Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

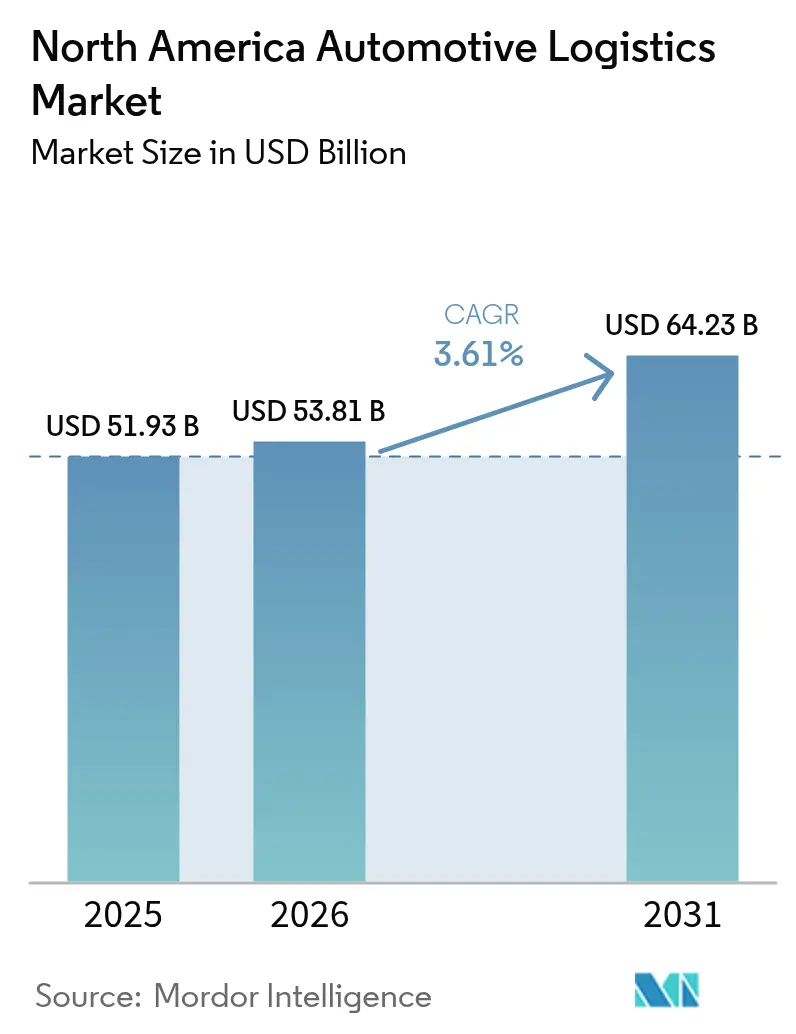

| Base Year Market Size (2025) | USD 51.93 Billion |

| Market Size (2026) | USD 53.81 Billion |

| Market Size (2031) | USD 64.23 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

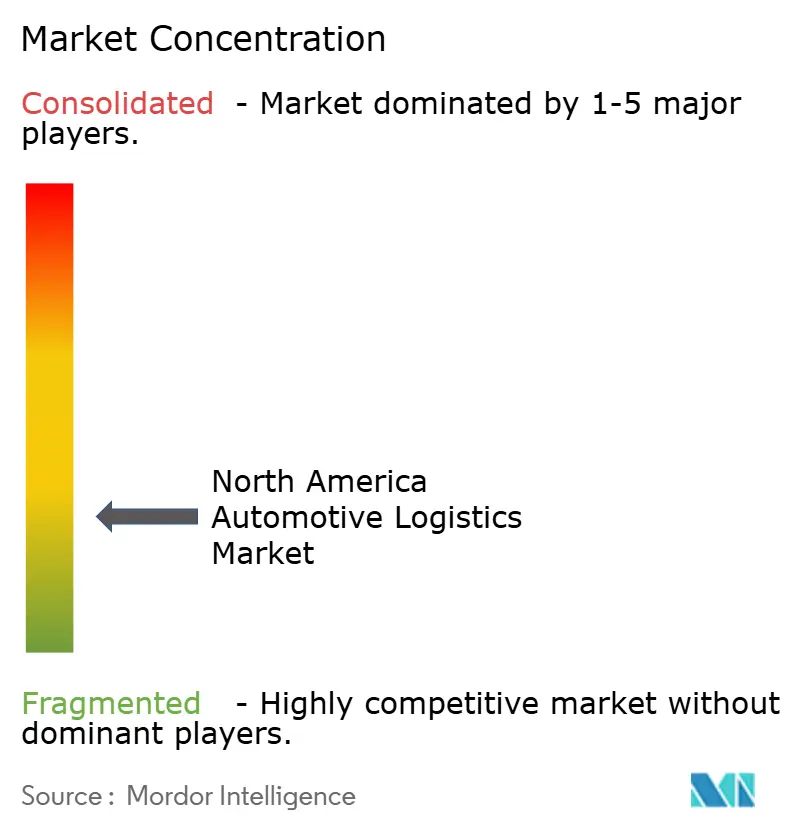

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Logistics Market Analysis by Mordor Intelligence

The North America Automotive Logistics Market size was valued at USD 51.93 billion in 2025 and estimated to grow from USD 53.81 billion in 2026 to reach USD 64.23 billion by 2031, at a CAGR of 3.61% during the forecast period (2026-2031).

Resilient demand comes from production near-shoring under USMCA, rising e-commerce parts flows, and the specialized, high-value movement of electric-vehicle (EV) batteries. The North America Automotive Logistics market is steadily shifting toward technology-enabled, value-added services that improve visibility, reduce empty-mile costs, and integrate kitting and sequencing at plants. Consolidation waves—exemplified by DSV’s USD 14.9 billion acquisition of DB Schenker in April 2025—are producing larger, multimodal service platforms able to manage end-to-end flows for original-equipment manufacturers (OEMs) and aftermarket clients. Despite a persistent driver shortage, cross-border investments and port expansions in Mexico support the North America Automotive Logistics market’s long-term trajectory.

Key Report Takeaways

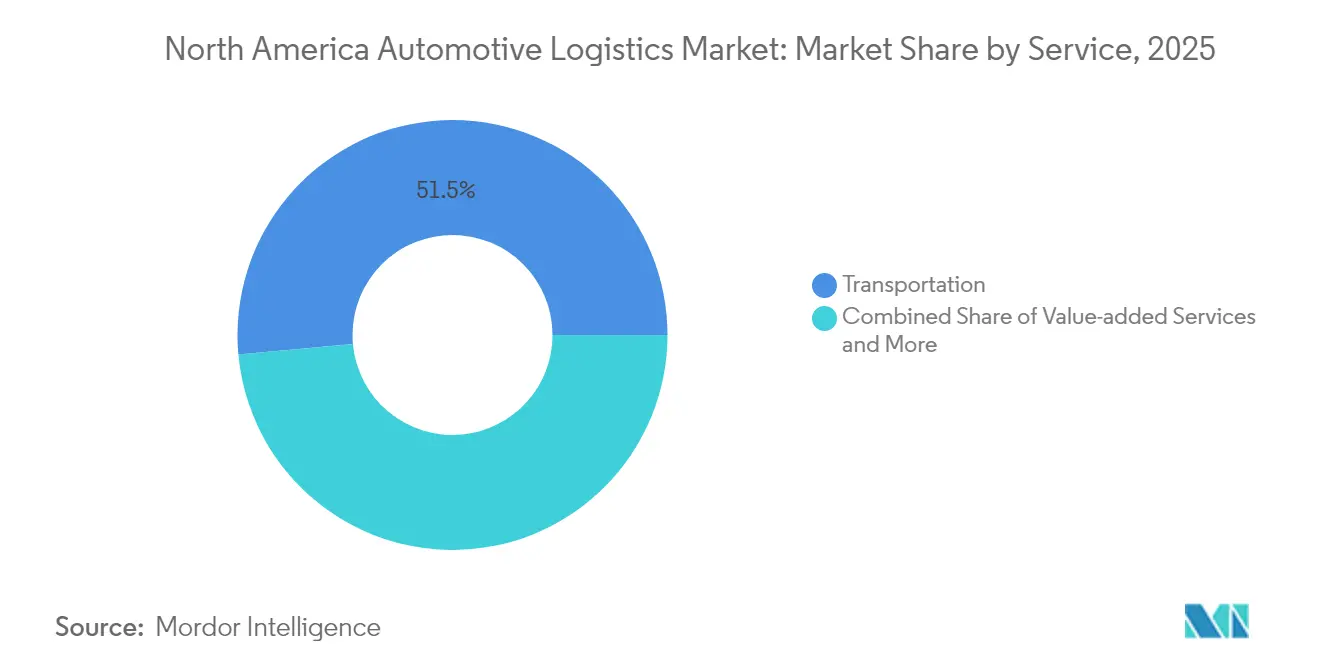

- By service, transportation held 51.45% of the North America Automotive Logistics market share in 2025, while value-added services are advancing at a 2.95% CAGR through 2031.

- By type, aftermarket logistics is expected to record a 3.65% CAGR through 2031, outpacing OEM flows, which retained a 56.20% share of the North America Automotive Logistics market size in 2025.

- By cargo type, finished vehicles captured 40.30% of the North America Automotive Logistics market size in 2025, whereas EV batteries and power electronics are projected to grow at a 3.32% CAGR to 2031.

- By country, the United States commanded 78.35% market share in 2025, but Mexico is forecast to post the fastest 3.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Automotive Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental regulations tightening | +0.6% | United States, Canada | Medium term (2-4 years) |

| Growth of e-commerce parts flows | +0.5% | North America-wide | Short term (≤ 2 years) |

| OEM near-shoring & USMCA production ramp-up | +0.4% | Mexico, United States | Long term (≥ 4 years) |

| Technology-enabled supply-chain visibility | +0.3% | North America-wide | Medium term (2-4 years) |

| Mexico’s Pacific port expansions | +0.3% | Mexico, Western United States | Long term (≥ 4 years) |

| AI-driven dynamic routing | +0.3% | North America-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Regulations Tightening (2025-2030)

The EPA’s Phase 3 greenhouse-gas standards, effective 2027, push logistics fleets toward low- and zero-emission trucks, altering asset procurement and routing strategies[1]U.S. Environmental Protection Agency, “Greenhouse Gas Emissions Standards for Heavy-Duty Vehicles,” epa.gov. States adopting California’s Advanced Clean Fleets Rule accelerate the transition by mandating zero-emission vehicle purchases. Operators face higher capital outlays for electric tractors yet expect lifetime fuel and maintenance savings to offset those costs. Warehouses install energy-management systems and secure ISO 14001 certification to meet shipper sustainability criteria. Logistics partners that can document quantifiable carbon-footprint reductions increasingly win long-term contracts from automakers focused on ESG metrics. Consequently, compliance investments become both a market entry ticket and a brand-building lever within the North America Automotive Logistics market.

Growth of E-commerce Parts Flows

Direct-to-consumer parts sales are fragmenting shipment profiles, shifting from pallet-level moves to parcel-size consignments that demand automated picking, labeling, and same-day fulfillment[2]Automotive Aftermarket Suppliers Association, “Industry Resources and Data,” aftermarketsuppliers.org. Cross-docks and micro-fulfillment centers near urban demand nodes shrink order-to-delivery cycles, while SKU proliferation necessitates real-time inventory visibility. Packaging engineers design tamper-proof, static-free solutions to protect sensors and electronics in parcel networks. Returns complexity rises as consumers expect hassle-free exchanges, prompting 3PLs to add refurbishment and restocking lines inside warehouses. The North America Automotive Logistics market thus pivots from purely cost-focused transportation to integrated, tech-driven services that manage e-commerce volatility.

OEM Near-shoring & USMCA Production Ramp-up

USMCA’s 75% regional-value content threshold is attracting engine, transmission, and EV-battery factories to Mexico, redirecting inbound flows from Asia to North American corridors[3]Office of the United States Trade Representative, “USMCA Chapter 4 Rules of Origin,” ustr.gov. Daily cross-border truckloads have climbed, compelling 3PLs to establish dedicated fast-lane programs with embedded customs-brokerage teams. Rail operators expand intermodal capacity linking Monterrey, Saltillo, and Puebla to Midwest U.S. auto hubs. Finished-vehicle terminals at Veracruz and Altamira add rail sidings and storage lots to handle build-ups during model launches. As regionalized sourcing deepens, synchronized production and logistics calendars cut pipeline inventory and boost on-time line-feeding for assembly plants spread across the North America Automotive Logistics market.

AI-driven Dynamic Routing Slashes Empty-Mile Costs

Machine-learning platforms synthesize traffic, weather, fuel, and driver-HOS variables to build real-time, optimal route plans that lift load factors and lower idle time. Predictive maintenance modules draw on telematics data to pre-schedule service stops, avoiding unplanned breakdowns. Integrated with warehouse management systems, these engines resequence dock appointments, allowing trucks to depart earlier and trim detention. Shippers gain dashboard visibility that flags excess carbon intensity per shipment, aligning with ESG scorecards. Carriers monetizing AI savings secure multi-year bids, reshaping competitive benchmarks in the North America Automotive Logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic cyclicality of auto output | -0.4% | North America-wide | Short term (≤ 2 years) |

| Driver shortage & wage inflation | -0.2% | United States, Canada | Medium term (2-4 years) |

| Battery-hazard regulations | -0.2% | North America-wide | Long term (≥ 4 years) |

| Port-side dwell-time fines | -0.1% | Coastal regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Driver Shortage & Wage Inflation

The commercial driver gap reached multi-tens-of-thousands of positions in 2025, straining capacity and lifting median pay[4]American Trucking Associations, “Economics and Industry Data,” trucking.org. Automotive freight suffers disproportionately because hazmat and car-haul endorsements narrow the qualified labor pool. Carriers raise sign-on bonuses and tuition reimbursement programs, yet still struggle to backfill retirements. Dedicated auto lanes face re-pricing every quarter as fleets chase the most profitable contracts. Autonomous-truck pilots show promise for hub-to-hub moves, but regulatory and public-acceptance barriers keep widescale deployment beyond the forecast horizon, preserving labor scarcity as a medium-term drag on the North America Automotive Logistics market.

Battery-hazard Regulations Constrain EV Logistics Capacity

Lithium-ion packs travel under Class 9 dangerous-goods codes that impose UN 3480-compliant packaging, real-time temperature logging, and placarded trailers. Only a subset of carriers invests in reinforced containers and fire-suppression kits, limiting available slots and pushing rates above standard component freight. Annual driver re-certification adds training hours and costs. Warehouses require fire-walls, negative-pressure rooms, and emergency-response plans, thinning the field of compliant sites. For urgent battery replacements, airfreight is often precluded, forcing ground expedites that stretch delivery timelines and compress margins throughout the North America Automotive Logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Amid Value-Added Growth

Transportation generated 51.45% of the North America Automotive Logistics market size in 2025, anchored by road haulage that shuttles components between tier-1 suppliers and assembly plants. Intermodal rail corridors link Mexican factories with Midwest hubs, benefiting from locomotive fleet upgrades that raise velocity. Airfreight retains a niche for high-value ECUs and urgent tooling. Value-added services—kitting, sequencing, and light assembly—are growing at a 2.95% CAGR (2026-2031) as automakers offload non-core tasks to 3PLs, freeing floor space for EV production lines.

Providers differentiate through digital twins that model plant inventories and push kanban replenishment, shrinking work-in-process buffers. Warehousing footprints add mezzanines for returns processing and battery-state-of-health diagnostics. The segment shift rewards integrators that can couple transport with in-plant material-handling teams and line-side just-in-sequence delivery. Consequently, value-added contracts are lengthening to five-plus years, locking in cross-selling potential across the wider North America Automotive Logistics market.

By Type: Aftermarket Dynamism Outpaces OEM Stability

OEM flows still command 56.20% of the North America Automotive Logistics market share in 2025, supported by stable model-year production cycles and high-volume, repetitive lane structures. Yet, aftermarket logistics is accelerating at a 3.65% CAGR (2026-2031) on the back of aging vehicle fleets and click-to-door parts sales that require parcel networks and urban micro-hubs. Aftermarket SKUs exceed 500,000 part numbers, necessitating AI-driven slotting algorithms and robotic piece-picking to meet same-day delivery promises.

Reverse-logistics streams for core returns and battery recycling grow in parallel. OEM supply chains, bolstered by near-shored component production, concentrate on line-feeding precision and downtime avoidance, employing EDI-linked visibility dashboards. The divergence in service models encourages 3PLs to run discrete operating divisions, each tailored to the cadence and volatility of its customer segment within the North America Automotive Logistics industry.

By Cargo Type: EV Battery Complexity Drives Specialization

Finished vehicles accounted for 40.30% of the North America Automotive Logistics market size in 2025, moving on double-deck car carriers and rail autoracks that now employ telematics to track jounce-and-tilt forces. Auto components follow as the volume leader by shipment count, yet yield slimmer per-lane revenues. EV batteries and power electronics, projected to rise 3.32% CAGR to 2031, command premium freight rates because of hazmat compliance and temperature-controlled requirements.

Specialized flat-rack containers with fire-retardant linings reduce thermal-runaway risk. Sensor arrays beam real-time state-of-charge data to control towers, where intervention protocols trigger should thresholds swing. Ancillary cargo—fluids, tires, and accessories—grows at market pace but must navigate evolving EPA disposal mandates. Cargo-type diversification thus fuels investment in modular equipment fleets able to flex across automotive product categories, deepening specialization within the North America Automotive Logistics market.

Geography Analysis

The United States dominates the North America Automotive Logistics market, holding 78.35% share in 2025, thanks to entrenched production clusters, a comprehensive freight rail network, and dense interstate highways. Environmental rules and labor shortages elevate operating costs, spurring the adoption of electric yard tractors and driver-assist systems. Technology pilots scale rapidly because shippers prioritize real-time visibility and on-time performance across a vast domestic dealer network.

Mexico is expected to post the fastest 3.98% CAGR to 2031 as OEMs shift EV and ICE model allocations southward to meet USMCA thresholds. Pacific port upgrades at Lázaro Cárdenas and Manzanillo add Ro-Ro lanes, while inland rail corridors integrate with new dry ports that pre-clear customs. Growing supplier parks around Monterrey and Guanajuato attract 3PL campuses offering bonded warehousing, sequencing, and yard management, making Mexico a magnet for fresh capital within the North America Automotive Logistics market.

Competitive Landscape

Consolidation gives top providers scale economies, yet the North America Automotive Logistics market retains space for regional specialists. DSV’s takeover of DB Schenker in 2025 created a multibillion-dollar giant with integrated cross-dock-to-dealer capability. DHL’s acquisition of Inmar added reverse-logistics depth, particularly in e-commerce returns, strengthening end-of-life component flows for tier-1 suppliers.

Investment in AI routing and warehouse robotics is redefining service benchmarks; early adopters report 10-15% cost take-out alongside on-time improvements. Battery-logistics certification forms a new moat—companies with trained hazmat crews and fire-suppression-equipped trailers win dedicated contracts with EV makers. Patent activity in autonomous yard-shunting, previously a niche, accelerates as 3PLs seek labor-light models to offset wage inflation.

Vertical integration trends see carriers adding contract manufacturing services such as module sub-assembly inside warehouses adjacent to plants, locking in five-year+ agreements. Yet niche operators survive by mastering difficult lanes—mountain passes, winter routes, or cross-border paperwork—where giant platforms may lack agility. The resultant ecosystem marries scale efficiencies with specialist knowledge, sustaining diverse competition within the North America Automotive Logistics market.

North America Automotive Logistics Industry Leaders

DHL

C.H. Robinson

XPO Logistics

Penske Logistics

Ryder System Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV closed its USD 14.9 billion Schenker deal, unlocking multimodal automotive capacity across North America.

- March 2025: Kuehne + Nagel consolidated three Laredo cross-docks into a 40,000 sq m facility, doubling prior capacity.

- January 2025: DHL Supply Chain acquired Inmar Supply Chain Solutions, adding 14 returns centers and 800 associates.

- June 2024: Ryder opened a 228,000 sq ft Nuevo Laredo warehouse and expanded its drayage yard to manage 250,000 annual border moves.

North America Automotive Logistics Market Report Scope

The automotive logistics process involves the planning, implementation, and control of an efficient and effective movement and storage of vehicles, parts, or related materials from origin to consumption point. A complete background analysis of the North American automotive logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The North American automotive logistics market is segmented by services (transportation, warehousing, distribution, and inventory management, and other services), type (finished vehicle, auto components, and other types), and country (United States, Canada, and Mexico). The report offers market size and forecasts for all the above segments in value (USD).

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea / Ro-Ro / Short-Sea | |

| Warehousing, Distribution & Inventory Management | |

| Value-added Services |

By Type

| OEM |

| Aftermarket |

By Cargo Type

| Finished Vehicles |

| Auto Components |

| EV Batteries and Power-Electronics |

| Other Cargo |

By Country

| United States |

| Canada |

| Mexico |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea / Ro-Ro / Short-Sea | ||

| Warehousing, Distribution & Inventory Management | ||

| Value-added Services | ||

| By Type | OEM | |

| Aftermarket | ||

| By Cargo Type | Finished Vehicles | |

| Auto Components | ||

| EV Batteries and Power-Electronics | ||

| Other Cargo | ||

| By Country | United States | |

| Canada | ||

| Mexico |

Key Questions Answered in the Report

What is the 2026 value of the North America Automotive Logistics market?

The market stands at USD 53.81 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to expand at a 3.61% CAGR to reach USD 64.23 billion by 2031.

Which geography is projected to record the quickest growth?

Mexico is forecast to post the fastest 3.98% CAGR through 2031.

Which service segment is expanding the fastest?

Value-added services such as kitting and sequencing are growing at 2.95% CAGR.

What cargo category commands premium pricing?

EV batteries and power-electronics, due to hazardous-materials compliance requirements.

How is consolidation influencing competition?

Large acquisitions like DSV-Schenker are creating integrated platforms, yet space remains for specialists serving niche lanes or battery logistics.

Page last updated on: