Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

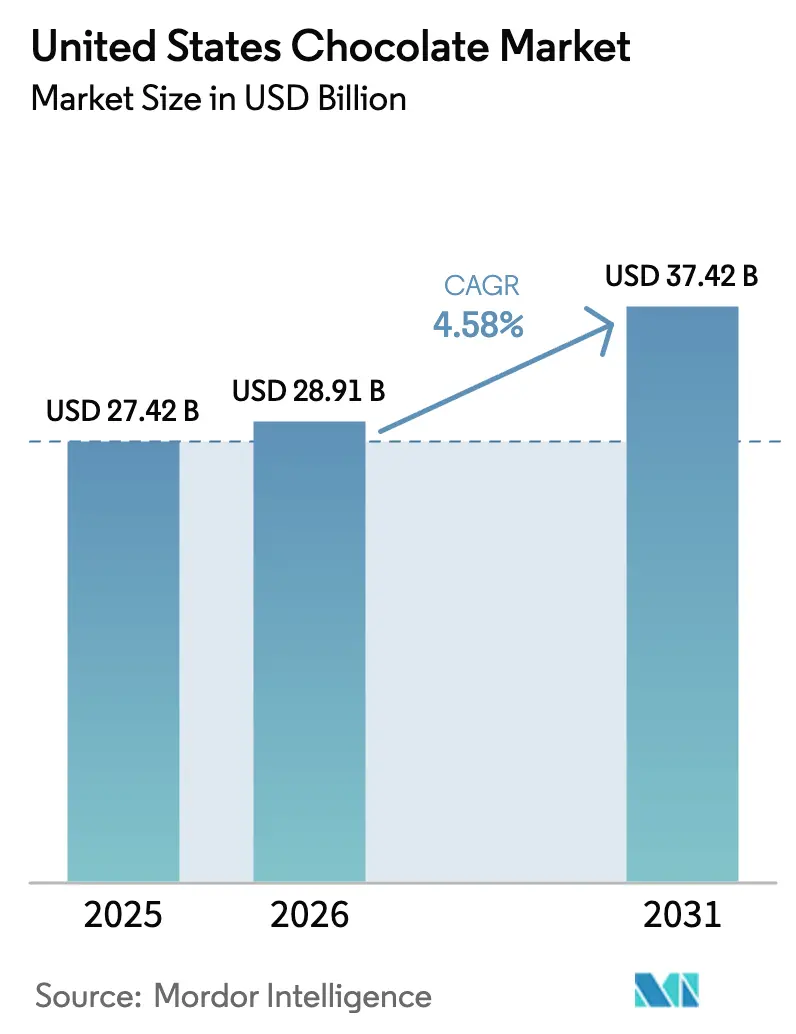

| Base Year Market Size (2025) | USD 27.42 Billion |

| Market Size (2026) | USD 28.91 Billion |

| Market Size (2031) | USD 37.42 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

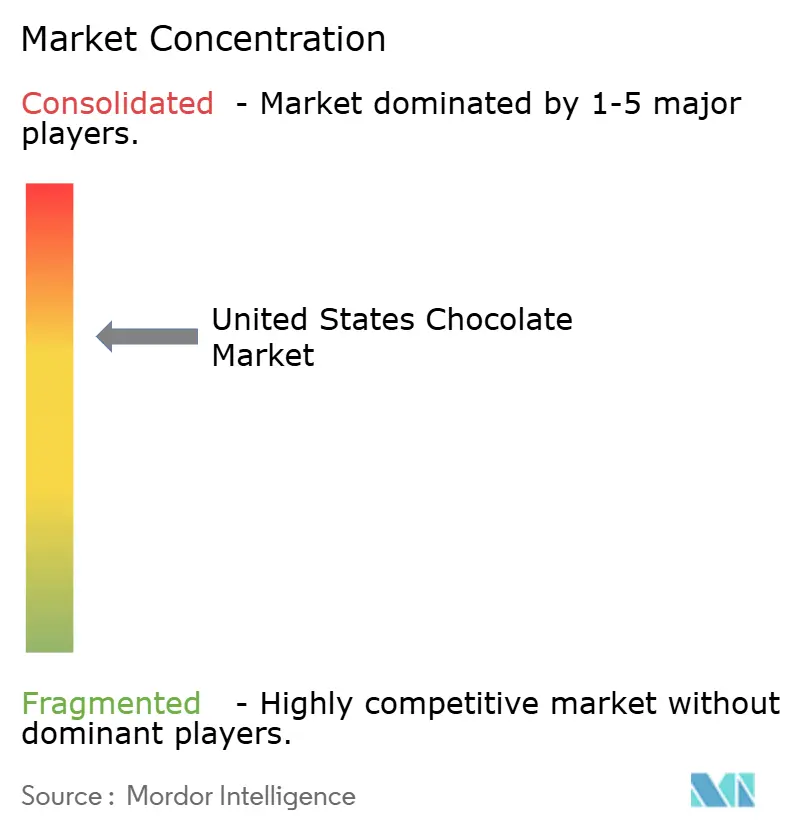

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Chocolate Market Analysis by Mordor Intelligence

The United States chocolate market size was USD 27.42 billion in 2025, stood at USD 28.91 billion in 2026, and is projected to reach USD 37.42 billion by 2031, advancing at a 5.47% CAGR. In 2024, a brief surge in futures prices coincided with a significant increase in retail prices. Yet, volumes remained stable, driven by health-conscious consumers gravitating towards single-origin and plant-based products, especially those sold directly to them through e-commerce platforms. These products appeal to consumers seeking transparency, sustainability, and healthier options, aligning with broader market trends. Mars made headlines with its USD 36 billion acquisition of Kellanova, while Mondelēz is eyeing a potential takeover of Hershey. These moves underscore a trend: major players are leveraging scale to mitigate input volatility, enhance operational efficiencies, and fuel innovation in product offerings. On another front, craft producers are tapping into blockchain-verified sourcing narratives, which provide traceability and authenticity. These stories are captivating younger consumers who are increasingly willing to pay a 30% premium for products that align with their values and preferences.

Key Report Takeaways

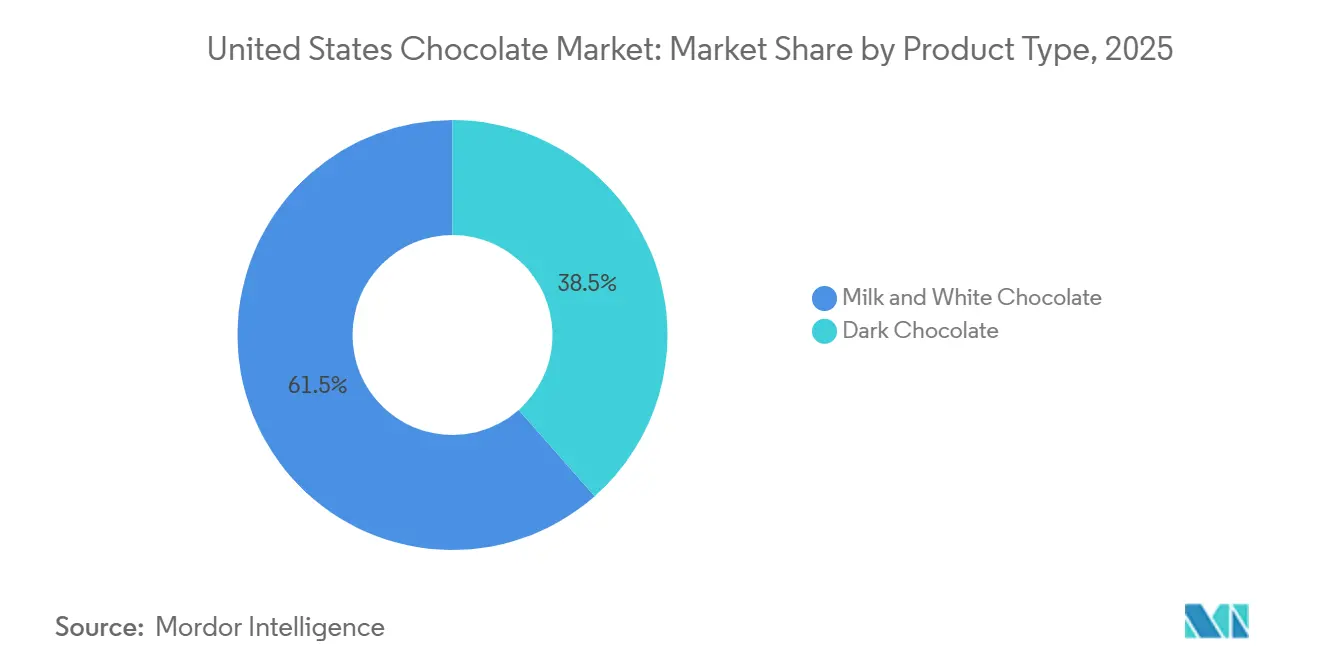

- By product type, Milk and White Chocolate retained 61.51% share in 2025 while Dark Chocolate is forecast to post a 7.83% CAGR to 2031.

- By form, Tablets and Bars held 68.53% share in 2025; Pralines and Truffles are on track for a 6.24% CAGR through 2031.

- By price range, Mass accounted for 54.15% share in 2025, but Premium is set for a 7.42% CAGR.

- By ingredient type, Dairy-based offerings dominated with 71.18% share in 2025; Single Origin Chocolate leads growth at a 10.15% CAGR.

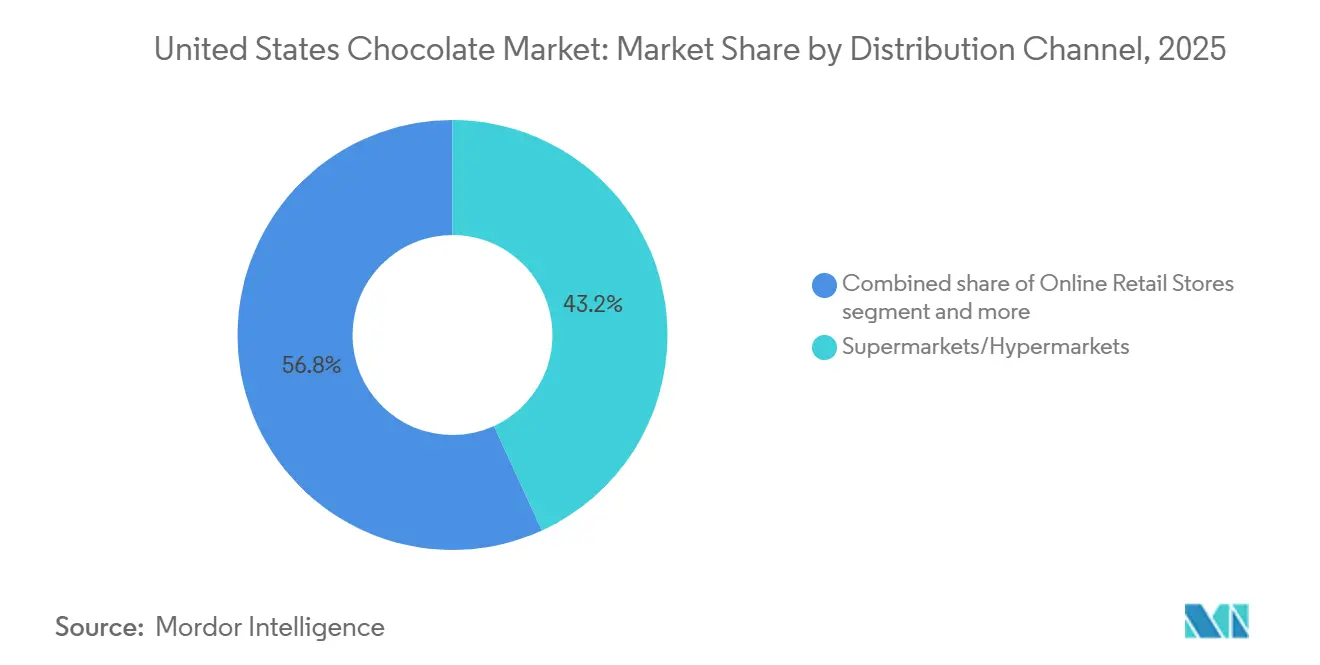

- By distribution channel, Supermarkets and Hypermarkets controlled 43.17% share in 2025 while Online Retail Stores are expanding at a 7.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium and clean-label chocolate | +1.2% | Coastal urban markets and college towns | Medium term (2-4 years) |

| Seasonal and gifting culture sustaining volume sales | +0.8% | Northeast and Midwest peaks in Q4-Q1 | Short term (≤ 2 years) |

| Innovation in flavors and functional inclusions | +0.9% | West Coast and large metropolitan areas | Medium term (2-4 years) |

| Expansion of e-commerce and DTC channels | +1.1% | Suburban and rural markets lacking specialty retail | Long term (≥ 4 years) |

| Corporate bulk-purchase perk programs | +0.5% | Tech hubs and financial centers | Short term (≤ 2 years) |

| Upcycling of cacao fruit into new SKUs | +0.7% | Supply-chain benefits concentrated in sourcing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for premium and clean-label chocolate

As manufacturers grapple with rising cocoa costs, premium positioning has transitioned from a niche focus to a mainstream approach. Today's consumers are more discerning, favoring straightforward recipes that highlight cacao, sugar, and cocoa butter, and shunning artificial emulsifiers. This shift reflects a broader trend toward healthier and more transparent food options. In 2024, Barry Callebaut noted a significant 34% surge in clean-label requests across North America, driven by growing consumer demand for products with minimal and recognizable ingredients. Bars that are single-origin and provide farm coordinates command prices 30% higher and sell more swiftly, meeting the demand for radical transparency. These products not only appeal to ethically conscious buyers but also align with the increasing preference for traceability in the supply chain.

Seasonal and gifting culture sustaining volume sales

Halloween, Valentine's Day, Easter, and winter holidays anchor annual volume, cushioning softer everyday demand. In 2024, Halloween confectionery spending reached USD 4.1 billion, with chocolate making up 70% of sales. Valentine's Day 2024 saw spending hit USD 25.8 billion, led by boxed chocolates and premium truffles[1]Source: National Retail Federation, " Valentine's Day Data Center" , nrf.com. These seasonal events represent critical revenue opportunities for confectionery brands, as they drive significant consumer spending and demand for innovative products. To secure shelf space during these peak times, brands must keep their innovation pipelines active. For instance, Hershey's seasonal KIT KAT Santas and Kisses Snoopy Valentine editions highlight how established brands leverage licenses, limited-edition packaging, and themed offerings to drive impulse purchases and maintain consumer interest.

Innovation in flavors and functional inclusions

Flavor experimentation now melds indulgence with wellness. Dark bars, now infused with adaptogens or probiotics, cater to shoppers desiring treats with added functional benefits, such as stress relief or improved gut health. Hershey’s Reese’s Chocolate Lava Big Cup showcases how texture enhancements, like molten centers, can command a 15-20% price premium by offering a more indulgent experience. Barry Callebaut’s 100% CacaoFruit Experience champions sustainability by repurposing cacao pulp and peel, which are typically discarded, into new product lines. The World Resources Institute highlights that upcycling cacao fruit could boost West African farmer incomes by an estimated USD 500 million annually, providing brands with a compelling ESG narrative that appeals to corporate purchasers focused on sustainability and ethical sourcing.

Expansion of e-commerce and DTC channels

In 2024, e-commerce's share of the U.S. food and beverage market reached 16.4%[2]Source: United States Census Bureau, "QUARTERLY RETAIL E-COMMERCE SALES 3rd QUARTER 2025" , census.gov. Notably, chocolate sales outpaced others, benefiting from efficient shipping and high profit margins. This growth highlights the increasing consumer preference for convenience and the ability to access a wider variety of products online. Craft brands, leveraging direct-to-consumer models, are now testing limited product runs through social media preorders. This approach not only gathers valuable first-party data but also reduces customer acquisition costs, enabling these brands to refine their offerings and target audiences more effectively. Meanwhile, subscription boxes are curating personalized assortments that consumers can't find in traditional stores, offering a unique value proposition by catering to individual preferences and enhancing customer loyalty. Acknowledging the distinct challenges of fulfillment, storytelling, and analytics in the digital realm compared to mass retail, established players are increasingly opting to acquire or partner with digital-native firms instead of developing their own platforms. This strategy allows incumbents to leverage the expertise and agility of digital-first companies while focusing on their core operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cocoa price volatility | -1.3% | Manufacturers lacking forward-hedging programs | Short term (≤ 2 years) |

| Sugar-reduction health pressures | -0.6% | Regulatory influence strongest in California and New York | Medium term (2-4 years) |

| State-level traceability/deforestation rules | -0.4% | States mirroring EU standards | Long term (≥ 4 years) |

| Skilled-labor shortages in artisanal plants | -0.5% | Craft-chocolate hubs lacking vocational training pipelines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cocoa price volatility

In April 2024, cocoa futures surged to USD 12,000 per metric ton, driven by significant crop failures in Côte d'Ivoire and Ghana, which together account for 60% of the global cocoa supply. These crop failures were attributed to adverse weather conditions and pest infestations, severely impacting production levels. By late 2024, prices moderated to the USD 7,000-8,000 range as market conditions stabilized slightly. Despite this price dip, Hershey implemented a 9.5% price hike to offset rising input costs, while Mondelēz experienced a 150 basis point compression in its operating margins, reflecting the challenges of managing profitability in a volatile market. Smaller manufacturers, without the scale to hedge against such price fluctuations, find themselves in a precarious position; a 50% price spike can wipe out their gross margins entirely, threatening their survival. While diversifying sourcing to Latin America and Southeast Asia provides some respite by reducing dependency on West Africa, these regions fall short in terms of infrastructure development and the consistency of cocoa varietals that West Africa offers. The dilemma is clear: passing increased costs onto consumers could lead to a drop in sales volume, yet absorbing those costs can severely dent profitability, leaving manufacturers with difficult strategic decisions.

Sugar-reduction health pressures

In 2024, the FDA set voluntary targets aiming for a 20% sugar reduction over five years. The World Health Organization, emphasizing the need for sugar moderation, suggests keeping free sugars below 10% of total energy intake, with chocolate coming under the spotlight due to its high sugar content and widespread consumption[3]Source: World Health Organization, " Healthy diet", who.int. Reformulating products poses significant challenges: alternatives like stevia, monk fruit, and allulose come with a hefty price tag, and consumer acceptance is still uncertain, as taste and texture often differ from traditional sugar-based products. While Hershey's has ventured into the realm with its sugar-reduced dark bars, leveraging cacao-fruit pulp as a natural sweetener, the journey to scale demands substantial supply-chain investments that often exceed the budgets of many craft producers. Should the industry falter on voluntary compliance, the imposition of mandatory caps could swiftly lead to the discontinuation of numerous SKUs, potentially disrupting product portfolios and market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains Ground on Health Positioning

In 2025, milk and white chocolate commanded a dominant 61.51% share of the U.S. chocolate market, driven by a preference for sweeter flavors and the tradition of seasonal gifting. These segments continue to thrive due to their widespread appeal across various demographics and their association with celebratory occasions. Amidst market saturation and constrained pricing power, innovations like Hershey's 2024 oat-milk Reese's cups bolster their stance by catering to evolving consumer preferences for plant-based alternatives. Meanwhile, General Mills debuted its Reese's Puffs Dark Chocolate cereal in December 2025, signaling a trend of adjacent categories tapping into dark chocolate's health allure to attract health-conscious consumers. However, growth has been tepid as consumers under 40 pivot towards wellness-centric choices, reflecting a broader shift in dietary priorities.

Dark chocolate is on a rapid ascent, boasting a 7.83% CAGR through 2031, outpacing the broader market by a notable 236 basis points. This surge is bolstered by FDA-endorsed flavanol health claims, spotlighting cardiovascular benefits that resonate strongly with health-focused consumers. Thanks to the FDA's 2024 guidance, premium brands can now tout risk reduction claims, allowing for justifiable price hikes of 20-30%. Consumers under 40, viewing dark chocolate as a wellness indulgence, are 40% more inclined to make a purchase. Catering to this discerning audience, craft brands are rolling out 85%+ cacao bars, priced over USD 10 per 100g, emphasizing their antioxidant benefits and appealing to purists who prioritize quality and health attributes in their chocolate choices.

By Form: Tablets and Bars Dominate, but Pralines and Truffles Capture Gifting Premiums

In 2025, Tablets and Bars captured 68.53% of the U.S. chocolate market, thanks to their convenience, portability, and appeal for everyday snacking. Their dominance is further strengthened by established supply chains and extensive retail distribution, ensuring consistent availability across various retail formats, including supermarkets, convenience stores, and online platforms. However, private-label offerings from Trader Joe's and Whole Foods, which match quality but come at 20-30% lower prices, are steadily eroding this market share, pushing the industry towards commoditization. These private-label products appeal to cost-conscious consumers without compromising on taste or quality. In a bid to elevate the segment, Hershey's is launching the Reese's Jumbo Cup in June 2024, targeting the gifting market and aiming to position the format as a premium option for special occasions.

Pralines and Truffles are on a growth trajectory, expanding at a 6.24% CAGR through 2031, largely due to their association with gifting and experiential allure. In 2024, Valentine's Day spending reached a whopping USD 25.8 billion, with a significant portion directed towards boxed varieties. These premium offerings command prices 2-3 times higher per ounce, thanks to their craftsmanship, which includes intricate designs, high-quality ingredients, and unique flavor profiles. Brands like Lindt LINDOR, Godiva, and Dandelion's single-origin pralines emphasize artistry, focusing on texture, layering, and scarcity, which shields them from commoditization. Their appeal lies in the luxurious experience they provide, making them a preferred choice for consumers seeking indulgence and exclusivity.

By Price Range: Premium Segment Outpaces Mass on Transparency and Terroir

In 2025, mass-market chocolate commanded a 54.15% market share, buoyed by brisk sales in grocery, convenience, and drug stores. However, growth is tempered by market saturation and diminished pricing power, with private labels often undercutting established brands by 20-30%. To safeguard their volumes, established players are turning to seasonal variants and premium sub-brands to bolster margins. Seasonal variants, such as holiday-themed chocolates, help maintain consumer interest, while premium sub-brands cater to a growing segment of consumers willing to pay more for perceived quality. Meanwhile, retailers are increasingly prioritizing shelf space for these fast-moving items, ensuring that high-velocity products dominate store shelves.

Premium chocolate, on the other hand, is on a rapid ascent, boasting a 7.42% CAGR through 2031, outpacing the broader market by 200 basis points. This growth is driven by a focus on transparency, sustainability, and product differentiation. For instance, craft bean-to-bar producers not only disclose farm origins and pay premium prices but also command a price point of USD 8-12 for a 100g bar. These producers emphasize ethical sourcing and high-quality ingredients, appealing to a niche but growing consumer base. A 2024 Deloitte survey highlights the trend, revealing that 62% of buyers under 40 are willing to switch brands for verified sustainability. However, the sector grapples with scalability challenges, primarily due to artisanal constraints and sourcing dependencies. Limited production capacity and reliance on specific supply chains make it difficult for these producers to meet rising demand while maintaining their unique selling propositions.

By Ingredient Type: Single Origin Chocolate Leads Growth on Traceability and Terroir

In 2025, dairy-based chocolate commanded a dominant 71.18% share of the U.S. chocolate market, primarily driven by the popularity of milk chocolate. This category's stronghold is attributed to its widespread consumer acceptance and established presence in the market. In 2024, Hershey's launched "Reese's Plant Based," signaling how established players are embracing plant-based trends to safeguard their market positions. While plant-based alternatives, using oat, almond, or coconut milk, address lactose intolerance and vegan preferences, they still grapple with challenges in achieving a creamy texture that matches traditional dairy-based chocolate. Despite a growing shift towards alternatives, the deep-rooted familiarity and trust in dairy-based chocolate products continue to reinforce their market dominance.

Single Origin Chocolate is on a rapid ascent, projected to grow at a 10.15% CAGR through 2031. This surge is fueled by factors like traceability, compelling terroir narratives, and direct compensation for farmers. These chocolate bars, which disclose their exact farm or regional origins, emphasize unique varietal flavors often lost in blends, commanding a premium of USD 8-12 per 100g. The appeal of Single Origin Chocolate lies in its ability to connect consumers with the source of their product, offering a sense of authenticity and exclusivity. Brands like Dandelion, TCHO, and Mast Brothers capitalize on their ethically marketed access to exclusive, rare cacao, which is often sourced through direct trade practices that ensure fair pay for farmers. This level of transparency resonates strongly with younger consumers, who increasingly prioritize ethical sourcing and sustainability, especially in specialty retail channels.

By Distribution Channel: Online Retail Gains Share as DTC Models Proliferate

In 2025, Supermarkets and Hypermarkets commanded a 43.17% share of the U.S. chocolate market, positioning themselves as the primary destination for everyday purchases, thanks to their diverse selections and competitive pricing. These outlets offer a wide range of chocolate products, catering to various consumer preferences and budgets, making them a preferred choice for bulk and routine purchases. Meanwhile, Convenience stores, along with specialty shops, kiosks, and vending outlets, cater to impulse buys and travel-related needs, prioritizing convenience over cost. These channels are particularly effective in capturing last-minute purchases and satisfying on-the-go consumption patterns. To enhance both volume and visibility, many are adopting omnichannel strategies, integrating physical and digital platforms to reach a broader audience. Supermarkets are also pushing back against e-commerce by leveraging their own platforms, focusing more on sales velocity than profit margins, and ensuring a seamless shopping experience for customers.

Online Retail Stores are projected to expand at a robust 7.12% CAGR through 2031. This growth is largely attributed to direct-to-consumer access, allowing craft brands to bypass traditional markups, experiment with flavors without financial risk, and collect valuable purchase data. The direct-to-consumer model also enables brands to build stronger relationships with their customers by offering exclusive products and personalized experiences. E-commerce's penetration in the food and beverage sector reached 16.4% in 2024, a notable rise from 14.8%, with chocolate products benefiting from their ease of shipping and favorable profit margins. Subscription services like Chocomize and Cocoa Runners are setting new standards in personalization, offering curated selections tailored to individual tastes. Lindt's platform, offering custom gifts, showcases how premium brands are forging deeper connections without relying solely on physical shelf space, further enhancing customer loyalty and brand differentiation.

Geography Analysis

In the U.S. chocolate market, regional consumption patterns are influenced by demographic density, income levels, and cultural preferences, though metrics aren't detailed at the state level. Urban coastal hubs like New York, Los Angeles, and San Francisco, with their higher disposable incomes and affinity for specialty retail, are at the forefront of adopting premium and craft chocolates. These cities also dominate e-commerce, with online chocolate sales projected to grow at a 7.12% CAGR through 2031. This surge is partly due to suburban and rural consumers, who, lacking access to specialty retail, increasingly turn to direct-to-consumer platforms. Meanwhile, the Midwest and South show a pronounced loyalty to mass-market brands such as Hershey and Mars, with grocery and convenience store shelf space being the main purchase driver.

In the Northeast and Midwest, colder climates and extended winters bolster gifting traditions, leading to a heightened demand for boxed chocolates and premium truffles during seasonal occasions. Major players like Hershey and Mars, capitalizing on their national distribution networks, maintain their market presence. They introduce seasonal editions and limited-time flavors to stimulate trials without the need for additional shelf space. On the other hand, craft brands, often lacking the capital for mass retail, prioritize establishing a foothold in affluent urban markets before considering regional expansion. Dandelion Chocolate exemplifies this approach, opening flagship stores in San Francisco, Los Angeles, and New York. Each store, featuring in-house production and tasting experiences, underscores the potential of experiential retail in justifying premium pricing and enhancing brand equity prior to venturing into wholesale distribution. However, regional preferences can be rigid; a brand that thrives in coastal markets by highlighting single-origin traceability might find it challenging in the Midwest, where value and brand familiarity dominate purchasing decisions.

Regulatory landscapes differ across states. California and New York, at the forefront of health-centric legislation, may soon impose sugar-reduction targets or front-of-pack warning labels on high-calorie products. The influence of these states is magnified, as manufacturers often reformulate on a national scale, leading to quicker industry-wide shifts towards cleaner labels and reduced-sugar products. While the FDA's 2024 endorsement of cocoa flavanols as a qualified health claim offers a boost for dark chocolate nationwide, state-level traceability rules, akin to the EU's Deforestation Regulation, pose a risk. If compliance costs push smaller brands out of certain states, it could lead to a fragmented U.S. chocolate market. Thus, brands are urged to stay vigilant on regulatory changes at both federal and state levels, investing in adaptable compliance infrastructures that uphold operational efficiency amidst varying requirements.

Competitive Landscape

The U.S. chocolate market exhibits moderate concentration, major players like Mars, Hershey, Ferrero, Mondelēz, and Lindt dominate. However, this concentration belies a growing fragmentation, as craft chocolate makers have emerged over the last decade. These artisans have carved out a niche in premium channels, commanding price premiums of 30-50% over their mass-market counterparts, thanks to their emphasis on transparency and terroir narratives. While industry giants leverage national distribution networks and hefty media budgets to ensure their products are ubiquitous, craft brands cultivate loyalty among sustainability-minded consumers through direct-trade sourcing and exclusive limited-edition releases. Mars' USD 36 billion acquisition of Kellanova in August 2024 underscores its commitment to scale and snacking adjacencies, aiming to consolidate production and explore cross-selling in both confectionery and savory categories. Meanwhile, Mondelēz's December 2024 discussions of a potential USD 50 billion takeover of Hershey highlight a strategic move to navigate cocoa market volatility and bolster innovation funding through consolidation.

Emerging opportunities lie at the crossroads of health, sustainability, and convenience. The rise of plant-based chocolates, utilizing oat, almond, or coconut milk as dairy substitutes, caters to lactose-intolerant, vegan, and flexitarian consumers. Yet, this segment remains under-penetrated compared to its plant-based milk and yogurt counterparts. Hershey's 2024 debut of Reese's Plant Based showcases incumbents' proactive stance against challenger brands. However, the challenge lies in replicating the creamy mouthfeel of milk chocolate without dairy, a feat demanding costly formulation expertise. Another frontier is cacao-fruit upcycling, transforming pulp and peel into juice, flour, and natural sweeteners. Barry Callebaut's CacaoFruit Experience not only showcases this technical feasibility but also highlights its sustainability advantages. While still a niche, blockchain-enabled traceability is gaining momentum. Corporate buyers increasingly seek proof of deforestation-free sourcing to uphold ESG commitments, creating a compliance barrier that smaller brands find challenging to navigate.

Market leaders are adopting varied strategies to fuel their growth. Hershey's August 2024 introduction of the Reese's Chocolate Lava Big Cup, a 2.8-ounce treat with a molten peanut-butter center, exemplifies a push towards premiumization. Priced 15-20% higher than standard cups, it caters to the demand for innovative textures. Barry Callebaut's 2024 launch of the CacaoFruit Experience, a chocolate crafted entirely from cacao fruit's pulp and peel, counters sustainability concerns by monetizing waste and minimizing added sugar reliance, all while introducing a unique flavor profile. With the Kellanova acquisition now complete, Mars stands poised to optimize shared distribution and manufacturing networks. This strategic move not only cuts logistics costs but also accelerates new product rollouts across an expanded snacking range. These maneuvers highlight a landscape where top-tier consolidation coexists with craft-tier fragmentation, signaling potential margin pressures for the middle market unless it carves out distinct cost leadership or genuine differentiation.

United States Chocolate Industry Leaders

-

Chocoladefabriken Lindt & Sprüngli AG

-

Ferrero International SA

-

Mars Incorporated

-

Mondelēz International Inc.

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Hershey's rolled out a limited-edition "Dubai-Inspired" chocolate bar. This bar, featuring creamy pistachio, crispy kadayif, and Hershey's iconic milk chocolate, was restricted to just 10,000 units. They were made available through Gopuff and Hershey’s Chocolate World.

- July 2025: Lindt & Sprüngli USA launched its "Dubai Style" chocolate bars nationwide at major retailers such as Walmart and Target. These bars feature Lindt's signature milk chocolate blended with 45% pistachio paste, along with crunchy kadayif, almonds, and hazelnuts.

- May 2025: Hershey's released the "Milk Chocolate with Caramel Bar," offering a rich, gooey caramel twist to enhance the classic s'mores experience and cater to evolving snacking preferences.

- February 2025: GODIVA unveiled its 2025 Valentine's Day Collection as part of the "Love, GODIVA" campaign. The collection, crafted with premium ingredients to emphasize luxury and passion, was promoted on a Times Square billboard.

United States Chocolate Market Report Scope

The chocolate market encompasses the global industry involved in the production, distribution, and sale of chocolate products derived from cocoa beans.

The chocolate market is segmented by product type, form, price range, ingredient type, distribution channel, and geography. Based on product type, dark chocolate, milk, and white chocolate. Based on form, the market is segmented into tablets and bars, molded blocks, pralines and truffles, and other forms. Based on price range, the market is segmented into mass and premium. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels.

The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single-origin |

By Distribution Channel

| Supermarket/Hypermarket |

| Convenience Store |

| Online Retail |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single-origin | |

| By Distribution Channel | Supermarket/Hypermarket |

| Convenience Store | |

| Online Retail | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms