Automotive TPMS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

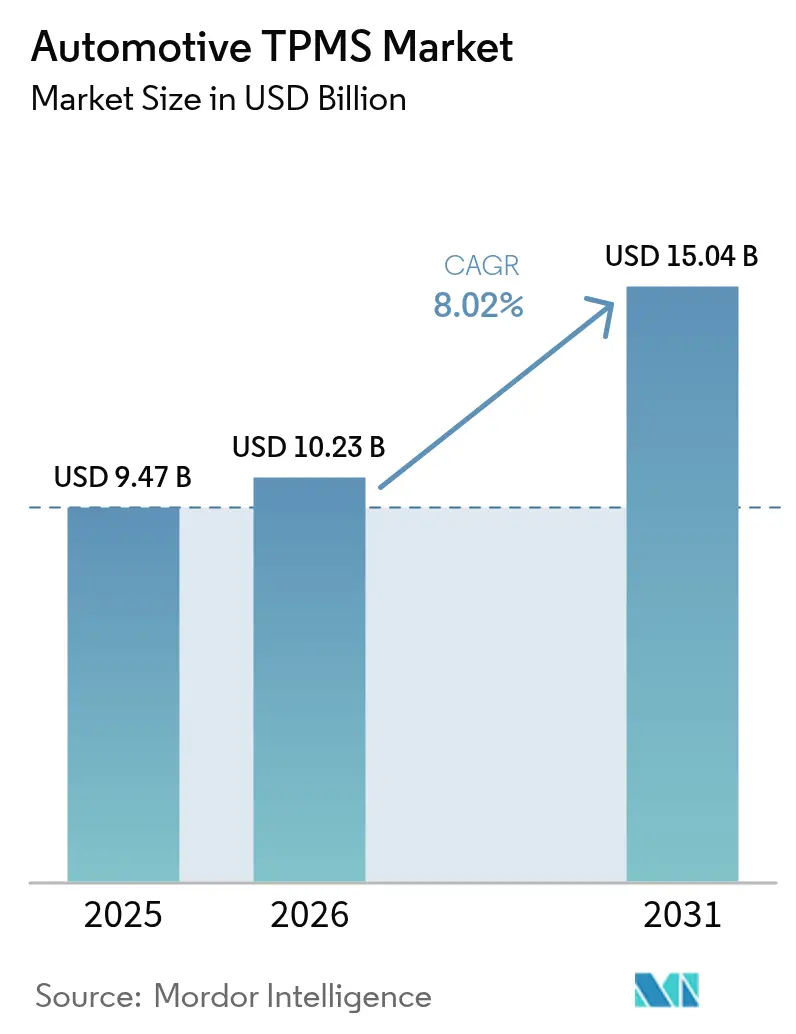

| Market Size (2026) | USD 10.23 Billion |

| Market Size (2031) | USD 15.04 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive TPMS Market Analysis by Mordor Intelligence

The Automotive TPMS market size is projected to expand from USD 9.47 billion in 2025 and USD 10.23 billion in 2026 to USD 15.04 billion by 2031, registering a CAGR of 8.02% between 2026 and 2031. Direct sensor architectures led revenue in 2025, yet the Automotive TPMS market is already pivoting toward embedded modules and ultra-wideband frequencies as connected-vehicle stacks grow. Electrification is magnifying range-loss penalties from under-inflation, encouraging automakers to treat tire telemetry as a core energy-management input. Fleets are bundling TPMS data with predictive-maintenance dashboards, while insurers are beginning to link tire-pressure compliance to premium discounts. Cybersecurity rules promulgated by UNECE are raising the bar for sensor authentication while also opening avenues for suppliers to differentiate by certifying secure over-the-air update pipelines.

Key Report Takeaways

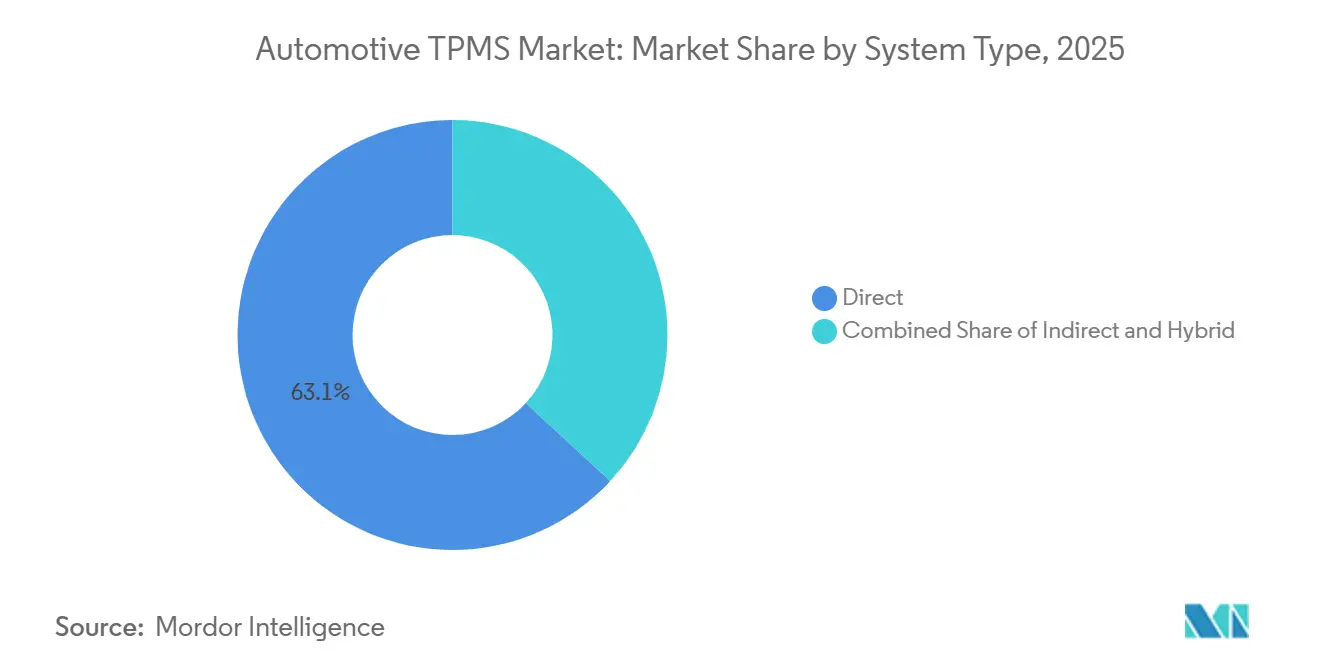

- By system type, direct solutions led with 63.11% of the Automotive TPMS market share in 2025; indirect-to-direct hybrids are projected to post the fastest 8.17% CAGR through 2031.

- By sensor technology, MEMS capacitive devices held 51.62% share of the Automotive TPMS market size in 2025, whereas piezoelectric technology is pacing an 8.23% CAGR to 2031.

- By fitting method, valve-stem mounting accounted for 67.25% of the Automotive TPMS market in 2025, and embedded-tire modules are expanding at an 8.25% CAGR through 2031.

- By frequency band, the 433 MHz class commanded 53.26% of the Automotive TPMS market share in 2025; 2.4 GHz + UWB frequencies are advancing at an 8.33% CAGR to 2031.

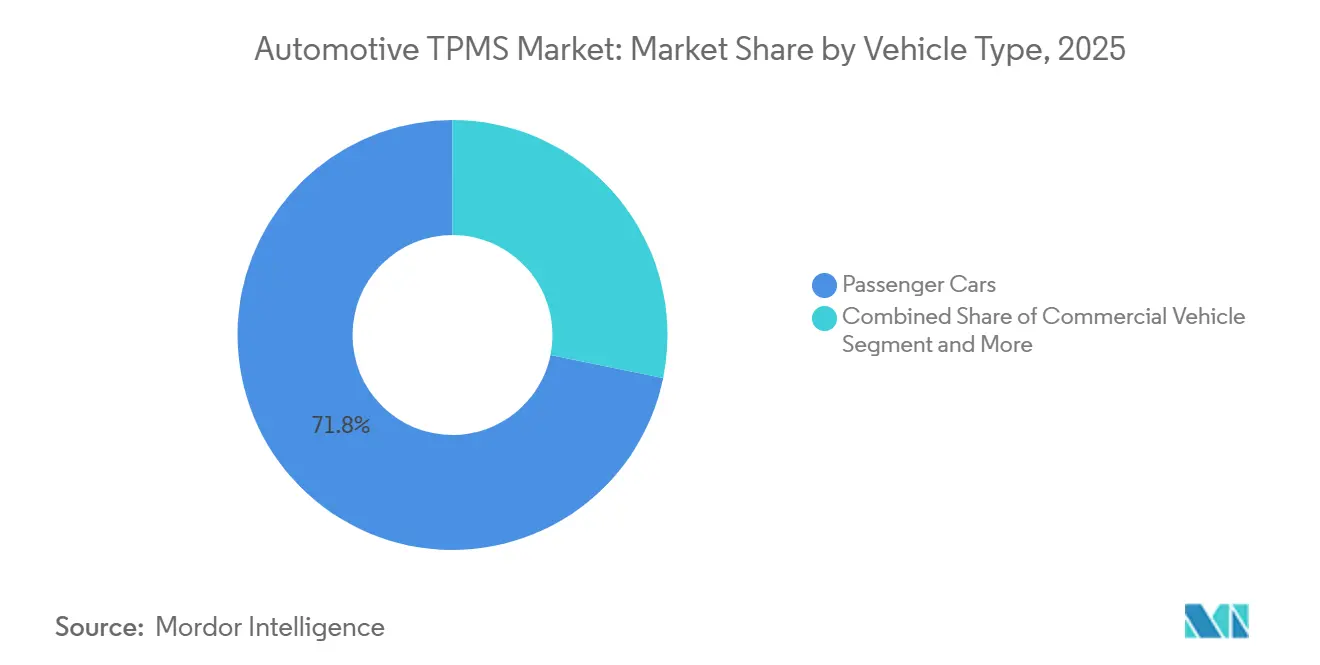

- By vehicle type, passenger cars dominated the Automotive TPMS market with 71.79% of the market share in 2025, while two-wheelers are forecast to grow at an 8.19% CAGR through 2031.

- By sales channel, OEM factory-fit installations accounted for 67.98% of the Automotive TPMS market in 2025, and the aftermarket retrofit route is growing at an 8.31% CAGR through 2031.

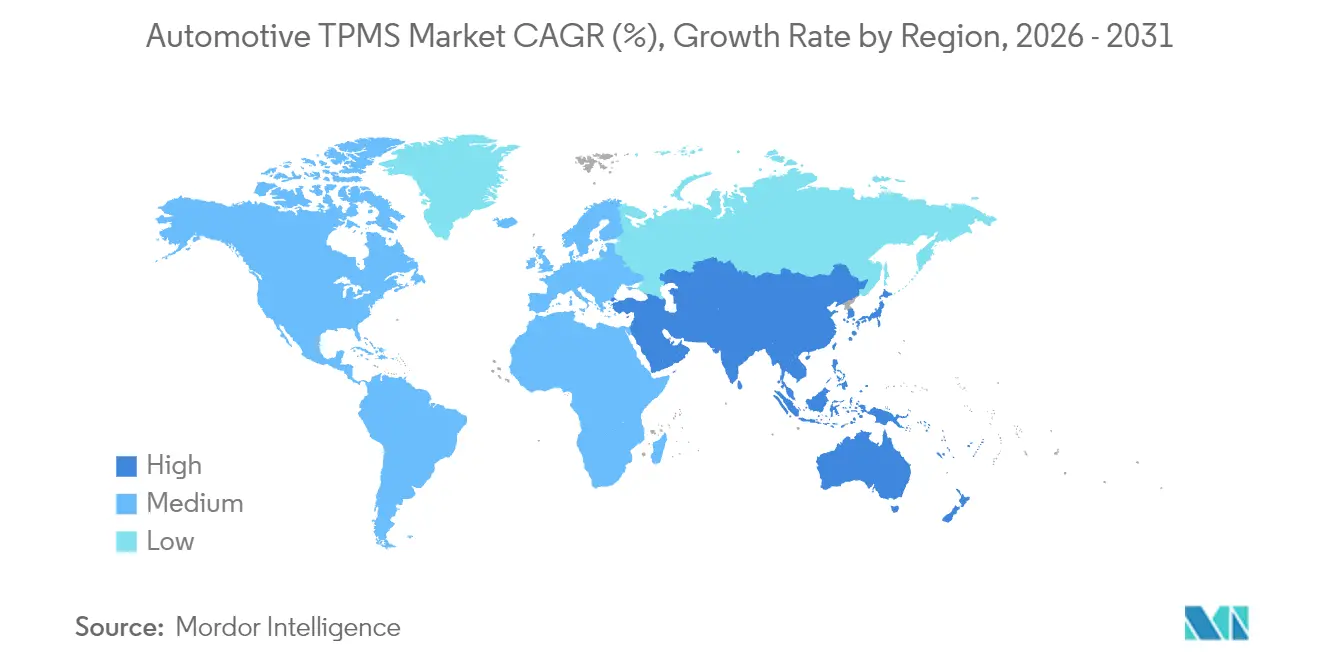

- By geography, North America accounted for 36.81% of the Automotive TPMS market in 2025, and the Asia Pacific is growing at an 8.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated TPMS Fitment | +2.1% | Global, with enforcement peaks in EU, North America, China, India | Medium term (2–4 years) |

| Integration with Connected-Car Telematics Platforms | +1.8% | North America, EU, APAC (China, Japan, South Korea) | Long term (≥4 years) |

| Weight-Sensitive Range Anxiety | +1.5% | Global, concentrated in EU, China, North America EV corridors | Medium term (2–4 years) |

| Smart-Tire Health-Analytics | +1.2% | North America & EU fleet operators; APAC emerging | Long term (≥4 years) |

| Low-Cost MEMS Sensors | +0.9% | APAC core (India, China, Southeast Asia) | Short term (≤2 years) |

| Insurance-Telematics Incentives | +0.7% | North America, EU; pilot programs in APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Mandated TPMS Fitment in New-Vehicle Safety Regulations

Global legislation continues to make TPMS an optional item into a compulsory homologation item. Regulatory expansion is widening beyond passenger cars into trucks, buses, and trailers, now mandated by the EU’s General Safety Regulation from July 2024[1]“Regulation (EU) 2019/2144 on type-approval requirements for motor vehicles,” Directorate-General for Mobility and Transport, europa.eu . In the United States, rules under FMVSS 138 keep all light vehicles under 10,000 lb within scope and have demonstrated fitment costs of USD 48.44–69.89 per unit[2]"FMVSS 138: Tire Pressure Monitoring Systems (TPMS)", NTEA, ntea.com. At the same time, China’s GB 26149 revision brings motorcycles and electric scooters into scope. India’s draft AIS 141 phases in direct measurement for two-wheelers over a multi-year window. These synchronized rules guarantee baseline demand, shielding the Automotive TPMS market from short economic swings and prompting sensor suppliers to scale capacity early.

Rising Integration with ADAS and Connected-Car Telematics Platforms

Centralized compute domains inside new vehicles now harvest TPMS telemetry for route planning, driver alerts, and fleet dashboards. Continental’s ContiConnect Pro, launched at IAA 2024, streams pressure, temperature, and tread data to cloud analytics that trigger maintenance work orders. Such integrations compel sensors to support Ethernet gateways and secure firmware, nudging the Automotive TPMS market toward higher-bandwidth designs. North American fleets lead adoption, yet European logistics operators are rapidly embedding tire data into cost-per-mile algorithms.

Electrification Increasing Weight-Sensitive Range Anxiety

Battery-electric models are significantly heavier than their combustion counterparts. As a result, under-inflated tires can noticeably reduce their driving range. In 2024, Continental expanded its TPMS capacity in Bangalore, emphasizing the importance of extending EV range with its second-generation sensors. Automakers are now incorporating tire pressure data into their range calculators, highlighting the direct impact of TPMS data on customer satisfaction. Regions like China and the European Union, with their strong EV adoption, are expected to benefit the most.

Shift Toward Smart-Tire Health-Analytics Ecosystems

Predictive analytics are repositioning TPMS from a cost center to a subscription revenue driver. Continental’s fleet platform provides automated alerts that link inflation patterns to fuel burn and tire wear, enabling fleets to defer replacements and negotiate usage-based tire leases. Suppliers that control both sensor hardware and cloud software gain recurring fees while improving vehicle uptime. Adoption is strongest in North American heavy-duty trucking, but early pilots in India and China show parallel momentum as logistics providers chase efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sensor and Calibration Cost | -1.3% | APAC (India, Southeast Asia), Latin America, Africa | Short term (≤2 years) |

| Cybersecurity Vulnerabilities | -0.9% | Global, with regulatory focus in EU, Japan, South Korea | Medium term (2–4 years) |

| Installation Complexity and Maintenance Issues | -0.6% | North America, EU aftermarket channels | Short term (≤2 years) |

| Airless and Run-Flat Technologies | -0.4% | Global, early adoption in commercial fleets and military | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Sensor and Calibration Cost in Entry-Level Segments

Entry-level cars and two-wheelers feel the pinch as sensor prices, along with installation labor, stretch budgets, making it challenging for manufacturers to offer cost-effective solutions. Though cheaper, indirect algorithms fail to meet the now-standard accuracy requirements, which are increasingly being enforced across various regions to ensure safety and reliability. While advancements in semiconductor scaling are gradually reducing unit costs, achieving cost parity with indirect systems remains a long-term goal. This delay continues to hinder widespread adoption in price-sensitive markets, particularly in rural India and certain regions of Africa, where affordability is a critical factor for consumers.

Wireless TPMS Cybersecurity Vulnerabilities

TPMS modules are vulnerable to spoofing and denial-of-service attacks due to unencrypted radio transmissions. While UNECE 155 mandates risk assessments and secure key storage, it also introduces additional engineering challenges. ISO/SAE 21434 goes a step further, emphasizing the importance of lifecycle cybersecurity engineering and urging suppliers to implement secure-boot and encrypted-messaging retrofits. These compliance costs burden smaller vendors, which could lead to reduced supplier diversity and decelerated innovation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Direct Systems Lead Integration Wave

Direct architectures accounted for 63.11% of revenue in 2025 and continue to expand at an 8.17% CAGR through 2031, driven by accurate in-tire pressure readings and regulatory endorsement. Direct sensors meet stringent error margins, making them the default for passenger cars in Europe, North America, and China. Indirect systems remain in low-cost vehicles but cannot detect simultaneous under-inflation across all wheels. Hybrid configurations, blending direct sensors with indirect algorithms, appeal to cost-sensitive commercial fleets that juggle payload variability.

In the Asia-Pacific region, new motorcycle regulations mandate real-time pressure data, significantly increasing the demand for direct sensors. The need for enhanced safety and compliance with evolving standards drives this surge. To address this demand, Continental has introduced its entry-level TPMS Go diagnostic tool, which allows aftermarket shops to efficiently pair sensors, thereby reducing installation complexities and time. While the adoption of hybrid systems might stabilize as sensor prices decline, many heavy-duty operators continue to favor the robustness and reliability of dual-mode setups, particularly for extended long-haul routes where durability is critical.

By Sensor Technology: Piezoelectric Innovation Disrupts Power Paradigms

MEMS capacitive devices held 51.62% share in 2025, prized for low power draw and CMOS compatibility. Piezoelectric sensors, although currently less dominant, are set to grow the fastest, at an 8.23% CAGR, as they can withstand extreme heat and vibration, making them ideal for heavy trucks. Strain-gauge solutions serve as a transitional option, appreciated for their linear output, though they face higher current consumption.

Continental’s Bangalore production line focuses on MEMS capacitive formats tailored for light vehicles, while Japanese suppliers are scaling up piezoelectric ceramics to meet the demands of harsh operating environments. Semiconductor availability plays a critical role in determining technology choice. MEMS devices benefit from established 8-inch wafer fabrication processes, whereas piezoelectric stacks rely on specialized ceramic supply chains. Over the forecast period, hybrid IC packages that integrate capacitive and piezoelectric elements are expected to emerge as a promising solution, offering a balance of resilience and accuracy.

By Fitting Method: Embedded Modules Enable Continuous Monitoring

Valve-stem assemblies accounted for 67.25% of installations in 2025, remaining the dominant retrofit-friendly form factor thanks to standard tire-service tools and technician familiarity. Band-mounted sensors secure a foothold in run-flat wheel wells, but their straps add weight and complicate balancing. Embedded-tire modules grow at an 8.25% CAGR, the quickest among fitting options, because they vanish inside the carcass, deter theft, and allow tire makers to sell data-rich service subscriptions. European truck fleets are trialing embedded suites that harvest tread-wear metrics at every rotation and feed them into tire-as-a-service contracts, tying payments to miles rather than pairs of rubber.

Adoption hurdles remain: embedded devices need new curing presses, must survive vulcanization temperatures, and force recyclers to separate electronics from rubber waste streams. Schrader’s heavy-duty clamp-in sensor, launched in November 2025, illustrates why valve-stem hardware still rules. OE interchangeability and quick roadside replacement keep downtime low for freight carriers. Nevertheless, sustainability regulations that monetize lifecycle traceability could tip the balance toward embedded SKUs by decade-end. If that pivot occurs, the Automotive TPMS market size attributable to embedded modules would multiply, redrawing competitive maps now weighted toward valve suppliers.

By Frequency Band: Higher Frequencies Enable Advanced Features

Units operating at 433 MHz held 53.26% shipment share in 2025, yet sensors working at or above 2.4 GHz are anticipated to post the strongest 8.33% CAGR. Legacy sub-gigahertz radios enjoy mature antennas, low penetration losses through steel bodywork, and harmonized type-approval rules. New vehicles adopting zonal architectures, however, appreciate 2.4 GHz chips that mesh with Bluetooth Low Energy stacks already on board, slashing gateway costs. UWB additionally supports centimeter-level ranging, enabling roadside weigh stations to interrogate tire status during rolling scans, an attractive feature inside the European Cooperative Intelligent Transport Systems roadmap.

Continental’s ContiConnect Pro leverages high-frequency links to stream minute-level updates into cloud dashboards, convincing logistics managers who juggle dozens of depots. Yet power-density limits vary across jurisdictions, obliging firmware to toggle duty cycles and reducing straight-line range in some markets. Component availability also factors: 433 MHz surface-acoustic-wave filters remain cheap and abundant, while automotive-qualified UWB SoCs occupy constrained foundry capacity. Despite those frictions, premium EVs and autonomous prototypes specify UWB to consolidate sensor fusion under a single time-synchronized clock, ensuring that high-band channels will continue to expand fastest across all frequency categories.

By Vehicle Type: Two-Wheelers Drive Emerging Market Expansion

Passenger cars accounted for 71.79% of sensors in 2025, after two decades of statutory mandates across OECD economies. However, two-wheelers are emerging as the fastest-growing segment, with an 8.19% CAGR through 2031, driven by regulatory changes in regions such as China, where new standards are accelerating the adoption of direct TPMS on motorcycles and electric scooters. Commercial trucks fall somewhere in between; they rely on pressure data to optimize fuel efficiency and minimize tire-related breakdowns, but their overall sensor usage remains lower than that of light vehicles.

Sensor miniaturization is critical for motorcycle rims that spin above 10,000 rpm and offer limited cavity space. Vendors race to shrink PCB footprints and battery cells without sacrificing signal strength, a design squeeze that benefits fabless teams with RF-in-package know-how. Fleet demand for truck TPMS stays robust as insurers roll out mileage-based premiums that penalize under-inflation events. Collectively, rising bike volumes and steady truck retrofits are widening the Automotive TPMS market even as passenger-car fitment nears saturation.

By Sales Channel: Aftermarket Retrofit Accelerates Fleet Adoption

OEM assembly lines accounted for 67.98% of units in 2025, reflecting automakers’ need to secure type approval before vehicles reach showrooms. The aftermarket records the highest CAGR of 8.31% because older fleets retrofit sensors to capture insurance discounts and meet tightening regional rules. Universal programmable SKUs reduce inventory headaches for distributors, letting one part flash multiple protocols via a handheld programmer. Continental’s TPMS Go handheld brings one-technician installs within reach of neighborhood garages, slicing downtime for vehicle owners who previously avoided sensor replacement costs.

Channel economics differ sharply: OEM contracts emphasize multi-year volume guarantees at slim margins, whereas aftermarket players pursue higher unit profitability amid fragmented demand. Warranty terms also sway buying behavior; factory sensors often carry five-year coverage, while many retrofit options offer only two years, pushing fleets to weigh capital costs against risk exposure. As the car parc continues to age in Europe and North America, retrofit penetration drives total shipment growth even as new-vehicle sales flatten, ensuring that the aftermarket remains the fastest-moving lane in the current Automotive TPMS market landscape.

Geography Analysis

North America retained 36.81% of the Automotive TPMS market revenue in 2025, reflecting an entrenched regulatory history and high vehicle ownership. Growth in the region now depends on telematics bundling and commercial-fleet adoption rather than new passenger-car fitment. The U.S. aftermarket is buoyed by an average vehicle age exceeding 12 years, while Canada shows parallel patterns in light-truck segments. Cybersecurity provisions under UNECE 155 do not bind U.S. domestic models, yet multinational OEMs voluntarily align to simplify export compliance.

Europe follows closely but with different dynamics. The General Safety Regulation broadened TPMS coverage to virtually every new light and heavy vehicle from July 2024. Retrofit demand spikes among cars registered before 2014 that lack factory sensors. Germany, France, and the United Kingdom rank highest in retrofit volumes, thanks to insurance rebates for verified tire pressure compliance. The region also leads in embedded-sensor pilots, motivated by sustainability targets that encourage circular tire-management schemes.

Asia-Pacific is the fastest-growing arena, advancing at an 8.35% CAGR through 2031. China’s extension of GB 26149 to motorcycles and electric scooters creates a multi-million-unit annual opportunity. Continental’s Bangalore line gives the company a local hub to meet surging OEM demand and export to South Korea. Japan and South Korea, both aligned with UNECE rules, emphasize cybersecurity certifications, rewarding vendors that can document ISO/SAE 21434 conformance.

Mordor Intelligence provides coverage of the automotive tpms market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

TPMS demand remains anchored in safety-led type-approval and performance requirements across major vehicle markets. In the United States, NHTSA enforces FMVSS No. 138 for light vehicles, requiring systems to warn drivers when tires are significantly under-inflated, which keeps OEM factory-fit adoption structurally embedded in new-vehicle programs.

In UNECE-aligned markets, UN Regulation No. 141 (R141) provides the technical framework used by many contracting parties, and it aligns with the European Union approach where Regulation (EU) 2019/2144 (General Safety Regulation) broadened safety feature requirements across vehicle categories starting July 2024. UNECE WP.29 discussions in 2026 around R141 supplement references to automated-driving definitions and test annex updates, pointing to a compliance shift from standalone warning functionality toward tighter integration with vehicle control and communications architectures. That direction raises the case for authenticated sensor messaging and robust validation during homologation.

Value Chain Analysis

The value chain starts with semiconductor and sensing inputs (MCUs/ASICs, MEMS elements, RF components, batteries, and valve hardware), then moves through module packaging and assembly, calibration and end-of-line testing, and ends with integration into OEM platforms or aftermarket kits. This integration is supported by tools for programming and relearn. Tier-1 suppliers and sensor brands (such as Continental, DENSO, Sensata Technologies/Schrader, Huf, and Pacific Industrial) sit between component makers and automakers, while diagnostic-tool providers and distributors extend aftermarket reach through universal programmable sensors and workshop equipment.

Supply continuity and qualification depth are persistent constraints because TPMS depends on automotive-grade electronics often built on mature-node capacity, alongside tightly specified RF and battery performance. In 2026, electronics allocation risk visible in broader automotive chip supply dynamics pushes OEMs and Tier-1s toward more flexible BOM strategies, additional approved vendors, and software-enabled calibration workflows that reduce SKU fragmentation. Downstream, channel execution, including dealer service lanes, independent workshops, and fleet maintenance, affects replacement velocity, since battery end-of-life and sensor pairing complexity shape retrofit economics and recurring service revenue.

Competitive Landscape

The Automotive TPMS market is poised for moderate consolidation, anchored by Continental, Sensata Technologies, Pacific Industrial, Huf, and DENSO. These leaders leverage deep OEM pipelines and global homologation portfolios to protect share. Continental’s July 2024 agreement with Samsara demonstrates the pivot from one-off hardware sales to subscription analytics, exchanging gross margin for sticky software revenue. Sensata’s recent report highlights its strong focus on research and development and its commitment to advancing electrification technologies for vehicles. The company has expressed a clear intent to enhance the capabilities of next-generation TPMS chips, showcasing its dedication to innovation and meeting the evolving needs of the automotive industry.

Second-tier contenders center on regional niches. Pacific Industrial dominates Japanese mini-vehicle fitment, while Huf supplies premium German brands that value lightweight clamp-in valves. Cybersecurity mandates under UNECE 155 invite specialty chipmakers that can embed hardware security modules into sensor ASICs, potentially disrupting the incumbent hierarchy. Meanwhile, tire manufacturers experiment with embedded modules to wrap data services into tire-as-a-service contracts, pressuring standalone sensor suppliers to prove added value beyond raw pressure readings.

Barriers to entry rest less on capital intensity and more on the scope of certification. ISO/SAE 21434 compliance audits and UN type-approval dossiers consume engineering bandwidth, deterring small firms. At the same time, aftermarket toolmakers eye retrofit growth, bundling TPMS diagnostics with broader OBD solutions. As ecosystems converge, the competitive narrative tilts toward software capabilities, cloud-to-edge encryption, and over-the-air update reliability rather than sensor bill of materials alone.

Automotive TPMS Industry Leaders

-

DENSO Corporation

-

Continental AG

-

Sensata Technologies (Schrader)

-

Huf Hülsbeck & Fürst

-

Pacific Industrial Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space shows up where compliance and accuracy requirements are rising faster than installed-base capability, particularly in two-wheelers and commercial fleets adding direct measurement rather than relying on indirect inference. Regional regulatory anchors, including U.S. FMVSS No. 138 and UNECE UN R141, along with the EU General Safety Regulation rollout from July 2024, keep OEM-fit volumes tied to type-approval cycles, while also creating follow-on opportunities in service and retrofit as vehicles age and sensors reach battery end-of-life.

Product and ecosystem moves from 2024-2026 point to a wider opportunity set beyond standalone warning functions. Connected fleet platforms (for example, Continental ContiConnect Pro showcased at IAA 2024) and smart-tire concepts are pulling TPMS into predictive maintenance, tire-as-a-service, and energy-management use cases, especially for heavier EVs where under-inflation translates into measurable range penalties. On the packaging side, integration-friendly designs such as tires built with sensor pockets (Continental commercial tire developments in 2026) and embedded smart tires introduced in India (JK Tyre, 2025) show how tire makers and sensor suppliers can package monitoring as a higher-value system. At the same time, cybersecurity requirements referenced in the report scope (UNECE R155 and ISO/SAE 21434) raise demand for secure sensor authentication and update mechanisms, which supports differentiation in OEM sourcing and fleet deployments.

Recent Industry Developments

- June 2026: Continental unveiled Sensor Ready commercial tires for the Conti Coach HA3 line with an integrated, factory-molded sensor pocket to simplify installation of digital tire monitoring hardware. By building the mounting interface into the tire, Continental reduces fitment friction and supports faster scaling of connected tire monitoring in commercial fleets where downtime and installation labor are critical.

- March 2026: DENSO expanded its First Time Fit aftermarket offering with 12 new TPMS sensor part numbers, extending coverage to an additional 14 million vehicles. Broader coverage increases replacement addressability as the vehicle parc ages and supports distributors and workshops seeking to standardize on fewer supplier lines while improving service fill rates.

- November 2025: Schrader introduced a heavy-duty TPMS portfolio for fleet and commercial vehicles, including sensors, valves, and the VT Truck 2.0 tool with integrated OBD-II functionality and Wi-Fi updates. The bundled hardware-and-tool approach strengthens Schrader's position in commercial-vehicle retrofits by reducing relearn complexity and keeping diagnostic capability current through over-the-air tool updates.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from tire pressure monitoring systems used in road vehicles, including the hardware and electronics that detect pressure changes and send alerts to the driver or vehicle system.

Scope exclusions: It does not include tire sales, wheel and rim assemblies, or broader vehicle safety electronics that do not perform tire pressure monitoring.

Segmentation Overview

-

By System Type

- Direct

- Indirect

- Hybrid

-

By Sensor Technology

- MEMS Capacitive

- Strain-Gauge

- Piezoelectric

- Others (Optical, SAW, etc.)

-

By Fitting Method

- Valve-Stem (Snap-In & Clamp-In)

- Band / Rim-Mounted

- Embedded-Tire Module

-

By Frequency Band

- 315 MHz

- 433 MHz

- More than or equal to 2.4 GHz & UWB

-

By Vehicle Type

- Passenger Cars

- Commercial Vehicle

- Two-Wheelers

-

By Sales Channel

- OEM Factory-Fit

- Aftermarket Retrofit

-

Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

For the initial market structure, we relied on public and official data that can be cross-checked, such as vehicle production and registration statistics from government transport agencies, road safety regulators, and customs trade databases where available. We also reviewed standards and rule documents that shape fitment requirements, along with trade association releases and technical papers that explain how direct and indirect monitoring works.

To ground the revenue model, we used secondary inputs from company filings, investor presentations, product brochures, and reputed automotive press coverage discussing feature adoption and replacement cycles. In parallel, we accessed paid subscriptions for company financials and intelligence, patent databases, and an import-export shipment-level database to validate supplier activity signals and the direction of sensor-related technology. The sources listed here are illustrative, and many other references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary discussions were conducted with stakeholders across the TPMS value chain, including component suppliers, module assemblers, vehicle OEM contacts, distributors, and service networks. These inputs helped confirm fitment rates by vehicle category, typical replacement behavior in the aftermarket, and realistic pricing movement for sensors and related modules across regions, so the assumptions remained practical.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 15% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down model where the global vehicle parc, new vehicle production, and TPMS fitment rules were translated into an addressable unit pool, and then converted into value using average selling price ranges by system type and channel. The totals were checked with selective bottom-up approximations, including sampled sensor and module volumes in key countries, channel checks for OEM versus aftermarket splits, and sanity checks based on supplier revenue exposure to TPMS-linked components.

We used practical inputs as main drivers, such as passenger car versus commercial vehicle build mix, penetration of direct versus indirect TPMS, OEM factory-fit share versus retrofit demand, replacement frequency tied to battery life and service cycles, and regional differences in frequency bands and compliance requirements. Where country-level data was missing, we filled gaps using proxy indicators like vehicle registrations and import patterns, then validated the resulting ranges during interviews. Forecasting leaned on scenario analysis with short multivariate checks, where expected vehicle production, regulation-driven adoption, and price-erosion assumptions were stress-tested before locking the final curve.

Data Validation & Update Cycle

Outputs were validated through multiple steps, starting with cross-checks against independent signals such as vehicle production trends, regional adoption shares, and channel-mix expectations that came up repeatedly in interviews. When a country or segment showed an unusual jump, we rechecked underlying drivers, reviewed price and unit assumptions, and then re-contacted sources if the variance could not be explained.

Before publication, the model and key assumptions go through analyst reviews to ensure the math ties out and the logic stays consistent across regions and years. The report is refreshed annually, with interim updates when material changes occur, such as regulation updates or sharp shifts in vehicle builds. A final review is completed prior to delivery so the client receives the most current view available.

Mordor Intelligence's Automotive Tpms Market Size Compared With Other Published Estimates

Published TPMS market sizes can differ even when they appear to cover the same space, because the included products, counted channels, and year definitions are not always aligned. Differences also show up when pricing is treated as a single global average instead of being tied to system type, vehicle mix, and OEM versus aftermarket behavior.

Replacement-only sensor revenue sits outside Mordor Intelligence's scope when it is reported as a standalone service item, which creates a gap versus estimates that blend service labor, kits, and adjacent tire electronics into one total. In addition, some publishers assume faster price increases or aggressive adoption curves for connected features without rechecking those assumptions against vehicle build data and channel feedback, and that can lift the near-term number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.47 B (2025) | |

| Global Consultancy A | USD 10.92 B (2025) | Uses a broader packaged definition that can roll OEM and aftermarket systems together with adjacent installation and kit value, and applies a higher growth path over the same base year. |

| Industry Publisher B | USD 8.01 B (2025) | Takes a narrower value pool by emphasizing core system components with conservative pricing, and the channel mix assumption leans heavily toward OEM shares that reduce aftermarket value contribution. |

Across the three figures, the spread mainly comes from what is counted around the core system, and how OEM versus aftermarket pricing and replacement behavior are treated. By tying the total to observable vehicle build and parc signals, and then stress-testing channel and ASP assumptions with interview feedback, our estimate remains easier to trace and repeat year after year.

Key Questions Answered in the Report

What CAGR will TPMS revenues post between 2026 and 2031?

The Automotive TPMS market is forecasted to grow at an 8.02% CAGR from 2026 to 2031.

Which system type holds the largest revenue share in 2025?

Direct TPMS accounts for 63.11% of 2025 sales and remains the dominant architecture.

What makes embedded-tire modules attractive?

They eliminate external hardware, reduce theft risk, and enable tire makers to bundle data services throughout the tire lifespan.

How do cybersecurity rules affect TPMS suppliers?

UNECE 155 and ISO/SAE 21434 require secure key storage and encrypted messaging, adding certification costs but creating differentiation for compliant vendors.

Are retrofit kits gaining popularity?

Yes, aftermarket retrofit is expanding at 8.31% as older vehicles seek compliance and fleets tie pressure data into insurance telematics.

Page last updated on: