India Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

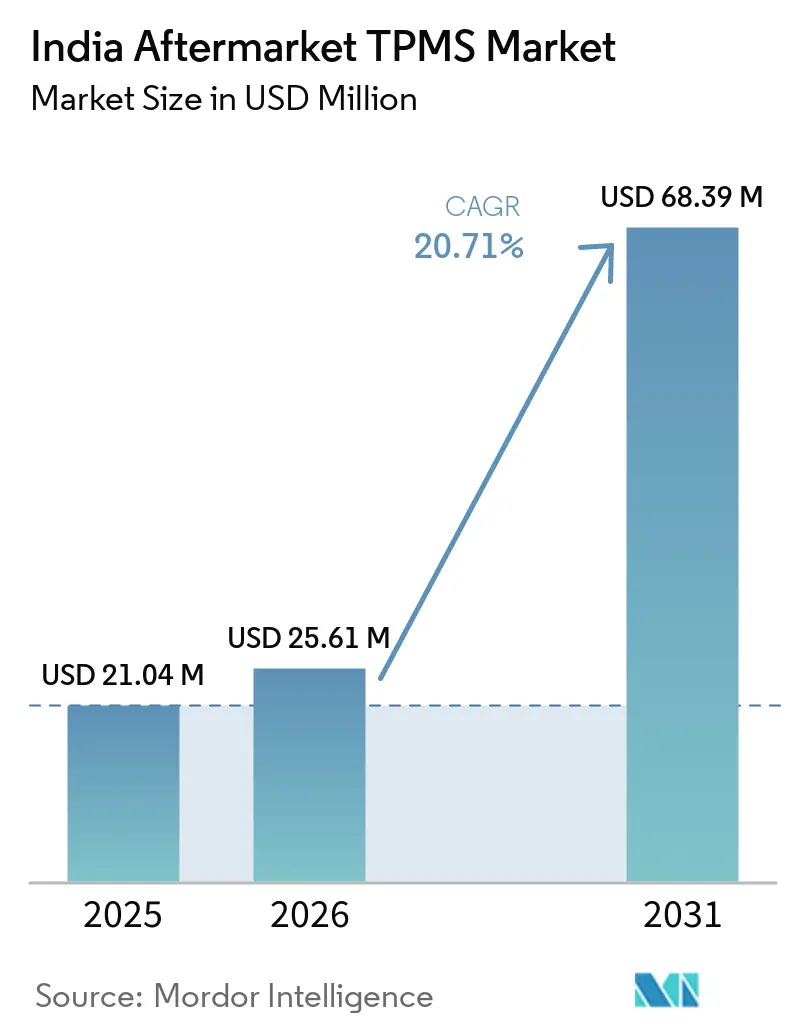

| Base Year Market Size (2025) | USD 21.04 Million |

| Market Size (2026) | USD 25.61 Million |

| Market Size (2031) | USD 68.39 Million |

| Growth Rate (2026 - 2031) | 20.71% CAGR |

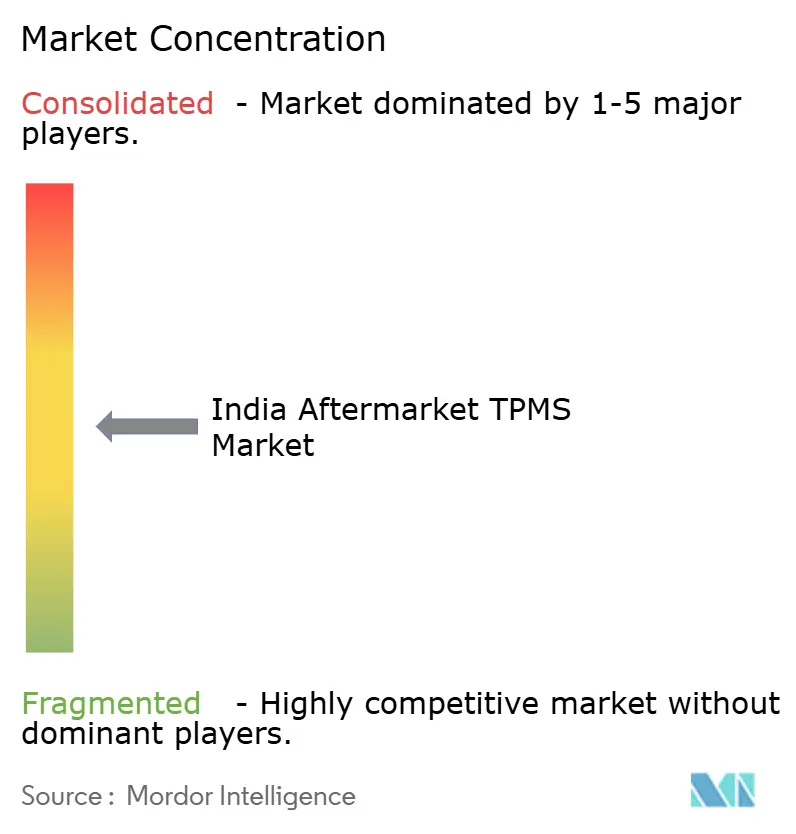

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Aftermarket TPMS Market Analysis by Mordor Intelligence

The Indian aftermarket TPMS market is projected to grow from USD 21.04 million in 2025 to USD 25.61 million in 2026 and is forecast to reach USD 68.39 million by 2031, growing at a CAGR of 20.71% from 2026 to 2031. Retrofit demand across aging passenger-car and light-truck fleets, the impending AIS-151 Stage-II retrofit mandate for heavier commercial classes, and the rapid growth of electric and CNG vehicles together lift addressable volumes far faster than original-equipment uptake. Organized tire-service chains bundle smart sensors with alignment, rotation, and nitrogen-inflation packages. At the same time, e-commerce storefronts expose do-it-yourself buyers to clamp-in kits priced under USD 15, extending reach into Tier-2 and Tier-3 cities. Insurers now embed TPMS telemetry into usage-based products that cut premiums 10-40%, incentivizing accurate, logged pressure management for fleets as small as 10 vehicles. Meanwhile, counterfeit sensors account for nearly one-third of the unorganized parts channel, hampering trust and prompting warranty-backed sourcing alliances among brand-name suppliers.

Key Report Takeaways

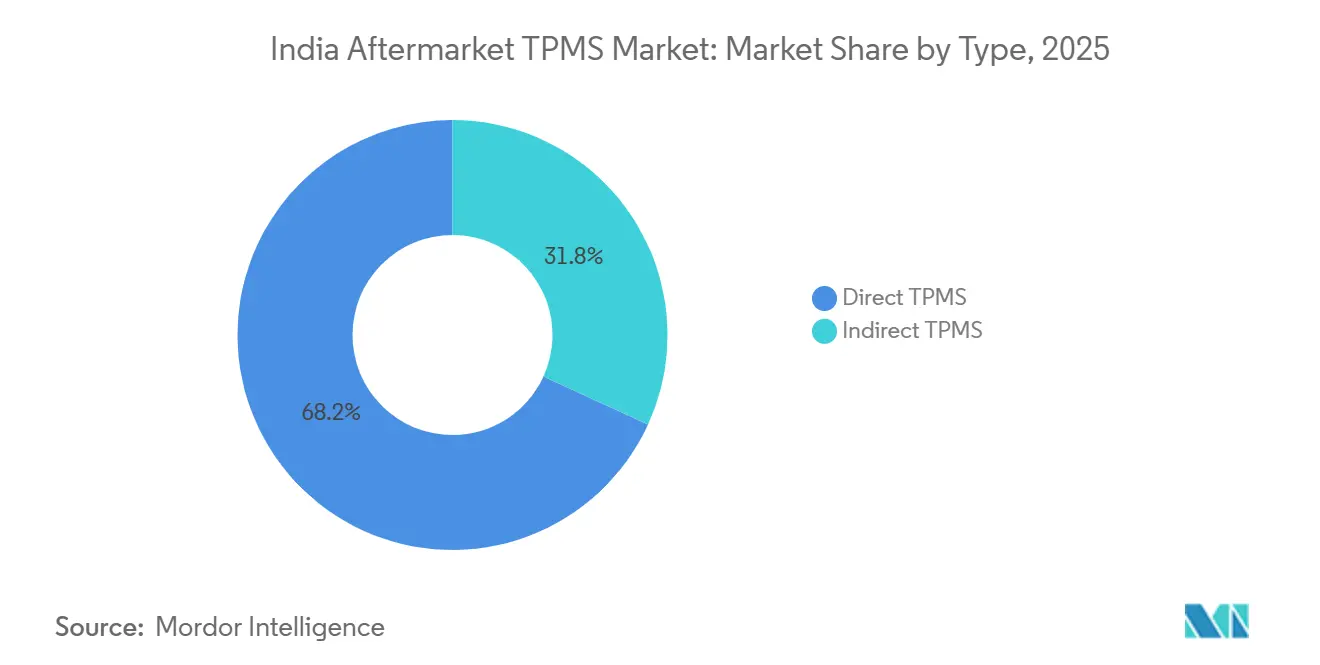

- By type, Direct TPMS captured 68.17% of the Indian aftermarket TPMS market share in 2025, whereas Indirect solutions are forecast to expand at a 21.17% CAGR through 2031.

- By technology integration, stand-alone kits held 58.83% of the Indian aftermarket TPMS market share in 2025, but connected or smart variants are advancing at a 21.42% CAGR through 2031.

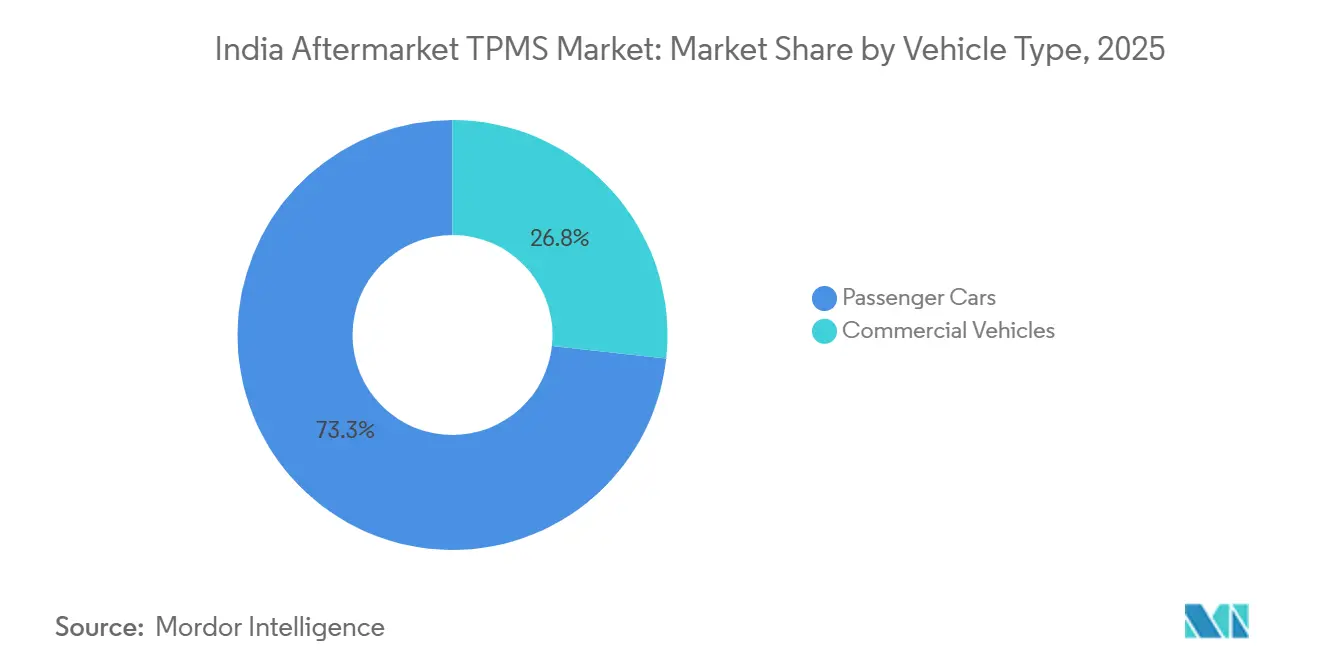

- By vehicle category, passenger cars commanded 73.25% of the Indian aftermarket TPMS market share in 2025, while commercial vehicles are projected to post the fastest growth at a 20.94% CAGR over 2026-2031.

- By channel, offline retail retained 64.51% of the Indian aftermarket TPMS market share in 2025, yet online distribution is projected to post the highest growth at a 21.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India contributes to a system defined not by any single country or region but by the interaction of many. The global aftermarket tpms market data by Mordor Intelligence represents that combined structure.

India Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AIS-151 Stage-II Mandate for Retro-Fitment | +6.2% | National, with early gains in Tamil Nadu, Karnataka, Maharashtra | Short term (≤ 2 years) |

| Growth of E-commerce & DIY Tyre | +4.8% | Urban centers, spill-over to Tier-2 cities | Medium term (2-4 years) |

| Heavier EV/CNG Vehicles Raising Tyre-Safety Sensitivity | +3.7% | Maharashtra, Kerala, Karnataka leading EV adoption | Medium term (2-4 years) |

| Expansion of Organized Service Chains | +2.9% | Metro cities expanding to Tier-2/3 markets | Long term (≥ 4 years) |

| SME Fleet Digitisation to Curb Tyre-Related OPEX | +2.1% | Commercial corridors: Delhi-Mumbai, Chennai-Bangalore | Medium term (2-4 years) |

| Insurance Telematics Discounts | +1.4% | Urban markets with higher insurance penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AIS-151 Stage-II Mandate for Retrofitment Across N2, N3, M2, M3 Categories

Implementing AIS-151 Stage-II compels medium- and heavy-duty vehicles on Indian roads to install TPMS. Compliance inspection is linked to annual fitness certificates, making adoption a non-optional cost item for fleet budgets[1]“Automotive Industry Standards AIS-151 Phase-II,” Ministry of Road Transport and Highways, morth. nic. in . Suppliers gain multi-year demand visibility and can plan localized manufacturing, inventory, and last-mile distribution. Enforcement certainty also improves financing prospects for domestic sensor makers, encouraging capacity expansion. Early adoption clusters in Tamil Nadu, Karnataka, and Maharashtra create reference customers that accelerate diffusion into adjacent markets. The regulation further normalizes TPMS fitment for light-commercial fleets, even though they are not legally required to do so.

Growth of E-commerce & DIY Tyre-Maintenance Culture

Online marketplaces like Flipkart and Amazon recorded double-digit growth in TPMS kit sales as younger male buyers aged 15-35 increasingly bypass brick-and-mortar stores. Transparent pricing, peer reviews, and step-by-step installation videos reduce information asymmetry and lower perceived risk for first-time buyers. Independent garages in Tier-2 and Tier-3 cities bulk-order sensors online to shorten lead times and widen SKU choices. Rising technical literacy among vehicle owners fosters a do-it-yourself ethos that substitutes labor cost with personal time, widening the addressable base. These factors shift value capture from physical dealers toward digital platforms that bundle payment, warranty, and logistics.

Heavier EV/CNG Vehicles Raising Tyre-Safety Sensitivity

In August 2024, India registered 4.4 million EVs and continues adding range-extending battery packs that increase axle loads[2]“Indian Electric Vehicle Statistics 2025,” Ministry of New and Renewable Energy, mnre.gov.in . CNG tanks similarly increase curb weight and affect tire pressure during thermal swings. Fleet managers report that under-inflation amplifies rolling resistance and cuts EV range by 6-10 km per charge. TPMS, therefore, becomes an operational efficiency tool rather than merely a safety accessory. The technology’s capability to send real-time alerts enables proactive pit-stop scheduling, reducing roadside downtime and tire-replacement frequency. Growth potential is highest in Maharashtra and Kerala, where policy incentives are accelerating the adoption of alternative fuels.

Expansion of Organised Service Chains Bundling Smart TPMS

Networks such as GoMechanic and myTVS position TPMS as part of bundled tire-care or annual-maintenance contracts. In-app dashboards display live pressure, temperature, and leak history, encouraging subscription renewals for data analytics. Volume purchasing allows these chains to price sensors competitively, limiting unorganized garages’ cost advantage. Standardized fitment practices and nationwide warranty coverage address customer trust gaps that emerge in a fragmented aftermarket. As chains expand into Tier-2/3 geographies, bundled packages raise awareness among price-sensitive users who value a predictable total cost of ownership over the lowest upfront price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-Sensitive Consumer Mindset | -4.3% | Rural and semi-urban markets, price-conscious segments | Short term (≤ 2 years) |

| Counterfeit Low-Cost Sensor Influx Hurting Trust | -2.8% | Unorganized retail channels, Tier-2/3 cities | Medium term (2-4 years) |

| Shortage of Trained Technicians | -2.2% | National, acute in Tier-2/3 cities with limited technical infrastructure | Long term (≥ 4 years) |

| Inter-Operability Issues With OE Infotainment Units | -1.8% | Premium vehicle segments, multi-brand service centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Consumer Mindset

A TPMS kit typically costs INR 5,000–10,000 (USD 54-108), a meaningful discretionary outlay when many owners already postpone routine maintenance. Surveys indicate 68% of drivers defer non-essential vehicle upgrades during economic uncertainty. Rural and semi-urban households, where disposable income is lower, often prioritize visible accessories such as infotainment over unseen safety electronics. Replacing the battery every 5–7 years adds a recurring cost, reinforcing hesitation. Southern and western states with higher per-capita incomes show better conversion rates, but sustained price promotions or financing schemes remain critical for nationwide diffusion.

Counterfeit Low-Cost Sensor Influx Hurting Trust

Fake sensors entering India through unorganized channels fail within 6–12 months, while genuine variants last nearly a decade. National police data (National Crime Records Bureau (NCRB)) link counterfeit parts to 20% of road-accident cases, damaging the category’s reputation among consumers and installers[3]“Impact of Counterfeit Auto Parts on Road Safety,” Society of Indian Automobile Manufacturers, Siam.in . Warranty claims are rejected once the counterfeit origin is verified, fuelling negative word of mouth that suppresses repeat demand. Major brands now embed QR-code authentication and tamper-proof packaging, but adoption is uneven outside metropolitan centers. Until enforcement curbs the grey market, quality failures will significantly drag on sentiment, especially in Tier-2/3 regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct Accuracy Retains Value Leadership

Direct sensors accounted for 68.17% of the Indian aftermarket TPMS market share in 2025, underscoring fleet preference for ±1 PSI accuracy that satisfies insurer data-logging requirements, thereby reinforcing the India aftermarket TPMS market share advantage for valve-mounted technology. Continental’s Bengaluru line now ships second-generation units rated for 7-10 year battery endurance, lowering lifetime service costs. Yet, Indirect platforms are forecast to grow at a 21.17% CAGR through 2031 as hatchback and sedan owners adopt ABS-based inference to stay under the INR 5,000 (USD 54) installation threshold, expanding the India aftermarket TPMS market footprint among first-time buyers.

Indirect adoption is further normalized by Maruti Suzuki’s 2026 range, which offers wheel-speed-based alerts across mid-tier trims. However, limited precision and the need for manual resets after rotations limit their utility for long-haul trucks, keeping Direct systems the backbone of predictive maintenance contracts and preserving the Indian aftermarket TPMS market's premium in commercial niches.

By Technology Integration: Smart/Connected Kits Redefine Total Cost of Ownership

Stand-alone displays retained 58.83% of the Indian aftermarket TPMS market share in 2025, signaling a large installed base that values one-time outlays. Smart TPMS platforms, however, are growing at a 21.42% CAGR, exporting data to cloud dashboards that unlock fuel-savings analytics; this dynamic positions connected sensors as the fastest value compounder in the Indian aftermarket TPMS market.

Shriram General Insurance cuts premiums by 10-15% for fleets that maintain tire pressure within tolerance for 95% of operating hours, validating the payback on telematics subscriptions. As 5G coverage expands, latency falls, and over-the-air firmware updates become routine, the Indian aftermarket TPMS industry is moving toward data-driven services rather than hardware margins.

By Vehicle Type: Commercial Vehicles Spur Incremental Units

Passenger cars made up 73.25% of the Indian aftermarket TPMS market share in 2025, reflecting rapid SUV and MUV penetration in Tier-2 cities. Embedded TPMS in Maruti’s 2026 line illustrates mainstreaming that sustains the India aftermarket TPMS market through replacement cycles. Yet commercial fleets are projected to post a 20.94% CAGR as telematics-linked TPMS becomes pivotal in reducing tire-related operating expenses by 15-20%.

Light commercial vans used by last-mile e-commerce couriers deliver proven ROI, and Fleeca’s 22-sensor Kawach package enables multi-axle rigs to document compliance with stricter overloading fines, thereby expanding the India aftermarket TPMS market opportunity in freight corridors.

By Distribution Channel: Online Gains Share but Service Remains Offline

Offline outlets accounted for 64.51% of the Indian aftermarket TPMS market share in 2025. Fleeca points and JK Tire dealerships are offering bundled services, including installation, calibration, and warranty. With a focus on quality assurance and counterfeiting prevention, consumers remain loyal to these service chains. As a result, the Indian aftermarket TPMS market is increasingly leaning on in-shop expertise, particularly for Direct sensors.

Conversely, online marketplaces are growing at a 21.51% CAGR by targeting hobbyists with screw-in units shipped nationwide. Flipkart’s seller-verification badges and expanded return windows aim to curb substandard imports, and pilot tie-ups with local garages promise to merge click-to-buy convenience with professional fitting, potentially unlocking new strata of the India aftermarket TPMS market.

Geography Analysis

India's six largest metros—Delhi NCR, Mumbai, Bangalore, Chennai, Pune, and Hyderabad—dominate sensor sales, a testament to their dense vehicle populations and a wide array of certified service centers. In Bangalore, manufacturing and R&D thrive, bolstered by Continental's large-scale plant and Goodyear's algorithm lab, both of which attract skilled labor and ensure timely supplies. Delhi's robust logistics networks are paving the way for early trials of Smart TPMS, while in Mumbai, the urgency of ride-hail fleets, which can afford minimal downtime, accelerates retrofit cycles.

Meanwhile, Tier-2 cities like Ahmedabad, Jaipur, and Lucknow are witnessing robust growth. Here, SMEs are turning to telematics as a strategy to combat surging diesel prices. In Gujarat's bustling industrial corridor, companies like Regrip are celebrating successes, with clients reporting significant reductions in fleet expenses thanks to TPMS-driven maintenance. Although rural areas grapple with challenges such as price sensitivity and inconsistent data coverage, the ongoing Bharatmala highway development projects are improving travel speeds. This progress is nudging safety-conscious operators to consider sensors in the near future.

In states like Tamil Nadu and Maharashtra, where vehicle-fitness exams are rigorously enforced, there's an unintended boost to sensor adoption. As the AIS-151 Stage-II rollout looms, with a focus on the accident-prone Delhi-Jaipur and Mumbai-Pune expressways, regional demand is set to surge. This momentum positions the Indian aftermarket TPMS market as a nationwide phenomenon, transcending its initial metro-centric roots.

The aftermarket tpms market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for Japan, China, United States, and South Korea, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

With no single manufacturer holding a significant share of revenue, competition remains moderate. Continental recently increased its output in Bengaluru and aims to reach full capacity within a few years. This move, catering to both domestic demands and exports to Korea, highlights India's emergence as a cost-effective manufacturing hub. Meanwhile, JK Tire introduced embedded sensors under its Treel brand. This initiative emphasizes vertical integration, avoiding retrofit challenges while allowing JK Tire to command a price premium, albeit at the expense of narrowing its target market.

Manatec, leveraging an endorsement from ASRTU, has secured bus contracts and established a niche in public transport that few competitors can rival. Fleeca stands out by offering rechargeable batteries and a nationwide service network. They ensure data authenticity with QR-code validation, effectively warding off counterfeit threats. Goodyear and CEAT are pivoting towards algorithmic differentiation, integrating intelligence within the casing or ECU. This strategy shifts the value proposition from mere hardware to actionable predictive insights. Furthermore, emerging API-driven models are enabling insurers and ERP platforms to access pressure histories on demand. This trend underscores a significant shift in the ecosystem, highlighting the growing importance of software proficiency in India's aftermarket TPMS landscape.

India Aftermarket TPMS Industry Leaders

Sensata Technologies (Schrader)

Continental AG

Treel Mobility (JK Tyre)

Steelmate Co Ltd

Blaupunkt India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: At its Banmore plant, JK Tire & Industries Ltd. introduced India's first factory-embedded smart tires, equipped with sensors during production and distributed through numerous retail outlets.

- March 2025: CEAT unveiled its SportDrive run-flat tires, featuring foam noise dampers and integrated TPMS, specifically designed to enhance the performance and safety of high-performance SUVs. These tires aim to deliver superior driving comfort, reduced noise, and improved handling, catering to the growing demand for advanced tire technologies in the automotive market.

India Aftermarket TPMS Market Report Scope

The Indian Aftermarket TPMS Market Report is Segmented by Type (Direct TPMS and Indirect TPMS), Technology Integration (Stand-Alone TPMS Units and Smart/Connected TPMS), Vehicle Type (Passenger Cars and Commercial Vehicles), and Distribution Channel (Offline and Online). The Market Forecasts are Provided in Terms of Value (USD).

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart / Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs) | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles | |

| Buses & Coaches |

| Offline |

| Online |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart / Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs) | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | ||

| Buses & Coaches | ||

| By Distribution Channel | Offline | |

| Online | ||

Key Questions Answered in the Report

What revenue is forecast for the India aftermarket TPMS market by 2031?

The market is expected to reach USD 68.39 million by 2031, expanding at a 20.71% CAGR through 2031.

Which TPMS type grows fastest through 2031?

Indirect, ABS-based systems are projected to post a 21.17% CAGR because they meet cost thresholds for hatchback owners.

Which distribution channel is gaining share most rapidly?

Online platforms expand at a 21.51% CAGR as buyers seek transparent pricing and DIY options.

Why are EV and CNG vehicles accelerating TPMS adoption?

Extra axle load from batteries and cylinders heightens blowout risk; real-time monitoring preserves range and safety for high-torque drivetrains.

How do counterfeit sensors affect the market?

Counterfeits shorten sensor life and erode consumer trust, subtracting an estimated 2.8% points from forecast CAGR.

Page last updated on: