Automotive Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 153.67 Billion |

| Market Size (2031) | USD 349.23 Billion |

| Growth Rate (2026 - 2031) | 17.82% CAGR |

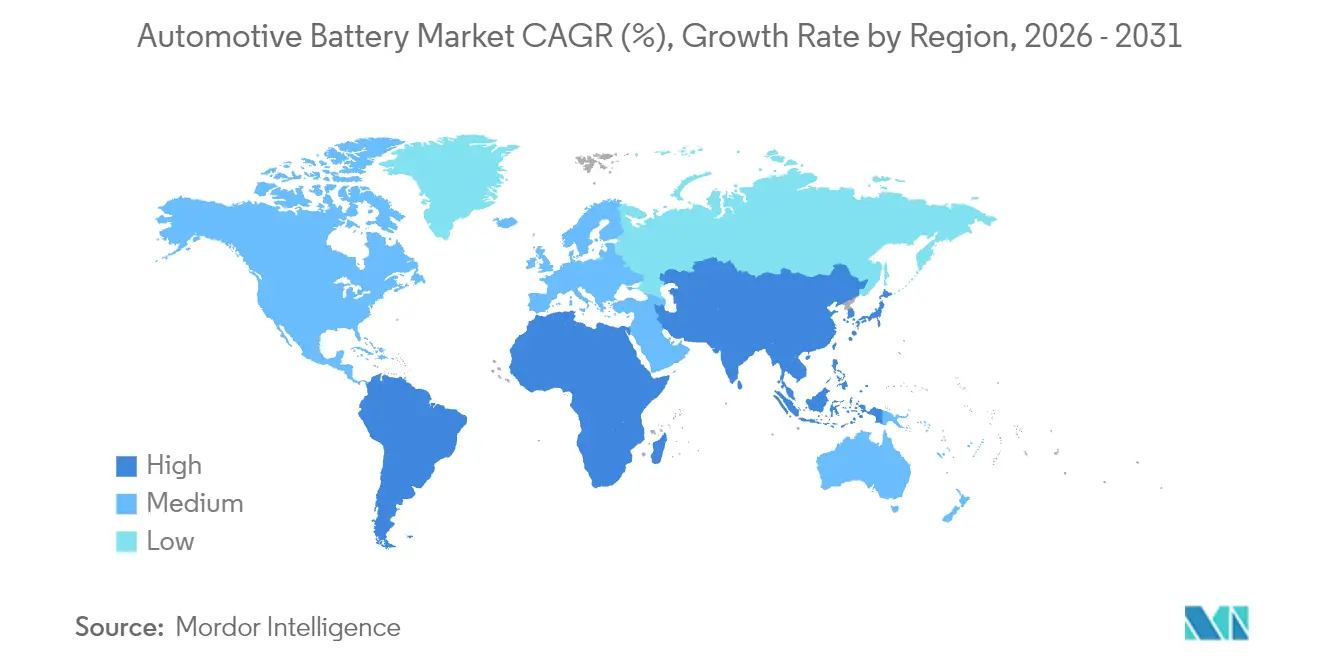

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Battery Market Analysis by Mordor Intelligence

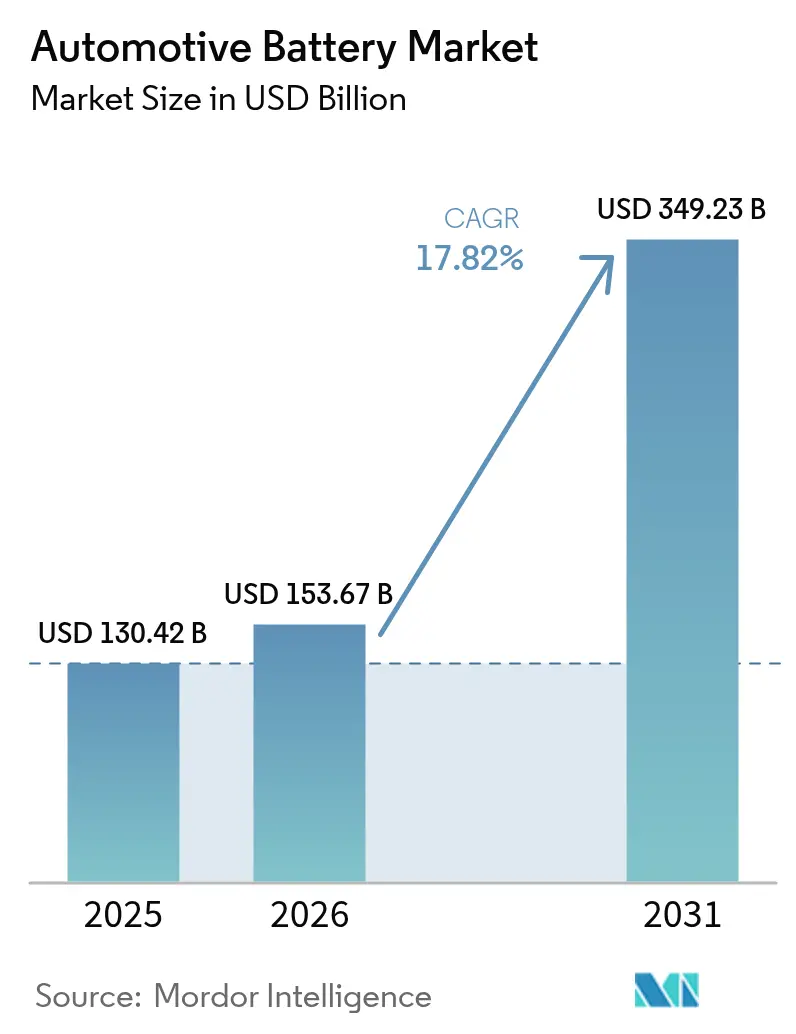

The automotive battery market size is expected to grow from USD 130.42 billion in 2025 to USD 153.67 billion in 2026 and is forecast to reach USD 349.23 billion by 2031 at 17.82% CAGR over 2026-2031. This vigorous expansion reflects a convergence of aggressive electrification mandates, regionalized supply-chain strategies, and breakthrough chemistries that lower total battery costs. China continues to anchor global capacity with 76% of worldwide output in 2024, Europe is advancing its localization efforts through InvestAI. This initiative aims to mobilize EUR 200 billion for AI investments, which includes a new European fund of EUR 20 billion for AI gigafactories. South America is gaining strategic attention as the fastest-growing region, bolstered by Brazil’s 90% year-over-year rise in electric-vehicle sales during 2024. Amid rapid lithium-ion adoption, lead-acid technologies still dominate the starting-lighting-ignition segment, underscoring cost-sensitivity in replacement and aftermarket channels. Competitive intensity stays high as CATL, BYD, and LG Energy Solution collectively control a significant global automotive battery market share.

Key Report Takeaways

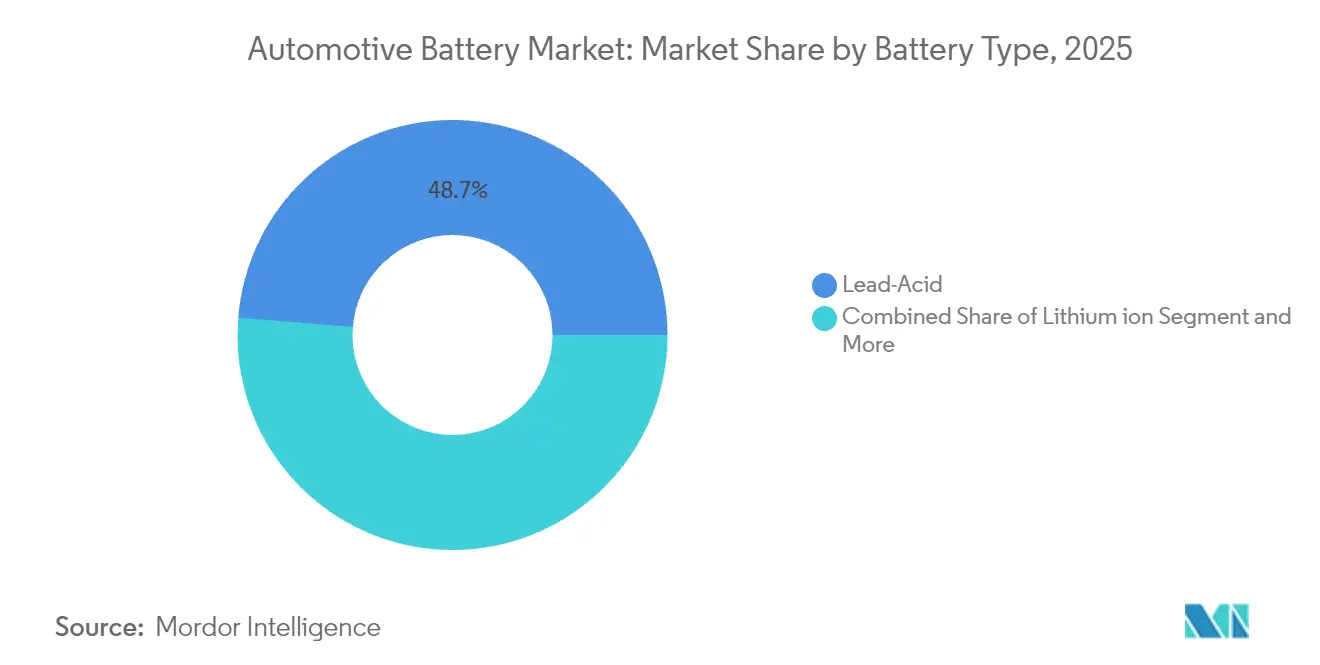

- By battery type, lead-acid captured 48.72% of the automotive battery market share in 2025; Other battery types are forecast to expand at an 18.05% CAGR through 2031.

- By vehicle type, passenger cars held 70.05% of the automotive battery market size in 2025, while medium and heavy trucks are advancing at an 18.44% CAGR.

- By drive type, ICE applications retained 82.55% share of the automotive battery market size in 2025; battery electric vehicles record the highest projected CAGR at 19.18%.

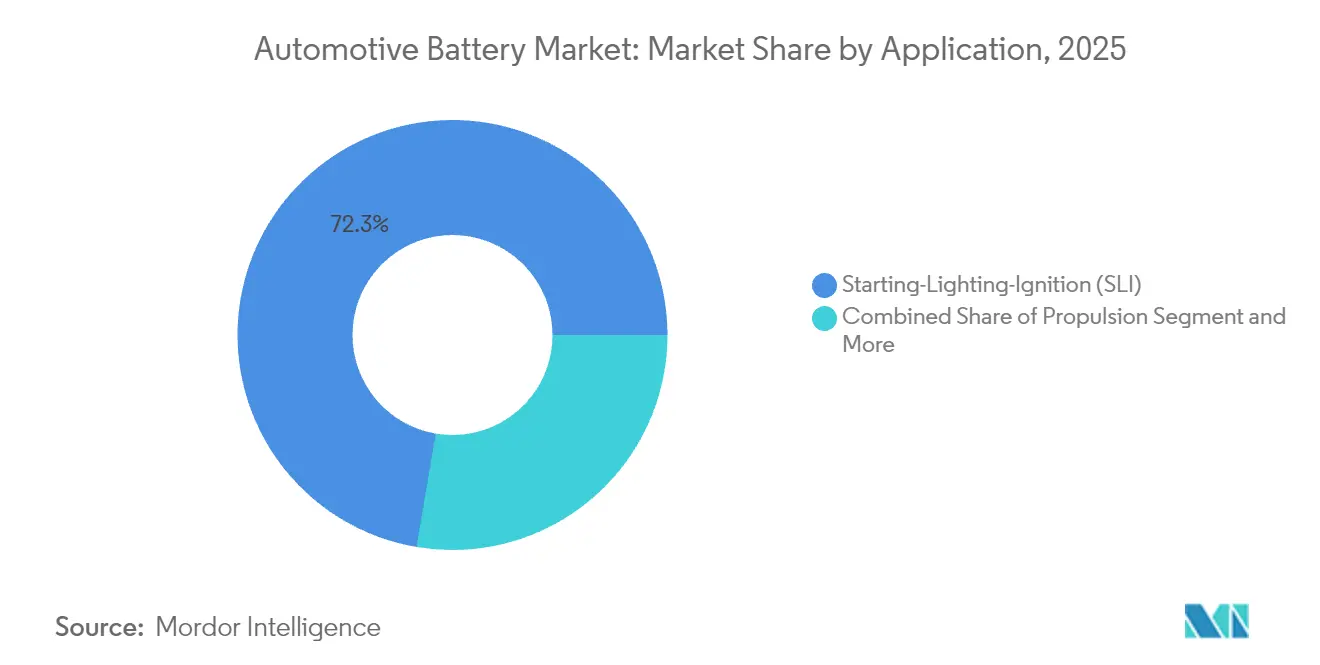

- By application, starting-lighting-ignition commanded a 72.32% share of the automotive battery market size in 2025, and propulsion systems are progressing at an 18.22% CAGR.

- By sales channel, OEMs held a 61.74% share of the automotive battery market in 2025, whereas the aftermarket grew at an 17.95% CAGR.

- By geography, Asia-Pacific led 42.68% of the automotive battery market share in 2025; South America exhibits the fastest regional CAGR at 18.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV Production and Sales | +3.2% | Global, Asia-Pacific leads with manufacturing share | Short term (≤ 2 years) |

| Government Incentives and Emission Norms | +2.8% | North America and EU, expanding to Asia-pacific | Medium term (2-4 years) |

| Vehicle-to-grid Pilots Boosting Second Life | +2.1% | North America and EU early adoption | Long term (≥ 4 years) |

| Rapid Decline in Li-ion Price/kWh | +1.9% | Global, China reaches USD 100/kWh for commercial use | Short term (≤ 2 years) |

| Localization via IRA/EU Subsidies | +1.6% | North America and EU | Medium term (2-4 years) |

| Growing Demand for 12 V Li-ion Replacements | +1.4% | Global, Europe leads in premium models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging EV Production and Sales

Global EV sales climbed to 14 million units in 2024, lifting the automotive battery market toward record volumes[1]“2024 Impact Report,”, Tesla Inc., tesla.com. China supplied 80% of electric truck deliveries, but momentum now spreads to commercial fleets in Europe and North America. Battery cost parity achieved at USD 100/kWh in China has widened adoption to price-sensitive segments. Heavy-duty operators favor lithium iron phosphate packs that now support 300-mile ranges without nickel-rich chemistries. Fleet buyers increasingly regard electrification as an operational necessity once predictable energy outlays and lower service downtime are factored in.

Government Incentives & Emission Norms

The U.S. Inflation Reduction Act requires domestic battery-component content, while the EU Battery Regulation mandates carbon footprint [2]“Regulation (EU) 2023/1542,” European Commission, europa.eu. Such rules compel manufacturers to build regional capacity, breaking dependence on single-region supply chains. California’s Advanced Clean Fleets rule fixes a 2036 zero-emission target for medium and heavy vehicles, strengthening long-term demand visibility. Plants near renewable-power sources gain a cost edge because life-cycle emissions enter purchasing criteria. As similar frameworks appear in Japan, Canada, and India, the automotive battery market expands across multiple continents.

Localization Via IRA/EU Battery Subsidies

North American and European cell plants qualifies for generous tax credits and low-interest loans. Local sourcing requirements push tier-2 suppliers to co-locate, creating regional ecosystems that reduce shipping cost and political risk. OEMs negotiate long-term take-or-pay contracts to lock in capacity, which improves project finance and accelerates construction. Spillover benefits reach Canada and Mexico through the United States–Mexico–Canada Agreement. Although ramp-up costs elevate near-term pack prices, localized output stabilizes long-term supply for the automotive battery market.

Growing Demand for 12 V Li-Ion Start-Stop Replacements

Premium European brands now install 12 V lithium-ion batteries in start-stop systems, attracted by weight savings and superior cycling. Clarios, a North American corporation, is set to bolster its vehicle battery production in Europe. Having initiated factory expansions in 2022, Clarios is now channeling an investment of 200 million euros into its existing European facilities. This move aims to boost the production of advanced AGM (Absorbent Glass Mat) batteries in the EMEA region (Europe, the Middle East, and Africa) and enhance customer supply. In 2024, Eberspaecher, a prominent European player, also rolled out an ASIL-C-rated 12 V lithium-ion battery management system tailored for automotive use. This system, featuring an integrated semiconductor-based switch, is now powering the starter battery of a global automotive manufacturer, bolstering the safety of automated driving functions. Transitioning from lead-acid to lithium-ion batteries in the low-voltage range has resulted in significant weight savings. Based in Esslingen, this automotive supplier is already pioneering the next-gen battery management systems, targeting 12 to 48 volts. Moreover, regulatory fuel-economy targets in China, Korea, and the United States further drive adoption. Suppliers of battery monitoring electronics gain new revenue opportunities as micro-hybrid penetration widens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical Mineral Supply Volatility | -1.8% | Global, exposure in lithium, cobalt, nickel | Short term (≤ 2 years) |

| Thermal-Runaway Recalls and Safety Perceptions | -1.2% | Global, heightened sensitivity in Asia-Pacific | Medium term (2-4 years) |

| Solid-state and Na-ion Tech Risk | -0.9% | Global, threatens current Li-ion assets | Long term (≥ 4 years) |

| Recycling Over-Capacity | -0.7% | North America and EU first, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Critical Mineral Supply Volatility

Lithium carbonate prices oscillated after geopolitical disruptions in South America and Africa. China refines approximately 60% of lithium and 80% of cobalt, creating a single-point risk for cell manufacturers[3]“Long-Term Cathode Supply Agreement with LG Chem,”, General Motors, gm.com. Automakers like General Motors signed USD 19 billion deals to secure cathode feedstocks through 2035, reducing exposure but tying up capital. Sodium-ion research accelerates to diversify chemistries, yet automotive qualification demands three-to-five-year cycles, leaving a near-term vulnerability window. Price swings compress margins, particularly for mid-tier pack assemblers lacking long-term supply contracts.

Thermal-Runaway Recalls and Safety Perceptions

High-profile battery fires in Korea led regulators to require disclosure of cell brands on vehicle labels in 2024 [4]“EV Safety Disclosure Requirements,", Government of Korea, korea.go.kr . Insurance premiums for EVs in some markets exceed ICE equivalents by 10%, reflecting perceived risk. Manufacturers responded with enhanced thermal interfaces and cell-to-pack designs, but public confidence trails technical progress. Recall expenses can exceed, eroding profitability and denting brand perception. As urban charging infrastructure densifies, landlords and local authorities impose stricter safety certifications, adding compliance costs to the automotive battery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lead-Acid Holds Ground While Solid-State Accelerates

Lead-acid systems retained 48.72% of the automotive battery market share in 2025, illustrating the inertia of established SLI demand. The automotive battery market responds with parallel growth in lithium-ion variants that dominate propulsion packs, yet cost-sensitive replacement cycles keep lead-acid relevant. Enhanced flooded and absorbent glass-mat designs extend calendar life, while recycling networks recapture 99% of materials. Other battery types, such as solid-state batteries, although only on a pilot scale, are projected to rise at an 18.05% CAGR, representing the fastest sub-segment within the automotive battery market. Their promise of higher energy density and inherent safety attracts OEM investment, even as questions about throughput and anode supply linger.

The transition is not binary. LMFP, LFP, and NMC chemistries evolve simultaneously, while sodium-ion prototypes move into light commercial vehicles. Clarios, with 11 production facilities and two lead-acid battery recycling plants in the EMEA region, is ramping up its global investments. The focus is on manufacturing AGM batteries, aiming to bolster the Varta Automotive brand's presence in the EMEA aftermarket and ensure quicker and more efficient customer supply. Between 2022 and 2026, Clarios is channeling an investment of roughly EUR 200 million into its European facilities. The company aims to bolster production capacities for its advanced absorbent glass mat (AGM) vehicle batteries. By 2026, annual production is set to surge by approximately 50%. Other chemistries, such as lithium-sulfur and zinc-air, target aerospace and grid back-up niches. Producers allocate capex across multiple chemistries to hedge against future shifts, keeping the automotive battery market diversified and resilient.

By Vehicle Type: Commercial Electrification Takes Off

Passenger cars accounted for 70.05% of the automotive battery market in 2025, yet heavy trucks recorded the sharpest momentum with an 18.44% CAGR. Due to cost declines and rising diesel prices, pack sizes of 350-500 kWh are now economical for regional-haul operations. China captured 80% of electric-truck sales, leveraging cell supply and domestic policy support. Light commercial vans follow closely in major cities' last-mile delivery fleets pressed by zero-emission zones.

SUV demand pushes average pack capacity above 90 kWh, increasing raw-material intensity and challenging mineral supply security. Two-wheelers in India and Southeast Asia integrate standardized modules that facilitate swap stations, multiplying unit volumes. Off-highway equipment lags but demonstrates potential as pilot projects in mining and agriculture prove durability. Together, these trends sustain a broad vehicle-mix expansion that anchors long-term growth in the automotive battery market.

By Drive Type: ICE Leads but BEV Surges

Internal combustion engine applications still represented 82.55% of the automotive battery market share in 2025, reflecting the massive global fleet that requires SLI replacements. Yet battery electric vehicles advanced at a 19.18% CAGR, closing the gap rapidly..

In Europe and Japan, where charging availability fluctuates by region, hybrid and plug-in hybrid variants fill the infrastructure void by providing a practical alternative to fully electric vehicles. While fuel-cell trucks occupy a niche segment, they're gaining traction due to policy incentives in California and Germany, which aim to promote cleaner transportation solutions. OEMs are adopting 48 V mild-hybrid systems to enhance fuel economy, leading to a surge in demand for specialized lithium-ion modules designed to meet these requirements. This blend of technologies drives diverse procurement strategies in the automotive battery market, emphasizing a multi-chemistry approach to cater to varying performance and cost needs.

By Application: Propulsion Becomes Value Engine

Starting-lighting-ignition still held 72.32% of the automotive battery market size in 2025, driven by the global stock of legacy vehicles. Propulsion packs, however, are the fastest-growing use case at an 18.22% CAGR and now account for the majority of dollar value. Propulsion’s ascent forces suppliers to refine thermal management, fast-charging capability, and software for state-of-health analytics.

Auxiliary batteries remain important for redundancy in electric power steering and ADAS systems. Second-life adoption creates circular value streams as fleets monetize residual capacity in stationary storage. Battery-as-a-service contracts, led by NIO, blur strict application lines, turning packs into managed assets that migrate between mobility and grid services. These developments diversify revenue pools in the automotive battery market.

By Sales Channel: Aftermarket Reinvents Itself

OEMs controlled 61.74% of the automotive battery market share in 2025 through integrated vehicle programs, yet the aftermarket grows swiftly at an 17.95% CAGR. Predictive analytics platforms now schedule preventative maintenance, opening subscription revenue for independent service chains. Cell refurbishers swap degraded modules, extending pack life for ride-hailing fleets and utility trucks.

Standardizing battery enclosures and interfaces lowers entry barriers, allowing third-party suppliers to compete on price and turnaround time. OEMs respond by bundling connected services and longer warranties. Regulatory oversight tightens, favoring service providers with certified recycling pathways. This evolving landscape underscores how value migrates from physical hardware to lifecycle management within the automotive battery market.

Geography Analysis

Asia-Pacific’s 42.68% share underscores structural advantages. China’s cluster of cathode, anode, and separator plants, which shortens lead times and lowers logistics costs, allowing domestic OEMs to launch models in six-month cycles. India’s 50 GWh incentive accelerates localization, with Hyundai-Kia partnering Exide Energy on LFP production for 2026 roll-out. Japan and South Korea focus on high-nickel and solid-state R&D, sustaining premium-chemistry leadership. ASEAN nations incentivize e-two-wheeler assembly, pulling cell suppliers into Vietnam, Indonesia, and Thailand.

Based on policy tailwinds in Brazil, South America grows fastest at 18.01% CAGR, where plug-ins already form 71% of EV sales. Argentina’s lithium triangle attracts cathode investors who aim to ship half-processed materials to local pack plants. Chile leverages abundant copper and renewable power, targeting low-carbon certification that differentiates its exports. Infrastructure gaps remain in rural regions, but public-private partnerships roll out fast-charging corridors along major highways, anchoring future demand growth in the automotive battery market.

North America and Europe commit to supply-chain resilience through the Inflation Reduction Act and the EU Battery Regulation. Plants such as Samsung SDI-GM’s 36 GWh Indiana site and Volkswagen’s planned 240 GWh European network exemplify the trend. Carbon footprint rules in Europe are an advantage of Nordic facilities powered by hydro and wind. Canadian projects integrate raw-material mining with pack assembly, lowering cross-border flows. Together, these regions diminish reliance on Asian imports while sustaining high-wage employment in the automotive battery market.

Competitive Landscape

The market is moderately concentrated: CATL, BYD, and LG Energy Solution command significant share of the automotive battery market, shaping pricing and technology roadmaps. Their dominance stems from vertical integration and multi-chemistry portfolios that span LFP, NMC, and solid-state prototypes.

Technology partnerships sharpen differentiation. Volkswagen expanded its alliance with CATL to co-develop low-carbon cells and vehicle-to-grid software, signaling deeper value-chain cooperation. QuantumScape’s tie-up with Volkswagen aims to bring 40 GWh of solid-state capacity online, potentially rewriting energy-density benchmarks. Toyota and Idemitsu’s lithium-sulfide project targets high-anode stability to accelerate solid-state commercialization.

White-space entrants pursue sodium-ion, lithium-metal, and scalable recycling. Northvolt, ACC, and Verkor champion European green manufacturing, touting renewable power and closed-loop cathode production. Established tier-1 suppliers such as Bosch pivot to battery management systems and thermal modules, leveraging existing OEM relationships. Competitive intensity is expected to rise as subsidies wane and scale economies stabilize, compelling players to differentiate between lifetime value and cell price.

Automotive Battery Industry Leaders

-

Contemporary Amperex Technology

-

LG Energy Solution

-

Panasonic Holdings

-

BYD Co. Ltd.

-

Samsung SDI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Idemitsu, in partnership with Toyota Motor, is working to commercialize next-generation all-solid-state batteries, aiming to launch EVs with these batteries by 2027-2028. The project, estimated at 21.3 billion yen (USD143 million), includes building a new plant by June 2027 to support Toyota's goal of improving EV driving range and reducing charging times.

- February 2025: Eberspaecher and Farasis Energy Europe have formed an exclusive strategic partnership to collaborate on marketing, sales, development, and production of low-voltage batteries for automotive applications. The partnership focuses on high-performance low-voltage batteries for starter, back-up, and mild hybrid applications.

Global Automotive Battery Market Report Scope

A rechargeable battery used to start an automobile is an automotive battery or car battery. Its primary function is to supply an electric current to the electric starting motor, which in turn ignites the internal combustion engine that powers the vehicle's propulsion system or supplies power to electric vehicle motors.

The scope of the automotive battery market is segmented by battery type, vehicle type, drive type, and geography. By battery type, the market is segmented into lead-acid, lithium-ion, and other battery types. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By drive type, the market is segmented into internal combustion engines and electric vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the World.

The report offers the market size in value (USD) and forecasts for all the above segments.

| Lead-Acid |

| Lithium-ion |

| Nickel-Metal Hydride |

| Others (Li-S, Na-ion, Zinc-air) |

| Passenger Cars | Hatchback |

| Sedan | |

| Multi-Purpose Vehicle and Sport-Utility Vehicle | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Trucks | |

| Bus & Coach | |

| Two-Wheelers | |

| Off-Highway | Construction Equipment |

| Agricultural Machinery |

| Internal Combustion Engine (SLI & Start-Stop) |

| Hybrid (HEV & PHEV) |

| Battery Electric Vehicle (BEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Starting-Lighting-Ignition (SLI) |

| Propulsion |

| Start-Stop |

| Auxiliary/12 V Systems |

| Battery-as-a-Service / Swap |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Battery Type | Lead-Acid | |

| Lithium-ion | ||

| Nickel-Metal Hydride | ||

| Others (Li-S, Na-ion, Zinc-air) | ||

| By Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| Multi-Purpose Vehicle and Sport-Utility Vehicle | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Trucks | ||

| Bus & Coach | ||

| Two-Wheelers | ||

| Off-Highway | Construction Equipment | |

| Agricultural Machinery | ||

| By Drive Type | Internal Combustion Engine (SLI & Start-Stop) | |

| Hybrid (HEV & PHEV) | ||

| Battery Electric Vehicle (BEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Application | Starting-Lighting-Ignition (SLI) | |

| Propulsion | ||

| Start-Stop | ||

| Auxiliary/12 V Systems | ||

| Battery-as-a-Service / Swap | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive battery market in 2026?

The automotive battery market size reaches USD 153.67 billion in 2026 and is set to grow at an 17.82% CAGR to 2031.

Which battery chemistry grows fastest through 2031?

Solid-state batteries post the sharpest rise at an 18.05% CAGR as major producers plan mass production from 2027 onward.

What region leads global battery manufacturing?

Asia-Pacific dominates with 42.68% market share in 2025, anchored by China’s 76% share of worldwide cell capacity.

Why is the aftermarket expanding despite fewer mechanical repairs in EVs?

Data-driven diagnostics, second-life repurposing, and subscription-based battery-as-a-service models create fresh revenue streams in the aftermarket.

How is policy shaping battery localization?

The U.S. Inflation Reduction Act and EU Battery Regulation mandate local content and carbon-footprint limits, driving over USD 200 billion in regional gigafactory investments.

Page last updated on: