Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

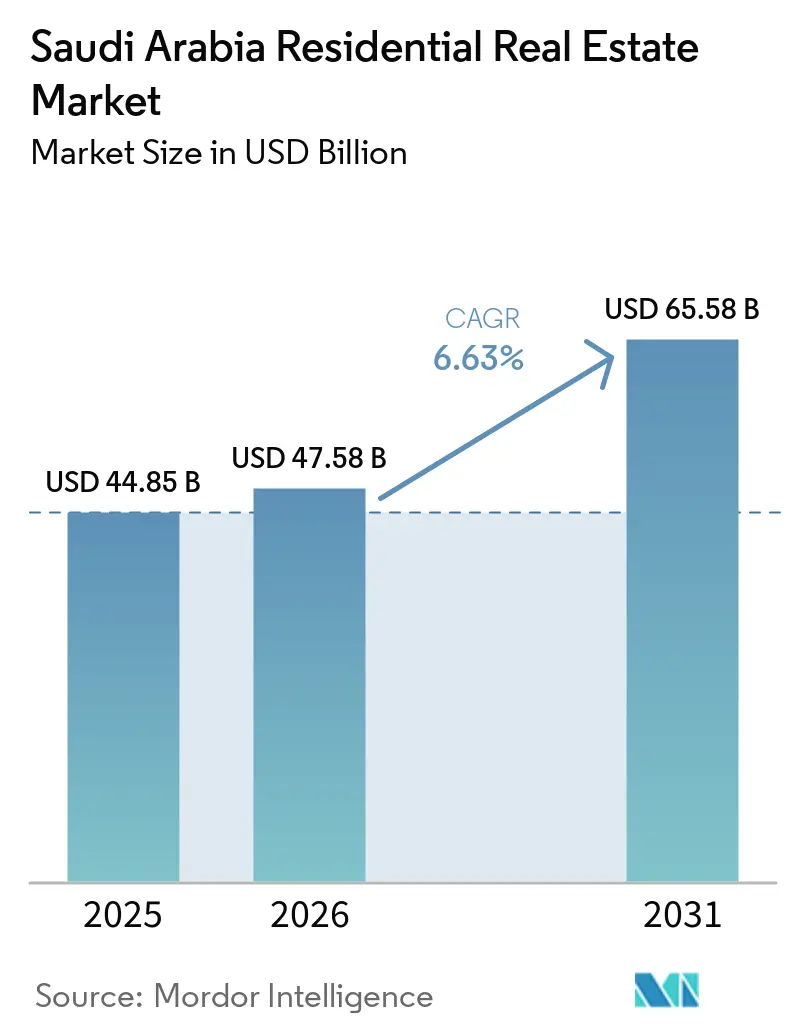

| Base Year Market Size (2025) | USD 44.85 Billion |

| Market Size (2026) | USD 47.58 Billion |

| Market Size (2031) | USD 65.58 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

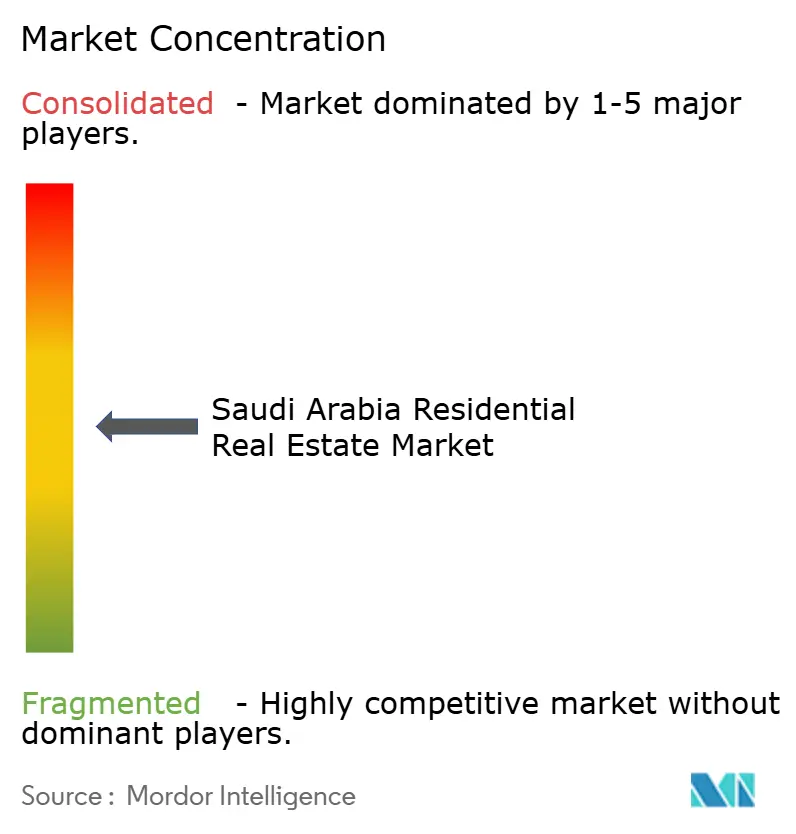

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Residential Real Estate Market Analysis by Mordor Intelligence

The Saudi Arabia Residential Real Estate Market size is expected to increase from USD 44.85 billion in 2025 to USD 47.58 billion in 2026 and reach USD 65.58 billion by 2031, growing at a CAGR of 6.63% over 2026-2031.

Continued government funding under Vision 2030, strong population growth, and rising mortgage liquidity are widening demand-supply gaps and propelling new deliveries. Sales remain the dominant route to homeownership, yet a deepening rental culture is reshaping unit mix, amenities, and lease lengths. Apartments capture the biggest slice of new builds as land in major cities tightens, while affordable housing outperforms on the back of subsidies, lower down-payments, and fast-track approvals. Execution capacity is improving: contract awards for real-estate projects rose 8% year-over-year in H1 2024, and total construction spending reached USD 49.3 billion, underscoring robust pipeline momentum.

Key Report Takeaways

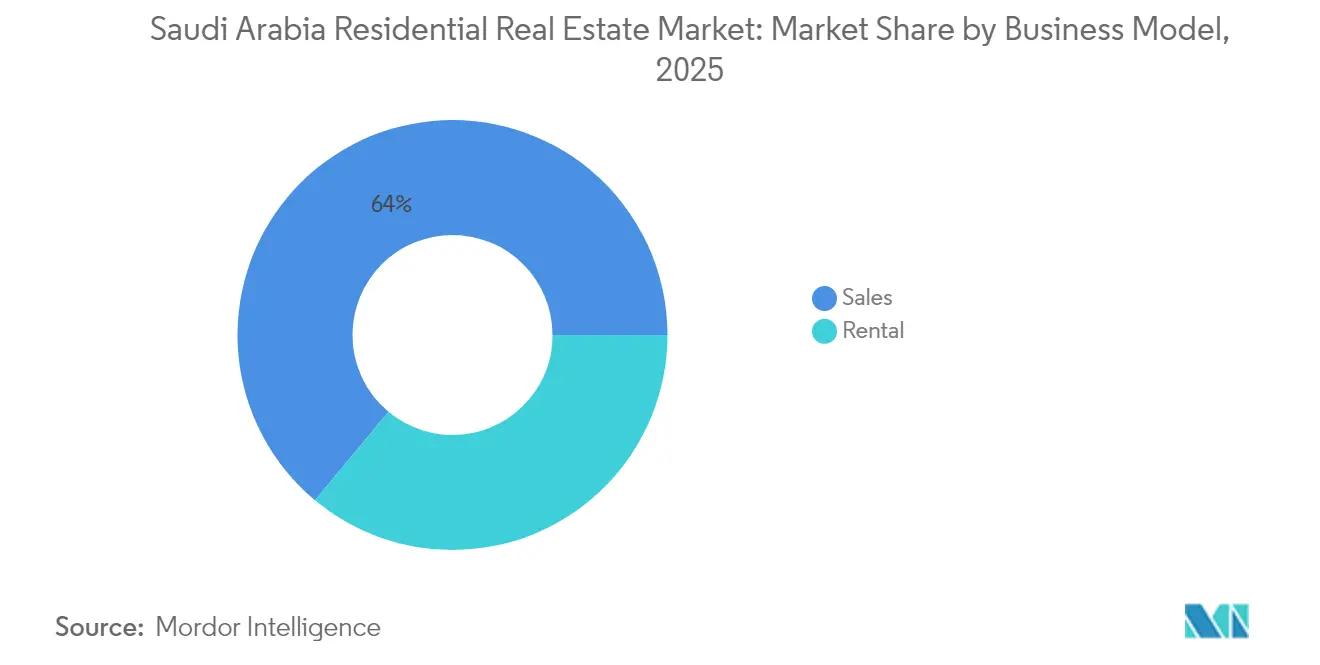

- By business model, sales held 63.95% of the Saudi Arabia residential real estate market share in 2025, while rentals are forecast to post the fastest 7.11% CAGR through 2031.

- By property type, apartments and condominiums captured 52.05% of revenue in 2025 and are advancing at a 7.29% CAGR to 2031.

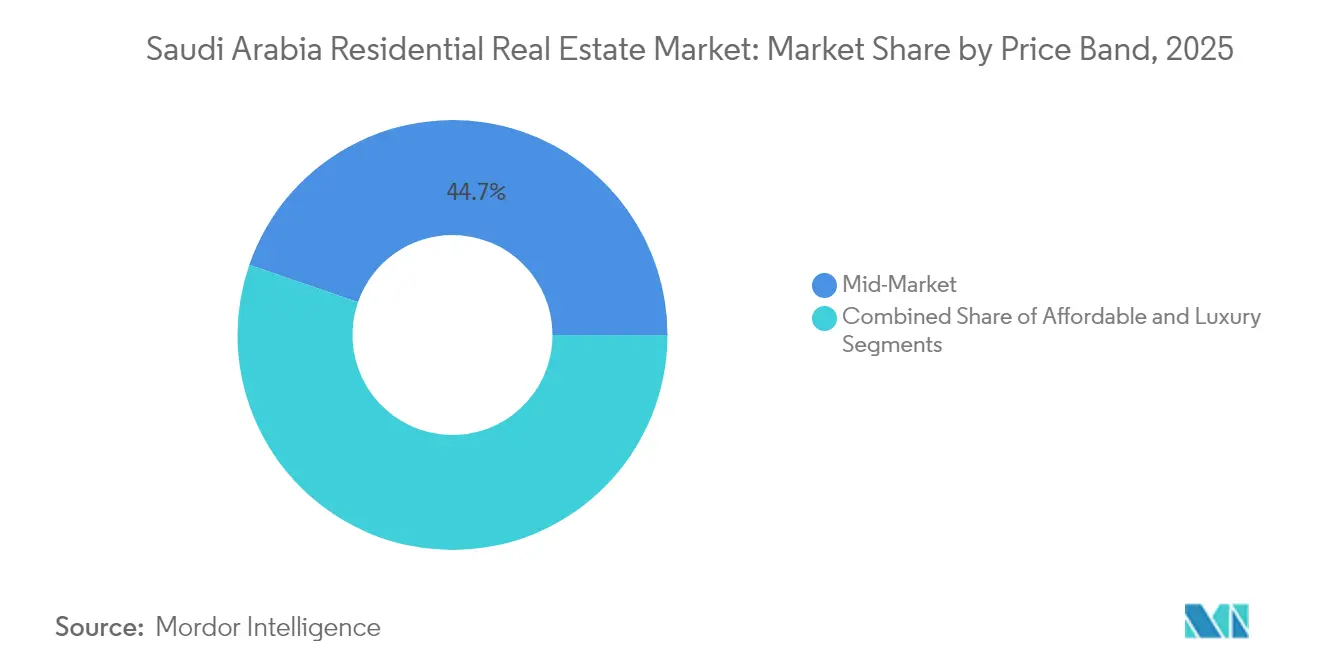

- By price band, mid-market units accounted for 44.70% of revenue in 2025, whereas affordable housing is projected to expand at the highest 7.46% CAGR through 2031.

- By mode of sale, primary transactions supplied 56.10% of revenue in 2025 and are expected to rise at a 7.22% CAGR over the forecast period.

- By city, Riyadh led with 39.85% of national revenue in 2025, while the Dammam Metropolitan Area is set to register the strongest 7.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed housing initiatives under Vision 2030 improving homeownership access | +2.1% | National, with concentrated deployment in major urban centers | Medium term (2-4 years) |

| Persistent housing shortage sustaining demand for new residential projects | +1.8% | National, with acute pressure in Riyadh, Jeddah, DMA | Long term (≥ 4 years) |

| Expanding young population and rising household formation boosting residential demand | +1.5% | National, with higher intensity in Eastern Province and Riyadh | Long term (≥ 4 years) |

| Large-scale urban development and infrastructure projects creating new residential hubs | +1.2% | Riyadh, Jeddah, NEOM, Red Sea coastal areas | Medium term (2-4 years) |

| Growing preference for gated communities and modern apartments in urban centers | +0.9% | Riyadh, Jeddah, DMA metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Backed Housing Initiatives Under Vision 2030 Improving Homeownership Access

Government-backed housing initiatives under Vision 2030 are transforming homeownership opportunities in Saudi Arabia, making it more accessible for citizens. As part of Vision 2030, the government targets a 70% homeownership rate by reducing down-payments to 5% and enhancing mortgage liquidity through securitization. The National Housing Company signed a USD 665 million agreement with China State Construction Engineering to deliver 20,000 housing units, showcasing strong execution capabilities and fostering international collaboration. Additionally, the Saudi Real Estate Refinance Company's USD 906 million portfolio acquisition from Saudi National Bank marked the Kingdom's largest secondary-market transaction, reinforcing investor confidence. Land-release programs and escrow-protected off-plan regulations further support these financing reforms, collectively expanding access to Saudi Arabia's residential real estate market.

Persistent Housing Shortage Sustaining Demand for New Residential Projects

The housing market in Saudi Arabia is grappling with a significant supply-demand imbalance, creating opportunities for new residential developments. Saudi Arabia is projected to require over 800,000 additional homes by 2030, maintaining strong demand across all price segments. However, the planned addition of 300,000 units by 2025 is insufficient to meet the annual household formation rate, particularly in Riyadh, where government hiring is concentrated. This shortfall is most pronounced among mid-income households, driving robust presales even during early construction phases. The Real Estate General Authority is actively ensuring quality compliance and encouraging developers to address underserved areas. These persistent deficits are expected to support long-term stability in the Saudi residential real estate market.

Expanding Young Population and Rising Household Formation Boosting Residential Demand

The residential real estate market in Saudi Arabia is undergoing a significant transformation, driven by demographic and economic shifts. With over two-thirds of the population under 35, the country is experiencing a rise in household formations as graduates secure non-oil jobs. This trend is increasing demand for smaller, amenity-rich apartments in central areas. Young Saudis often begin with rentals, invigorating the leasing market and creating a pathway to homeownership. Rental demand is particularly strong in Riyadh’s financial district and the industrial hubs of the Eastern Province, contributing to the growth of the residential real estate market. Additionally, affordable financing schemes for first-time buyers are enabling transitions into starter homes, supporting absorption across various unit classes[1]KAPSARC Researchers, “Demographic Shifts and Housing Demand,” KAPSARC, kapsarc.org.

Large-Scale Urban Development and Infrastructure Projects Creating New Residential Hubs

Saudi Arabia's urban development initiatives are transforming the residential real estate market, creating vibrant and sustainable communities. Flagship projects such as NEOM, SEDRA, MARAFY, and Diriyah Gate are introducing thousands of walkable, mixed-use residential units. ROSHN plans to deliver 30,000 homes in SEDRA and over 14,000 in MARAFY, integrating heritage with advanced smart-city features. Enhanced transportation corridors are linking these hubs to key job clusters, reducing commute times and increasing land values. Significant contract awards, including Red Sea Global’s USD 175 million build-out, are driving construction activity and employment growth. These developments are extending the economic influence of Saudi Arabia's residential real estate market beyond traditional city centers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction costs driven by material price volatility and labor shortages | -1.4% | National, with acute impact in remote project locations | Short term (≤ 2 years) |

| Economic dependence on oil prices impacting consumer affordability and investor confidence | -1.1% | National, with higher sensitivity in private sector employment regions | Short term (≤ 2 years) |

| Regulatory and approval delays affecting project timelines | -0.8% | National, with concentration in major urban planning jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Construction Costs Driven by Material Price Volatility and Labor Shortages

The construction industry in Saudi Arabia is grappling with escalating costs, driven by material price volatility and labor shortages. In the first half of 2024, cement consumption reached 22.6 million tons, with prices ranging from USD 58.5 to 63.9 per ton, significantly impacting project budgets. Giga-projects exceeding USD 850 billion in value are monopolizing materials and skilled labor, causing delays. Developers in remote areas face higher freight costs, further challenging affordable housing projects. Although local manufacturing is expanding, it will take years to meet demand. Stockpiling and hedging strategies are increasing carrying costs, compressing margins in the Saudi Arabian residential real estate market.

Economic Dependence on Oil Prices Impacting Consumer Affordability and Investor Confidence

The Saudi Arabian economy's reliance on oil prices continues to shape consumer affordability and investor sentiment. Public-sector wages and housing fiscal outlays remain closely tied to oil revenues. Declines in oil prices quickly affect job security and disposable income. In January 2025, housing inflation reached 2%, with villa rents rising by 7.7%, placing pressure on middle-income renters. By June 2024, individual home-loan origination dropped 11% year-on-year to USD 1.41 billion as crude prices softened. Although foreign-ownership levies decreased to 5%, international buyers remain cautious, closely monitoring oil market trends before committing capital. To mitigate the impact of oil price volatility, Saudi Arabia is focusing on diversifying fiscal revenues and advancing mortgage securitization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales Remain Core While Rentals Surge

Sales captured 63.95% of the Saudi Arabia residential real estate market in 2025, reflecting a cultural preference for ownership backed by subsidized mortgages and ample government land grants. Primary transactions often involve off-plan commitments secured through escrow structures that protect buyers and release funds in stages, reinforcing confidence. Developers such as ROSHN have embraced virtual showrooms and instant mortgage approvals to accelerate bookings for large master-planned districts. Meanwhile, the rental channel is forecast to grow at a 7.11% CAGR to 2031, powered by expatriate mobility and the demands of younger Saudis seeking flexible housing near new business districts. Leasing platforms such as Ejari are digitalizing contract issuance and rent collection, increasing transparency and professional management standards across the Saudi Arabia residential real estate market.

Rental growth clusters around Riyadh’s King Abdullah Financial District and the Dammam corridor, where petrochemical employers attract transient engineers. Institutional landlords are emerging; for instance, Sedco Capital is assembling a diversified multifamily portfolio, signaling gradual maturation toward an investable rental asset class. Technology tie-ups—ROSHN’s IoT collaboration with Cisco—support smart-home features that command rental premiums. Sales will continue to dominate value, yet rentals provide a safety valve during economic cycles and complement life-stage housing choices, enriching the overall Saudi Arabia residential real estate market structure.

By Property Type: Apartments Anchor High-Density Expansion

Apartments and condominiums secured 52.05% of revenue in 2025 and led growth with a 7.29% CAGR through 2031, underscoring their primacy in land-constrained metros. The segment excels at delivering scale: multi-story blocks in SEDRA, MARAFY, and ALDANAH yield cost efficiencies that hasten delivery schedules and align with Vision 2030 affordability objectives. Developers increasingly bundle co-working lounges, on-site childcare, and rooftop recreation into apartment complexes, matching evolving lifestyle expectations. Villas still attract extended families, yet escalating plot costs and utility bills are narrowing the affordability gap, steering middle-income buyers toward vertical living.

Demand tailwinds are pronounced in the Saudi Arabia residential real estate market size for apartments, where integrated transit links shorten commutes and align with government sustainability targets. Digital permitting, along with modular construction, is helping domestic firms like Dar Al Arkan trim build cycles by up to 15%. Foreign partners contribute façade engineering, façade cleaning robotics, and energy-efficient glazing systems, broadening unit appeal. With more than 70,000 apartment keys scheduled for handover across major cities by 2027, the segment will remain the centerpiece of new urban development.

By Price Band: Affordable Housing Gains Speed on Policy Tailwinds

Mid-market stock held 44.70% revenue share in 2025, but affordable housing is projected to outpace every other band at a 7.46% CAGR to 2031. The White Land tax, reduced down-payments, and subsidized long-tenor mortgages are converging to lower entry thresholds for households earning between USD 1,600 and USD 2,400 monthly. Projects in Riyadh’s Khuzam area offer units from USD 66,500 and report reservation rates above 75% within weeks of launch.

The Saudi Arabia residential real estate market size for affordable units is benefiting from international cost-reduction know-how: China State Construction Engineering applies precast panels that cut material wastage by 20%. Egyptian builders bring value engineering for interior layouts that comply with local cultural norms yet maximize sellable area. As macroeconomic headwinds persist, affordable housing’s counter-cyclical nature is likely to stabilize developer cash flows and reinforce Vision 2030 social goals.

By Mode of Sale: Primary Pipeline Maintains Top Position

Primary sales controlled 56.10% of 2025 revenue and are expected to expand at a 7.22% CAGR as mega-projects release successive construction phases. Escrow rules enacted in late 2024 channel funds into dedicated project accounts, nurturing trust and accelerating presales for communities such as ALDANAH in Dhahran, where 1,000 units were sold within three weeks of launch. Secondary transactions flourish in mature districts but face limited inventory and renovation overheads that temper growth.

Liquidity initiatives boost the Saudi Arabia residential real estate market size for primary transactions: SRERC securitizations recycle bank capital into new mortgage originations, while digital marketing cuts customer-acquisition costs. Developers incentivize early buyers through staged payment plans and furniture vouchers, ensuring construction drawdowns align with cash inflows. The continual rollout of large-scale phases will likely keep the primary market in pole position for the next five years, while secondary deals serve as a liquidity platform for move-up buyers.

Geography Analysis

In 2025, Riyadh maintained its leadership in the national transaction value, accounting for 39.85%, driven by the presence of government ministries, financial institutions, and headquarters of major giga-projects. The ongoing downtown renewal of New Murabba, along with metro expansions, is fostering the development of mixed-use clusters that integrate workplaces with an increasing housing supply. For instance, ROSHN’s SEDRA project is expected to deliver 30,000 new residences, enhancing product diversity and addressing the backlog of 85,000 potential buyers. High absorption rates have ensured that average delivery periods remain below 14 months, reflecting the operational efficiency of Saudi Arabia's residential real estate market.

Jeddah continues to hold its position as the second-largest market, supported by initiatives such as ROSHN’s MARAFY canal district and tourism-driven submarkets developed by Red Sea Global. Waterfront apartments are experiencing the fastest rental growth, fueled by increased year-round activity from cruise terminals and hospitality venues. The modernization of the port has also boosted logistics employment, and when combined with relaxed foreign-ownership regulations, it has attracted regional professionals seeking both lifestyle benefits and investment opportunities. Jeddah’s combination of cultural heritage and modern infrastructure aligns with Vision 2030’s objectives to diversify the economy, ensuring a steady demand for housing.

The Dammam Metropolitan Area is demonstrating the highest regional growth, with a compound annual growth rate (CAGR) of 7.95% projected through 2031. This growth is being driven by expansions in the petrochemical sector and upgrades to port infrastructure, which are attracting new labor inflows. Master plans such as Aldanah, located near Dhahran, are emerging as key destinations for knowledge workers, particularly those associated with Aramco and its downstream industries. Additionally, new corridors like NEOM and the Red Sea coast are developing into greenfield hubs, supported by renewable energy jobs and high-tech manufacturing. These regions benefit from lower land costs and favorable policy incentives, expanding the geographic scope of Saudi Arabia's residential real estate market while gradually alleviating the pressure on the country’s two largest cities.

Competitive Landscape

The residential real estate market in Saudi Arabia is moderately concentrated. Government-backed developers, ROSHN and the National Housing Company (NHC) are strategically combining land banks, securing concessionary financing, and establishing global partnerships. Through collaborations with Cisco and Naver, ROSHN is integrating smart-city frameworks into its flagship sites, positioning itself as a leader in technology within Saudi Arabia's residential real estate market. Meanwhile, NHC is leveraging secondary-market refinancings to ensure mortgage costs remain affordable and has signed build-operate agreements worth USD 1.33 billion, aimed at strengthening supply chains and fostering growth.

Private companies such as Dar Al Arkan, Al-Akaria, and Sumou Holding are focusing on design innovation and catering to specific market segments. Dar Al Arkan’s USD 57 million villa package within SEDRA highlights partnerships with European architects, appealing to high-income buyers seeking international aesthetics. Similarly, Sumou’s memorandum of understanding with Egypt’s Hassan Allam introduces modular construction expertise, which accelerates project timelines for suburban developments. These collaborations bring in external expertise while effectively managing costs, enhancing the competitiveness of Saudi Arabia's residential real estate sector[3]National Housing Company Press Office, “Digital Twin Agreement with Naver,” NHC, nhc.sa.

Institutional investments are playing a pivotal role in advancing market sophistication. Real estate investment trusts (REITs), such as Jadwa REIT and Sedco Capital REIT, are diversifying into residential blocks, providing developers with guaranteed post-handover leasing and creating viable exit strategies. Additionally, the Saudi Real Estate Refinance Company’s securitization platform is expanding its investor base to include pension funds and insurers, thereby reducing funding costs for originators. In conclusion, the integration of strategic partnerships, digital technologies, and structured financial mechanisms is shaping a dynamic yet moderately concentrated Saudi Arabia residential real estate market.

Saudi Arabia Residential Real Estate Industry Leaders

Roshn

Dar Al Arkan

Saudi Real Estate Co (Alaqaria)

Jabal Omar Development Co

Emaar Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ROSHN and Ajdan Real Estate agreed to build 113 upscale villas in Makkah’s Al Manar community. Spanning 32,921 sq m, the phase feeds into a wider plan for 4,149 homes designed to house more than 17,000 residents.

- May 2025: National Housing Company enlisted China State Construction Engineering to deliver 5,000+ homes in Riyadh’s Murcia project for USD 666.7 million (SAR 2.5 billion). The 2.7 million sq m development bolsters affordable inventory along the capital’s northern corridor.

- May 2025: ROSHN partnered with credit bureau SIMAH to plug real-time credit scores into its digital sales portal, letting buyers gauge eligibility and lock in mortgages faster.

- November 2024: National Housing Company rolled out 11 projects in Riyadh’s fast-growing Khuzam district, unveiling more than 10,000 units that mix modern apartments with upscale villas. Entry prices start at USD 66,700 (SAR 250,000), widening access to quality housing on the capital’s eastern flank.

Saudi Arabia Residential Real Estate Market Report Scope

Residential real estate is an area developed for people to live in. As defined by local zoning ordinances, residential real estate cannot be used for commercial or industrial purposes.

This report aims to provide a detailed analysis of the Saudi Arabian residential real estate market. It focuses on the market dynamics, technological trends, insights, government initiatives taken in the residential real estate sector, and the impact of COVID-19 on the market.

The residential real estate market in Saudi Arabia is segmented by type (condominiums and apartments and villas and landed houses) and key cities (Riyadh, Jeddah, Dammam, and the rest of Saudi Arabia). The report offers the Saudi Arabia residential real estate market size in value (USD) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How large is the Saudi Arabia residential real estate market today?

The sector generated USD 164.85 billion in 2026 and is projected to hit USD 227.12 billion by 2031.

What is driving apartment demand in Saudi cities?

Rapid urbanization, shrinking household sizes, and integrated amenities are steering buyers toward higher-density apartments, which already account for 52.05% of 2025 sales.

How are mortgage reforms helping first-time buyers?

Down-payments fell to 5%, while securitization by the Saudi Real Estate Refinance Company is lowering borrowing costs and widening lender capacity.

Which region is growing fastest for housing?

The Dammam Metropolitan Area leads with a 7.95% CAGR thanks to petrochemical expansions and port upgrades that attract skilled labor.

Why are construction costs a concern for developers?

Cement prices climbed to USD 58.5-63.9 per ton and skilled-labor shortages persist, squeezing margins and extending project timelines.

What role do giga-projects play in the housing outlook?

Developments like NEOM, SEDRA, and MARAFY are adding tens of thousands of units while creating new employment hubs that bolster long-term housing demand.

Page last updated on: