United States Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

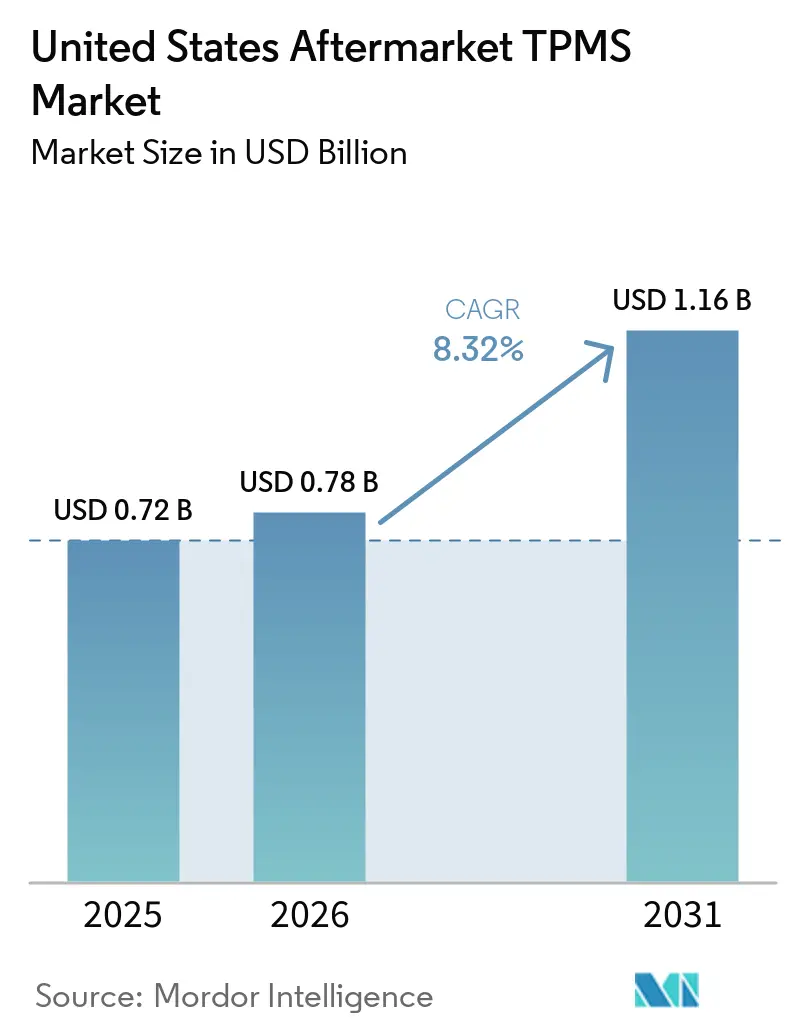

| Base Year Market Size (2025) | USD 0.72 Billion |

| Market Size (2026) | USD 0.78 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Aftermarket TPMS Market Analysis by Mordor Intelligence

The United States aftermarket TPMS market size is expected to grow from USD 0.72 billion in 2025 to USD 0.78 billion in 2026 and is forecast to reach USD 1.16 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031). Rising enforcement of FMVSS 138, a swelling pool of first-generation sensors now reaching the end of life, and widening e-commerce access to universal sensors underpin this expansion. Tightening state vehicle-inspection regimes elevates replacement urgency, while programmable dual-frequency sensors reduce installer inventory costs and broaden do-it-yourself uptake. Competitive activity remains steady as leading suppliers invest in domestic tool training and firmware updates, yet price compression from counterfeit imports constrains installer margins. Early signals from smart-tire demonstrations hint at longer-term technology disruption that could reshape sensor-replacement economics.

Key Report Takeaways

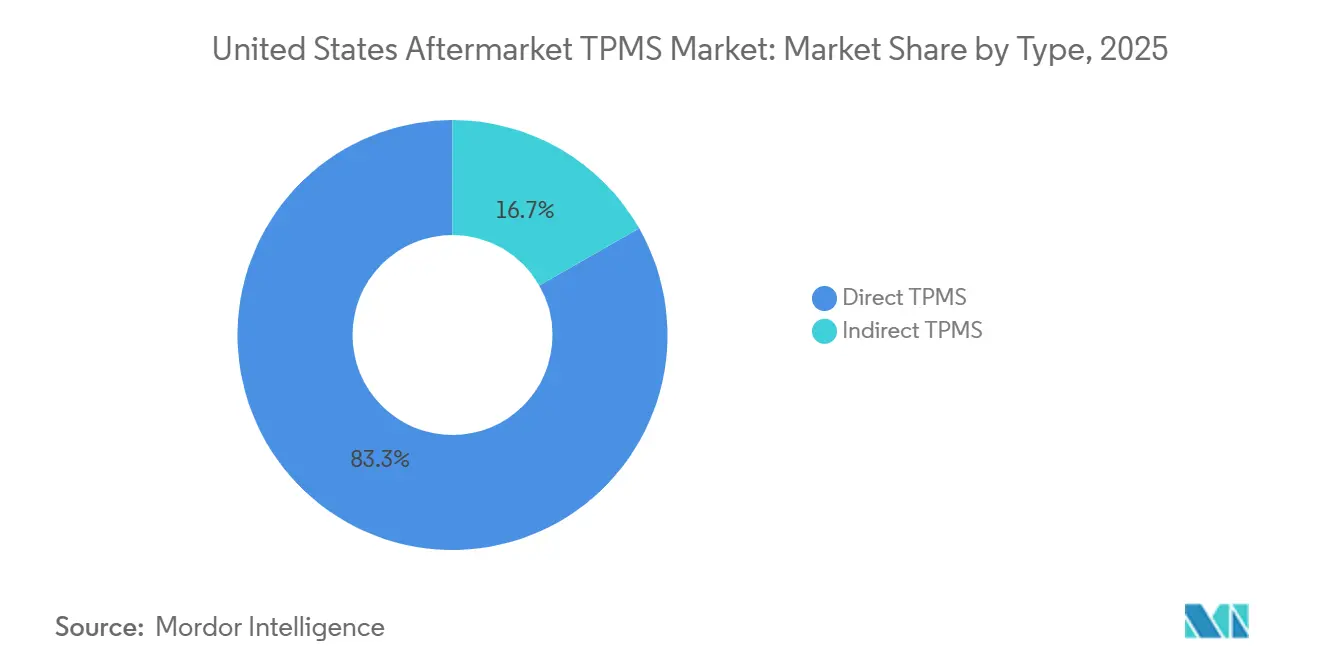

- By TPMS type, direct TPMS led with 83.26% of the United States aftermarket TPMS market share in 2025, while indirect TPMS is forecast to grow fastest at an 8.56% CAGR through 2031.

- By technology integration, stand-alone TPMS units accounted for 64.15% of the United States aftermarket TPMS market share in 2025, whereas smart / connected TPMS is projected to expand at an 8.37% CAGR to 2031.

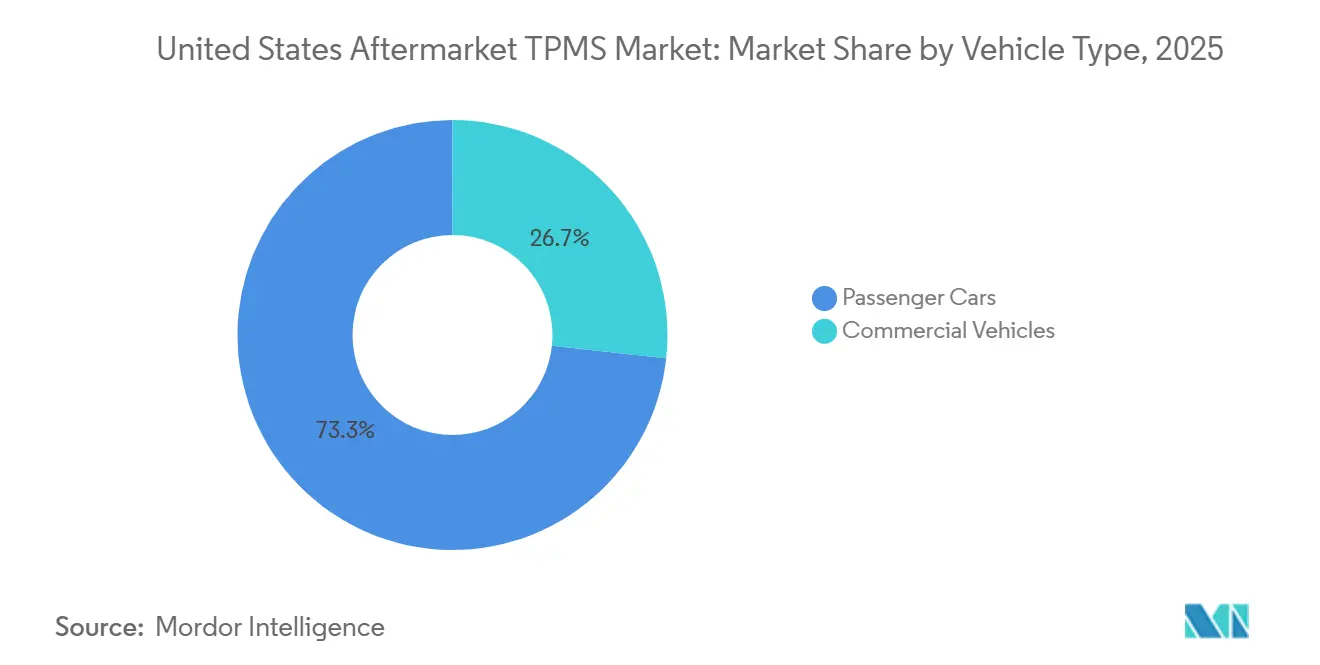

- By vehicle type, passenger cars held 73.28% of the United States aftermarket TPMS market share in 2025; commercial vehicles recorded the highest projected growth at an 8.55% CAGR over 2026-2031.

- By distribution channel, offline outlets captured 76.51% of the United States aftermarket TPMS market share in 2025, yet online sales are advancing at an 8.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with United states being one of the contributors. Our global aftermarket tpms market size represents that cumulative total.

United States Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated TPMS Replacement Interval | +2.1% | National | Medium term (2-4 years) |

| Surging E-commerce Volumes | +1.8% | National, concentrated in suburban markets | Short term (≤ 2 years) |

| Growing Fleet Telematics Retrofits | +1.4% | National, early adoption in logistics hubs | Medium term (2-4 years) |

| Rise in ADAS Recalibration Bundling | +1.2% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Insurance-linked Discounts | +0.9% | National, pilot programs in select states | Long term (≥ 4 years) |

| Lithium-free MEMS Pressure-Sensor Breakthroughs | +0.8% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FMVSS 138 Enforcement and Sensor Replacement Cycles

FMVSS 138 mandates a per-wheel warning when tire pressure drops significantly below placard levels, solidifying the dominance of direct TPMS in new vehicles. Sensors from the first wave are now outlasting their sealed lithium batteries, leading to a replacement demand that's independent of regular tire service events. A recent recall affecting Tesla's Model 3 and Y underscores the compliance scrutiny nudging owners to promptly service sensors. In states like New York, Pennsylvania, and Texas, inspection programs automatically flag non-functional TPMS, turning regulatory non-compliance into instant aftermarket sales. Legislators, under the FAST Act mandate, are delving into tamper-resistant architectures, eyeing potential rulemaking that could redefine future service protocols[1]“Federal Motor Vehicle Safety Standard 138,” National Highway Traffic Safety Administration, nhtsa.gov.

E-commerce Expansion for DIY TPMS Sensors and Diagnostic Tools

Amazon's marketplace highlights a surge in online sales for a relearn tool and GM-compatible sensors, underscoring rapid online penetration [2]“Tire Pressure Monitor Sensor Listings,” Amazon, amazon.com. Universal sensors, like Alligator’s Sens.it RS+, cover nearly all vehicles. These sensors receive firmware updates through web-connected tools, allowing repair shops to significantly reduce their OEM-specific inventory. While these cost savings attract consumers, the de minimis threshold means many small parcels can skip federal inspection, heightening the risk of counterfeits, a concern noted by U.S. Customs. This dynamic presents both growth opportunities and quality-control hurdles for installers.

Fleet Telematics Retrofits Among Light Commercial Vehicle Operators

Light commercial fleets integrate TPMS data into existing telematics dashboards to curb fuel spend and cut unscheduled tire downtime. Real-time pressure analytics enable predictive scheduling to avoid roadside failures and extend casing life. Suppliers packaging sensors with cloud dashboards win sticky fleet contracts with multi-year service fees. Logistics hubs in states such as Texas and Illinois are seeing early adoption, raising the technology bar for independent tire shops that serve last-mile operators.

Insurance-Linked Discounts for Connected-TPMS Adoption

Real-time tire data integration in usage-based insurance pilots is recalibrating risk models, enabling fleets to sidestep blowouts that typically incur significant liabilities and downtime costs. With the aid of connected sensors, operators receive alerts when tire data dips below a certain threshold, empowering them to act before breaching FMVSS violation points. While radio-frequency interception raises privacy concerns, manufacturers are proactively embedding encryption that aligns with new cybersecurity standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Sensor ASPs Squeezing Installer Margins | -1.6% | National, acute in competitive metro markets | Short term (≤ 2 years) |

| Increasing Competition from Low-Cost Chinese Clones | -1.3% | National, concentrated in price-sensitive segments | Medium term (2-4 years) |

| Technical Skill Gap | -1.1% | National, severe in rural and small-town markets | Medium term (2-4 years) |

| EV Solid-State Tires with Embedded Self-Inflation Tech | -0.7% | National, early adoption in premium EV segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Sensor ASPs Squeezing Installer Margins

Aftermarket sensor prices have decreased significantly. Once priced higher at OEMs, they now include programmable units and budget generics at much lower costs. Installers, with an industry-average service ticket, find it challenging to maintain profits after accounting for parts and labor. This challenge is further intensified by the availability of affordable DIY relearn tools, which enable savvy owners to bypass professional assistance. While high-volume tire chains utilize their purchasing power and cross-sell tires to counteract shrinking sensor margins, single-location shops face tighter profit margins.

Technical Skill Gap at Independent Repair Shops

A recent poll by the Tire Industry Association found that many technicians failed to update the firmware on their TPMS tools. With the rapid introduction of new Bluetooth-enabled sensors and manufacturer-specific relearn sequences, these outdated tools often lead to service comebacks and dissatisfied customers. While training sessions from tool companies like Bartec and Autel strive to bridge this knowledge gap, technicians in rural areas remain significantly behind their counterparts in affluent metropolitan regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct Systems, Anchor Compliance, and Data Accuracy

Direct systems captured 83.26% of the United States aftermarket TPMS market share in 2025, owing to FMVSS 138’s per-wheel accuracy requirements, securing the largest share of the United States aftermarket TPMS market. Indirect solutions, reliant on ABS wheel-speed comparisons, held 16.74% yet may grow 8.56% CAGR through 2031 among cost-sensitive light-commercial fleets.

Direct technology continues to adopt Bluetooth LE and remote firmware updates, shifting revenue emphasis from hardware units to software subscriptions. Indirect options remain limited by their inability to detect simultaneous pressure loss or stationary leaks, relegating them to a secondary role to direct sensors in compliance-driven environments.

By Technology Integration: Connected Platforms Monetize Data

Stand-alone configurations accounted for 64.15% of the United States aftermarket TPMS market share in 2025, but are now in gradual decline as fleets adopt connected platforms aligned with ISO 15638-23. Smart solutions are projected to outpace overall growth with an 8.37% CAGR through 2031.

Logistics operators harness cloud analytics for maintenance scheduling, reporting a significant drop in unplanned tire failures. Upgraded encryption addresses privacy issues highlighted in academic studies, rendering connected TPMS (Tire Pressure Monitoring Systems) more palatable for insurance underwriting and corporate compliance teams.

By Vehicle Type: Commercial Fleets Power Future Units

Passenger cars generated 73.28% of the United States aftermarket TPMS market share in 2025, supported by the vast legacy fleet. Commercial platforms, however, are growing at an 8.55% CAGR and will capture a larger share of the United States aftermarket TPMS market by 2031.

Light-commercial vans drive the most volume, leveraging TPMS telematics bundles for 5% fuel savings. Heavy trucks and articulated buses add double-digit sensor counts per vehicle and face FMCSA roadside inspections that increasingly reference TPMS operability, ensuring steady pull-through demand.

By Distribution Channel: Omnichannel Dynamics Take Hold

Offline outlets still accounted for 76.51% of the United States aftermarket TPMS market share in 2025. Still, online marketplaces posted the highest growth at 8.59% CAGR through 2031, aided by universal sensor listings and low-cost tools. The United States aftermarket TPMS market share of digital channels will expand as broadband and consumer familiarity rise.

Tire-service chains respond by bundling complimentary sensor resets with tire purchases, defending traffic from e-commerce players. Meanwhile, independent garages embracing subscription-based programming tools position themselves as trusted installers for customers wary of counterfeit products online.

Geography Analysis

States with the largest registered-vehicle bases lead the demand. California, Texas, and Florida, with significant numbers of vehicles and stringent inspection programs that penalize cars with TPMS warning lamps, together account for a substantial share of the nation's aftermarket revenue.

California's battery-electric vehicles highlight the critical role of sensors; accurate pressure can extend driving range per charge. In Texas, large commercial fleets based near Dallas-Fort Worth are proactive in replacing sensors to sidestep FMCSA out-of-service citations[3]“Vehicle Registration Statistics 2025,” California Department of Motor Vehicles, dmv.ca.gov.

E-commerce penetration skews towards coastal regions. Amazon and RockAuto dominate, capturing a notable share of sensor sales in California, New York, and New Jersey. In contrast, rural states in the Great Plains remain largely offline, hindered by limited broadband access and a hesitance to undertake complex DIY automotive repairs. Enforcement of inspections varies: New York, Virginia, and Pennsylvania's annual mandates create predictable replacement cycles, while tire service events primarily drive demand in South Dakota and Wyoming.

Coverage of the aftermarket tpms market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for China, India, South Korea, and Japan, each shaped by local operating conditions.

Competitive Landscape

Market concentration remains moderate. Sensata Technologies (Schrader), Continental AG, and Huf Hülsbeck & Fürst collectively command a significant share of the aftermarket revenue. Sensata capitalizes on its vast OEM installed base, introducing new coverage for its EZ-sensor platform, now including Ford and Land Rover. Continental has ramped up production in Bangalore, aiming to reach an ambitious target of millions of units annually to serve both global aftermarket and OEM customers. Huf's IntelliSens line stands out for its on-the-fly protocol updates, which simplify garage inventory management.

Tool suppliers like Bartec and Autel bolster their competitive edge by bundling sensors with software subscriptions and technician training. Autel's MaxiCOM MK906S PRO2-TS boasts comprehensive TPMS functions alongside Bluetooth LE support. Meanwhile, Bartec's latest release has expanded its coverage to include a broader range of models.

Emerging competition arises from smart-tire initiatives. Goodyear's SightLine event unveiled a groundbreaking approach: integrating multi-sensor arrays directly into tires, which then relay data to NVIDIA DRIVE Hyperion stacks. This move hints at a future where tire manufacturers might sidestep traditional TPMS components altogether. In response, suppliers are diversifying, forging telematics partnerships, and enhancing data-service offerings, positioning themselves for a landscape where hardware might become commoditized.

United States Aftermarket TPMS Industry Leaders

Sensata Technologies (Schrader)

Continental AG

Huf Hulsbeck & Fürst

Pacific Industrial

DENSO Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bartec USA unveiled software version 8.2, which broadens its coverage to include 2026 models and introduces enhancements to OBD-II reset features. This update aims to improve functionality and expand compatibility for users, ensuring the software remains up to date with the latest vehicle models and diagnostic requirements.

- June 2025: Bosch’s new SMP290 MEMS sensor integrates Bluetooth Low Energy for tire pressure monitoring. It offers ultra-low power consumption, 10-year lifespan, over-the-air updates, and smartphone connectivity, enhancing vehicle safety and efficiency.

United States Aftermarket TPMS Market Report Scope

The United States aftermarket TPMS market report is segmented by type (direct TPMS and indirect TPMS), technology integration (stand-alone TPMS units and smart/connected TPMS), vehicle type (passenger cars and commercial vehicles), and distribution channel (offline and online). The market forecasts are provided in terms of value (USD).

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart/Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs) | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles | |

| Buses & Coaches |

| Offline |

| Online |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart/Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs) | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | ||

| Buses & Coaches | ||

| By Distribution Channel | Offline | |

| Online | ||

Key Questions Answered in the Report

What is the current value of the United States aftermarket TPMS market?

The market is expected to grow from USD 0.72 billion in 2025 to USD 0.78 billion in 2026 and is forecast to reach USD 1.16 billion by 2031.

How fast is the market expected to grow?

The market is projected to grow at a CAGR of 8.32% during the forecast period (2026-2031).

Which TPMS type dominates U.S. replacements?

Direct TPMS held 83.26% share in 2025 due to FMVSS 138 compliance.

Which vehicle category will grow fastest?

Commercial vehicles are set to post the highest 8.55% CAGR as fleets retrofit connected systems.

Could smart tires reduce future sensor demand?

Yes, integrated tire-as-sensor platforms demonstrated in 2026 may eventually displace standalone TPMS in some premium EV segments.

Page last updated on: