Ready-to-Drink Protein Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

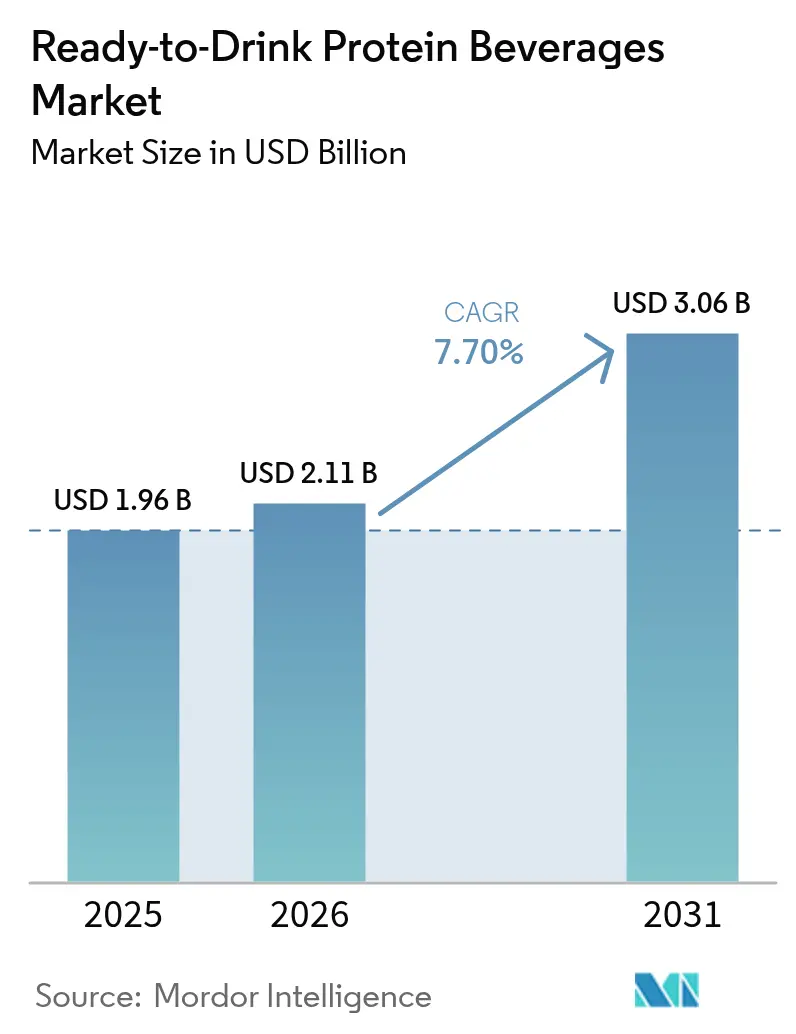

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 7.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ready-to-Drink Protein Beverages Market Analysis by Mordor Intelligence

The Ready-to-Drink (RTD) protein beverages market size was valued at USD 1.96 billion in 2025 and estimated to grow from USD 2.11 billion in 2026 to reach USD 3.06 billion by 2031, at a CAGR of 7.70% during the forecast period (2026-2031). This growth stems from changing consumer preferences, combining health awareness with the need for convenient nutrition options in modern lifestyles. Consumers increasingly prefer portable nutrition solutions that support fitness, muscle recovery, and wellness while maintaining taste and quality. Market growth factors include the expanding global fitness culture, urbanization, and rising demand for plant-based and allergen-free proteins. Animal-based proteins, particularly whey, remain dominant due to established dairy infrastructure and consumer trust. However, plant-based alternatives like pea and soy proteins are gaining market share, driven by environmental consciousness and sustainable diet preferences. North America dominates the market through its robust retail infrastructure, acceptance of premium products, and established fitness culture. The Asia-Pacific region shows the highest growth rate, supported by economic development, increasing health awareness among middle-class consumers, and favorable regulations.

Key Report Takeaways

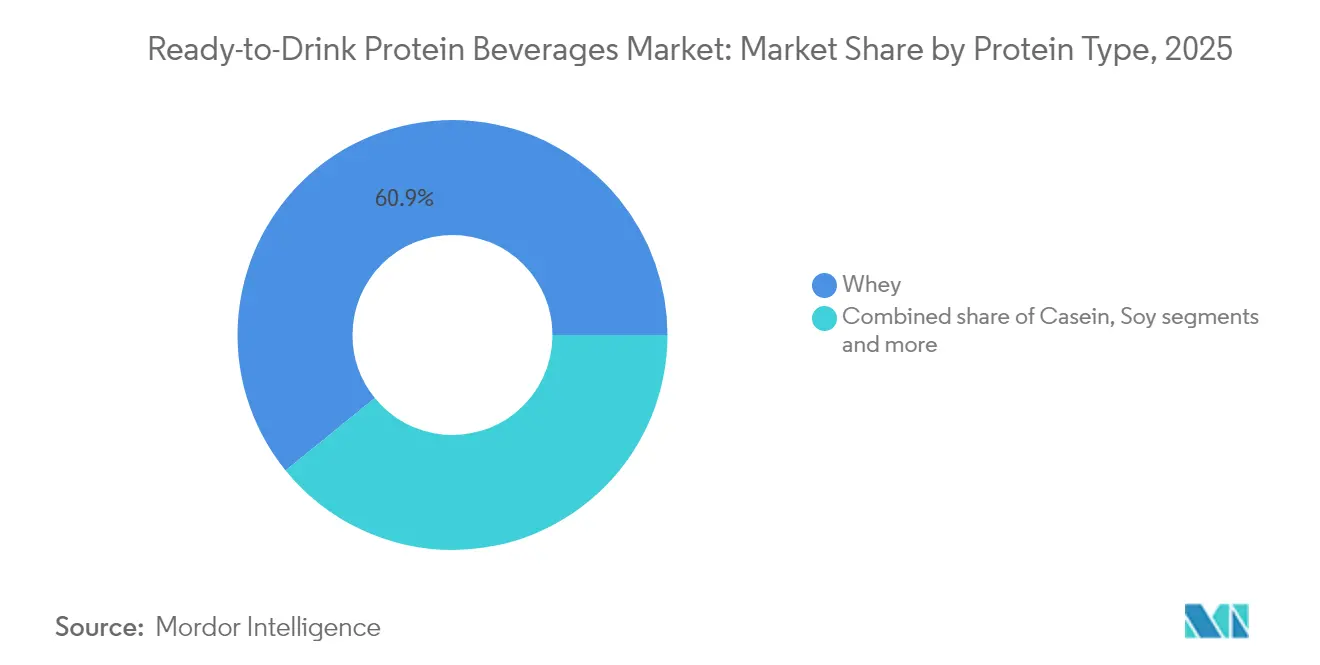

- By protein type, whey protein held 60.85% of the Ready to Drink Protein Beverages market share in 2025; pea protein is projected to expand at a 8.74% CAGR through 2031.

- By protein source, animal proteins accounted for 70.55% share of the Ready to Drink Protein Beverages market size in 2025, while plant-based proteins are advancing at an 8.33% CAGR to 2031.

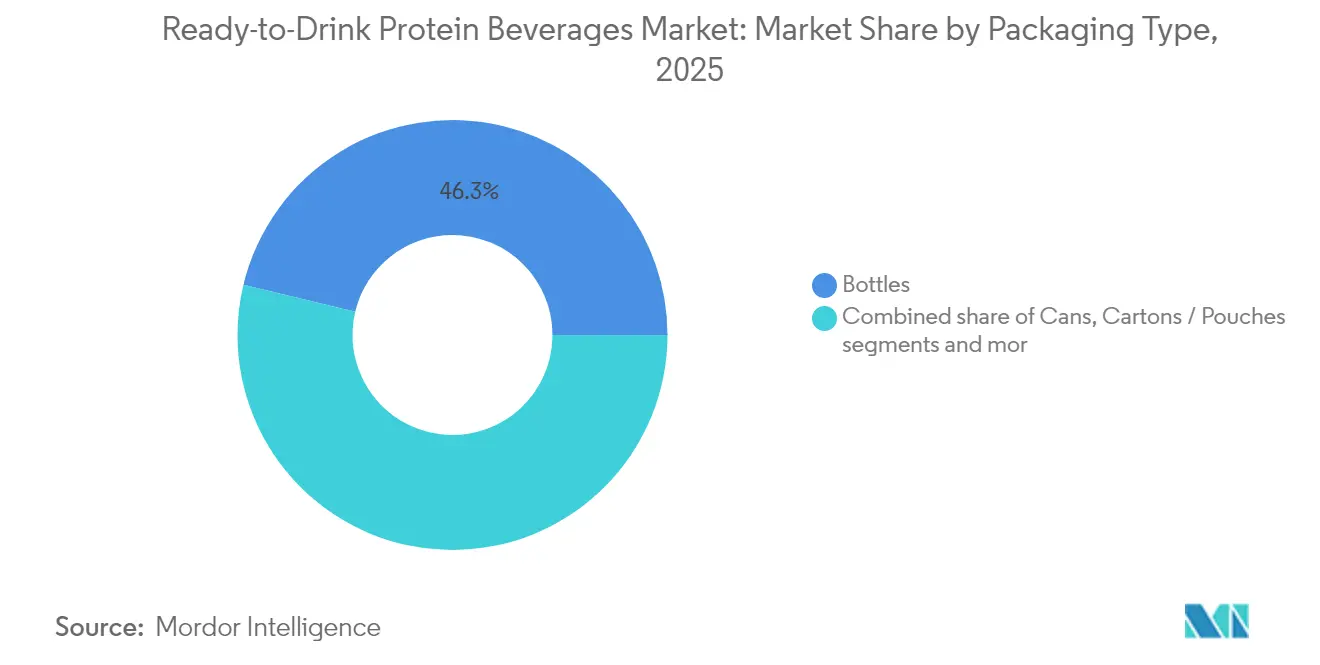

- By packaging type, bottles captured 46.25% revenue share in 2025; cartons and pouches are forecast to grow at a 7.75% CAGR between 2026-2031.

- By distribution channel, supermarkets and hypermarkets commanded 53.10% share of the Ready to Drink Protein Beverages market size in 2025; online retail records the highest projected CAGR at 9.85% through 2031.

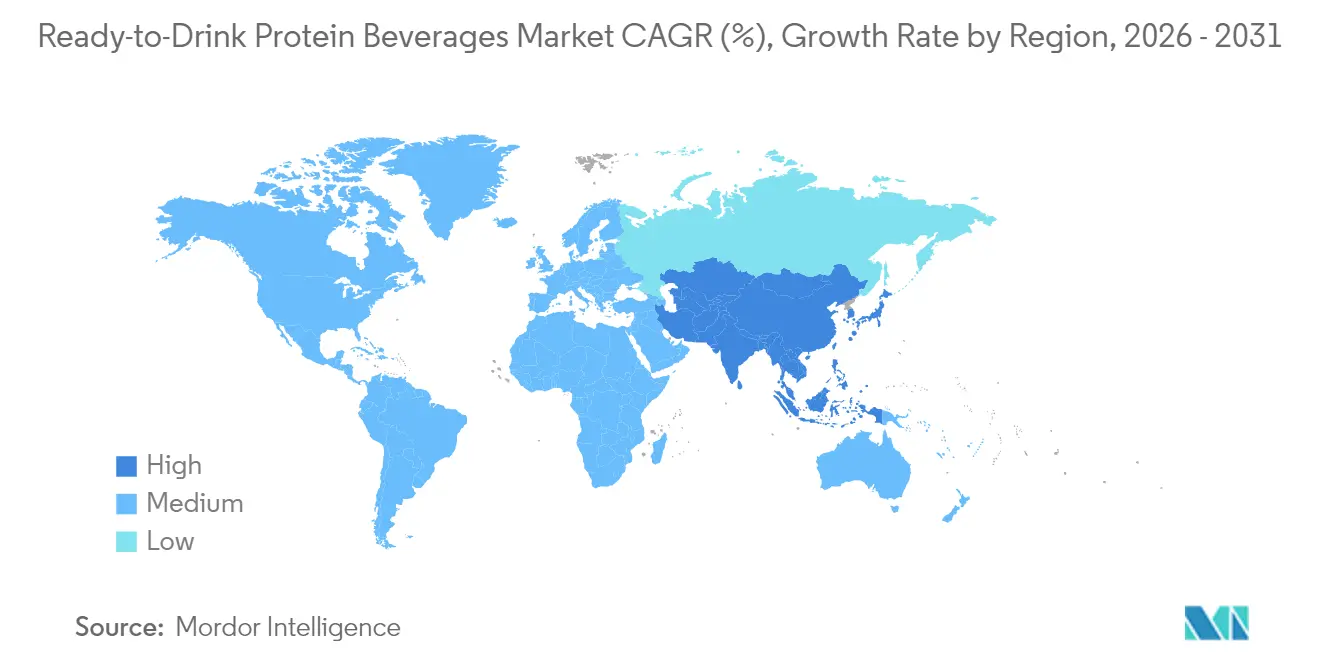

- By geography, North America led with 38.40% revenue share in 2025, whereas Asia-Pacific is set to register the quickest regional pace at a 8.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ready-to-Drink Protein Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and wellness awareness among consumers | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increasing adoption of fitness and active lifestyles | +1.5% | North America and Asia-Pacific core, spill-over to Europe | Long term (≥ 4 years) |

| Growing demand for convenient and on-the-go nutritional solutions | +1.2% | Global, particularly urban centers | Short term (≤ 2 years) |

| Expanding consumer base for plant-based and vegan diets | +0.9% | North America and the European Union, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Continuous product innovation in the market | +0.8% | Global, with strongest impact in North America | Long term (≥ 4 years) |

| Rising demand for meal replacement and weight management products | +1.0% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Wellness Awareness Among Consumers

Health consciousness and wellness awareness among consumers drive the ready-to-drink (RTD) protein beverages market growth. Consumers are increasingly informed about their health due to concerns over lifestyle-related conditions such as obesity, diabetes, and cardiovascular diseases. This awareness leads to healthier eating habits and increased consumption of functional foods and beverages that support weight management, muscle health, and overall well-being. According to the United States Centers for Disease Control and Prevention (CDC), the prevalence of obesity in adults was 40.3% from August 2021 to August 2023 [1]Source: Centers for Disease Control and Prevention (CDC), "Obesity and Severe Obesity Prevalence in Adults", cdc.gov. This high obesity rate, particularly in adults aged 40-59, demonstrates the need for wellness-oriented products and increases consumer interest in ready-to-drink protein beverages. The consistent obesity rates, despite public health initiatives, indicate continued demand for convenient nutrition products that support weight management, muscle health, and overall wellness.

Increasing Adoption of Fitness and Active Lifestyles

The increasing adoption of fitness and active lifestyles drives the ready-to-drink (RTD) protein beverages market growth. Higher participation in structured exercise and gym memberships creates demand for convenient nutrition products that support muscle recovery, energy replenishment, and physical performance. Ready-to-drink (RTD)protein beverages offer an accessible source of high-quality protein, meeting the needs of fitness enthusiasts who require efficient nutrition around workouts. According to the Health & Fitness Association (HFA), in 2024, approximately 77 million Americans aged six and above—representing 25% of the United States population- held memberships in gyms, studios, or fitness facilities. The growth of fitness studios, gyms, and multipurpose clubs, combined with increased attendance rates, generates higher demand for protein supplements that support muscle building, weight management, and recovery. Ready-to-drink (RTD) protein beverages appeal particularly to active consumers who need nutrition solutions compatible with their busy schedules.

Growing demand for convenient and on-the-go nutritional solutions

The increasing consumer demand for convenient and on-the-go nutritional solutions serves as a primary growth factor in the ready-to-drink (RTD) protein beverages market. The contemporary workforce, characterized by intensive schedules, extended commuting periods, and time constraints, necessitates nutritious food alternatives requiring minimal preparation time. Ready-to-drink (RTD) protein beverages fulfill this market requirement by offering portable, pre-packaged protein sources appropriate for consumption across various settings, including workplace environments, post-exercise recovery periods, and during transit. In May 2023, Danone strategically expanded its market presence beyond traditional dairy products through the introduction of Oikos Protein Shakes in the RTD shelf-stable beverage segment. The product specifications include 30 grams of protein, 5 grams of prebiotic fiber to enhance digestive function, 1 gram of sugar without additional sweeteners, and essential vitamins A and D for immunological support per 12-ounce serving. This strategic product introduction addresses the market demand for functional, clean-label nutritional products that accommodate rigorous daily schedules while delivering sustained energy and satiety benefits.

Expanding Consumer Base for Plant-Based and Vegan Diets

The growing consumer preference for plant-based and vegan diets drives the ready-to-drink (RTD) protein beverages market. This growth stems from increased awareness of environmental sustainability, animal welfare concerns, and the health benefits of plant-based nutrition. Consumers seek alternatives to animal-derived proteins due to concerns about climate change, resource scarcity, and ethical food production. The prevalence of dietary restrictions, including lactose intolerance and allergies to dairy and soy, increases demand for plant-based protein sources such as pea, rice, and hemp. Manufacturers are responding by introducing high-protein plant-based beverages. For instance, in January 2024, Suja Organic launched Suja Organic Protein Shakes, containing 16 grams of plant-based protein from pea, rice, and hemp sources. The product line features flavors including Vanilla Cinnamon, Chocolate, and Coffee Bean, addressing consumer demand for nutritious plant-based options. This product launch demonstrates the market's response to consumer requirements for plant-based protein products with organic certification and transparent ingredient labeling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and high raw material costs | -1.2% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Availability of substitutes and intense market competition | -0.8% | Global, most intense in mature markets | Medium term (2-4 years) |

| Stringent regulatory requirements and compliance standards | -0.5% | North America and the European Union primarily | Long term (≥ 4 years) |

| Product development challenges in taste and texture optimization | -0.3% | Global, affecting plant-based segments more | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility and High Raw Material Costs

Raw material price volatility and high costs constrain the global Ready-to-Drink (RTD) protein beverages market growth. The industry depends on essential ingredients like whey, soy, and dairy derivatives, whose prices fluctuate due to climate conditions, supply chain disruptions, and changing trade policies. These price variations increase production costs, making it difficult for manufacturers to maintain competitive pricing while ensuring product quality. According to the United States Department of Agriculture (USDA), the all-milk price is projected at USD 22.00 per hundredweight in 2025 and USD 21.65 per hundredweight in 2026. These high milk prices directly affect the cost structure of protein beverage manufacturers who use dairy-based ingredients. The price instability impacts market growth by reducing profit margins, forcing manufacturers to either increase retail prices, potentially limiting consumer access, or absorb the higher costs, affecting their financial performance. Additionally, manufacturers face challenges in supply planning and strategic operations due to difficulties in accurate cost forecasting.

Availability of substitutes and intense market competition

The global Ready-to-Drink (RTD) protein beverages market encounters substantial limitations attributed to product substitution and market competition. The segment experiences direct competition from alternative protein delivery formats, including protein bars, powders, and conventional dairy products such as milk and yogurt. These substitutes compete across multiple parameters, encompassing price points, accessibility, organoleptic properties, and nutritional composition, subsequently impacting the profit margins of Ready-to-Drink (RTD) beverage manufacturers. The proliferation of protein source fragments affects consumer expenditure and market distribution, creating barriers for individual brands to establish market dominance. Traditional dairy products maintain significant consumer allegiance as fundamental protein sources, particularly in regions with established dairy consumption patterns. This competitive landscape necessitates continuous product development initiatives and strategic marketing investments to sustain consumer engagement and market positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Whey Dominance Drives Market Maturity

Whey protein maintains its market leadership in 2025 with a 60.85% share, supported by established dairy industry infrastructure and consumer familiarity with milk-derived proteins. The United States Department of Agriculture reports that dairy production in the United States reached 227.2 billion pounds, ensuring consistent whey protein availability through higher fat and skim-solids content in milk . This dairy production foundation enables manufacturers to meet demand reliably. Whey protein's market position stems from its nutritional profile, high bioavailability, and muscle recovery benefits, which appeal to fitness enthusiasts and health-conscious consumers.

Pea protein shows the highest growth potential with a projected CAGR of 8.74% from 2026 to 2031. This growth results from increased adoption of plant-based diets and its allergen-free characteristics, which attract consumers with dairy sensitivities and lactose intolerance. Derived from yellow field peas, this protein offers essential amino acids in a hypoallergenic form, providing an alternative to common allergens like dairy and soy. The expansion of vegan, vegetarian, and flexitarian diets, combined with environmental and ethical considerations, increases demand for pea protein as a sustainable option. Consumers choose pea protein for its cardiovascular health benefits, weight management properties, and muscle preservation capabilities.

By Protein Source: Animal Proteins Lead Despite Plant-Based Momentum

Animal-based proteins hold 70.55% of the market share in 2025, primarily due to established supply chains and consumer acceptance of dairy-derived ingredients. The dairy industry infrastructure provides a consistent supply of high-quality proteins such as whey and casein. These proteins offer complete amino acid profiles, high bioavailability, and demonstrated benefits for muscle building and recovery. Consumer preference for these traditional protein sources stems from their familiarity, scientifically validated health benefits, and availability across various formats, including powders, ready-to-drink beverages, and nutritional supplements. The market position strengthens further through innovations in clean-label, grass-fed, and organic options.

Plant-based proteins are experiencing rapid growth at an 8.33% CAGR from 2026 to 2031, driven by evolving dietary preferences and environmental awareness. Proteins derived from pea, soy, lentil, and rice are increasing in popularity due to their allergen-free properties and compatibility with vegan, vegetarian, and flexitarian diets. Consumer concerns about the environmental impact of animal agriculture, including greenhouse gas emissions, land use, and water consumption, support the expansion of plant-based alternatives. Moreover, according to Agriculture and Agri-Food Canada, India's soy milk production used 19.5 metric tons of plant-based protein ingredients in 2023, highlighting the importance of soy protein in the plant-based dairy alternatives market .

By Packaging Type: Sustainability Drives Format Innovation

Bottles constitute 46.25% of the packaging market share in 2025, attributed to established consumer recognition and retail merchandising advantages that enhance product visibility. The conventional bottle format delivers precise portion control and accessibility, specifically advantageous in fitness facilities and professional environments where single-serve packaging is essential. Glass bottles cater to premium market segments, while plastic alternatives provide cost-effectiveness and durability for consumers with active lifestyles. Manufacturers leverage the established bottle production and filling infrastructure to optimize production volume management.

Cartons and pouches demonstrate a projected growth rate of 7.75% CAGR from 2026-2031, primarily attributed to environmental sustainability advantages and technological packaging advancements. Environmental consciousness among consumers and organizational sustainability objectives influence purchasing behaviors across demographic segments. These flexible packaging configurations minimize transportation expenses and maximize storage efficiency, generating operational advantages that translate to enhanced consumer value propositions. The implementation of aseptic processing technologies in cartons and pouches facilitates ambient temperature storage, expanding distribution capabilities and reducing cold chain infrastructure requirements across various geographical regions.

By Distribution Channel: Digital Transformation Reshapes Retail Access

Supermarkets and hypermarkets hold a 53.10% share of distribution in 2025. These traditional retail formats benefit from established consumer shopping habits and create cross-merchandising opportunities that encourage impulse purchases and brand discovery. These channels offer product visibility and sampling opportunities essential for brand development, especially for new product launches and educating consumers about protein beverage benefits. The addition of health and wellness sections in traditional retail stores provides dedicated space for protein beverages, enhancing category visibility and consumer consideration. Distribution reach expands through retail partnerships with fitness centers and health-focused retailers, connecting with key consumer segments.

Online retail is projected to grow at a 9.85% CAGR from 2026-2031, making it the fastest-growing distribution channel. This growth reflects increased e-commerce adoption in food and beverages, supported by subscription models that generate repeat purchases. Digital channels enable direct-to-consumer relationships, providing manufacturers with consumer data and feedback for product development and marketing improvements. Online ordering and home delivery meet the needs of busy consumers while supporting bulk purchases that improve economics for both buyers and manufacturers. E-commerce platforms support purchase decisions through detailed nutritional information and customer reviews, particularly important for functional beverages where benefits require explanation.

Geography Analysis

North America leads the global protein beverage market in 2025, holding a substantial 38.40% share. This leadership stems from its established fitness culture and consumer acceptance of premium functional beverages that drive higher per-capita consumption rates. The region's advanced retail infrastructure supports diverse distribution channels, while consumers demonstrate willingness to pay premium prices for health-oriented products. This market environment supports continuous brand development and product innovation, particularly in clean-label, plant-based, and reduced-sugar formulations. The United States and Canada dominate the North American market, with growing fitness trends, health consciousness, and high health club membership rates driving protein beverage adoption.

Asia-Pacific emerges as the fastest-growing region with a projected CAGR of 8.89% from 2026 to 2031. Economic development and expanding middle-class populations drive this growth. Increased health consciousness, adoption of fitness and protein-rich diets, and urbanization in China, India, Japan, and Australia support market expansion. Manufacturers respond to regional preferences by developing protein beverages with local flavors, including plant-based and clean-label options. Government wellness programs, increasing gym memberships, and consumer interest in sustainable lifestyles further accelerate market growth.

Europe maintains a mature and stable market with established regulatory frameworks and high consumer awareness of functional beverages and their health benefits. South America and the Middle East & Africa demonstrate emerging growth potential driven by urbanization, rising disposable incomes, and increasing health awareness. The growing demand for protein-rich foods and expanding food and beverage industries support market development, alongside rising interest in sports nutrition and supplements.

Competitive Landscape

The ready-to-drink protein beverages market shows moderate fragmentation, with competition among established beverage companies, specialized nutrition firms, and emerging plant-based manufacturers. Market concentration reflects the substantial capital requirements for manufacturing operations and distribution networks. Regulatory compliance requirements create entry barriers that benefit companies with established quality systems and compliance expertise. Major players in the market include Glanbia PLC, PepsiCo Inc., The Coca-Cola Company, Danone SA, and Nestlé S.A.

Companies focus on ingredient differentiation, sustainability credentials, and omnichannel distribution capabilities to gain competitive advantages. Innovation in protein sources and functional ingredients drives product differentiation. The acquisition of OWYN by The Simply Good Foods Company in June 2024 represents strategic consolidation in the plant-based ready-to-drink protein segment, aiming to leverage distribution networks and expand consumer reach.

Technology adoption improves supply chain efficiency and consumer engagement, with digital platforms enabling direct-to-consumer relationships and subscription models that increase customer retention. Companies with robust quality management systems and regulatory compliance capabilities gain advantages through enhanced food safety and preventive controls.

Ready-to-Drink Protein Beverages Industry Leaders

-

Glanbia PLC

-

PepsiCo Inc.

-

The Coca-Cola Company

-

Danone SA

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vital Proteins launched its first ready-to-drink protein shake. The chocolate-flavored beverage contains 30 grams of protein and 10 grams of collagen peptides per serving to support health and wellness objectives.

- July 2025: Not Rocket Science introduced a ready-to-drink protein shake containing 26g of protein for daily consumption. The product, Protein Punch, provides nutritional benefits for regular daily activities. The shake is lactose-free, gluten-free, and contains no added sugar.

- June 2025: BioSteel, a Canadian sports nutrition brand, entered the protein drink market by launching its first Ready-to-Drink (RTD) protein beverage. Each 330mL bottle of BioSteel Protein RTD contains 30 grams of protein and is free from added sugar, preservatives, and lactose.

- April 2025: Nestle launched a new line of protein-based drinks targeting consumers on weight loss programs, specifically those using GLP-1 medications like Ozempic. The products incorporate whey protein microgel technology.

Global Ready-to-Drink Protein Beverages Market Report Scope

The ready-to-drink protein beverages are products produced using a variety of high-protein substances to fulfill the daily nutrient requirements of individuals and are considered a convenient way to consume nutrients on the go. The ready-to-drink protein beverages market is segmented by source, type of packaging distribution channel, and geography. The market is further segmented by source: whey, casein, soy, and other sources. By type of packaging, the market is segmented as bottles, cans, and others. By distribution, the market is segmented as supermarkets/hypermarkets, pharmacies/drugstores, specialist retailers, online retail, and other channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market size for each segment is based on value (USD million).

| Whey |

| Casein |

| Soy |

| Pea |

| Other Sources |

| Animal-based |

| Plant-based |

| Bottles |

| Cans |

| Cartons / Pouches |

| Others |

| Supermarkets / Hypermarkets |

| Pharmacies / Drugstores |

| Specialist Retailers |

| Online Retail |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Protein Type | Whey | |

| Casein | ||

| Soy | ||

| Pea | ||

| Other Sources | ||

| By Protein Source | Animal-based | |

| Plant-based | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Cartons / Pouches | ||

| Others | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Pharmacies / Drugstores | ||

| Specialist Retailers | ||

| Online Retail | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Ready to Drink Protein Beverages market in 2026 and what growth is expected by 2031?

Value reached USD 2.11 billion in 2026 and is projected to hit USD 3.06 billion by 2031, reflecting a 7.70% CAGR driven by health and convenience trends.

Which region buys the most ready-to-drink protein beverages today?

North America leads with 38.40% of global revenue thanks to entrenched fitness culture and premium acceptance.

Which protein source is expanding fastest?

Plant-based beverages, especially those using pea protein, are forecast to grow at an 8.33% CAGR between 2026-2031.

How are online platforms influencing category sales?

Online retail shows a 9.85% CAGR as subscriptions and direct-to-consumer models boost repeat purchases and data-driven personalization.

Page last updated on: