Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.11 Billion |

| Market Size (2030) | USD 5.12 Billion |

| Growth Rate (2025 - 2030) | 10.51% CAGR |

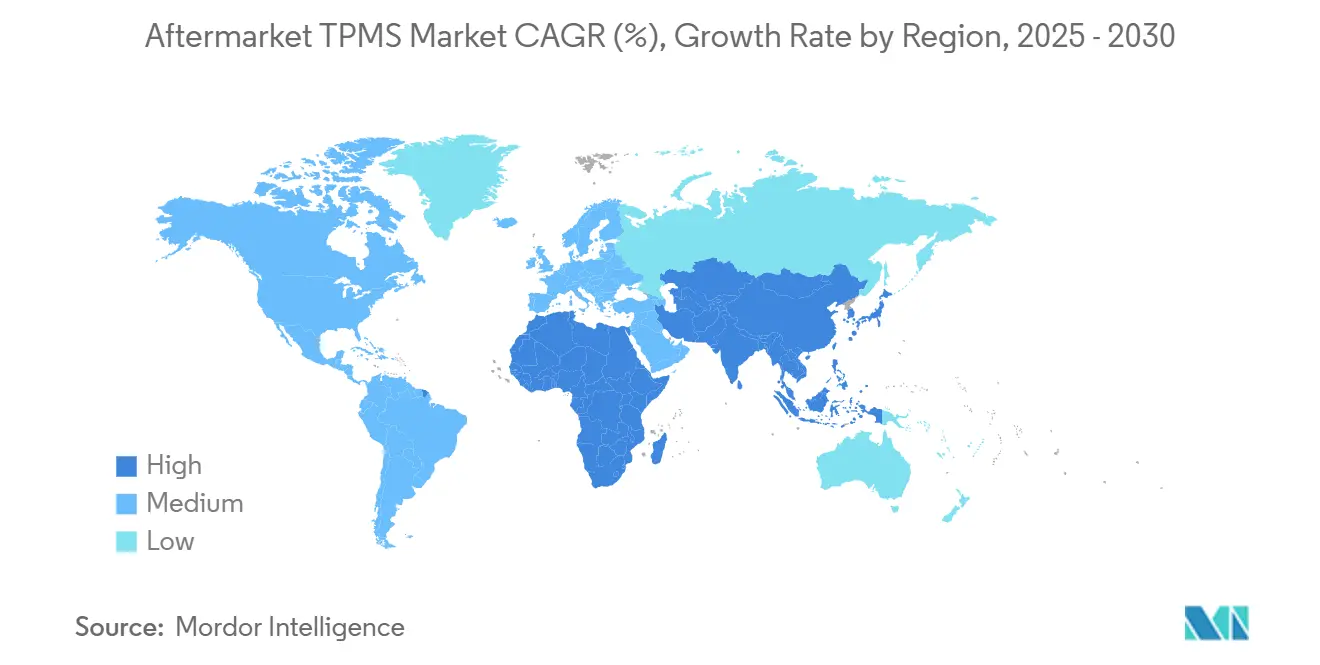

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

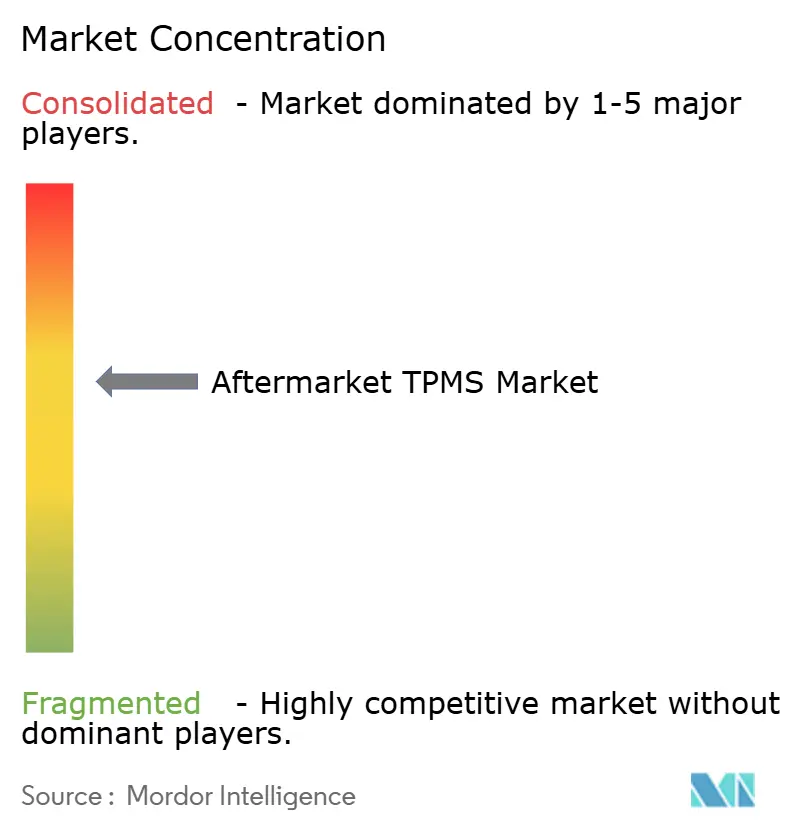

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aftermarket TPMS Market Analysis by Mordor Intelligence

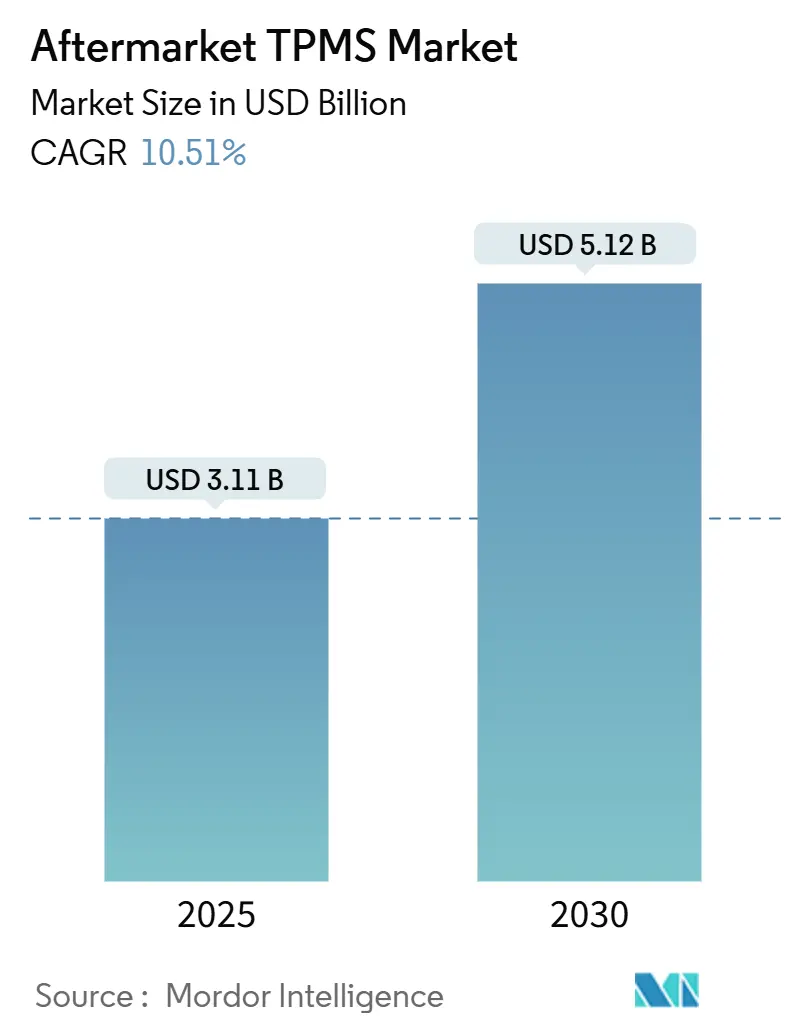

The Aftermarket TPMS market size reached USD 3.11 billion in 2025 and is set to climb to USD 5.12 billion by 2030, translating into a healthy 10.51% CAGR for the forecast period. Momentum stems from the convergence of regulatory enforcement, the rising average age of the global vehicle fleet, and rapid digitization that folds tire data into wider connected-vehicle ecosystems. Sensor batteries installed during the 2007-2012 regulatory wave are now expiring, creating a predictable replacement surge that runs parallel to first-time mandates in China and India. Cost-sensitive regions encourage localized chip production—as shown by the AutoChips-X-FAB collaboration—while North America and Europe emphasize feature-rich replacements that integrate pressure, temperature, and tread analytics. Across all regions, e-commerce channels are capturing a bigger slice of the Aftermarket TPMS market as do-it-yourself buyers rely on online tutorials and same-day delivery to overcome installation complexity.

Key Report Takeaways

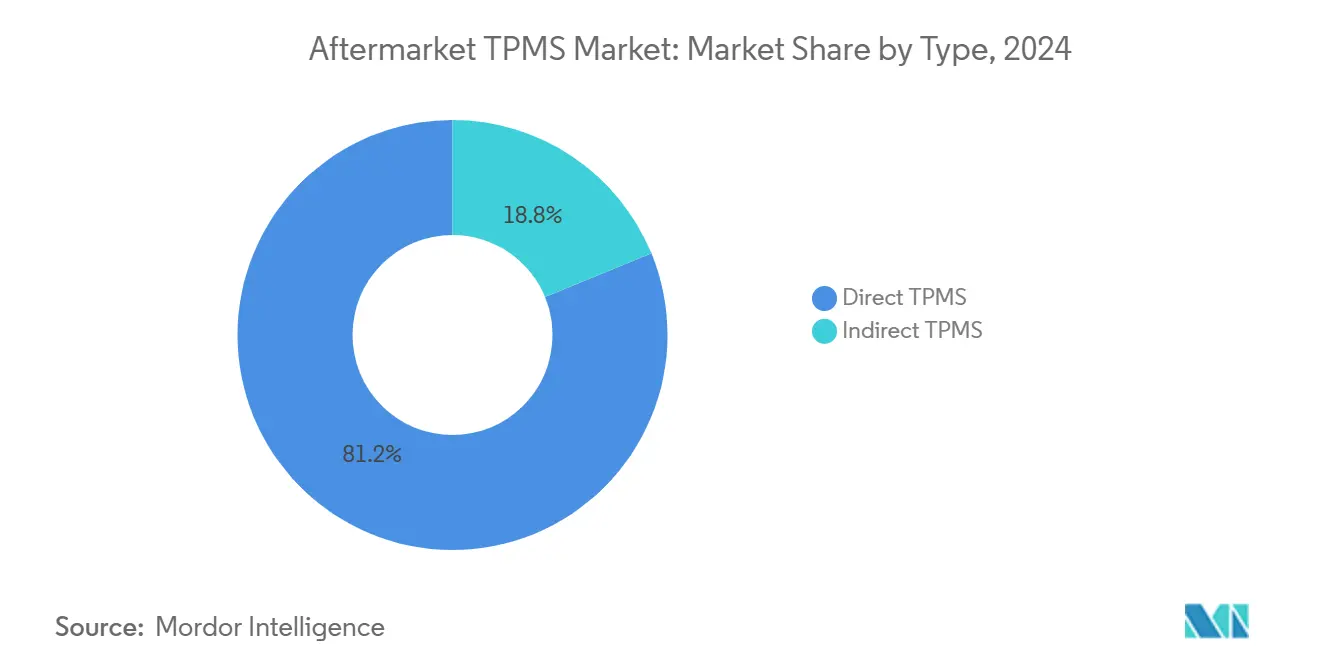

- By technology, direct TPMS retained 81.24% of the Aftermarket TPMS market share in 2024, and is projected to expand at a 10.87% CAGR through 2030.

- By technology integration, stand-alone units accounted for 72.33% of the Aftermarket TPMS market size in 2024, while smart/connected systems are projected to expand at a 14.04% CAGR between 2025 and 2030.

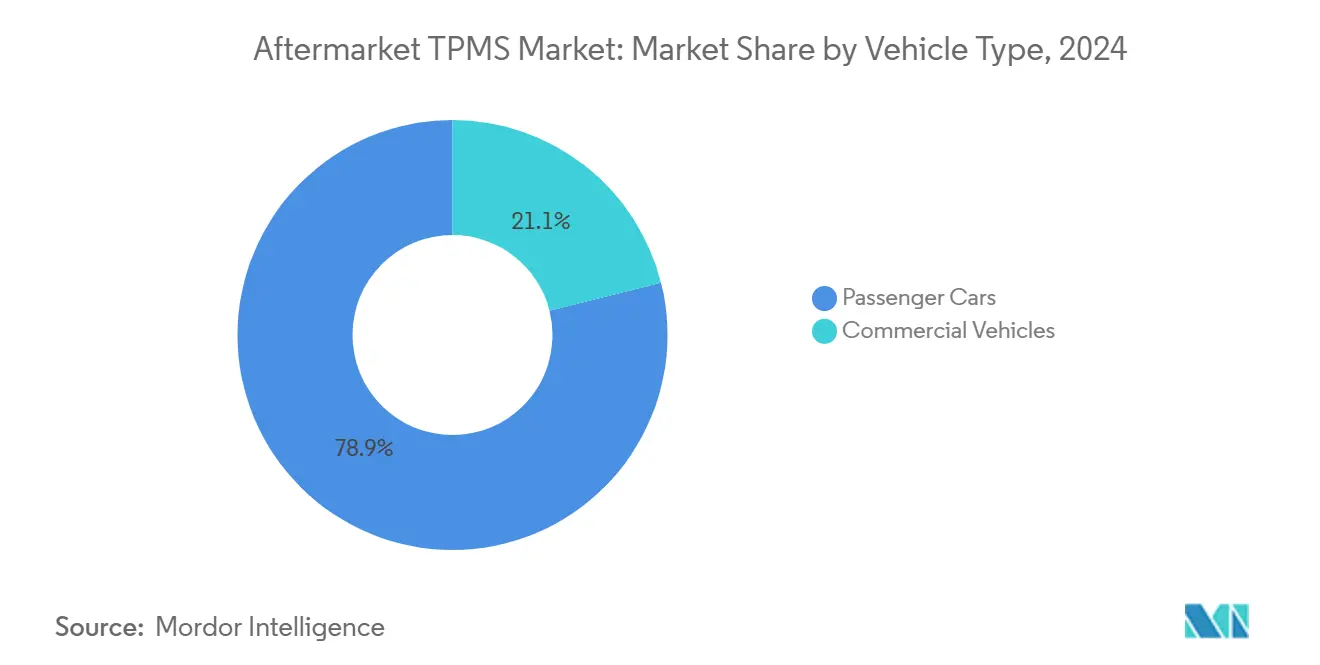

- By vehicle category, passenger cars led with 78.89% revenue share of the Aftermarket TPMS market in 2024; commercial vehicles are set to advance at a 13.52% CAGR to 2030.

- By sales channel, offline outlets controlled 66.25% of the 2024 Aftermarket TPMS market, yet online platforms are growing at a 13.84% CAGR.

- By geography, Europe captured 37.38% of the global Aftermarket TPMS market revenues in 2024, while Asia Pacific is projected to grow at a 15.08% CAGR through 2030.

Global Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TPMS Mandates for Fitment | +3.2% | Global, early gains in North America and the EU, expanding to the Asia Pacific | Long term (≥ 4 years) |

| Older Vehicles Drive TPMS Demand | +2.8% | Global, strongest in emerging markets | Medium term (2-4 years) |

| Smart TPMS in Connected Cars | +2.1% | North America and the EU leading, Asia Pacific following | Medium term (2-4 years) |

| E-commerce Grows Aftermarket Channels | +1.9% | Global, fastest in urban areas | Short term (≤ 2 years) |

| Fleet Predictive Maintenance with TPMS | +1.5% | North America and the EU, spreading to Asian commercial hubs | Medium term (2-4 years) |

| Telematics Insurance for Tire Data | +0.9% | North America and the EU, pilot projects in the Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for TPMS Fitment

Legally required tire-pressure monitoring sets the floor for the Aftermarket TPMS market expansion. The U.S. TREAD Act obligated new cars below 10,000 lb to carry TPMS from September 2007, and the European Union did the same for M1 vehicles from November 2014. As those first-generation sensors reach 15-18 years of service, owners face little choice but to replace batteries or full modules. China enforced TPMS on new cars starting January 2020, and India is drafting parallel guidelines, ensuring the next wave of replacements will record double-digit demand growth well past 2030 [1]Schrader TPMS Solutions, “Mandate Tracker and Replacement Forecast,” schradertpmssolutions.com. Commercial-vehicle mandates are still limited, yet voluntary uptake is increasing as fleet managers link tire health to fuel savings and uptime. Overall, mandates secure a stable revenue baseline and lessen cyclicality in the Aftermarket TPMS market.

Rising Global Vehicle Parc and Average Vehicle Age

Global light-vehicle circulation keeps setting records, while average age edges upward because owners weigh repair over replacement in the face of economic uncertainty. Each extra year on the road pushes sensors closer to battery depletion, reinforcing a rolling cadence of service visits. The trend is most visible in South America and Southeast Asia, where owners often keep vehicles beyond 15 years. Extended ownership cycles convert into sustained sensor sales, valve-stem kits, and programming services, helping the Aftermarket TPMS industry secure long-tail revenue even when new-car sales slow.

Surge in Connected-Vehicle Architectures Enabling Smart TPMS

Automakers now design cars around centralized connectivity hubs that welcome Bluetooth-Low-Energy, cellular V2X, and Wi-Fi modules, allowing TPMS data to flow into dashboards, cloud servers, and smartphone apps [2]Samsara, “Connected Fleet 2025 Report,” samsara.com. This infrastructure jump-starts smart TPMS retrofits that add tread-wear, alignment, and temperature analytics. Fleets leverage these data streams to schedule just-in-time tire rotations and eliminate blowout-related downtime. The Aftermarket TPMS market gains pricing power because connectivity unlocks software subscriptions that complement one-off hardware sales.

Growth of E-commerce Aftermarket Channels

E-commerce is rewriting distribution as parts portals, marketplace aggregators, and OEM webshops shorten the path between sensor manufacturers and end users. Algorithm-based product recommendations guide buyers to vehicle-specific sensors, while how-to videos demystify relearn procedures. Accelerated last-mile logistics in urban zones deliver sensors within hours, making online buying increasingly viable for urgent repairs. Brick-and-mortar outlets answer with click-and-collect models that fuse digital ordering and on-site installation, further enlarging the Aftermarket TPMS market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Sensitivity in Price Regions | -2.1% | Asia Pacific core, South America, parts of the Middle East, and Africa | Short term (≤ 2 years) |

| Competition from Smart Tire Tech | -1.3% | Global, first in premium segments | Long term (≥ 4 years) |

| Rapid Obsolescence from Vehicle-to-Cloud | -0.8% | North America and the EU, selective Asia Pacific markets | Medium term (2-4 years) |

| Cybersecurity Worries with Connected TPMS | -0.6% | EU, North America, spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensor and Service Cost Sensitivity in Price-Driven Regions

In emerging economies, replacement sensors can exceed a household’s monthly maintenance budget, prompting drivers to disable warning lights rather than purchase new units. Labor scarcity further inflates service charges, and counterfeit-sensor availability introduces safety risks while diluting legitimate vendor revenue. Localization of chipset fabrication and simplified installation kits are bridging the affordability gap, yet cost pressure remains the largest hurdle to holistic Aftermarket TPMS market penetration.

Competition from Integrated Smart/Airless Tire Technologies

Airless tire prototypes now embed structural elements that resist punctures and include micro-sensors as standard. Premium electric vehicles are likely first adopters, potentially bypassing the need for separate TPMS hardware. Although commercial readiness remains several years away, the prospect disciplines aftermarket pricing and nudges suppliers to enrich sensors with additional diagnostics that stand apart from new tire technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct TPMS leadership amid indirect acceleration

Direct systems contributed 81.24% of the revenue to the Aftermarket TPMS market in 2024, underpinned by their real-time accuracy and multi-parameter sensing capabilities. The Aftermarket TPMS market size for direct assemblies is projected to grow at a CAGR of 10.87% by 2030, following a steady replacement curve, supported by established calibration tools in service bays worldwide. Battery swaps require sustained workshop visits every 5-7 years and generate recurring income for valve-stem accessory makers.

Indirect TPMS is reliant on wheel-speed algorithms rather than in-tire sensors. Lower unit cost and simple fitment favor emerging economies and budget fleets. As microcontroller precision improves, pressure-loss detection thresholds narrow, closing the performance gap that once relegated indirect systems to niche status. The Aftermarket TPMS market benefits because indirect options entice penny-pinching owners who would otherwise ignore malfunction lamps altogether.

By Technology Integration: Smart systems disrupt stand-alone dominance

Stand-alone units still held 72.33% of the Aftermarket TPMS market share in 2024, thanks to a sizable installed base and universal compatibility. Many drivers prioritize straightforward pressure alerts, particularly where cellular reception is patchy. However, smart-connected kits are pacing at a 14.04% CAGR by weaving tire data into fleet dashboards, smartphone apps, and insurer portals.

Suppliers bundle Bluetooth-Low-Energy modules, over-the-air firmware, and tread-depth probes, converting sensors from passive safety devices into active data nodes. Subscription revenue from analytics dashboards cushions hardware margin compression and extends vendor relationships beyond the initial sale.

By Vehicle Type: Commercial growth outpaces passenger car base

Passenger cars continue to anchor the Aftermarket TPMS market, contributing 78.89% in 2024, a legacy of universal mandates in the United States and Europe. Replacement demand follows a clock-like rhythm as OEM-equipped sensors reach the end of their battery life.

Despite starting from a smaller base, commercial fleets are advancing at a 13.52% CAGR because fuel, tire, and downtime savings are easily quantified. Trailer-specific kits and extended-range antennas answer the unique challenges of multi-axle combinations. As more logistics firms link TPMS alerts to maintenance management software, adoption will broaden to medium-duty urban delivery fleets.

By Distribution Channel: Online platforms scale rapidly

Offline retailers, including tire shops, wholesale distributors, and car dealers, retained 66.25% of 2024 revenue. Professional programming tools, vehicle relearn procedures, and sensor-torque guidelines keep many owners reliant on trained technicians.

Online channels, nonetheless, present a 13.84% CAGR opportunity. Marketplace listings now bundle vehicle lookup tools that trim selection errors, while same-day couriers handle urgent breakdown orders. The Aftermarket TPMS market benefits from hybrid models such as order-online-install-offline, which combine pricing transparency with expert service.

Geography Analysis

The Asia Pacific region will increase faster than any other territory at a 15.08% CAGR. Government mandates, rising disposable income, and local chip fabrication underpin growth. Asia Pacific started 2025 with nearly half of all Aftermarket TPMS market revenue, and regulators in China and India are rolling out fitment deadlines that will create a multi-million-unit service wave by 2027. Local chipsets cut retail prices, aligning with demand from first-time car buyers who still rank safety features high when inflating tires every fortnight. Price erosion is balanced by volume spikes, enabling component makers to scale without sacrificing profitability [3]X-FAB, “China’s First Domestic TPMS Chipset,” x-fab.com.

Europe recorded similar maturity by accounting for 37.38% of the global revenue in 2024, yet consumer expectation for lower CO₂ emissions incentivizes adopters to pick sensors that integrate rolling-resistance analytics. GDPR compliance drives encryption as a default, allowing European suppliers to charge a premium for cybersecurity-certified hardware. In Eastern Europe, cost sensitivity encourages indirect kits, generating a two-tier market where advanced features and value engineering coexist.

North America’s Aftermarket TPMS market revolves around replacements. Sensors first sold under the TREAD Act window began aging out in 2022, sending a steady flow of vehicles to service bays for battery swaps. The push toward connected fleets accelerates smart-sensor penetration, particularly among e-commerce delivery companies chasing uptime guarantees.

Mordor Intelligence provides coverage of the aftermarket tpms market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China, India, United States, South Korea, and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The top five suppliers control a significant share of global sales, indicating moderate concentration. Schrader (Sensata Technologies) leads by longstanding OEM ties that lower validation hurdles for its aftermarket portfolio. Continental AG follows, leveraging its electronics expertise while enhancing online configurators that steer buyers to correct part numbers.

Other incumbents invest in wireless protocol upgrades that avoid cross-brand relearn tools, simplifying installer workflow and building stickiness. Patents around antenna geometry, pressure algorithms, and low-power chips protect margins against low-cost entrants. Start-ups like BANF address niche segments like heavy-duty trucking, proving that specialization can still carve out share despite formidable incumbents.

Cybersecurity capabilities are emerging as a key differentiator. Vendors that embed cryptographic keys and secure-boot firmware into sensors find favor with fleets and insurers wary of signal spoofing. This trend intertwines hardware and software, steering suppliers toward platform business models that monetize over-the-air services long after initial sale.

Aftermarket TPMS Industry Leaders

Sensata Technologies (Schrader)

Infineon Technologies AG

DENSO Corporation

ZF Friedrichshafen AG (TRW)

Hamaton Automotive Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Schrader TPMS Solutions introduced AirCheck BLE, an app-based universal retrofit kit that pairs OE-level performance with mobile diagnostics.

- March 2025: Schrader launched OE replacement sensors for Hyundai, Kia, and Genesis applications.

- September 2024: Continental revealed ContiConnect Lite and Pro at IAA Transportation, adding mobile and full-suite options to its digital tire-management range.

- January 2024: BANF partnered with Integre Trans to roll out the Intelligent Tire Profile System on European truck fleets.

Global Aftermarket TPMS Market Report Scope

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart/Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Offline - Parts Stores, Specialty Shops, Service Centers |

| Online - OEM Sites/Apps, E-commerce Platforms |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart/Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUV and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Distribution Channel | Offline - Parts Stores, Specialty Shops, Service Centers | |

| Online - OEM Sites/Apps, E-commerce Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will replacement demand become by 2030?

Installed sensors from early mandates will bring the Aftermarket TPMS market to USD 5.12 billion by 2030, underpinned by a 10.51% CAGR.

Which segment is growing fastest?

Connected or smart TPMS units are pacing at 14.04% CAGR because fleets seek data-rich tire intelligence.

Are commercial vehicles required to use TPMS?

Regulations remain limited, yet fleets adopt systems voluntarily to cut fuel and tire costs, driving a 13.52% CAGR in commercial applications.

What role does cybersecurity play in adoption?

Encryption and secure firmware are now essential as connected sensors interface with cloud platforms, especially under EU GDPR rules.

Page last updated on: