guidelines,” mas.gov.sg Hybrid architectures, keeping sensitive personal data on premise while bursting analytics to sovereign clouds, are becoming the default for Tier-1 migrations. One European mega-bank migrated 14 million accounts in 2025 using such a model, cutting release cycles from quarterly to fortnightly. Cloud-native approaches unlock elastic scaling, fault isolation, and micro-upgrade paths, benefits that directly translate into shorter time-to-market for new products. As more central banks publish cloud guidance, institutional resistance is waning, giving the banking and financial services enterprise resource planning market a structural tailwind.

Cyber-Resiliency Mandates Driving ERP Modernization

Post-incident reporting deadlines tighten every year, and annual threat-led penetration tests are now mandatory under DORA Article 17. Legacy ERP stacks, often running unsupported operating systems, struggle to meet multi-factor authentication, immutable logs, and auto-failover requirements. Modern suites ship with built-in governance dashboards that surface real-time control effectiveness, accelerating board-level oversight. Vendors increasingly bundle cyber-resilient hosting and managed detection services, shifting accountability from bank IT teams to solution providers. As penalties for outages increase, institutions migrate at speed, feeding demand into the market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Core System Complexity and High Integration Costs | -1.4% | Global, acute in North America and European Union institutions with multi-decade mainframe estates | Long term (≥ 4 years) |

| Data-Residency and Sovereignty Barriers to Public Cloud Migration | -1.1% | China, Russia, European Union, India, with emerging constraints in Middle East | Medium term (2-4 years) |

| Shortage of ERP-Savvy Treasury and Compliance Talent | -0.8% | Global, most severe in North America and European Union | Medium term (2-4 years) |

| Escalating Subscription OPEX Due to AI Add-On Pricing | -0.6% | Global, disproportionately affecting small and medium enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Core System Complexity and High Integration Costs

Many universal banks still run COBOL-based cores written in the 1980s, interwoven with proprietary middleware and undocumented business logic. Large incumbents spend up to 75% of annual technology budgets on maintenance, leaving limited capital for modern ERP rollouts. Full migrations can last five years and cost USD 100 million-plus, and high-profile failures such as TSB’s 2018 outage remain cautionary tales, with approximately USD 440 million in remediation costs and the approximately USD 65 million in fines imposed by the Financial Conduct Authority continuing to shape risk committees' approach to ERP transformation.[2]Financial Conduct Authority, “TSB Bank Operational Resilience Failures,” fca.org.uk Boards often favor incremental wrap-and-renew approaches, slowing wholesale adoption. This complexity keeps the brakes on the market even as modernization imperatives mount. Despite these challenges, demand for scalable, efficient ERP solutions continues to grow as institutions strive to remain competitive in a rapidly evolving market.

Data-Residency and Sovereignty Barriers to Public Cloud Migration

Jurisdictions including China, Russia, and India enforce local storage mandates, while the European Union’s GDPR adds hurdles to data transfers. Vendors must build regional data centers, certify local staff, and segregate operational access, inflating infrastructure costs and elongating sales cycles. Banks that operate across multiple sovereignty regimes face architectural sprawl and duplicative investments, limiting the pace at which cloud-only ERP models can scale. Although sovereign-cloud variants alleviate part of the burden, fragmentation remains a headwind to the market. This ongoing fragmentation underscores the need for tailored solutions that address both compliance and scalability challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Models Balance Control and Flexibility

On-premises systems accounted for 58.21% of 2025 revenue, underscoring that regulatory audits and latency-sensitive ledgers still anchor workloads in bank data centers. The share of cloud implementations is rising swiftly, expanding at a 7.83% CAGR, as sovereign cloud regions assuage data localization fears. Hybrid models partition sensitive ledgers on-premises and analytics in the cloud, creating an architecture that satisfies supervisors yet delivers the agility finance teams need. Vendors now ship workload classifiers that automatically route data based on regulatory tags, trimming integration friction. Over the forecast window, hybrid footprints are expected to anchor more than half of incremental spending, embedding the market in a dual-state paradigm.

Challenger banks embrace pure SaaS because they lack legacy drag and prefer usage-based subscription economics. Conversely, Tier-1 treasuries keep settlement engines co-located with market-infrastructure gateways where microsecond latency is critical. As regulators become more comfortable with encryption at rest and multi-region replication guarantees, a gradual pivot toward cloud is inevitable, but the coexistence of all three deployment modes will define the competitive playbook through 2031 across industry. This shift will likely encourage innovation and adaptability in financial technology solutions.

By Application: Compliance Engines Outpace Payment Hubs

Payment management retained the largest 42.57% share of 2025 spend owing to global ISO 20022 migrations, 24-hour real-time payment rails, and mounting cross-border reconciliation complexity. Yet risk and compliance modules are forecast to post the fastest CAGR of 8.23% as institutions automate sanctions screening, beneficial ownership checks, and climate risk disclosures. Generative AI is now parsing unstructured contracts, cutting manual review by half, and supervised-learning models are slashing false-positive alerts in transaction-monitoring queues, proving a strong return on incremental licenses. Those gains propel the market size allocated to compliance from a support function cost to a strategic budget line.

Customer relationship management and staff operations suites are being bundled into broader ERP stacks, offering banks a unified data model for headcount planning, conduct-risk monitoring, and personalized product offers. This integration enables banks to streamline operations and improve decision-making processes. As integration tightens, payment hubs and compliance engines will increasingly share event streams, lowering reconciliation costs while boosting real-time insight for treasury teams across the market. Additionally, this shift supports enhanced scalability and adaptability, ensuring banks can respond effectively to evolving regulatory and market demands.

By Organization Size: Consumption-Based Cloud Lures Mid-Tier Banks

Large enterprises maintained 62.98% of 2025 turnover, reflecting their capital heft and multi-jurisdictional operations that demand multi-entity consolidation and sophisticated treasury analytics. These clients prize configurability, regional data-center choices, and certified partner ecosystems, features best delivered by legacy heavyweights. Meanwhile, SMEs are growing at a 7.63% CAGR as cloud-native vendors introduce per-account or per-transaction pricing that aligns cost with revenue trajectories. Removing upfront license fees lowers the barrier to entry, unlocking latent demand in community banks and digital-only upstarts and nudging them into the market.

Banking-as-a-service operators further broaden the addressable SME pool by leasing out charter access, substituting regulatory capital with technology spend. This approach enables smaller firms to focus on their core operations while leveraging advanced financial services. Tight tech labor markets mean smaller firms prefer turnkey SaaS stacks with embedded regulatory content. Over time, those patterns could erode Tier-1 banks' scale advantage and trigger a rebalancing of ERP market share in banking and financial services between large and mid-sized institutions.

By Component: Services Revenue Mirrors Migration Complexity

Software licenses and subscriptions accounted for 68.89% of 2025 revenue, yet professional and managed services are tracking a 7.98% CAGR, as migration from COBOL cores to microservices is rarely a lift-and-shift exercise. Mapping legacy business logic to modern workflows demands skilled architects fluent in payment rails, risk models, and multiple accounting frameworks. As a result, consulting hours regularly exceed the initial software invoice amounts, underscoring that transformation, not licensing, fuels value creation in the market.

Managed cloud services and DevSecOps outsourcing attract banks that want to offload day-to-day patching and resilience drills. Advisory specialists are also carving out high-margin niches in DORA, climate risk, and Basel III output floor configuration. Oracle reported 28% year-over-year growth in managed cloud services revenue in its fiscal 2025 third quarter, with financial services as the fastest-growing vertical. Effective training and change management are essential for maximizing ERP benefits, as low user adoption undermines ROI. Insufficient training leads to extended parallel runs of legacy and new systems, increasing costs and operational risks.[3]Oracle Corporation, “Fiscal 2025 Annual Report,” investor.oracle.com Vendors that couple subscription revenue with deep domain consulting are positioned to capture a larger slice of the industry over the next five years.

Geography Analysis

North America accounted for 37.37% of the 2025 value, driven by Federal Reserve stress-test cycles and OCC oversight that require quarterly capital-ratio modeling and continuous data availability.[4]Federal Reserve Board, “Comprehensive Capital Analysis and Review,” federalreserve.gov The United States and Canada both tightened cyber guidelines in 2024, compelling platform upgrades that feed directly into the market. Mexico’s open-banking rollout likewise spurred demand for API-ready systems among local incumbents, further enhancing the region's technological infrastructure.

Europe is undergoing a DORA-led modernization wave that requires immutable audit trails and four-hour incident disclosures, driving comprehensive ERP refreshes. Simultaneously, Prudential Regulation Authority rules on operational resilience have elevated board-level focus on integrated financial and risk data, thereby expanding the addressable budget. Additionally, the region's emphasis on sustainability reporting is pushing banks to adopt advanced analytics tools. Asia-Pacific, forecast at an 8.48% CAGR, benefits from digital-bank license issuances in Singapore and Hong Kong, India’s small-finance bank push, and China’s domestic-cloud mandates, each necessitating new ERP deployments.

South America is leveraging open-banking frameworks, most notably Brazil’s PIX success, to catalyze payment-hub investments, while Middle East and Africa banks adopt Islamic-finance-compliant modules amid accelerated digital banking adoption. These advancements are fostering innovation and competition within the banking sector. Furthermore, the growing focus on financial inclusion in these regions is driving the adoption of digital solutions. Collectively, these regional dynamics maintain a structurally positive outlook for the market.

Competitive Landscape

Concentration remains moderate, with the five largest suppliers, SAP, Oracle, Temenos, Microsoft, and Finastra, controlling roughly 45% of global revenue. Incumbents extend their portfolios with banking-specific clouds that integrate treasury, fraud, and regulatory modules, blunting the edge of niche providers in certain functional domains. Specialized core-banking players such as Temenos Transact and FIS Modern Banking Platform leverage multidecade domain expertise to win large replacement deals, thereby preserving their relevance in the market.

Cloud-native challengers, Mambu, Thought Machine, and nCino, court Tier-1 banks for greenfield digital sub-brands, leveraging event streaming, open APIs, and usage-aligned pricing. Their deployments validate pure-SaaS architectures for critical banking workloads and are pushing incumbents to re-platform at speed. Partnerships with regulatory-technology firms to automate IFRS disclosures and ISO 20022 reconciliation have become table stakes, and vendors lacking such alliances risk exclusion from shortlists.

Strategic acquisitions and funding rounds point to an arms race in AI, climate-risk analytics, and embedded finance. Large vendors are embedding large-language models to automate covenant extraction and board reporting, while payment specialists acquire cloud-native cores to widen addressable markets. Patent filings in distributed ledger settlement and tokenized collateral hint at future architectural shifts, but supervisory acceptance remains nascent, suggesting incremental rather than disruptive change for the market through 2031.

Banking And Financial Services ERP Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Fidelity National Information Services, Inc. (FIS)

Temenos AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP SE announced the general availability of its Generative AI Hub for S/4HANA Cloud, enabling banks to build custom LLM apps for contract analysis and regulatory impact assessment.

- January 2026: Temenos AG secured a USD 120 million hybrid-cloud migration deal covering eight subsidiaries across Southeast Asia, with completion due in Q4 2027.

- December 2025: Oracle Corporation launched Oracle Banking Cloud Services in its EU Sovereign Cloud, winning three European anchor banks for H2 2026 go-lives.

- November 2025: Microsoft Corporation integrated the Azure OpenAI Service into Dynamics 365 Finance for natural-language liquidity queries and automated variance analysis.

- October 2025: Fiserv, Inc. completed its USD 650 million acquisition of cloud-native core banking provider Finxact to accelerate SaaS conversion.

Global Banking And Financial Services ERP Market Report Scope

The market for enterprise resource planning (ERP) solutions that support the operational, financial, and regulatory requirements of banks and financial institutions. These ERP systems integrate critical functions such as payment processing, staff operations, customer relationship management, and risk and compliance management into a unified platform, enabling organizations to improve operational efficiency, regulatory compliance, and data-driven decision-making.

The Banking and Financial Services Enterprise Resource Planning Market Report is Segmented by Deployment Mode (On-Premise, Cloud-Based, and Hybrid), Application (Payment Management, Staff Operations Management, Customer Relationship Management, Risk and Compliance Management, and Other Applications), Organization Size (Large Enterprises, and Small and Medium Enterprises), Component (Software, and Services), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud-Based |

| Hybrid |

| Payment Management |

| Staff Operations Management |

| Customer Relationship Management |

| Risk and Compliance Management |

| Other Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| Software |

| Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | On-Premise | ||

| Cloud-Based | |||

| Hybrid | |||

| By Application | Payment Management | ||

| Staff Operations Management | |||

| Customer Relationship Management | |||

| Risk and Compliance Management | |||

| Other Applications | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Component | Software | ||

| Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the banking and financial services Enterprise Resource Planning market in 2031?

It is forecast to reach USD 16.24 billion by 2031.

Which deployment model is expanding the fastest?

Cloud-based ERP is growing at a 7.83% CAGR during 2026-2031.

Which application area is expected to post the highest growth?

Risk and compliance management is slated for an 8.23% CAGR through 2031.

Why are banks gravitating toward hybrid Enterprise Resource Planning architectures?

Hybrid models satisfy data-residency rules by keeping sensitive ledgers on premise while leveraging cloud elasticity for analytics.

Which region will see the quickest growth?

Asia-Pacific is projected to expand at an 8.48% CAGR, the highest among regions.

How concentrated is vendor competition?

The top five suppliers hold about 45% share, indicating moderate concentration and space for niche challengers.

Page last updated on: