Anti-foaming Agent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

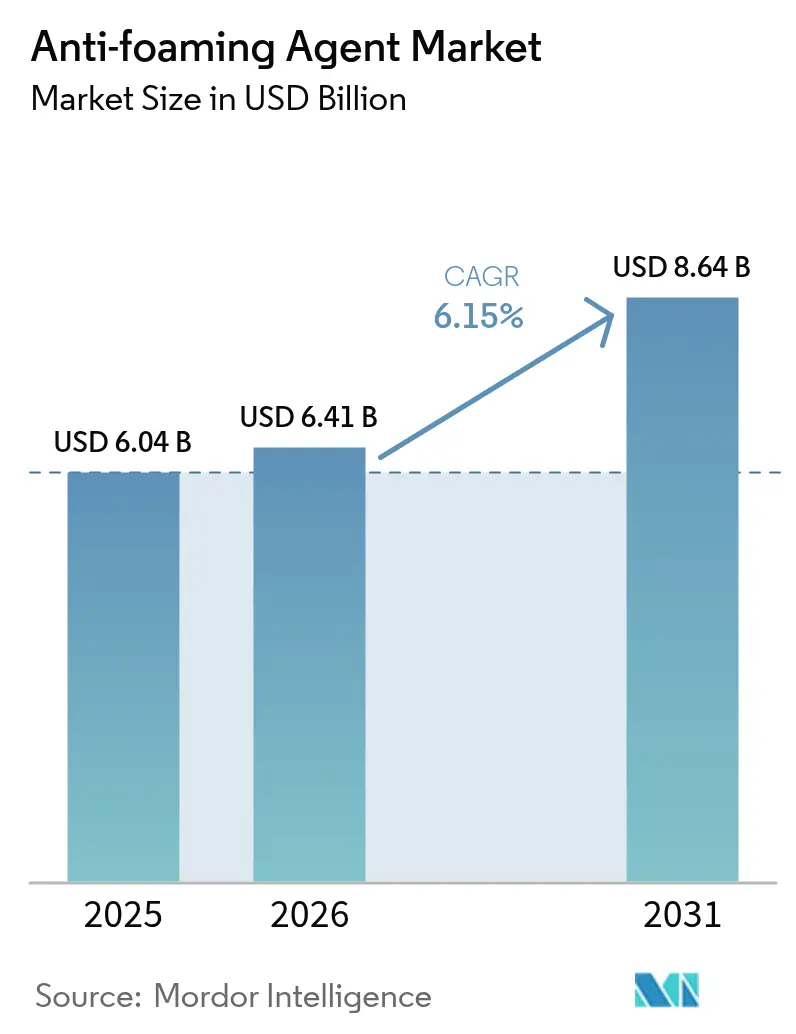

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 8.64 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-foaming Agent Market Analysis by Mordor Intelligence

The anti-foaming agents market size is expected to grow from USD 6.04 billion in 2025 to USD 6.41 billion in 2026 and is forecast to reach USD 8.64 billion by 2031 at 6.15% CAGR over 2026-2031. This growth is driven by increased investments in process-intensive industries, stricter water discharge regulations, and the need to protect high-speed production equipment. Silicone-based chemistries are leading the market due to their ability to maintain surface activity across a wide range of temperatures and pH levels, helping manufacturers reduce the risk of unplanned shutdowns and product rework. In the oil and gas sector, premium anti-foaming agents are being adopted to prevent foam-induced pressure fluctuations during deepwater drilling operations. The pulp and paper industry remains the largest consumer, supported by continuous kraft, oxygen, and bleach-tower processes. Regionally, Asia-Pacific is contributing the highest incremental revenue, with countries such as China, India, and Southeast Asian nations expanding wastewater treatment, beverage production, and textile manufacturing capacities to meet growing consumer demand and comply with environmental regulations. Across all end-use industries, procurement teams are increasingly assessing foam-control performance against evolving restrictions on cyclic siloxanes, mineral oil fractions, and persistent organic pollutants. This shift is encouraging formulators to develop hybrid or bio-based blends that reduce regulatory risks while maintaining operational reliability.

Key Report Takeaways

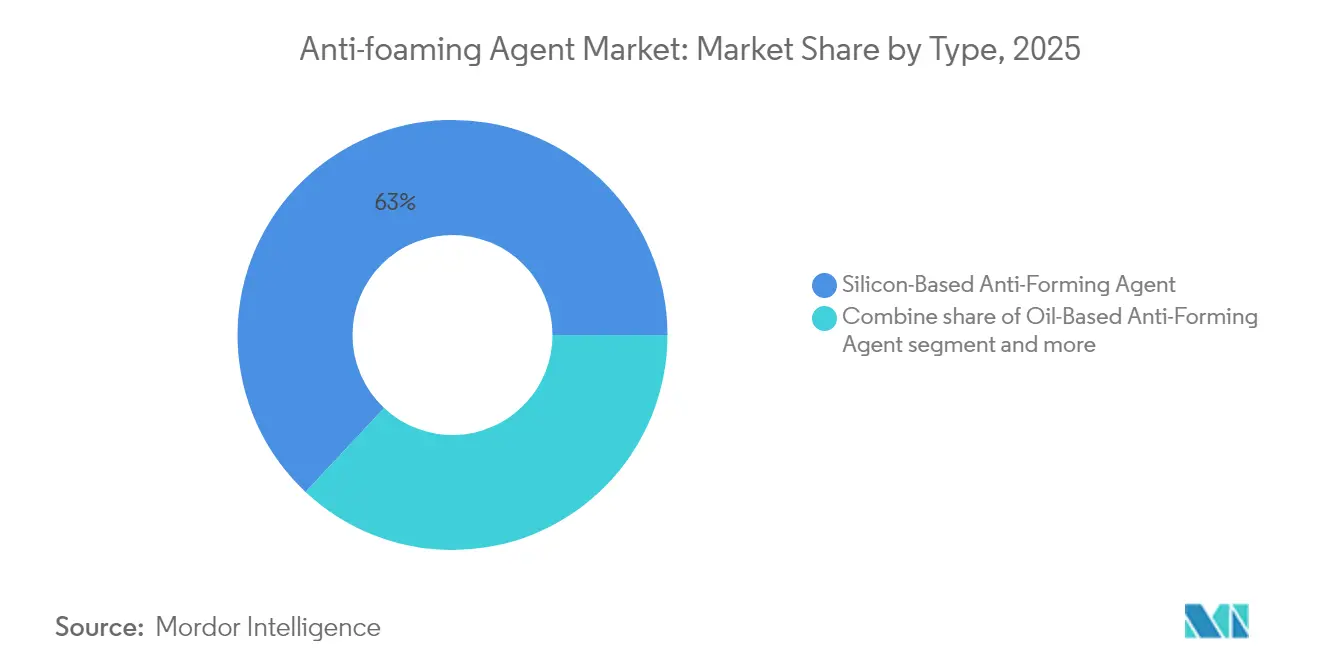

- By type, silicone-based formulations accounted for 63.02% of Anti-foaming Agents market share in 2025 and are on track to register a 7.35% CAGR to 2031.

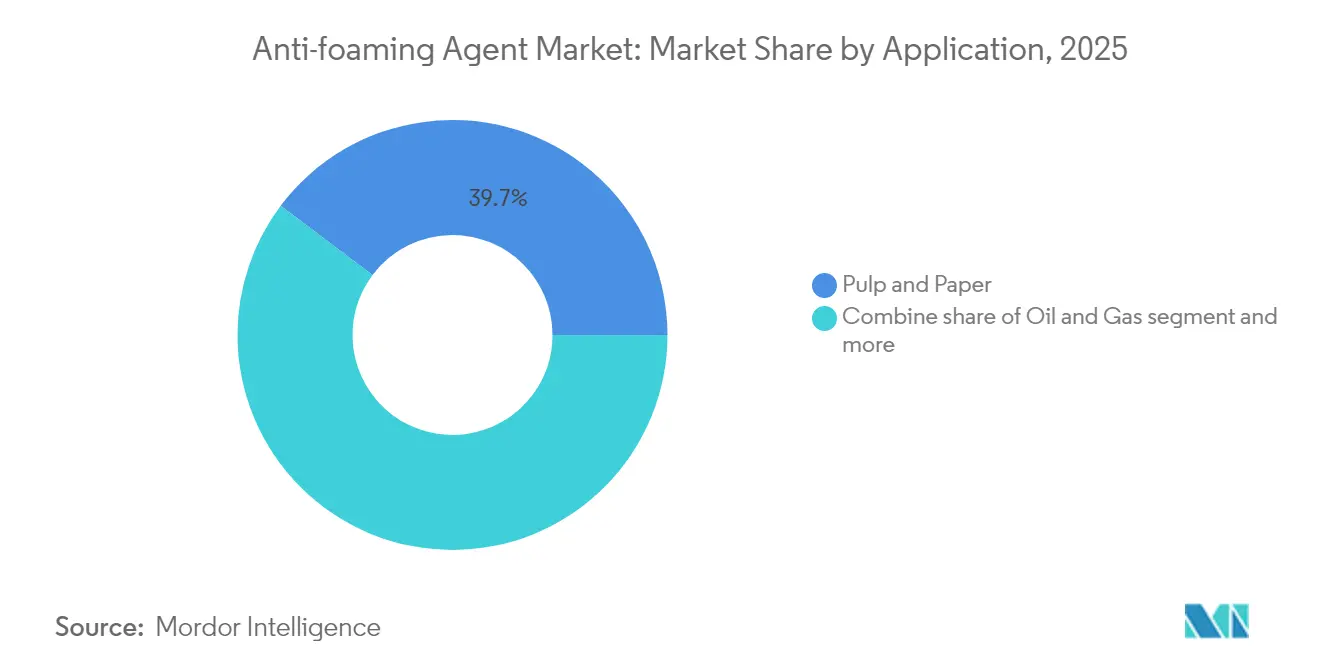

- By application, pulp and paper contributed 39.74% of 2025 revenue, whereas oil and gas usage is forecast to expand at 7.28% a year through 2031.

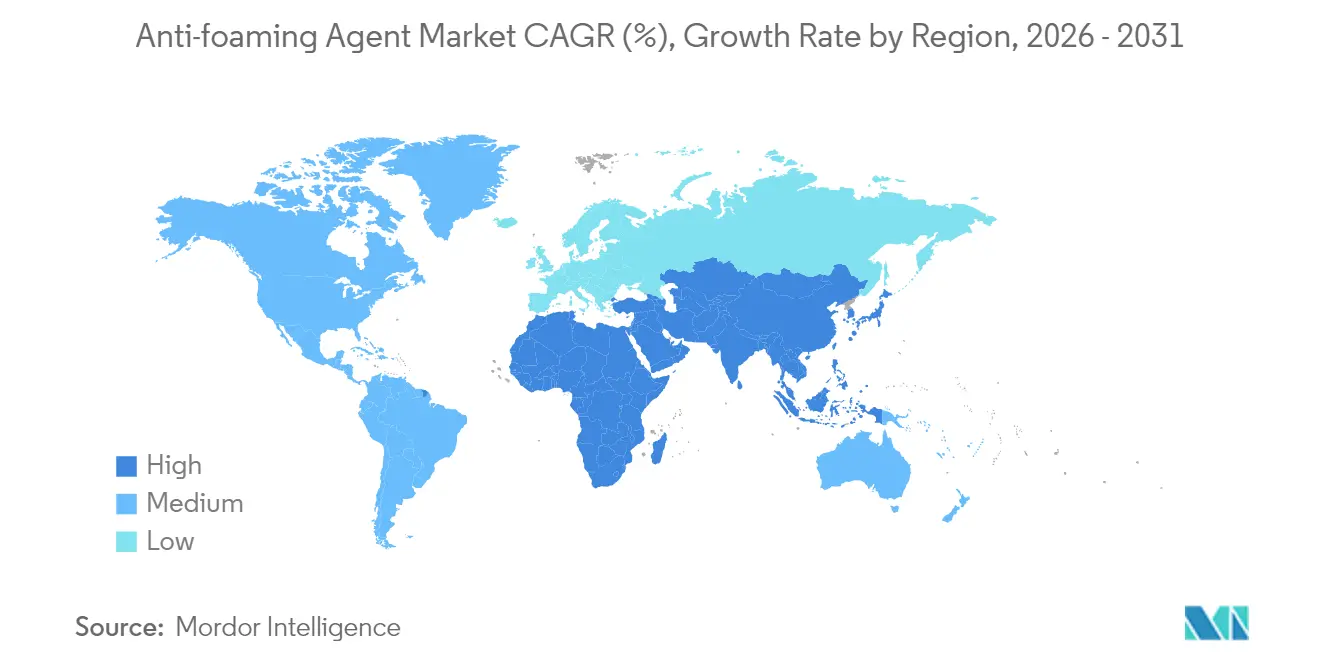

- By geography, Asia-Pacific commanded 37.01% of global sales in 2025 and is projected to post a 7.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-foaming Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of food and beverage processing industries, including brewing, soft drinks, and dairy | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in fermentation-based industries like biotech, enzymes, and biofuels producing foam | +1.4% | North America, Europe, Asia-Pacific core | Long term (≥4 years) |

| Rising wastewater treatment needs in municipal and industrial plants to manage foam | +1.6% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Short term (≤2 years) |

| Demand for enhanced productivity in pulp and paper mills through stabilized operations | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift to high-speed bottling and packaging lines sensitive to liquid foaming | +0.8% | Global, led by North America and Europe | Short term (≤2 years) |

| Technical benefits of silicone-based antifoams, including thermal stability and broad compatibility | +1.3% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of food and beverage processing industries, including brewing, soft drinks, and dairy

Food and beverage manufacturers are adopting higher-capacity fermentation vessels and continuous-flow pasteurizers to address rising per-capita consumption in emerging markets. However, these systems produce more foam per unit throughput compared to traditional batch equipment. Wacker's SILFOAM product line for brewing recommends dosages between 5 and 50 parts per million (ppm) to manage foam during wort boiling and yeast propagation. The product complies with Food and Drug Administration (FDA) 21 CFR 173.340, ensuring no off-flavors are introduced into the finished beer. Dairy processors encounter similar challenges, as ultra-high-temperature sterilization of milk at 135 degrees Celsius to 150 degrees Celsius generates protein-stabilized foam that can clog heat exchangers, reducing thermal efficiency by up to 12 percent if not controlled. Additionally, the growing demand for plant-based beverages such as soy, oat, and almond adds complexity. Vegetable proteins exhibit different foaming behaviors compared to casein, necessitating customized antifoam formulations that ensure effectiveness while meeting clean-label consumer preferences.

Growth in fermentation-based industries like biotech, enzymes, and biofuels producing foam

Biopharmaceutical contract manufacturers are expanding the production of monoclonal antibodies and recombinant proteins using 20,000-liter single-use bioreactors. In these systems, dissolved oxygen transfer relies on fine-bubble aeration, which naturally generates foam. To manage this, Momentive's food-grade silicone emulsions are applied at concentrations of 10 to 100 parts per million (ppm) to collapse foam without affecting cell viability or downstream chromatography processes. Similarly, industrial enzyme producers, such as Novozymes and DSM, use fed-batch fermentation for amylase and protease production. In these processes, foam carryover into off-gas filters can cause backpressure spikes and reduce bioreactor working volume by 15 percent to 20 percent. Biofuel refineries converting lignocellulosic feedstocks into ethanol also face foam-related challenges during enzymatic hydrolysis and simultaneous saccharification-fermentation. In these operations, antifoam costs account for 0.8 percent to 1.2 percent of total variable operating expenses. This cost sensitivity is encouraging formulators to adopt water-based polyether defoamers, which provide acceptable performance at lower costs compared to silicone alternatives. However, re-foaming remains a challenge in high-agitation zones.

Rising wastewater treatment needs in municipal and industrial plants to manage foam

Municipal wastewater plants in China and India are increasing activated-sludge capacity to accommodate growing urban populations. However, foam accumulation in aeration basins and secondary clarifiers disrupts solids settling processes and can lead to effluent non-compliance. The United States Environmental Protection Agency's 2024 guidance on per- and polyfluoroalkyl substances (PFAS) treatment has identified foam fractionation as an emerging method for PFAS concentration, driving demand for antifoams that do not interfere with subsequent granular activated carbon or ion-exchange treatment steps [1]Source: United States, “Environmental Protection Agency (EPA),“Potable Reuse and PFAS,” epa.gov. Industrial wastewater from processes such as textile dyeing, pulp bleaching, and petrochemical cracking contains surfactants and organic acids that stabilize foam. To maintain hydraulic throughput, operators typically dose oil-based or silicone antifoams at concentrations ranging from 20 to 200 parts per million (ppm). In India, the Central Pollution Control Board's 2024 mandate requiring biochemical oxygen demand (BOD) levels below 30 milligrams per liter (mg/L) for textile effluent has indirectly increased antifoam consumption. This is because tighter aeration control necessary to meet BOD targets often results in higher foam generation. Compliance requirements also influence antifoam usage through ISO 14001 environmental management systems, which many multinational operators adopt to standardize defoamer selection across their global facilities.

Demand for enhanced productivity in pulp and paper mills through stabilized operations

Pulp mills operate kraft digesters and bleach towers under alkaline conditions that saponify residual fatty acids, creating persistent foam that reduces effective vessel volume and extends cycle times. Kemira's defoamer portfolio for pulp includes fatty-alcohol ethoxylates and polysiloxane blends dosed at 50 to 500 parts per million (ppm), targeting foam control in brown-stock washing and oxygen delignification stages. Paper machines running at speeds above 1,200 meters per minute experience foam carryover into forming fabrics, which causes sheet breaks and unscheduled downtime. A single break can cost between USD 5,000 and USD 15,000 in lost production and waste fiber. The shift toward recycled-fiber furnishes, driven by sustainability mandates, introduces detergent residues and ink particles that amplify foaming, raising per-ton antifoam consumption by 10 percent to 15 percent compared to virgin-pulp systems. Operators are adopting inline foam sensors and automated dosing pumps to minimize overuse, a trend that favors suppliers offering integrated monitoring solutions alongside chemical products.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict environmental regulations on silicone, mineral-oil, and solvent-based defoamer components | -1.1% | Europe, North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Concerns over aquatic toxicity and bioaccumulation of certain antifoam chemistries | -0.7% | Global, led by Europe and North America | Long term (≥4 years) |

| Lower efficiency of bio-based defoamers compared to conventional silicone-based alternatives | -0.6% | Global, with emphasis on North America and Europe | Medium term (2-4 years) |

| Supply chain disruptions affecting silicone oils, surfactants, and specialty waxes for defoamers | -0.5% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Strict environmental regulations on silicone, mineral-oil, and solvent-based defoamer components.

The European Union's Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) regulation restricts the use of D4, D5, and D6 cyclic siloxanes in wash-off personal care products and is considering similar restrictions for industrial antifoams due to evidence of persistence and bioaccumulation in aquatic sediments [2]Source: The Cosmetic, Toiletry and Perfumery Association, “CTPA Position on a REACH Restriction on the Cyclic Siloxanes D4, D5 and D6 in Leave-On Cosmetic Products,” cpta.org.uk. Suppliers working to comply with these thresholds face research and development costs ranging from USD 500,000 to USD 2 million per product line, with no assurance that alternative chemistries will achieve the same performance levels in high-shear or high-temperature applications. In the United States, the Environmental Protection Agency's review under the Toxic Substances Control Act of certain mineral-oil fractions used in defoamers has delayed new product registrations, leading to supply constraints for oil-based formulations in food-contact applications. Compliance requirements also include International Organization for Standardization (ISO) 14001 and ISO 9001 certifications, which are increasingly mandated by multinational buyers as part of supplier qualification processes [3]Source: International Organization for Standardization, “ISO 9001 and ISO 14001,” iso.org. Smaller regional producers without these certifications risk losing access to Tier-1 accounts. These regulatory challenges are particularly significant for silicone and mineral-oil chemistries, driving increased interest in bio-based alternatives despite their current performance limitations.

Concerns over aquatic toxicity and bioaccumulation of certain antifoam chemistries

Ecotoxicology studies published in 2024 revealed that certain silicone antifoams have LC50 values (lethal concentration for 50% of test organisms) below 10 milligrams per liter (mg/L) for Daphnia magna. This classification under the Globally Harmonized System of Classification and Labelling of Chemicals designates them as hazardous to the aquatic environment. As a result, stricter requirements for labeling, transport, and disposal have been imposed, increasing the total cost of ownership for end users by 5 percent to 8 percent. Concerns about bioaccumulation focus on octamethylcyclotetrasiloxane (D4), which the European Chemicals Agency identified as a substance of very high concern in 2023. Residues of D4 detected in fish tissue from rivers receiving wastewater have led to calls for phase-out timelines similar to those implemented for polychlorinated biphenyls. In response, formulators are increasing the ratio of linear to cyclic siloxanes in emulsions. However, this adjustment reduces foam knock-down speed and requires higher dosages, which partially offsets the intended environmental benefits. Water-based polyether defoamers, which avoid these toxicity concerns, suffer from limited efficacy in non-polar media such as hydrocarbon solvents. This limitation confines their use to aqueous systems and leaves a performance gap in oil and gas drilling fluids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silicone Dominance Anchored by Thermal Resilience

Silicone-based anti-foaming agents accounted for 63.02% of the market share in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 7.35% through 2031, surpassing oil-based and water-based alternatives. This strong market position is due to polydimethylsiloxane's ability to maintain surface activity across a wide temperature range of -40°C to +200°C, which is unmatched by vegetable-oil or mineral-oil chemistries without experiencing thermal degradation. According to Wacker's technical data sheets for SILFOAM SE, viscosities range from 1,000 to 100,000 centistokes, enabling formulators to adjust droplet size and spreading coefficients for varied applications, including high-shear processes like jet-dyeing and low-shear processes such as anaerobic digestion.

Regulatory approvals, including the United States Food and Drug Administration (FDA) 21 Code of Federal Regulations (CFR) 173.340 for food contact, European Union (EU) Regulation 10/2011 for plastics, and National Sanitation Foundation/American National Standards Institute (NSF/ANSI) 60 for potable water, further strengthen silicone's position in risk-sensitive industries such as pharmaceuticals and municipal water treatment.

By Application: Pulp Leads, Oil and Gas Accelerates

The pulp and paper industry accounted for 39.74% of the application share in 2025, highlighting significant antifoam consumption. Kraft mills typically use 200 to 800 grams of antifoam per air-dried metric ton of pulp during the digester, washer, and bleach-tower stages. Kemira offers a range of silicone- and oil-based chemistries designed for specific process stages: fatty-alcohol blends are used for brown-stock washing (where carryover into the bleach stage is acceptable), while pure silicone emulsions are applied in oxygen delignification (where residues could deactivate catalysts). Despite its substantial share, the growth rate of the pulp and paper segment remains below the market average, as mill closures in North America and Europe counterbalance capacity expansions in Southeast Asia and South America.

Oil and gas applications are projected to grow at a compound annual growth rate (CAGR) of 7.28% through 2031, marking the fastest growth among end-use segments. In deepwater drilling, foam forms when gas influx interacts with water-based muds containing surfactant emulsifiers. Uncontrolled foam can reduce hydrostatic pressure, potentially leading to kicks or blowouts. Baker Hughes recommends silicone antifoams at dosages of 0.5 to 2.0 pounds per barrel of mud, with performance validated under American Petroleum Institute RP 13B-1 standards for high-pressure, high-temperature conditions.

Geography Analysis

Asia-Pacific captured 37.01% of global revenue in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 7.6% through 2031, making it the fastest-growing region. In 2024, China's industrial wastewater discharge exceeded 7.5 billion cubic meters, with the textile, chemical, and food-processing industries contributing the majority. The Ministry of Ecology and Environment's effluent standards require biochemical oxygen demand levels below 10 milligrams per liter (mg/L) for municipal plants and 30 mg/L for industrial dischargers. These regulations are pushing operators to optimize aeration systems and adopt antifoams that do not interfere with activated-sludge microbiology. Similarly, India's Central Pollution Control Board tightened its norms in 2024, mandating textile dye houses to limit total dissolved solids in effluent to below 2,100 mg/L. Achieving this target requires multi-stage treatment processes and foam control at both biological and chemical stages.

North America and Europe remain the leading regions in the anti-foaming agent market. However, their growth rates are below the global average due to mill closures in the pulp and paper industry, which represents the largest application segment. In the United States, the Environmental Protection Agency's (EPA) 2024 guidance on per- and polyfluoroalkyl substances (PFAS) treatment is prompting municipal wastewater plants to adopt foam-fractionation systems. These systems concentrate PFAS into smaller waste streams for destruction, necessitating anti-foaming agents that do not co-concentrate with PFAS or foul ion-exchange resins. In Europe, restrictions under the European Union's Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) regulation on cyclic siloxanes have driven reformulations toward linear polydimethylsiloxanes and bio-based alternatives. This transition temporarily constrained supply in 2024, leading to an 8% to 12% increase in spot prices for certain food-grade segments.

Brazil, the largest global exporter of eucalyptus pulp, consumes significant volumes of anti-foaming agents. However, economic instability and currency depreciation periodically impact import demand. In Argentina and Chile, the expansion of lithium-brine processing has increased the need for foam control during solvent extraction. This application could drive localized demand growth if lithium carbonate production scales as anticipated. In the Middle East, petrochemical complexes in Saudi Arabia and the United Arab Emirates utilize anti-foaming agents in ethylene crackers and polyethylene reactors. These facilities prefer high-temperature silicone formulations capable of withstanding process conditions exceeding 180 degrees Celsius. Meanwhile, in Nigeria and Egypt, investments in municipal wastewater infrastructure are creating opportunities for cost-effective oil-based and water-based anti-foaming agents. However, procurement in these regions often depends on funding from development-finance institutions, which can involve lengthy approval cycles lasting several years.

Regulatory Landscape

Anti-foaming agents used in food processing are regulated as food additives or processing aids with positive lists and quantitative limits that vary by jurisdiction. In the United States, 21 CFR 173.340 permits defoaming agents such as dimethylpolysiloxane with specified limitations, including a 10 ppm limit in ready-to-consume foods, with additional pathways for ingredients listed as GRAS under 21 CFR Part 182. In the European Union, Regulation (EC) No 1333/2008 governs food additives and includes antifoaming agents on the Union lists (Annexes), and the consolidated text current as of February 2026 anchors compliance for manufacturers supplying across member states and for UK operators aligning to retained EU-derived requirements.

Regulatory data requirements are tightening alongside substance-specific scrutiny, influencing both formulation design and dossier strategies. EFSA issued updated guidance in January 2026 on scientific data requirements for food additive applications, applicable to submissions from 20 July 2026, raising the bar for toxicology and exposure evidence. Outside the EU and US, national standards add further concentration caps, for example Japan's Standards for Use of Food Additives (updated November 2024) restrict silicone resin as an antifoaming agent to 0.050 g/kg, reinforcing the need for region-specific labels, residue testing, and documentation across global supply chains.

Value Chain Analysis

The value chain starts with upstream feedstocks spanning silicone intermediates (for polydimethylsiloxane-based antifoams), petrochemical-derived oils and solvents, and bio-based inputs such as fatty acids, esters, and renewable polyols. Integrated chemical producers with silicone value chains supply key base fluids, while specialty formulators convert these into emulsions, dispersions, and powders tailored to end-use conditions (temperature, shear, and pH) and to food-contact constraints. Regulatory compliance is embedded early in product development because food-use antifoams must align with frameworks such as 21 CFR 173.340 in the United States, Regulation (EC) No 1333/2008 in the European Union, and Codex GSFA references used by many import markets.

Midstream activities center on formulation, quality management, and packaging suited for industrial dosing, followed by distribution through global chemical distributors and local ingredient specialists that provide application support at customer sites. Distributors such as Brenntag SE, IMCD Group, and Univar Solutions play a key role in regional reach and technical service, while direct supply is common for multinational accounts with harmonized specifications (often linked to ISO 9001/ISO 14001 procurement requirements). Downstream, end users include breweries, dairy and plant-based beverage processors, fermentation and bioprocessing plants, and industrial wastewater operators, where performance verification, residue control, and supply continuity for silicone oils and surfactants are recurring procurement considerations.

Competitive Landscape

The Anti-foaming Agents Market demonstrates moderate fragmentation with a notable concentration of key players. Companies such as BASF, Dow, and Wacker benefit from backward integration into silicone-intermediate production, ensuring a stable raw material supply and capturing margins across multiple stages of the value chain. For example, BASF's Ludwigshafen facility produces both chlorosilanes and finished antifoam emulsions, enabling flexible production adjustments to meet demand fluctuations and mitigating exposure to spot-market volatility in dimethyldichlorosilane pricing.

Regional players in Asia-Pacific and Latin America primarily compete on price for commodity applications such as pulp washing and construction aggregates, where performance differentiation is minimal, and buyers focus on the delivered cost per ton of foam suppressed. Opportunities for innovation lie in hybrid chemistries that combine the thermal stability of silicones with the regulatory compliance of bio-based surfactants. Evonik's polyether-modified siloxanes exemplify this approach, catering to users balancing efficacy with environmental compliance requirements. Emerging technologies include enzyme-based defoamers that catalytically degrade foam-stabilizing proteins, gaining traction in food and bioprocessing industries where residue carryover into finished products is unacceptable.

Additionally, smaller firms are introducing inline foam-sensing and automated-dosing systems, which reduce antifoam consumption by 10% to 20%, shifting value creation from chemical sales to equipment and software subscriptions. Patent filings in 2024 highlight advancements in nanoparticle-stabilized emulsions and stimuli-responsive polymers that activate only when foam exceeds a specific threshold height, minimizing overuse and environmental discharge. Compliance with standards such as International Organization for Standardization (ISO) 9001 for quality management and ISO 14001 for environmental management is increasingly critical, as multinational buyers mandate these certifications. Suppliers without these accreditations risk exclusion from Tier-1 procurement processes, leading to a concentration of market share among certified players, even as the overall number of participants remains high.

Anti-foaming Agent Industry Leaders

BASF SE

Dow Inc.

Evonik Industries AG

Wacker Chemie AG

Ashland Global Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory change and buyer qualification practices create whitespace for suppliers that can simplify global compliance without compromising foam-control performance. EFSA's updated food additive application data requirements (issued January 2026, applicable to submissions from 20 July 2026) elevate the value of robust toxicology and exposure packages, encouraging reformulation work that reduces reliance on higher-risk components while staying within established permissions such as 21 CFR 173.340 in the United States and Regulation (EC) No 1333/2008 in the European Union. Japan's November 2024 update to its Standards for Use of Food Additives, including a 0.050 g/kg limit for silicone resin as an antifoaming agent, further supports multi-region product portfolios with tightly controlled residuals and harmonized documentation.

Operational efficiency programs in process industries support opportunities beyond the chemical itself, particularly in dosing optimization and process monitoring that cut overuse while maintaining throughput. In pulp and paper and other continuous operations where foam events translate into downtime, adoption of inline foam sensors and automated dosing systems aligns with procurement focus on total cost of ownership and auditability. A second opportunity track is silicone-free and bio-based antifoams for food and beverage processes where clean-label positioning and component scrutiny influence ingredient selection, providing room for suppliers to scale vegetable-oil, fatty-acid-ester, or polyether-based alternatives alongside validated silicone systems for demanding high-shear applications.

Recent Industry Developments

- May 2026: Evonik announced that TEGO Foamex 8051 received the Ringier Coating Innovation Award, highlighting performance positioning for mineral-oil-free defoaming in waterborne systems. The recognition supports product pull-through in industries that mirror food and beverage requirements for low-use-level efficacy and tighter ingredient scrutiny, reinforcing premiumization around higher-performing, lower-residue formulations.

- July 2025: TER Group expanded its partnership with Momentive to include distribution of Momentive food and beverage foam control solutions across 14 European countries. The agreement strengthened regional availability and technical service coverage for food-grade antifoams, tightening competition for local suppliers that lack a comparable application-support network.

- February 2024: DIC Corporation launched a PFAS-free antifoaming agent for EV lubricating oils, positioned as equivalent in performance to conventional PFAS-containing products with high-temperature and shear stability. The launch reflects broader reformulation pressure around persistent chemistries and provides a reference point for PFAS-avoidance strategies that can influence adjacent antifoam development and qualification approaches in other regulated end uses.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers chemical additives used to prevent foam formation or break down foam during industrial processing, where foam can reduce throughput and product quality. The sizing is tracked in value terms across major process industries that routinely need foam control.

Scope exclusions: Excludes mechanical foam control equipment and services, and it also excludes broader surfactant packages unless the anti-foaming function is the priced component.

Segmentation Overview

- By Type

- Silicon-Based Anti-Forming Agent

- Oil-Based Anti-Forming Agent

- Water-Based Anti-Forming Agent

- By Application

- Pulp and Paper

- Paints and Coatings

- Food and Beverages

- Oil and Gas

- Water and Waste-water Treatment

- Pharmaceuticals and Bioprocessing

- Detergents and Cleaning Chemicals

- Textiles and Leather

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Thailand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the market boundaries and build the first demand map around the main foam-generating processes. We referenced public sources such as US EPA wastewater and effluent guidance, Eurostat and UN Comtrade trade statistics, FAO and national agriculture statistics (for crop processing inputs), and USGS and government industrial output series where relevant, which helped anchor activity levels tied to foam control needs.

To translate activity into demand signals, we reviewed technical publications and standards sources, including peer-reviewed chemistry and process-engineering journals, plus trade association materials for pulp and paper, coatings, and food processing. Company annual reports, investor presentations, and reputable press were also used to cross-check product focus and regional exposure. Where needed, we used a paid subscription for company financials and a patent database selectively to validate supplier intensity and technology shifts. These are illustrative sources only, and many other public references were reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how anti-foaming agents are specified and purchased across key end users, and then aligning the model to real buying patterns. We spoke with a mix of manufacturers, distributors, and downstream formulators, as well as plant-level users across APAC, EMEA, and the Americas. This helped confirm use rates, typical application dosing ranges, and how price changes by chemistry and compliance requirements.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 42% |

| Mid tier: 42% | Functional/Unit leaders: 41% | EMEA: 35% |

| Smaller Players: 19% | Managers: 43% | Americas: 23% |

Market-Sizing & Forecasting

The core model starts with a top-down reconstruction where end-use output and processing intensity are converted into a foam-control demand pool, and then filtered by typical anti-foaming agent use rates in each process. We built the market by linking demand to a few practical drivers, including wastewater treatment throughput, pulp and paper production, paints and coatings output, food and beverage processing volumes, and oil and gas processing activity, and then we applied chemistry-level price ranges to translate the demand into value.

To keep totals realistic, the results were corroborated with selective bottom-up approximations. This included rolling up a sample of supplier revenues exposed to defoamers, checking distributor channel splits, and validating implied average selling prices against the price bands discussed in interviews. Where bottom-up coverage was incomplete, gaps were handled through conservative scaling based on regional production footprints and confirmed application mix shares, before totals were adjusted to avoid double counting across overlapping end uses.

Forecasts were developed using scenario analysis supported by trend-based smoothing. The key variables were projected using published industrial outlooks and then stress-tested through expert views on regulatory pressure on certain chemistries, substitution toward hybrid or bio-based blends, and the pace of capacity additions in high-growth regions. The final forecast was kept traceable to the same demand indicators used in the base year, so changes in volume drivers and price progression can be explained clearly.

Data Validation & Update Cycle

Validation is done in layers so that one data point does not steer the outcome on its own. Model outputs are checked against independent signals like trade flows for relevant additive categories, upstream feedstock movements that influence pricing, and the implied consumption per unit of output in the major end-use processes, and then anomalies are reviewed until the variance is understood.

Before sign-off, assumptions are rechecked through follow-up calls when the model shows sudden shifts by region or chemistry that are not supported by the demand indicators. Reports are refreshed annually, and interim revisions are triggered when material events occur, such as major regulatory actions, sharp input cost changes, or visible capacity moves. Right before delivery, an analyst runs a final update pass so the client receives the most current view available.

Mordor Intelligence's Antifoaming Agent Market Estimate Compared With Other Published Estimates

Published market numbers for anti-foaming agents can look far apart even when they point in the same growth direction, because the study boundaries are not always aligned. Differences usually come from what is counted as an anti-foaming agent versus a broader foam-control additive set, plus how each model treats end-use overlap and price assumptions.

By tracking application-level dosing ranges and price bands by base chemistry, and then checking them through interviews, Mordor Intelligence keeps the 2026 value tied to a defined set of anti-foaming agent sales rather than a wider mix of foam-control products.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.41 B (2026) | |

| Industry Publisher A | USD 5.83 B (2025) | Uses a different base year and tends to describe the space as foam-control additives in process fluids, which can shift what is included and how pricing is applied across types and applications. |

| Research Publisher B | USD 6.87 B (2024) | Starts from an earlier base year and layers in broad segmentation (including form factors and wide end-use buckets), which can raise overlap risk if end-use boundaries and conversion assumptions are not normalized. |

The spread in the table is largely explained by base-year choice and how tightly the product scope is defined, especially around overlaps with adjacent foam-control additives and how prices are progressed by chemistry. With a model that links value to clear industrial activity indicators, and then rechecks those assumptions with practitioners, we can explain each step and keep the final number repeatable year after year.

Key Questions Answered in the Report

How large is the Anti-foaming Agents market in 2026?

It stands at USD 6.41 billion and is on course to reach USD 8.64 billion by 2031.

Which product type leads sales?

Silicone-based grades deliver 63.02% share and post the fastest 7.35% CAGR through 2031.

What end use will grow the quickest?

Oil and gas applications expand at 7.28% yearly, propelled by deepwater and high-temperature drilling.

Why is Asia-Pacific critical for suppliers?

The region contributes 37.01% of revenue and advances at a 7.6% CAGR owing to tighter wastewater norms and manufacturing expansion.

Page last updated on: