China Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.53 Billion |

| Market Size (2026) | USD 0.61 Billion |

| Market Size (2031) | USD 1.20 Billion |

| Growth Rate (2026 - 2031) | 14.61% CAGR |

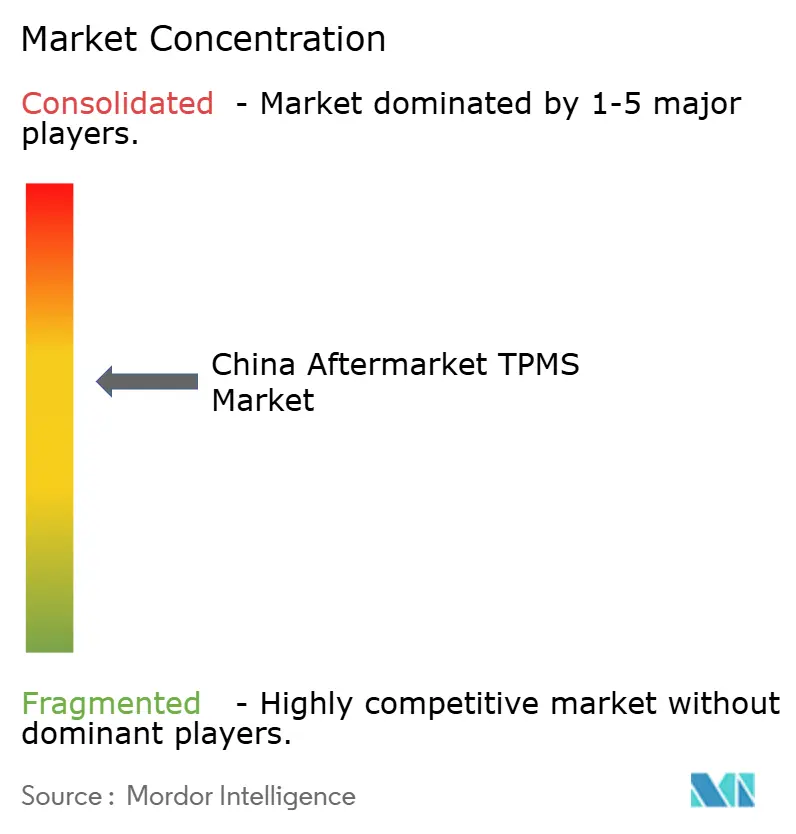

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Aftermarket TPMS Market Analysis by Mordor Intelligence

The China aftermarket TPMS market size is projected to grow from USD 0.53 billion in 2025 to USD 0.61 billion in 2026, and is forecast to reach USD 1.20 billion by 2031, growing at a CAGR of 14.61% from 2026 to 2031. In recent years, direct TPMS sensors have started reaching the end of their sealed-battery lifespan. This has initiated a replacement cycle, bolstering consistent aftermarket demand. Concurrently, battery-electric heavy trucks are not only accelerating tire wear but also heightening the importance of real-time pressure monitoring. E-commerce giants like JD.com and Tmall Auto have streamlined distribution. This is evident in JD.com’s surge in sales of smart tire monitors. The competitive landscape is fierce: numerous manufacturers showcase a wide range of TPMS SKUs on Made-in-China, with varying price points. This pricing pressure compels both global and local brands to stand out through enhanced software features, extended battery life, and over-the-air (OTA) firmware updates.

Key Report Takeaways

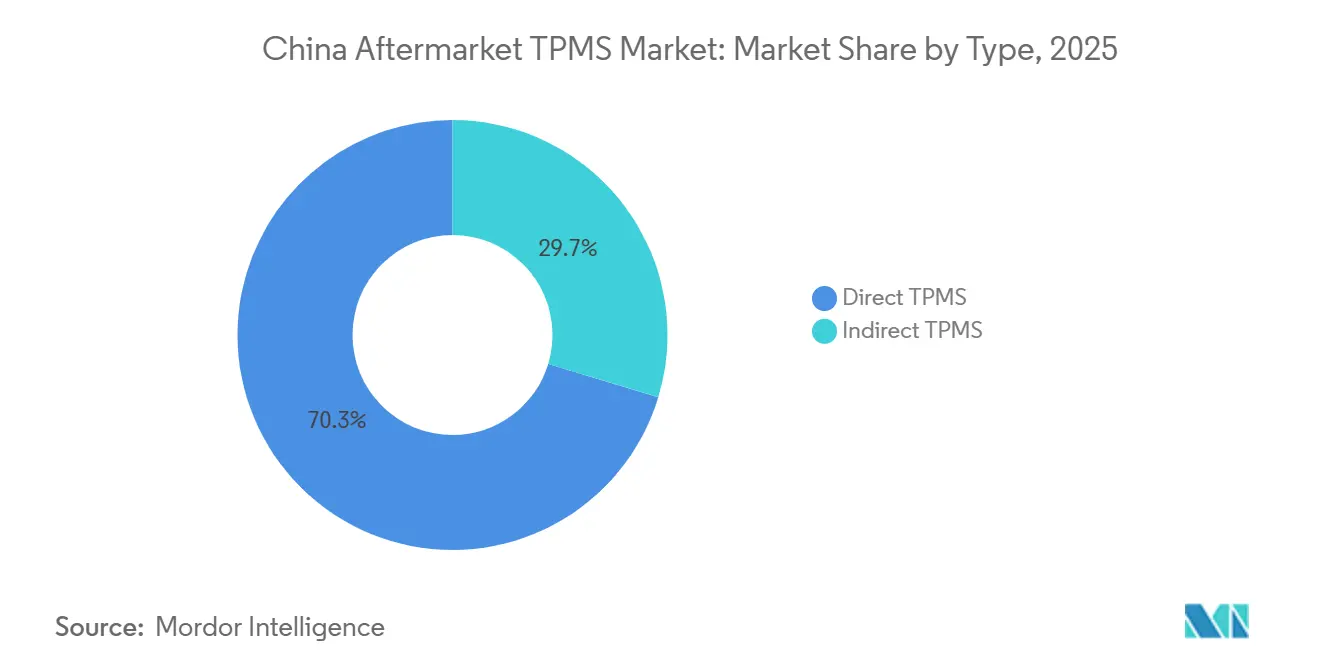

- By type, direct systems led the China aftermarket TPMS market with a 70.33% share in 2025; indirect systems are the fastest-rising segment and are forecast to expand at a 15.04% CAGR through 2031.

- By technology integration, stand-alone units accounted for 71.46% of the China aftermarket TPMS market share in 2025, while smart or connected solutions are projected to grow at a 17.11% CAGR through 2031.

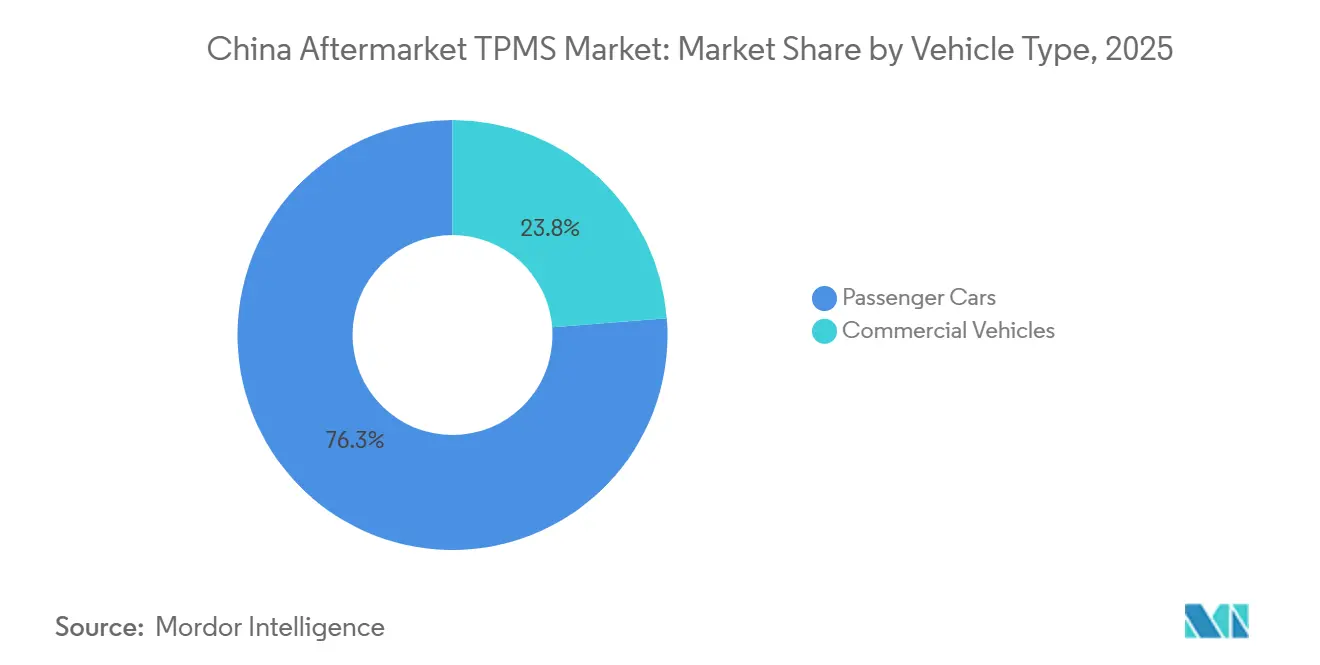

- By vehicle category, passenger cars accounted for 76.25% of the China aftermarket TPMS market share in 2025, whereas commercial vehicles are advancing at a 15.85% CAGR, driven by rising electrification and subsidy support.

- By distribution channel, offline outlets retained 64.36% of the China aftermarket TPMS market share in 2025, while online platforms are expanding at a 16.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on aftermarket tpms market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Passenger-Car Parc and Replacement Cycle | +3.2% | Eastern provinces | Long term (≥4 years) |

| Mandatory TPMS Fitment Spills Over to Retrofit Demand | +2.8% | Tier 1 cities and national fleets | Medium term (2-4 years) |

| Electrification Raising Tire-Wear on CV Fleets | +2.4% | National logistics hubs | Medium term (2-4 years) |

| Expansion of E-commerce Parts Channels | +2.1% | Urban areas nationwide | Short term (≤2 years) |

| Heightened Consumer Safety Awareness | +1.9% | Affluent coastal regions | Medium term (2-4 years) |

| Domestic One-Chip Silicon Cutting Kit Prices | +1.8% | National manufacturing base | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Passenger-Car Parc and Sensor-Replacement Cycle

China has a significant passenger-car parc and continues to add vehicles annually. Cars sold in recent years are equipped with sealed lithium batteries, which typically last several years. This will lead to a substantial replacement wave in the future, adding millions of sensors to the annual aftermarket demand. Medium-duty trucks, with a faster turnover rate, further contribute to increased volumes in the commercial segment. Since these batteries are non-serviceable, a dead cell requires complete sensor replacement, ensuring consistent revenue for suppliers. Tier-1 cities are leading due to their established service networks, while tier-2 and tier-3 regions are gradually advancing as their DIFM infrastructure develops.

Mandatory TPMS Fitment on New Vehicles Spills Over to Retrofit Demand

The implementation of GB 26149-2017 significantly increased the adoption of TPMS in passenger cars [1]“Passenger Vehicle TPMS Performance Requirements,” GB 26149-2017, ChineseStandard.net. With factory-equipped used cars now entering the secondary market, first-time owners are benefiting from real-time alerts and are also retrofitting older vehicles. Brands like Steel Mate and Orange Electronics offer both internal and external kits that can be self-installed or professionally installed at tire shops. Even without formal truck mandates, commercial operators are proactively installing these systems to prepare for future regulations and reduce fuel losses from underinflation. The Standardization Administration's continuous scrutiny ensures that retrofit momentum remains strong, particularly in the densely populated provinces along the east coast.

Electrification Accelerating Tire-Wear on CV Fleets

The Chinese government has introduced subsidies for electric trucks, which have rapidly become the dominant segment in China's logistics fleet[2]“Electric Truck Tire Wear Study,” Firemax, Firemax.com. Heavy battery packs, combined with instant motor torque, have led to a significant reduction in tire life compared to their diesel counterparts. Even slight under-inflation can further reduce tire lifespan and increase energy consumption. This issue is particularly concerning in winter, when battery performance diminishes considerably. To address these challenges, fleet managers are adopting TPMS sets equipped with LoRa telemetry, which relay data back to dispatch dashboards. Shenzhen EGQ, for instance, offers kits designed for multi-wheel configurations. Additionally, sensor manufacturers are refining pressure algorithms for the latest low-rolling-resistance truck tires, positioning the technology as an essential cost-saving tool rather than an optional add-on.

Expansion of E-Commerce Parts Channels

JD.com reported a significant increase in TPMS revenue, while Bosch celebrated a substantial profit from its inaugural Tmall Auto campaign. Hamaton’s U-Pro Hybrid, an NFC and Bluetooth sensor, can be easily programmed via smartphones, eliminating the need for costly diagnostic tools and enabling DIY installations. The platform Made-in-China showcases numerous unique TPMS SKUs, with minimum order quantities as low as 1 unit. This flexibility enables budget-conscious workshops to sidestep intermediaries. Suppliers are meeting the swift delivery demands of tier-1 customers by using regional warehouses, thereby ensuring quick fulfillment times. With the advent of connected cars that automatically reorder parts when battery voltage drops, e-commerce is poised to transition from a reactive model to a predictive replenishment model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity and Counterfeit Sensors | -1.8% | Rural markets nationwide | Long term (≥4 years) |

| Installation Complexity for Legacy Vehicles | -1.2% | Rural service networks | Medium term (2-4 years) |

| Non-Standard Frequencies and Battery Costs | -0.9% | National | Short term (≤2 years) |

| Data-Privacy Worries around Connected TPMS | -0.7% | Government and enterprise fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity and Counterfeit Sensors

Standard units fetch aftermarket prices within a certain range, while OEM-equivalent sensors are significantly more expensive. This price disparity fuels demand for low-cost substitutes, some of which turn out to be counterfeit. Stellantis and Petromin exposed a significant export ring dealing in imitation brake and steering parts, highlighting vulnerabilities in China's quality oversight. Counterfeit Tire Pressure Monitoring Systems (TPMS) often malfunction quickly, attributed to inadequate sealing and misaligned radio frequencies, eroding consumer trust. Freight operators, already feeling the pinch from electric-vehicle price wars, find little leeway for premium sensors, intensifying downward pressure on prices. While genuine brands are now prominently showcasing ISO and CE certifications online and extending warranties, enforcement of these measures is hindered by fragmented policing across numerous factories.

Installation Complexity for Legacy Vehicles

Retrofitting older models often requires rim drilling, valve-stem alterations, and dashboard integration beyond the skill set of many county-level workshops. Rural owners consequently postpone purchases, constraining nationwide penetration rates until simplified plug-and-play kits or broader vocational-training programs reduce the specialized labor bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct TPMS Dominates, Indirect Systems Gain Software Traction

Direct systems captured 70.33% of the Chinese aftermarket TPMS market in 2025 because GB 26149-2017 requires precise, per-wheel pressure alarms below 75% of recommended levels. Direct sensors provide temperature data and tire-level statistics prized by ADAS platforms from automakers such as Tesla and NIO. Indirect technology, however, is projected to advance at a 15.04% CAGR because an ABS-based software update can turn any pre-2019 vehicle into a basic alert system without new hardware. Yet indirect options cannot flag over-inflation or slow leaks, identify which wheel is failing, or be calibrated after every rotation, reducing fleet appeal.

Domestic chip makers are closing the cost gap: AutoChips’ single-die AC5111 has pushed average direct-sensor prices below a certain threshold, easing past price challenges. Baolong is investing significantly in R&D to enhance battery life and integrate Bluetooth connectivity, positioning itself for OTA ecosystems. Despite regulations favoring direct alerts, analysts predict direct sensors will surpass indirect units in total volume, even as indirect units penetrate price-sensitive markets.

By Technology Integration: Stand-Alone Leads, Smart/Connected Surges

Stand-alone TPMS devices held 71.46% of the Chinese aftermarket TPMS market in 2025 and remain staples for the used-car aftermarket, where a simple dash display suffices. Smart or connected platforms integrating BLE, NFC, and OTA updates are forecast to post a 17.11% CAGR, driven by smartphone ubiquity and telematics demand. RF-Star’s BLE kit allows drivers to monitor tire pressure, temperature, and sensor battery life via an app, and to push updates without removing the wheels. Honghe Technology demonstrated that encrypted OTA packages can achieve extremely low failure rates, enhancing confidence in field firmware upgrades.

Fleet operators are adopting cloud-linked systems that transmit tire data through LoRa gateways, reducing roadside downtime, which typically incurs high costs per commercial incident. For individual drivers, NFC-programmable models eliminate the need for a diagnostic tool, enabling a DIY tire swap in a short time. While stand-alone units are expected to dominate low-ticket sales for the foreseeable future, software-defined sensors are paving the way for subscription revenue through advanced analytics and remote diagnostics.

By Vehicle Type: Passenger Cars Anchor, Commercial Fleets Accelerate

Passenger cars accounted for 76.25% of the Chinese aftermarket TPMS market in 2025, reflecting a large car parc and mandatory fitment requirements. Still, commercial vehicles show a stronger outlook, with a 15.85% CAGR driven by tailwinds from electrification. SUVs and multi-purpose vehicles, known for carrying heavier loads and experiencing greater sidewall flex, are the first to adopt new sensors. Meanwhile, hatchbacks and sedans maintain steady aftermarket volumes as older sensors approach their end-of-life.

Electric heavy trucks, which weigh significantly more than their diesel counterparts, experience higher tire temperatures, leading to a substantial reduction in tread life. ZF’s OptiTire accommodates multiple rolling wheels plus a spare. It seamlessly integrates with telematics dashboards, offering potential fuel savings. With Beijing poised to introduce truck-segment mandates, the commercial adoption of such technologies is expected to shift from optional to essential.

By Distribution Channel: Digital Transformation Reshapes Market Access

Offline stores and workshops retained 64.36% of the Chinese aftermarket TPMS market in 2025, as complex installations still require lifts, torque tools, and ECU programming. Yet the Chinese aftermarket TPMS market tilts toward online storefronts, growing at 16.35% CAGR. A bundled mobile installation service resolves the skills gap for urban consumers. Hybrid “click-and-install” models intertwine e-commerce ordering with partner garages, creating omnichannel convenience without sacrificing artistry.

Traditional parts chains respond by launching in-house apps and on-site fitment vans. Transparent online pricing nudges offline players to sharpen their promotions, raising market efficiency. As rural broadband improves, an ever-larger slice of the China aftermarket TPMS market will transact digitally while finishing installation locally.

Geography Analysis

Eastern coastal provinces dominate value contribution owing to high vehicle density, strict inspection regimes, and established service networks. Guangdong, Jiangsu, and Zhejiang together account for over half of the Chinese aftermarket TPMS market. Tier-1 cities inside these provinces show early uptake of smart sensors because the telematics infrastructure is mature and consumer income supports incremental features.

Central and western regions emerge as volume drivers. Ongoing highway build-outs under national “western development” policies expand workshop footprints, enabling mid-range sensor offerings to reach new owners. Mountainous routes and harsher climates in provinces such as Sichuan accelerate tire degradation, raise replacement frequency, and enlarge the addressable base. Growing logistics traffic along the Belt and Road corridors also elevates TPMS demand among long-haul fleets.

Northern provinces house sizable government and SOE fleets that must comply with both safety and cybersecurity guidelines. Beijing and Tianjin fleets favor domestically hosted connected solutions vetted by regulators, giving local vendors an edge. Harsh winters magnify the safety benefits of timely pressure alerts, pushing penetration above the national average despite a modest population share.

Mordor Intelligence provides coverage of the aftermarket tpms market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to South Korea, Japan, India, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

In the Chinese aftermarket TPMS market, numerous manufacturers vie for dominance, offering a wide range of SKUs at affordable prices. This pricing strategy keeps average selling prices low while ensuring high turnover. Local leader Shanghai Baolong employs vertical integration—spanning MEMS design, certified mass production, and original equipment (OE) partnerships with key automotive brands—to safeguard its market share. The company allocates significant resources to R&D, supporting a large team of engineers across multiple facilities and securing numerous patents in TPMS and ADAS subsystems.

Global brands target premium segments. Sensata’s Schrader EZ-sensor family expanded its coverage to include additional vehicle models, showcasing the potential of diagnostic-tool ecosystems in prolonging hardware lifespan. Denso’s addition of new part numbers broadens its aftermarket catalog, making it accessible to more vehicles. ZF’s WABCO OptiTire, emphasizing multi-wheel trailer monitoring, seamlessly integrates with the ZF OptiLink app for enhanced predictive maintenance [3]“WABCO OptiTire Launch,” ZF Aftermarket, Autotrade-News.com.

The threat of counterfeits is palpable: a major crackdown on counterfeit operations highlighted the vast scale of counterfeit auto parts exports. In retaliation, reputable producers now prominently display ISO and FCC certifications and offer bundled multi-year warranties. New entrants like RF-Star and Honghe Technology are innovating by embedding BLE radios and OTA stacks into sensors priced competitively. These sensors can connect directly to smartphones, bypassing traditional garage systems. As platforms in connected vehicles begin to leverage tire data for comprehensive vehicle health assessments, the focus of differentiation is shifting from mere hardware costs to secure firmware, advanced analytics, and strategic platform collaborations.

China Aftermarket TPMS Industry Leaders

Sensata Technologies (Schrader)

Continental AG

Shanghai Baolong Automotive

Steelmate Automotive

Hamaton Automotive Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Li Auto awarded Shanghai Baolong the 2025 Supply Chain Strategic Partner accolade, underscoring their close collaboration on TPMS, wheel-speed sensors, and advanced chassis technologies.

- July 2025: ZF Aftermarket has launched WABCO OptiTire, a trailer TPMS that monitors up to 20 wheels and seamlessly integrates with ZF OptiLink to enhance fuel savings.

China Aftermarket TPMS Market Report Scope

The China aftermarket TPMS market report is segmented by type (direct TPMS, indirect TPMS), technology integration (stand-alone TPMS units, smart/connected TPMS), vehicle type (passenger cars, commercial vehicles), and distribution channel (offline, online). The market forecasts are provided in terms of value (USD) and volume (units).

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart/Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sports Utility Vehicles (SUVs) and Multi-Utility Vehicles (MUVs) | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Offline (Parts Stores, Specialty Shops, Service Centers) |

| Online (OEM Sites/Apps, E-commerce Platforms) |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart/Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sports Utility Vehicles (SUVs) and Multi-Utility Vehicles (MUVs) | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Distribution Channel | Offline (Parts Stores, Specialty Shops, Service Centers) | |

| Online (OEM Sites/Apps, E-commerce Platforms) | ||

Key Questions Answered in the Report

How fast is the China aftermarket TPMS market expected to grow between 2026 and 2031?

Industry revenues are forecast to rise from USD 0.61 billion in 2026 to USD 1.20 billion by 2031, which translates to a 14.61% CAGR over the period.

Which TPMS technology holds the largest revenue share today?

Direct systems commanded 70.33% of 2025 sales thanks to regulatory accuracy mandates.

Why are commercial-vehicle fleets adopting TPMS more aggressively now?

Heavier battery packs and instant torque in electric trucks accelerate tire wear, making real-time pressure data critical for uptime and cost control.

How is e-commerce influencing TPMS distribution in China?

Online platforms grew 16.35% annually as NFC and Bluetooth sensors allow DIY programming, while marketplaces list over 560 SKUs with transparent pricing.

Page last updated on: