Japan Aftermarket TPMS Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

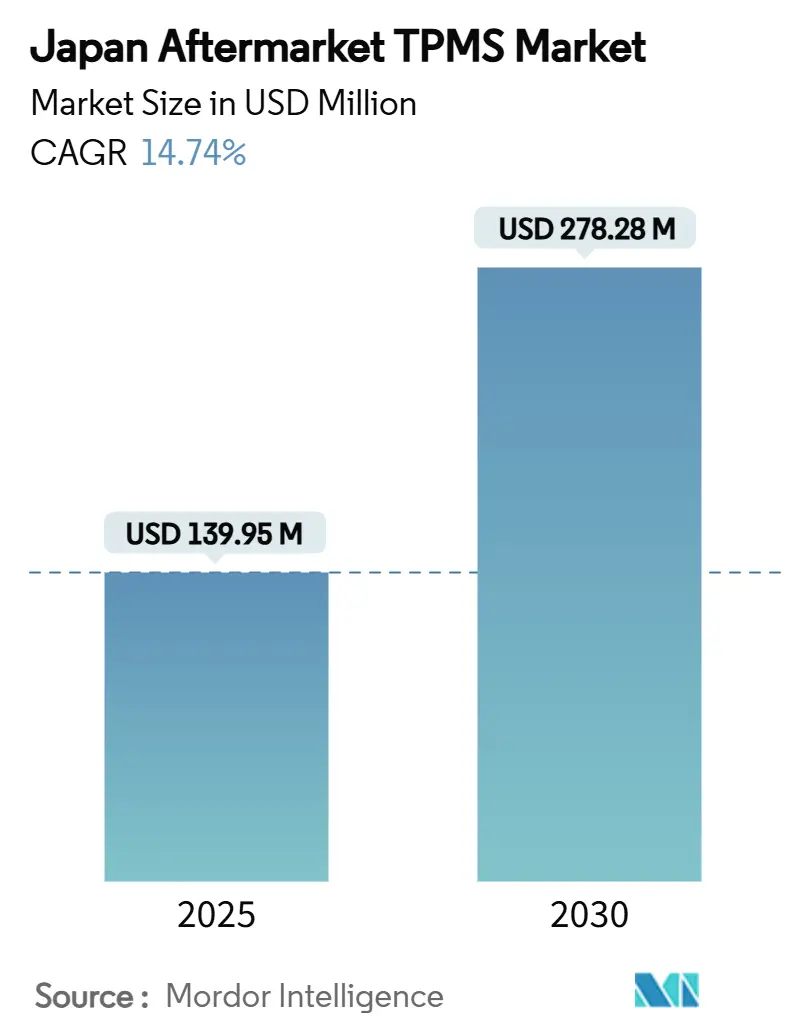

| Market Size (2025) | USD 139.95 Million |

| Market Size (2030) | USD 278.28 Million |

| Growth Rate (2025 - 2030) | 14.74% CAGR |

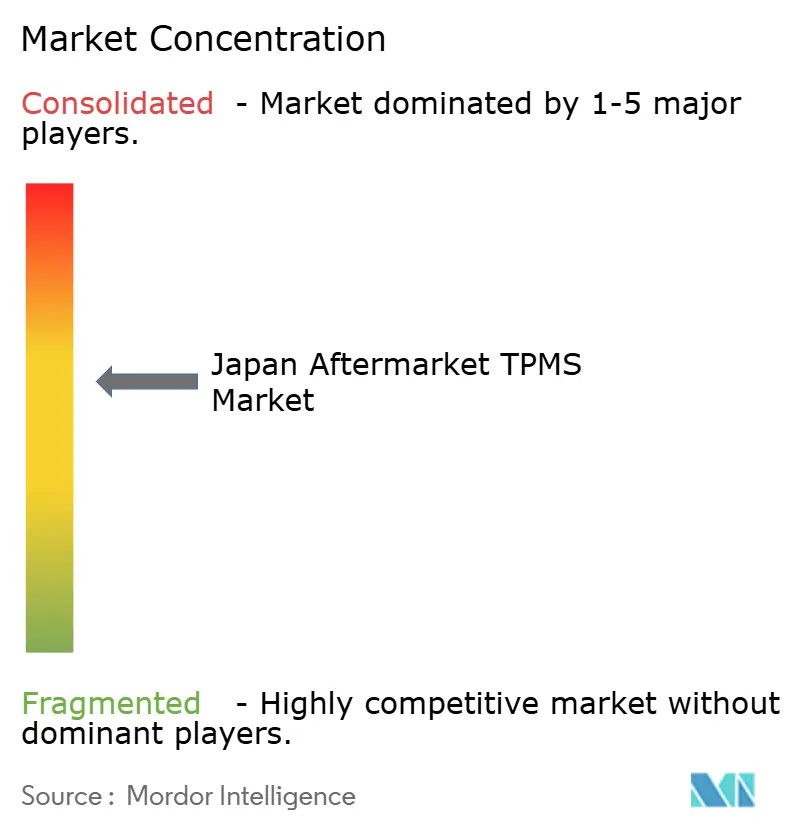

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Aftermarket TPMS Market Analysis by Mordor Intelligence

The Japan aftermarket TPMS market size is estimated at USD 139.95 million in 2025 and is projected to reach USD 278.28 million by 2030, representing a 14.74% CAGR. Sustained double-digit expansion rests on three pillars: compulsory TPMS fitment for new vehicles. This rapidly aging vehicle fleet requires sensor replacement and the integration of tire-pressure data into connected-car and smart-city platforms. Heightened safety expectations and fuel-efficiency concerns in a high-energy-price environment motivate owners to retrofit reliable pressure-monitoring solutions. Meanwhile, the country’s automotive maintenance sector has elevated electronic device servicing to strategic priority status, ensuring consistent workshop demand for replacement sensors. Finally, the 433 MHz spectrum reallocation imposes new certification costs that favor technically adept suppliers, further shaping competitive dynamics.

Key Report Takeaways

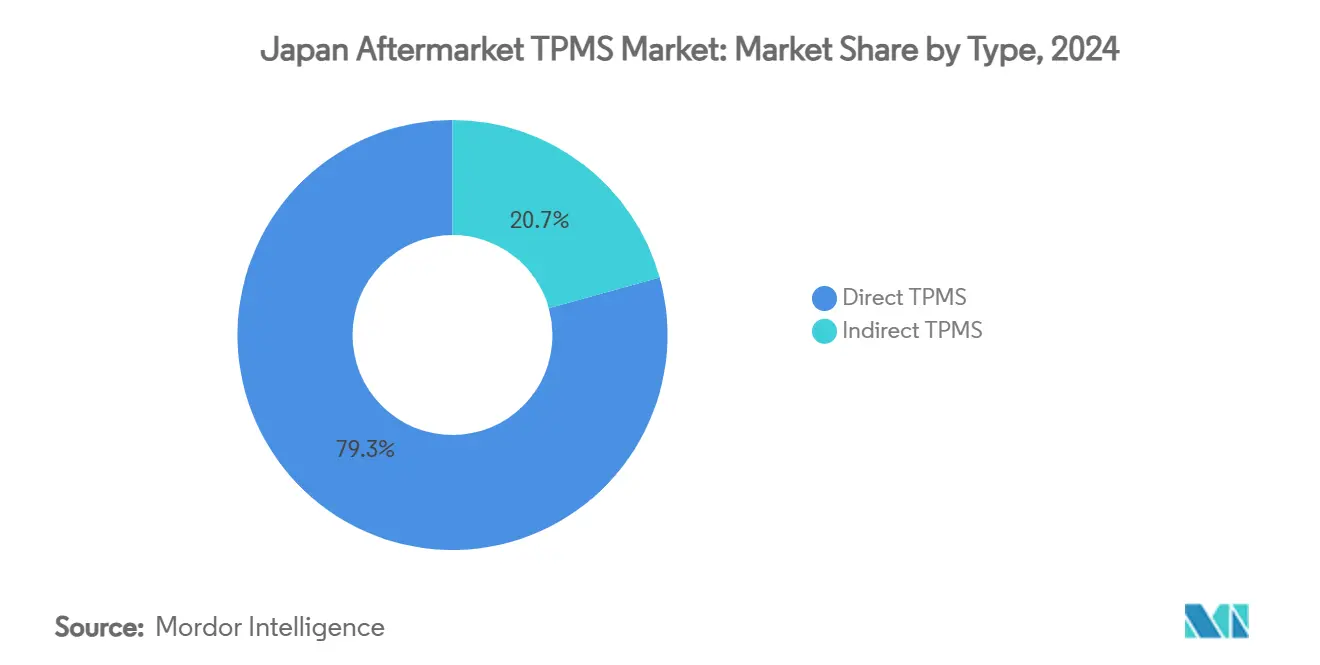

- By type, Direct TPMS captured 79.33% revenue share of the Japan aftermarket TPMS market in 2024 and is projected to advance at a 15.62% CAGR to 2030.

- By technology integration, Stand-alone TPMS Units held 67.25% revenue share of the Japan aftermarket TPMS market, while Smart/Connected TPMS is set to expand at 16.83% CAGR through 2030.

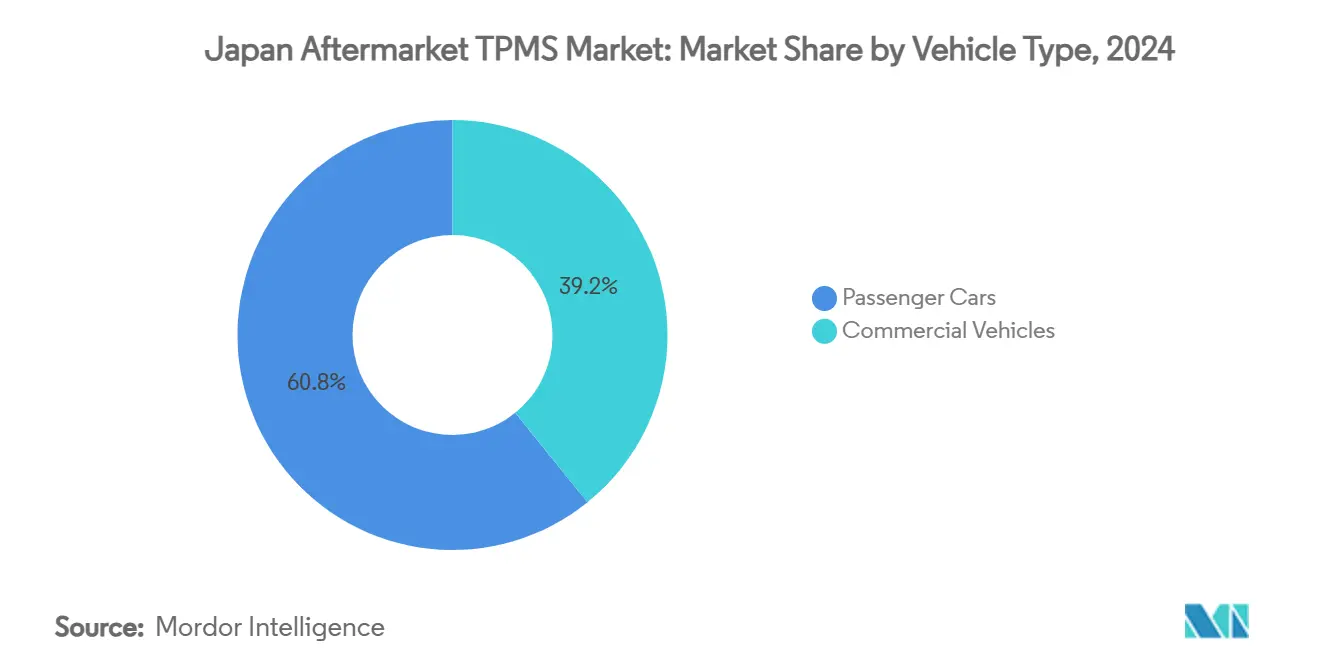

- By vehicle type, Passenger cars accounted for 60.77% of the Japan aftermarket TPMS market size in 2024, whereas commercial vehicles will record the highest projected CAGR at 16.26% through 2030.

- By distribution channel, Offline channels dominated with 85.13% share of the Japan aftermarket TPMS market in 2024, while online channels are expected to grow at a 17.13% CAGR through 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with Japan contributing to the overall trajectory. The outlook on worldwide aftermarket tpms market reflects how these are expected to evolve collectively.

Japan Aftermarket TPMS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory TPMS Fitment on New Cars | +4.2% | National | Short term (≤ 2 years) |

| Aging Vehicle Parc Increasing Replacement Demand | +3.8% | National | Medium term (2-4 years) |

| Expansion of E-commerce Auto-Parts Platforms | +2.1% | National | Medium term (2-4 years) |

| Rising Consumer Focus on Fuel Efficiency and Safety | +1.9% | National | Long term (≥ 4 years) |

| Smart-City Parking Systems using TPMS Data | +1.4% | Urban centers | Long term (≥ 4 years) |

| Subscription-Based Telematics Bundles incl. TPMS | +1.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory TPMS Fitment Drives Regulatory Compliance Wave

The 2024 MLIT decree that mandates TPMS installation on every newly registered vehicle triggers a surge in retrofit demand as non-compliant units fail periodic inspections [1]“Road Vehicle Safety Regulations Update 2024,” Ministry of Land, Infrastructure, Transport and Tourism, mlit.go.jp. Workshops must now upgrade diagnostic tools to service electronic control devices, a requirement that channels business toward suppliers with strong OEM training resources. Compliance deadlines also propel older vehicles into service bays, accelerating sensor replacement cycles in the Japan aftermarket TPMS market. Major domestic manufacturers leverage their documentation advantages to secure initial retrofitting contracts, while nimble specialist firms offer low-cost kits for legacy models. Enforcement via the Shaken inspection system guarantees a multi-year revenue stream for replacement sensors, cementing a foundation for steady growth.

Aging Vehicle Fleet Intensifies Replacement Cycles

Japanese motorists are keeping vehicles on the road longer because of inflation and supply-chain-driven new-car shortages, stretching the average fleet age well past seven years. In that period, first-generation TPMS batteries begin failing, creating a sweet spot for replacement demand. As OEM warranties lapse, owners flock to independent garages for competitively priced sensors, amplifying the Japan aftermarket TPMS market trajectory. Universal-fit sensors appeal to workshops that need to streamline inventory yet ensure broad compatibility. The trend strengthens direct TPMS uptake, given its battery end-of-life predictability compared with indirect systems.

E-commerce Transformation Reshapes Distribution Dynamics

Japan’s B2C e-commerce market exceeded JPY 24.8 trillion in 2024, making digital storefronts indispensable for sensor vendors[2]“FY2024 E-Commerce Market Survey,” Ministry of Economy, Trade and Industry, meti.go.jp. TPMS products naturally lend themselves to online sales because they are compact, standardized, and supported by abundant installation tutorials. Manufacturers exploit direct-to-consumer portals to sidestep traditional distributor margins, while detailed online specs reassure DIY buyers. However, the migration online forces brick-and-mortar parts chains, already hit by 445 workshop closures in 2024, to adopt hybrid click-and-collect models or risk obsolescence. Online growth thus diversifies the Japan aftermarket TPMS market while squeezing low-value intermediaries.

Consumer Safety Consciousness Drives Premium Adoption

High gasoline prices and Japan’s carbon-neutrality pledge have raised public awareness of tire pressure in fuel efficiency, with studies pointing to 3% savings when pressures are kept optimal. TPMS therefore shifts from regulatory necessity to perceived value-add, particularly when bundled with smartphone alerts and predictive maintenance features. The national target of cutting annual traffic fatalities by 1,200 by 2030 further elevates real-time tire-pressure monitoring in policy conversations. Fleets are adopting premium connected TPMS packages that integrate seamlessly with telematics dashboards, a trend that underpins rising average selling prices in the Japan aftermarket TPMS market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit Cost for Older Vehicles | -2.3% | National | Short term (≤ 2 years) |

| Intense Price Competition from Low-Cost Imports | -1.8% | National | Medium term (2-4 years) |

| Proliferation of Counterfeit Sensors | -1.4% | National | Medium term (2-4 years) |

| MLIT Spectrum Re-Allocation Compliance Costs | -0.9% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs Create Market Access Barriers

Sensor kits for vehicles without existing TPMS wiring can cost a significant outlay for cash-strapped owners, especially in rural prefectures where disposable incomes lag national averages. The price burden is heavier on fleet operators managing dozens of aging trucks: aggregate retrofit costs quickly climb into millions of yen, delaying widespread adoption. Some workshops offset expenses through government subsidies, but the overall headwind still trims the Japan aftermarket TPMS market growth rate, particularly in segments dominated by price-sensitive customers.

Import Competition Intensifies Pricing Pressures

Low-cost imports from mainland China continue to flood online marketplaces, undercutting domestic sensor makers by 30–40% on average. A weak yen marginally raises import prices yet fails to close the cost gap. As basic sensors become commoditized, local firms pivot toward premium, connected offerings while ceding volume share in the entry-level bracket. This strategic bifurcation compresses margins for mid-tier products and introduces volatility into the Japan aftermarket TPMS market pricing structure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct Technology Underpins Market Leadership

Direct systems contributed 79.33% of the Japan aftermarket TPMS market share in 2024, thanks to reliable, real-time pressure readings that meet MLIT performance standards. The segment is forecast to grow at a 15.62% CAGR through 2030, supported by integration with ADAS modules that use direct sensor data for tire-related safety measures. During this period, indirect TPMS remains a niche option for cost-sensitive retrofits but faces gradual replacement as OEMs and regulators adopt higher data-accuracy standards. Direct TPMS continues to improve through innovations like accelerometer-based wheel-position recognition, making tire rotations easier and reducing service labor time.

Japan's aftermarket TPMS market size gains accrue most strongly to suppliers that bundle direct sensors with proprietary diagnostic software, allowing garages to reprogram replacement units rapidly. Pacific Industrial’s Bluetooth-enabled cap sensors illustrate the design trend toward minimal installation complexity, broadening uptake among both DIY enthusiasts and professional installers [3]“Bluetooth-Enabled Cap-Type Sensor Launch,” Pacific Industrial Co., pacificind.co.jp.

By Technology Integration: Connected Systems Capture Growth Upside

Stand-alone modules held a 67.25% share of the Japan aftermarket TPMS market in 2024, reflecting retrofit practicality and lower unit prices. However, smart/connected variants, supported by cellular or Bluetooth gateways, will grow at a 16.83% CAGR until 2030. Toyota and NTT’s initiative to surpass 20 million connected vehicles worldwide by 2025 highlights the infrastructure boom driving sensor data monetization. Over-the-air firmware updates and app-based alerts distinguish connected TPMS units and boost replacement sensor sales in Japan's aftermarket TPMS market.

Subscription-based data services present new annuity streams, encouraging hardware vendors to subsidize initial sensor costs in exchange for monthly monitoring fees. Sensata’s remote-configuration feature set exemplifies this shift, enabling fleets to cut downtime through predictive maintenance scheduling.

By Vehicle Type: Commercial Fleets Accelerate Investment

Passenger cars still accounted for 60.77% of the Japan aftermarket TPMS market in 2024, but commercial vehicles are expected to grow at a 16.26% CAGR through 2030. Each truck or bus requires multiple sensors, increasing total unit demand. Fleet operators also value the fuel-saving potential that connected TPMS provides in daily logistics. Light commercial vehicles lead volume growth due to the rising last-mile delivery segment, where optimizing tire pressures directly improves payload efficiency.

Japan’s aftermarket TPMS market size for commercial vehicles benefits from regulations that require newly registered trucks to have certified TPMS hardware. Meanwhile, growth in passenger cars is focused on SUVs and crossovers, whose larger tires increase the risk of under-inflation and the perceived benefits of monitoring.

By Distribution Channel: Digital Expansion Gains Momentum

Offline service centers and parts stores retained 85.13% share of the Japan aftermarket TPMS market in 2024 but face a 6-point share contraction by 2030 as consumers migrate online. The online channel is expected to grow with a CAGR of 17.13% by 2030. E-commerce marketplaces led by Rakuten support same-day shipping on standardized sensor kits and provide video tutorials that demystify installation. Although online share rises, complex programming procedures ensure workshops continue capturing the majority of labor revenue, preserving their relevance in the Japan aftermarket TPMS market.

Manufacturers increasingly operate branded web stores that integrate VIN lookup tools to match sensors to vehicle specifications, shrinking error rates in online orders. Hybrid retail models—order online, install in-store—are emerging, giving traditional chains a path to defend market position.

Geography Analysis

Greater Tokyo anchors the largest concentration of Japan aftermarket TPMS market demand due to its dense passenger-car population and advanced repair-shop network. Osaka and Nagoya follow, each benefiting from extensive commercial-vehicle activity tied to port logistics and manufacturing clusters. Urban pilot programs that feed TPMS data into smart-parking platforms further drive adoption, enhancing municipal congestion-management systems.

In contrast, rural prefectures exhibit slower upgrade cycles, constrained by lower disposable incomes and limited access to specialist equipment. Yet these areas harbor sizable aging vehicle fleets, implying latent replacement opportunity once cost barriers fall. Coastal industrial corridors see brisk commercial-vehicle retrofits as freight carriers respond to fuel-cost headwinds by optimizing tire pressures.

Supply-chain resilience remains central: Japan’s archipelagic geography makes sensor logistics vulnerable to weather disruptions. Established domestic suppliers leverage regional warehousing and OEM ties to shorten lead times, a key competitive edge in servicing remote islands where shipping delays can stall vehicle inspections.

Analysis of the aftermarket tpms market by Mordor Intelligence spans multiple other regional evaluations across Europe, supported by country-level insights for India, South Korea, China, and United States, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Japan aftermarket TPMS market features moderate concentration. Denso, Pacific Industrial, and Alps Alpine capitalize on deep OEM linkages to secure first-fit technical documentation, subsequently repurposing platforms for aftermarket kits. Denso’s USD 3.6 billion R&D spend in fiscal 2024 bankrolls ASIC development that cuts sensor power draw, elongating battery life. Continental and Sensata reinforce global scale with localized distribution, while smaller domestic specialists target niche retrofit niches.

Technological differentiation centers on data analytics ecosystems rather than raw hardware. TDK’s alliance with Goodyear amalgamates tire performance metrics with embedded MEMS sensors to create full-spectrum monitoring services. Counterfeit proliferation challenges brand integrity, prompting vendors to embed encrypted authentication in sensor firmware.

Price competition intensifies as Chinese imports undercut local offerings. Domestic brands respond by bundling extended warranties and software updates that low-cost entrants cannot match easily. The resulting segmentation drives a dual-track strategy: high-value connected packages and basic economic units for older vehicles.

Japan Aftermarket TPMS Industry Leaders

Denso Corporation

Pacific Industrial Co., Ltd.

Continental AG

Schrader TPMS Solutions (Sensata)

Alps Alpine Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Japan introduced a scan-tool subsidy covering up to JPY 160,000 per maintenance shop for TPMS diagnostic hardware and technician training, helping small garages meet electronic safety-vehicle servicing standards.

- October 2024: The Radio Act Ordinance was amended to formalize 433.795–434.045 MHz as the dedicated band for TPMS transmissions, completing the national migration to a harmonized frequency plan.

Japan Aftermarket TPMS Market Report Scope

| Direct TPMS |

| Indirect TPMS |

| Stand-alone TPMS Units |

| Smart/Connected TPMS |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUVs and MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Offline (Auto-parts stores, specialty shops, service centers) |

| Online (OEM websites/Apps, e-commerce platforms) |

| By Type | Direct TPMS | |

| Indirect TPMS | ||

| By Technology Integration | Stand-alone TPMS Units | |

| Smart/Connected TPMS | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUVs and MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Distribution Channel | Offline (Auto-parts stores, specialty shops, service centers) | |

| Online (OEM websites/Apps, e-commerce platforms) | ||

Key Questions Answered in the Report

How large is the Japan aftermarket TPMS market in 2025?

The sector is valued at USD 139.95 million, with a forecast 14.74% CAGR to 2030.

What is driving sensor demand in older vehicles?

Battery-depleted first-generation sensors and rising vehicle age spur replacement cycles, especially for cars 7–12 years old.

Which TPMS technology is growing fastest?

Smart/Connected TPMS shows the quickest advance at a 16.83% CAGR through 2030 as connectivity becomes standard.

Why are commercial fleets installing TPMS faster than passenger-car owners?

Regulatory mandates plus fuel-saving and safety benefits boost adoption, and each truck needs multiple sensors.

Page last updated on: