Europe Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

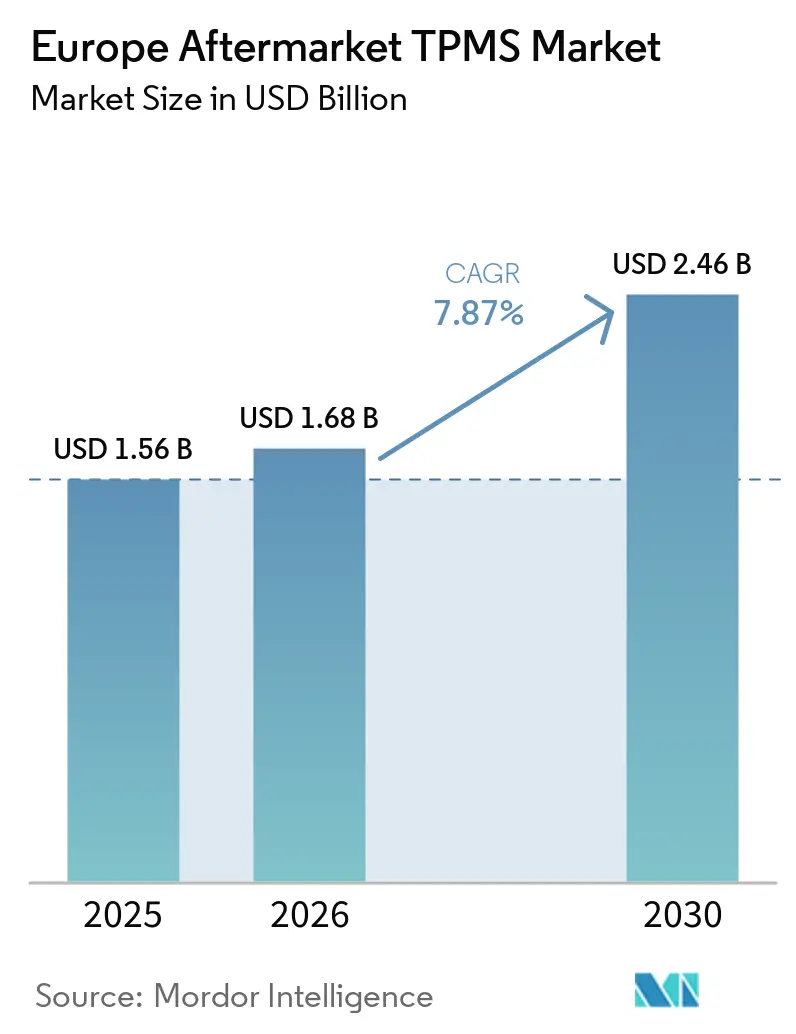

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2030) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 7.87% CAGR |

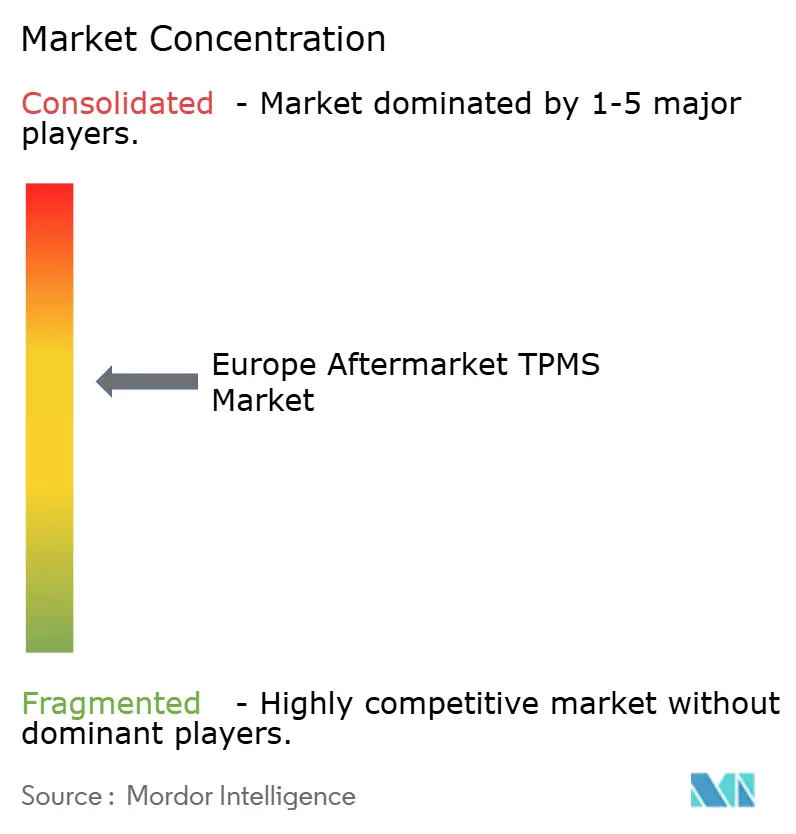

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aftermarket TPMS Market Analysis by Mordor Intelligence

The European aftermarket market size is projected to grow from USD 1.56 billion in 2025 to USD 1.68 billion in 2026, and is forecast to reach USD 2.46 billion by 2031, growing at a CAGR of 7.87% from 2026 to 2031. Stricter UNECE R141 mandates for trucks and trailers, coupled with the rapid expiration of sensors and batteries in an aging vehicle fleet, are driving momentum in the industry. Additionally, the increasing adoption of connected diagnostics, which convert tire-pressure data into ESG metrics, underscores this trend. Competitive pressures are mounting as universal programmable sensors are undercutting OEM units. These sensors allow smaller distributors to stock a single SKU compatible with most vehicles, diminishing the catalog advantage once held by established brands. While cost-sensitive fleet operators are leaning towards indirect Tire Pressure Monitoring Systems (TPMS) for their legacy vans, direct systems remain crucial in scenarios where regulations mandate pressure-loss detection within a tight time frame. Furthermore, telematics-ready sensors that can be upgraded over the air are paving the way for subscription revenue streams, helping suppliers counter hardware margin compression[1]“NTM88Kxx5S Tire Pressure Monitor Sensor, Rev 4.0,” NXP Semiconductors, NXP.com.

Key Report Takeaways

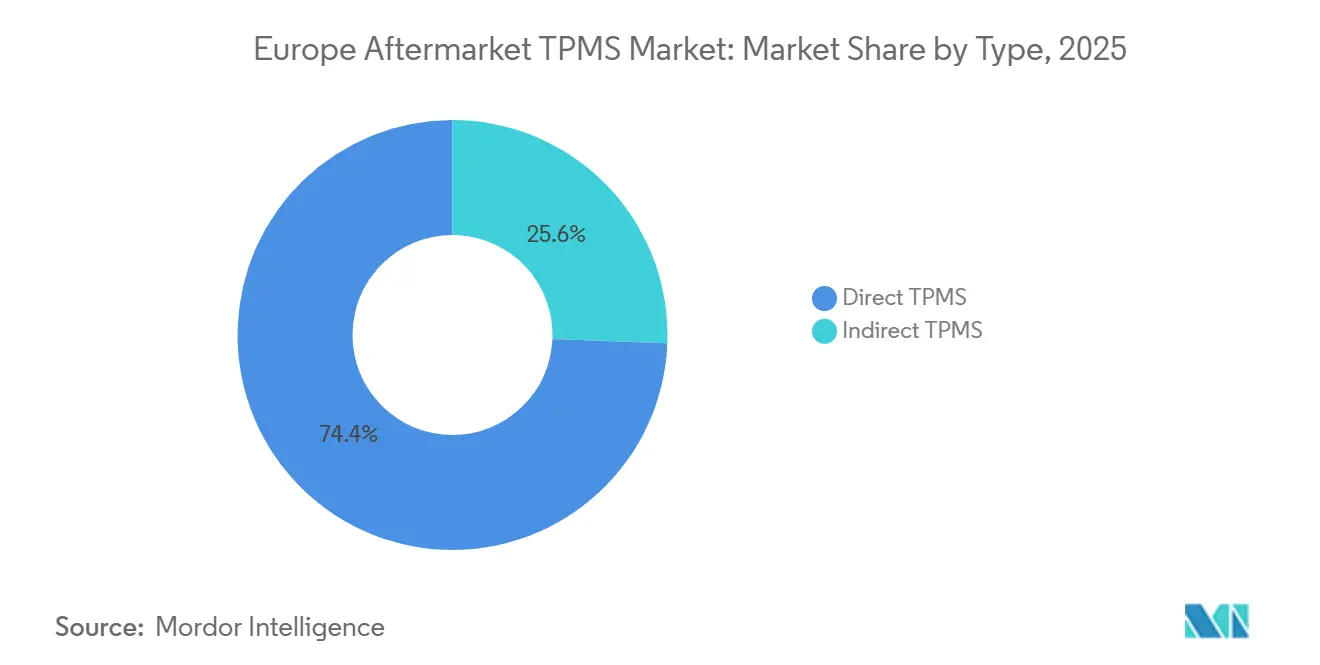

- By type, direct TPMS led the European aftermarket market with 74.38% market share in 2025, while indirect TPMS is forecast to expand at an 8.14% CAGR through 2031.

- By technology integration, stand-alone units held 57.19% of the European aftermarket market share in 2025, whereas smart/connected TPMS is projected to grow fastest at an 8.05% CAGR through 2031.

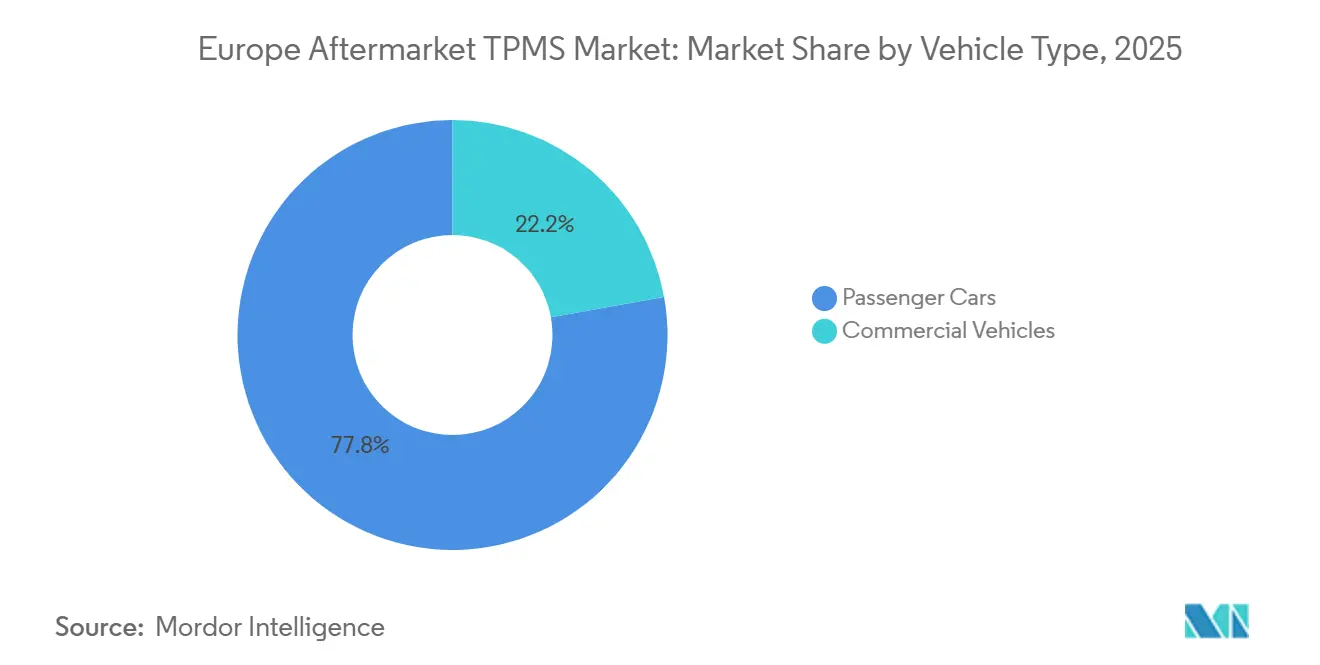

- By vehicle type, passenger cars accounted for 77.83% of the European aftermarket market size in 2025, yet commercial vehicles are set to record an 8.23% CAGR to 2031.

- By distribution channel, offline outlets captured 71.28% of the European aftermarket market share in 2025, but online platforms are growing at a 8.27% CAGR through 2031.

- Geographically, Germany dominated the European aftermarket market with 24.21% of the market size in 2025, whereas France is poised to deliver the highest 7.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The aftermarket tpms market share in our global report expresses these relative weights.

Europe Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Vehicle PARC Prolongs Sensor Replacement Demand | +2.1% | Europe-wide, concentrated in Western Europe | Medium term (2-4 years) |

| EU Regulation ECE 661/2009 Replacement-Cycle Pull | +1.8% | Pan-European, strongest in Germany, France, UK | Long term (≥ 4 years) |

| Rising Consumer Focus on Tire-Safety | +1.2% | Northern Europe leading, Southern Europe following | Medium term (2-4 years) |

| Fleet-Wide ESG Reporting Needs Real-time Pressure Data | +1.1% | Corporate fleets across major EU markets | Short term (≤ 2 years) |

| OTA-Upgradeable Connected TPMS Kits | +0.9% | Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| E-commerce Parts Channels Widen Access | +0.6% | Pan-European with UK, Germany leading adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Vehicle Parc Prolongs Sensor Replacement Demand

The average age of passenger cars in Europe has increased, with some regions reporting significantly older vehicles. This trend has led many first-generation direct sensors to exceed their typical battery life. To maintain affordability in repairs, workshops in cost-sensitive areas are increasingly using universal programmable sensors. This approach supports a sustained replacement trend expected to continue for the foreseeable future.

EU Regulation ECE 661/2009 Replacement-Cycle Pull

In Germany, France, and the Netherlands, periodic inspections now treat non-functional TPMS as failures, turning regulation into a reliable revenue source for service providers and manufacturers. This regulatory enforcement ensures that vehicles comply with safety standards, driving demand for TPMS maintenance and replacement. The extension of UNECE R141 to trucks and trailers signals a second compliance wave, benefiting direct TPMS that can meet the alert threshold. This development is expected to create growth opportunities in the market as fleet operators and OEMs prioritize compliance to avoid penalties and enhance operational safety.

Rising Consumer Focus on Tire Safety and Fuel Economy

Electric vehicle (EV) owners can see a noticeable drop in driving range when their tires are under-inflated, as highlighted on their energy-consumption dashboards. Underinflated tires increase rolling resistance, leading to higher energy consumption and reduced efficiency. Yet, owing to Bluetooth-enabled kits such as Continental's ContiConnect Lite, drivers can now keep tabs on tire pressure straight from their smartphones, underscoring the cost savings of prompt tire replacements[2]“Continental Launches ContiConnect Lite,” Tyrepress Newsdesk, Tyrepress.com. These advancements not only enhance convenience but also improve vehicle performance and safety.

OTA-upgradeable Connected TPMS Kits

Software-defined sensor platforms convert TPMS from one-time hardware sales into recurring data services. Bartec’s WiFi-enabled RITE-SENSOR modules already push calibration updates remotely, while NXP’s S32 CoreRide roadmap signals mass-market arrival of ultra-low-power UWB chips able to move tire-pressure data directly into vehicle zonal gateways. Predictive alerts based on slow-leak patterns promise lower downtime for last-mile fleets and new revenue shares for sensor vendors that bundle analytics subscriptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sensor & Labour Cost | -1.4% | Pan-European, acute in high-wage markets | Short term (≤ 2 years) |

| EV-Specific High-Pressure Tyres | -0.9% | EV adoption leaders: Norway, Netherlands, Germany | Medium term (2-4 years) |

| Accuracy Issues with Indirect TPMS Erode Confidence | -0.8% | Markets with high indirect TPMS adoption | Medium term (2-4 years) |

| Cyber-Risks in Connected Sensors | -0.6% | Connected vehicle markets, regulatory scrutiny zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Sensor and Labor Cost for Relearn/Programming

In Poland, many customers delay repairs even when dashboard warnings signal issues, primarily because replacing sensors is costly, especially when labor and programming are factored in. Additionally, encryption on BMW and Tesla systems compels workshops to either purchase OEM parts or invest in advanced tools, further driving up service bills.

EV-Specific High-Pressure Tires Create Compatibility Gaps

To counterbalance their heavier curb weights, electric vehicles (EVs) require higher tire pressures. However, installations often face pressure errors, a challenge particularly pronounced with indirect Tire Pressure Monitoring Systems (TPMS). These systems frequently struggle to interpret wheel-speed patterns during regenerative braking. While NXP's chips address this hardware gap, the software relearning process often demands tools typically found at dealerships. This dependency limits independent shops' involvement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct Systems Dominate Despite Indirect Growth

Direct TPMS commanded 74.38% of the European aftermarket market share in 2025, owing to real-time, wheel-specific alerts demanded by UNECE rules. Indirect systems priced 40–50% lower are growing at an 8.14% CAGR as operators of pre-2014 vans seek low-cost compliance, particularly in Southern Europe.

Over the forecast period, the EU TPMS aftermarket market for indirect TPMS is projected to accelerate as algorithm refinements reduce false positives. Yet, gaps in absolute-pressure measurement limit uptake to cost-sensitive fleets. Semiconductor advances, such as NXP’s AEC-Q100-qualified NTM88K, are cementing direct TPMS as the long-term default across heavy-duty vehicles, reinforcing the leadership position of direct solutions in the European aftermarket market.

By Technology Integration: Connected Systems Gain Traction

Stand-alone valves held 57.19% of the European aftermarket TPMS market size in 2025 as installers favored simpler re-learn processes that do not require pairing with telematics gateways. Universal-fit SKUs from Schrader and Huf keep inventory overhead low, sustaining loyalty among independent workshops.

Connected TPMS revenue will advance at an 8.05% CAGR on the back of ESG-driven data reporting and predictive maintenance contracts. The European aftermarket TPMS market share for connected kits could grow significantly if subscription prices become more affordable per vehicle per month. Fleet managers, hesitant about mid-cycle sensor swaps, may find NXP's UWB architecture appealing, offering a notable improvement in battery life.

By Vehicle Type: Commercial Segment Accelerates

Passenger cars continued to dominate, accounting for 77.83% of the European aftermarket market share in 2025, reflecting Europe’s scale in the parc. Luxury SUVs and crossover trims have standardized temperature-compensated direct sensors, pushing the average sensor ASP slightly higher than compact hatchbacks.

Commercial vehicles are forecast to compound at 8.23% CAGR as mandatory fitment on new vans took effect in 2024. The European aftermarket TPMS market size for light commercial vans alone is set to experience exponential growth by 2030, with parcel-delivery fleets citing a 3-month payback when proactive pressure alerts prevent sidewall blowouts on multi-stop routes.

By Distribution Channel: Digital Transformation Accelerates

Offline counters retained a 71.28% of the European aftermarket market share in 2025, due to the hands-on nature of relearn cycles. Tire-service specialists in Germany install an average of 14 sensors daily during winter peaks, supported by Continental’s wireless tablet, which slashes programming time to under 30 seconds per wheel.

With an 8.27% CAGR, click-and-collect models energize online sales, where drivers purchase universal valves through platforms such as AUTODOC and schedule fittings at affiliated garages. The Europe aftermarket TPMS market share transacted online will double by 2031 as AI-driven fitment advisors reduce model-lookup errors to below 1%.

Geography Analysis

Germany remains the epicenter of demand, with 24.21% market share in 2025, driven by strict TÜV inspections and high vehicle density. The European aftermarket TPMS market, derived solely from Germany, is set to grow drastically in 2026, accounting for almost one-fifth of regional revenue. Sensor ASPs are one-tenth above EU averages thanks to premium workshop labor rates and willingness to upsell connected kits.

The United Kingdom and France form the second tier, while France leads the forecast period with a 7.94% CAGR through 2031. Brexit-induced customs frictions initially inflated lead times, but the 2025 adoption of streamlined OE-equivalency declarations has stabilized inventory flow into UK jobbers. France’s BEV sales mix is spawning niche demand for high-pressure, silicone-coated valve stems, widening the European aftermarket TPMS market.

Southern Europe, including Italy and Spain, presents untapped potential. Older average fleet ages push sensor failure incidents higher, yet lower disposable incomes restrain immediate replacement. Government inspection reforms scheduled for 2026 are expected to tighten TPMS test rigor, smoothing revenue visibility. Central-Eastern clusters led by Poland are leveraging duty-free warehousing to redistribute sensors to Baltic and Balkan retailers, thereby shrinking delivery windows from 5 days to 72 hours.

Mordor Intelligence examines the aftermarket tpms market across diverse other regional markets as well, offering granular country-level perspectives for China, India, United States, South Korea, and Japan and more.

Competitive Landscape

Tier-1 suppliers like Continental, Sensata-Schrader, and Huf are leveraging their OEM pedigree to set industry standards and tap into the lucrative connected-services revenue stream. In contrast, universal-sensor vendors such as Autel, ATEQ, and Bartec are challenging these price premiums by providing a single SKU that covers most vehicles. While Sensata boasts a significant global OEM share, Autel's aggressive free-tool trade-in campaign underscores the potential to sway workshop loyalty through bold platform strategies.

Current technology roadmaps emphasize OTA firmware updates, Bluetooth connectivity, and stringent cybersecurity compliance. Notably, NXP's advanced chip is pivotal, allowing suppliers to consolidate both passenger-car and heavy-duty offerings into a unified architecture [3]“TECH450 Next Generation TPMS Tool,” Bartec Auto ID, Bartecautoid.com. The market remains moderately fragmented, with the top players collectively holding a substantial share, resulting in a moderate concentration score for the European TPMS aftermarket.

Europe Aftermarket TPMS Industry Leaders

Continental AG

Huf Hulsbeck & Furst

Alligator Ventilfabrik

Bartec Auto ID

Sensata Technologies, Inc (Schrader)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Aumovio Germany GmbH has secured a 7-year contract with Triton Valves Limited to provide TPMS valves. Under the terms of the agreement, Triton will supply 470 million valves over 2027-2031, anticipating revenues of approximately INR 1,120 million (USD 11.98 million) over the contract duration.

- September 2025: POLYN Technology unveiled its VibroSense Tire Monitoring Solution at IAA Mobility 2025. Designed for real-time tire-road friction analysis, VibroSense TMS is currently being tested on certified tracks. These tests, covering a range of tires and road surfaces, have effectively identified shifts in the peak friction coefficient (PFC).

Europe Aftermarket TPMS Market Report Scope

The European aftermarket TPMS market report is segmented by type (direct TPMS and indirect TPMS), technology integration (stand-alone TPMS units and smart/connected TPMS), vehicle type (passenger cars and commercial vehicles), and distribution channel (offline and online). The market forecasts are provided in terms of value (USD).

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart/Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sports Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs) | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Offline |

| Online |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart/Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sports Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs) | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will the EU TPMS aftermarket market be by 2031?

The market is forecast to reach USD 2.46 billion by 2031, rising from USD 1.56 billion in 2025 to USD 1.68 billion in 2026 at a 7.87% CAGR.

Which TPMS technology is growing fastest in Europe?

Smart/connected TPMS is projected to grow at an 8.05% CAGR, outpacing the broader market as fleets demand telematics integration and OTA updates.

Which TPMS technology is growing fastest?

Indirect systems are projected to grow at an 8.14% CAGR through 2031, mainly due to the cost-driven uptake among commercial fleets.

Why are connected TPMS kits gaining traction?

Fleet ESG reporting and predictive maintenance needs are prompting operators to install sensors that can stream real-time pressure data into telematics dashboards.

What challenges could slow market growth?

High relearn labor costs, indirect system accuracy concerns, and emerging cyber-security compliance requirements pose near-term hurdles.

Page last updated on: