South Korea Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

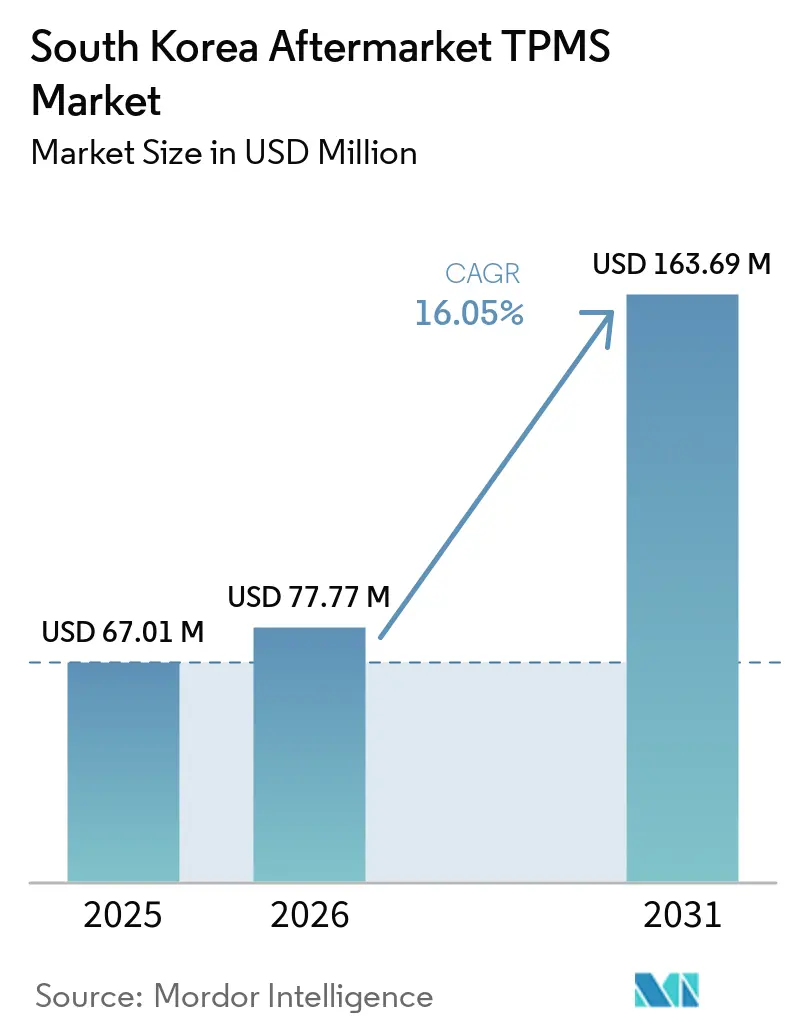

| Base Year Market Size (2025) | USD 67.01 Million |

| Market Size (2026) | USD 77.77 Million |

| Market Size (2031) | USD 163.69 Million |

| Growth Rate (2026 - 2031) | 16.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Aftermarket TPMS Market Analysis by Mordor Intelligence

The South Korean aftermarket TPMS market size is expected to grow from USD 67.01 million in 2025 to USD 77.77 million in 2026 and is forecast to reach USD 163.69 million by 2031, at a CAGR of 16.05% during the forecast period (2026-2031). The rapid expansion mirrors the confluence of strict national safety regulations, accelerating EV penetration, and the growing preference for larger-diameter tires that require dual-frequency sensor technology. Wider internet retail adoption is compressing price dispersion while enabling do-it-yourself (DIY) sensor installations, increasing replacement volumes. Simultaneously, fleet operators are linking TPMS data with telematics dashboards to curb fuel consumption and unplanned downtime, pushing demand for smart, Bluetooth-enabled sensors [1]“Motor Vehicle Management Act Updates,” Ministry of Land, Infrastructure and Transport, molit.go.kr. Cybersecurity scrutiny is also shaping product roadmaps, as encrypted telemetry becomes a differentiator.

Key Report Takeaways

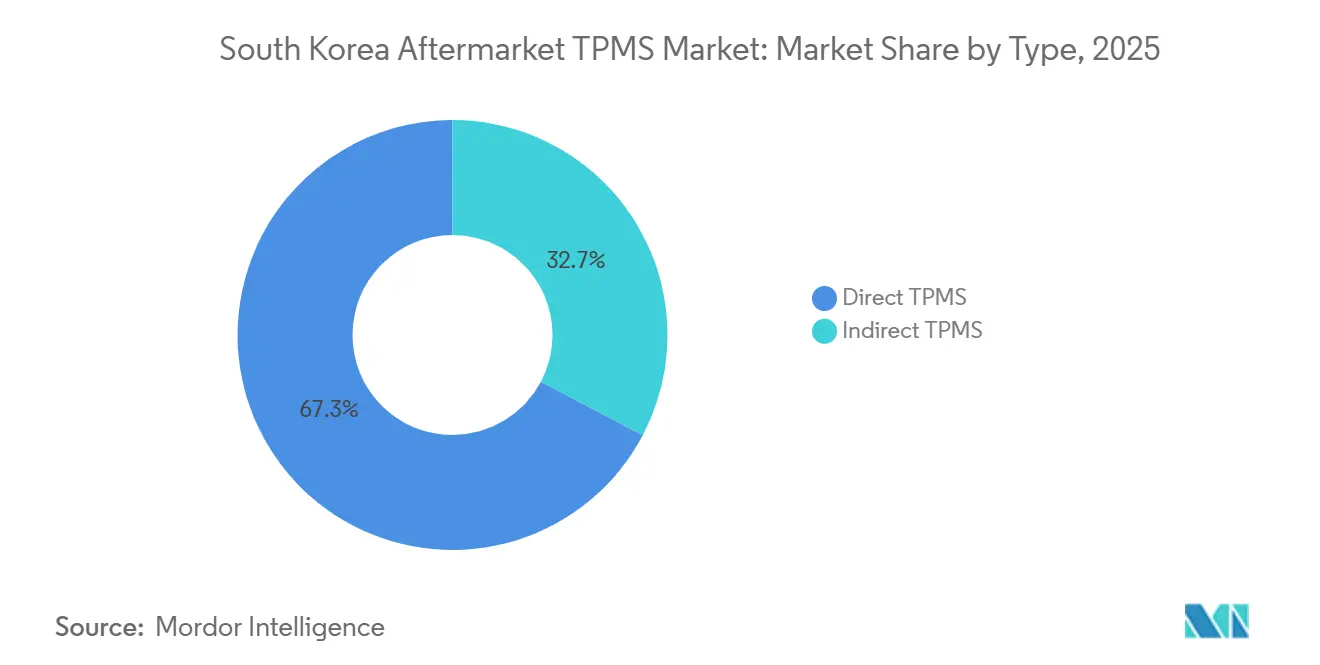

- By type, Direct TPMS accounted for 67.28% of the South Korean aftermarket TPMS market share in 2025, whereas Indirect TPMS is projected to register a 16.09% CAGR through 2031.

- By technology integration, stand-alone sensors held 57.16% of the South Korean aftermarket TPMS market share in 2025, while smart/connected solutions are set to grow at a 16.28% CAGR over 2026-2031.

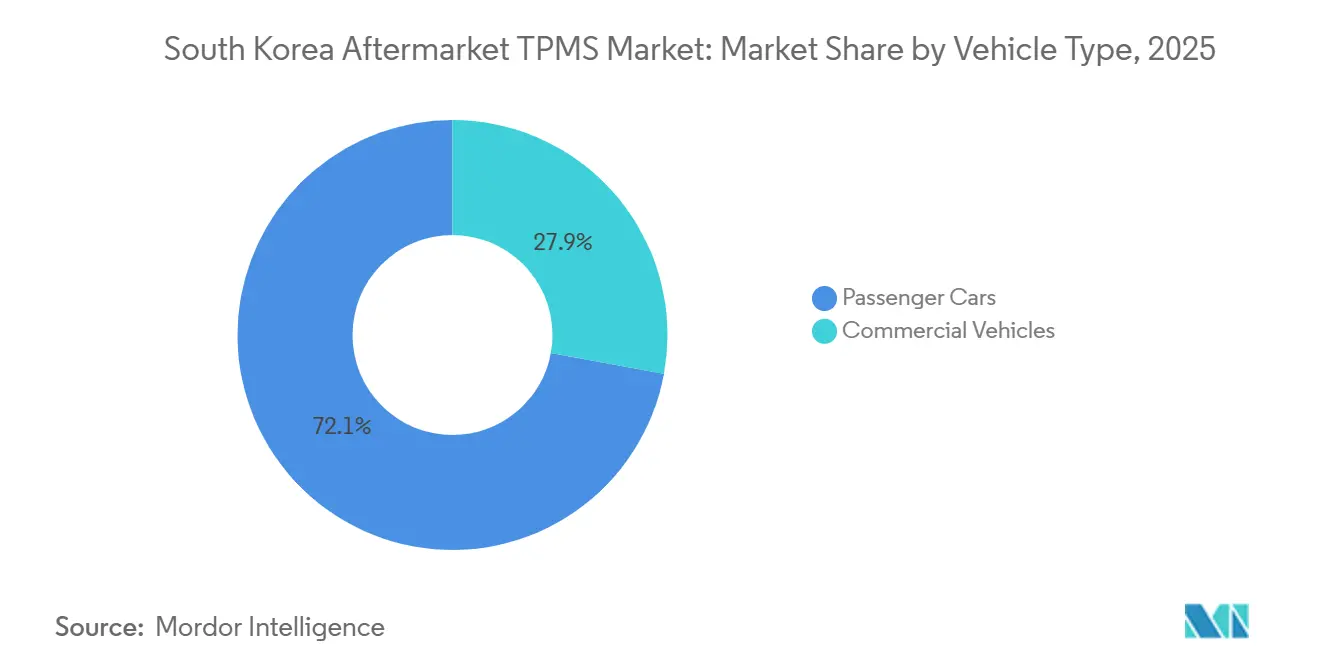

- By vehicle type, passenger cars dominated with 72.11% of the South Korean aftermarket TPMS market share in 2025; commercial vehicles will post the fastest expansion at a 16.16% CAGR through 2031.

- By distribution channel, offline outlets retained 65.78% of the South Korean aftermarket TPMS market share in 2025, yet online platforms will grow the fastest at a 16.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in South korea includes both locally based firms and those operating across multiple regions. The market landscape in the global aftermarket tpms industry research shows how these players are arranged internationally.

South Korea Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Retrofit Rule | +3.2% | South Korea nationwide | Medium term (2-4 years) |

| Surge In Online Tire And Parts | +2.8% | Urban areas, Seoul metropolitan region | Short term (≤ 2 years) |

| Growing SUV / EV Tire Upgrades | +2.1% | South Korea with concentration in affluent districts | Medium term (2-4 years) |

| Fleet-Telematics Bundles Now Bundling Bluetooth-Le Smart Tpms | +1.9% | Commercial vehicle corridors, logistics hubs | Long term (≥ 4 years) |

| Domestic Tire Makers' Loyalty-Programs | +1.7% | South Korea nationwide through dealer networks | Short term (≤ 2 years) |

| Start-Up Innovation Creating "Premium Retrofit" Niche | +1.4% | Fleet operators, premium vehicle segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Retrofit Rule For All Passenger Cars First Registered Before-2013 Deadline Extension

South Korea’s TPMS mandate applies to vehicles first registered from 2013 onward, yet millions of 2008-2012 models still lack factory sensors. During periodic inspections, service centers increasingly recommend universal retrofits to comply with tightening safety checks. Suppliers position pre-programmed kits that clone original IDs, bypassing long relearn cycles and reducing workshop time. The latent pool of aging vehicles, therefore, sustains baseline demand, especially in densely populated regions where inspection compliance is strictly enforced.

Surge In Online Tire and Parts Retail-Platforms Targeting DIY Sensor Swaps

Domestic e-commerce giants are undercutting dealership prices on universal sensors, attracting budget-conscious drivers. Owners can now invest in compact programming tools to seamlessly pair new sensors during seasonal wheel changes, effectively distributing the tool's cost across several vehicles. With transparent pricing and user reviews heightening competition, traditional brick-and-mortar outlets are responding by bundling services such as lifetime relearn support and extended warranties to safeguard their market share.

Growing SUV / EV Tire Upgrades (More Than 18-Inch) Requiring New Multi-Frequency Sensors

Hankook Tire reported that a significant share of new-vehicle tire sales was for 18-inch or larger tires, reflecting the growing popularity of SUVs and electric vehicles (EVs). Larger wheels are commonly associated with European imports that use a specific frequency, whereas domestic brands use another frequency. To address this difference, service centers are increasingly using dual-frequency programmable sensors. These sensors streamline inventory management while catering to nearly the entire spectrum of vehicles. Consequently, the trend toward higher-value tire upgrades is boosting the average ticket size for each replacement cycle in South Korea's aftermarket Tire Pressure Monitoring System (TPMS) market.

Fleet-Telematics Bundles Now Bundling Bluetooth-Le Smart TPMS for TCO Reduction

Start-ups such as BANF, partnering with KORE Wireless, are embedding BLE sensors that transmit data to cloud dashboards[2]“BANF Partnership Announcement,” KORE Wireless, korewireless.com. These dashboards link pressure, temperature, and tread wear data to specific route profiles. Pilot fleets have reported reductions in fuel consumption and extensions in tire life, achieving a return on investment within a short period. The credibility of these integrated telematics systems is reinforced by ISO standards, pushing logistics operators to incorporate smart TPMS into their new contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently High Labor Cost | -2.3% | Urban service centers, metropolitan areas | Short term (≤ 2 years) |

| Model-Year Protocol Fragmentation | -1.8% | South Korea nationwide, affecting all vehicle brands | Medium term (2-4 years) |

| Cyber-Security and Data-Privacy Concerns | -1.2% | Urban areas with high connected vehicle adoption | Medium term (2-4 years) |

| RF Congestion | -0.8% | Seoul, Busan, Daegu metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistently High Labor Cost For Sensor Fitment and ECU Relearn

Service centers charge a range for dismounting, valve replacement, and balancing, with additional programming fees applied per visit. Dealerships, positioned at the higher end of the pricing spectrum, emphasize their use of guaranteed OEM parts and the added benefit of liability coverage. In contrast, independent shops are turning to aftermarket sensors, allowing them to offer more competitive pricing. Rising labor costs are delaying proactive replacements. This, in turn, is extending service intervals and moderating short-term volumes in South Korea's aftermarket TPMS market.

Model-Year Protocol Fragmentation Causing Frequent Compatibility Failures

Kia’s 2025 SUV line shifts to a proprietary sensor security handshake, instantly rendering popular multiprotocol components like Hamaton HTS-3600 unusable. Retailers scramble to stock distinct SKUs per VIN range, bloating inventory and tying up cash. Schrader rushes out EZ-sensor firmware updates, but service bays still face mismatch errors because head units reject cloned IDs. When warning lamps persist after installation, customer dissatisfaction rises, leading to re-visits that erode installer profits. The fragmentation forces the South Korean aftermarket TPMS market to incur higher R&D and logistics overhead, which ultimately translates into price increases that could slow discretionary upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct Systems Maintain Dominance Despite Indirect Growth

Direct systems captured 67.28% of the South Korean aftermarket TPMS market share in 2025, underpinning segment leadership. Battery-powered valve-stem sensors stream absolute pressure and temperature values, offering real-time alerts favored by OEMs and performance-oriented drivers. However, each depleted battery triggers a full sensor swap, inflating lifetime costs. Indirect TPMS, forecast to clock a 16.09% CAGR through 2031, exploits existing ABS wheel-speed sensors and avoids in-tire hardware. Recent algorithms reduce false positives, attracting fleet buyers seeking lower maintenance overhead. As a result, indirect solutions will steadily chip away at volumes, while direct TPMS will continue to command premium prices in the South Korean aftermarket.

Indirect adoption also benefits rural workshops that lack advanced programming tools, as calibration requires only ECU resets after tire rotations. Yet the inability to display absolute pressure values limits integration with emerging telematics dashboards. Consequently, suppliers bundle indirect software with optional BLE add-ons that elevate functionality when budgets permit, creating a tiered upgrade ladder across vehicle ownership cycles.

By Technology Integration: Smart Solutions Drive Future Growth

Stand-alone modules retained 57.16% of the South Korean aftermarket TPMS market share in 2025, owing to broad compatibility and lower unit prices. They meet UNECE R64 compliance without external connectivity and are therefore the default replacement part for budget-minded motorists. In contrast, smart/connected TPMS is set to grow at a 16.28% CAGR as fleets value real-time dashboards and predictive analytics. As BLE and eSIM modules become more affordable in bulk, the market for smart sensors in South Korea's aftermarket TPMS is expected to grow significantly.

Data from commercial pilots indicate that maintaining optimal pressure variance can lead to significant fuel savings and extend tire life. These measurable benefits support strong payback models, positioning connected TPMS as the preferred choice for new logistics contracts. However, costs associated with cyber-hardening, such as advanced encryption and rotating IDs, slightly increase the bill of materials compared to traditional standalone units. Suppliers that ensure end-to-end security certification are poised to achieve higher margins throughout the forecast period.

By Vehicle Type: Commercial Segment Emerges as Growth Driver

Passenger cars accounted for 72.11% of the South Korean aftermarket TPMS market share in 2025, owing to the enormous installed base dating back to the 2013 mandate. Replacement demand peaks as early sensors enter end-of-life and SUV owners install larger wheels that require new sensors. The South Korean aftermarket TPMS market for passenger cars, therefore, remains substantial, even as unit ASPs trend downward.

Commercial vehicles are on course for the fastest growth, with a 16.16% CAGR through 2031. ISO has officially incorporated TPMS into its telematics compliance standards for freight carriers, prompting widespread retrofitting across fleets. The primary value lies in minimizing downtime and ensuring regulatory compliance, making smart TPMS a crucial factor in total cost of ownership assessments. Suppliers offering integrated sensing for pressure, temperature, and tread depth are gaining favor with long-haul operators, especially those covering significant distances each year.

By Distribution Channel: Digital Transformation Reshapes Market Access

Offline venues, dealerships, national tire chains, and neighborhood garages accounted for 65.78% of the South Korean aftermarket TPMS market share in 2025. Their enduring appeal lies in professional mounting equipment, wheel balancing, and on-the-spot ECU relearn capabilities. Still, high labor costs and travel time encourage price-sensitive consumers to pivot online, particularly for straightforward sensor swaps during seasonal wheel changes.

Online portals are expected to grow at a 16.33% CAGR, driven by transparent pricing, next-day delivery, and tutorial-rich product pages. Universal programmable sensors priced at USD 20-40 undercut OEM units by more than half, widening the DIY audience. To retain relevance, physical workshops now advertise flat-fee installation packages for sensors bought online, creating hybrid service models that blend e-commerce convenience with professional fitment confidence.

Geography Analysis

Seoul's capital region, with its dense vehicle population and stringent inspection regime, leads South Korea's aftermarket TPMS market. Workshops in Gyeonggi Province see a surge in activity during the spring and fall tire-change seasons, as vehicle owners switch between all-season and winter wheels. The area's high concentration of SUV-class vehicles boosts the demand for dual-frequency programmable sensors, catering to both domestic and imported models.

Incheon’s port, alongside Busan’s logistics hub, underpins the long-haul freight industry, driving a swift adoption of smart TPMS among trucking fleets. Fleet operators who incorporate sensor data into their route-optimization algorithms have noted significant drops in both idling times and tire-related roadside issues. Additionally, government subsidies for CNG-powered delivery vans that mandate on-board TPMS further bolster this trend in the maritime provinces.

In smaller cities like Daegu, Daejeon, and Gwangju, there's a noticeable uptick in online TPMS orders, as e-commerce platforms tackle last-mile delivery hurdles. Younger drivers in university towns, characterized by their digital savvy and fewer workshops, show a pronounced inclination towards DIY TPMS installations. With fiber-optic broadband and same-day courier services becoming ubiquitous, the once-varying intervals for sensor replacements across regions are aligning, paving the way for a consistent growth trajectory in South Korea's aftermarket TPMS market.

Mordor Intelligence tracks the aftermarket tpms market across other major regions such as Europe, with additional country-level coverage spanning China, India, United States, and Japan, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Sensata-Schrader commands mindshare through its OEM lineage, offering programmable EZ-sensor SKUs stocked in every major distributor’s catalog. Continental couples sensors with a SaaS dashboard sold alongside digital tachographs, generating annuity revenue that rivals hardware margins. Denso covers Japanese-badged imports that populate expat-heavy districts, giving it a stable niche. Korean champions Hyundai Mobis and CUB Elecparts exploit just-in-time logistics, slashing lead times for emergency resupply when new Kia protocols appear with little warning.

Protocol churn is both a weapon and a risk. Kia’s 2025 handshake change vaulted Hyundai Mobis to first-mover advantage for months, but Sensata’s firmware patch restored parity by year-end. Start-up BANF targets premium fleets unwilling to tolerate any unscheduled tire downtime. Its predictive-wear telemetry integrates with Volvo Trucks’ global cloud, securing credibility beyond domestic borders. Continental reacts by previewing a radar-aided sidewall stress-monitor launching mid-2026, signaling a pivot to multi-sensor fusion rather than standalone TPMS.

Cybersecurity is emerging as the new battlefield. Hyundai AutoEver markets subscription scanning for connected sensors that cannot host onboard encryption. Sensata invests in edge authentication chips expected to debut in 2027. As suppliers embed software into hardware, the mix of recurring revenue shifts the economics of the South Korean aftermarket TPMS market, rewarding firms that sustain both coding talent and manufacturing scale.

South Korea Aftermarket TPMS Industry Leaders

Continental AG

Autel Intelligent Technology

Sensata Technologies, Inc. (Schrader)

Cub Elecparts Inc.

Hyundai Mobis Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BANF and KORE Wireless introduced an advanced TPMS that utilizes BLE and AI analytics. They claim it delivers significant fuel savings and a considerable reduction in downtime for pilot fleets.

- July 2025: Bitsensing signed an MoU with KAIST AVE Lab and ZetaMobility to commercialize an AI-powered 4D imaging radar that integrates with TPMS data in advanced ADAS systems.

South Korea Aftermarket TPMS Market Report Scope

The South Korea TPMS market report is segmented by type (direct TPMS and indirect TPMS), technology integration (stand-alone TPMS units and smart/connected TPMS), vehicle type (passenger cars and commercial vehicles), and distribution channel (offline and online). The market forecasts are provided in terms of value (USD).

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart / Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sports Utility Vehicles and Multi Purpose Vehicles | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Offline |

| Online |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart / Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sports Utility Vehicles and Multi Purpose Vehicles | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Distribution Channel | Offline | |

| Online | ||

Key Questions Answered in the Report

How large is the South Korea aftermarket TPMS market in 2026?

The market is expected to grow from USD 67.01 million in 2025 to USD 77.77 million in 2026, on course for a 16.05% CAGR through 2031.

Which TPMS technology is growing the fastest?

Smart/connected sensors are expanding at a 16.28% CAGR as fleets integrate tire data with telematics dashboards.

Are cybersecurity features becoming mandatory?

While not yet mandated, encrypted telemetry is emerging as a competitive differentiator after studies exposed tracking risks in unencrypted TPMS broadcasts.

Are smart or stand-alone sensors preferred?

Stand-alone units dominate today, yet smart/connected sensors are growing at 16.28% CAGR due to BLE and OTA capabilities.

Which sales channel is winning incremental revenue?

Online marketplaces post the quickest gains, climbing at a 16.33% CAGR as same-day delivery erodes traditional channel advantages.

Page last updated on: