Anaerobic Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 657.73 Million |

| Market Size (2031) | USD 889.29 Million |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

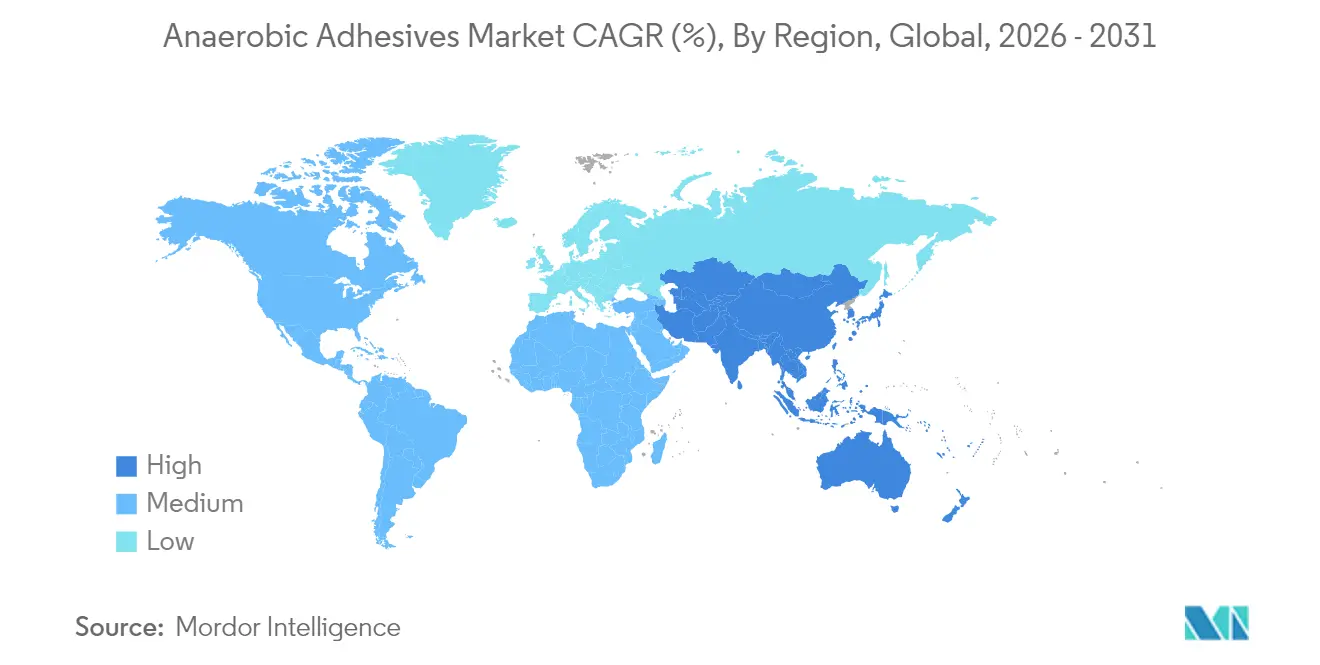

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anaerobic Adhesives Market Analysis by Mordor Intelligence

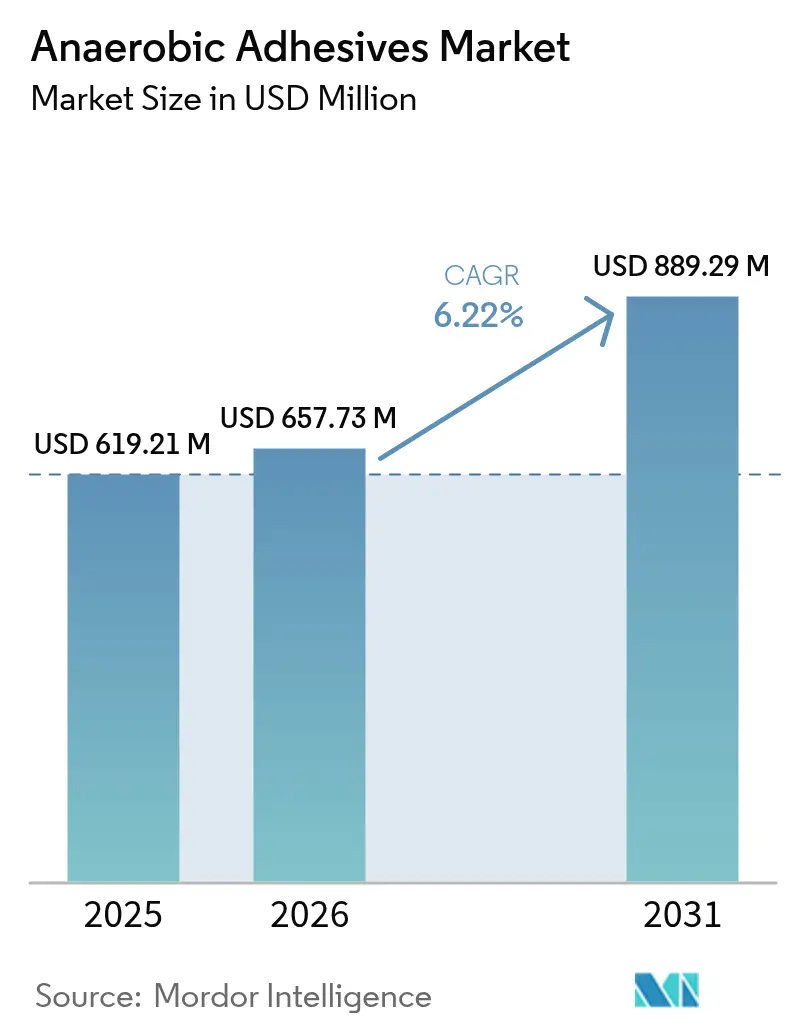

The Anaerobic Adhesives Market size was valued at USD 619.21 million in 2025 and estimated to grow from USD 657.73 million in 2026 to reach USD 889.29 million by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Rising demand for high-integrity fastening in electric vehicles, miniaturized electronics, and wind turbines is accelerating the shift from mechanical to chemical bonding. Manufacturers are prioritizing vibration-resistant, lightweight joining methods to improve product reliability and cut assembly weight. Tightening chemical regulations are simultaneously prompting rapid reformulation toward “label-free” products that remove substances of concern while preserving performance. Ongoing consolidation among leading suppliers is bringing scale advantages in research and development and global distribution, strengthening competitive moats while raising entry barriers for smaller formulators.

Key Report Takeaways

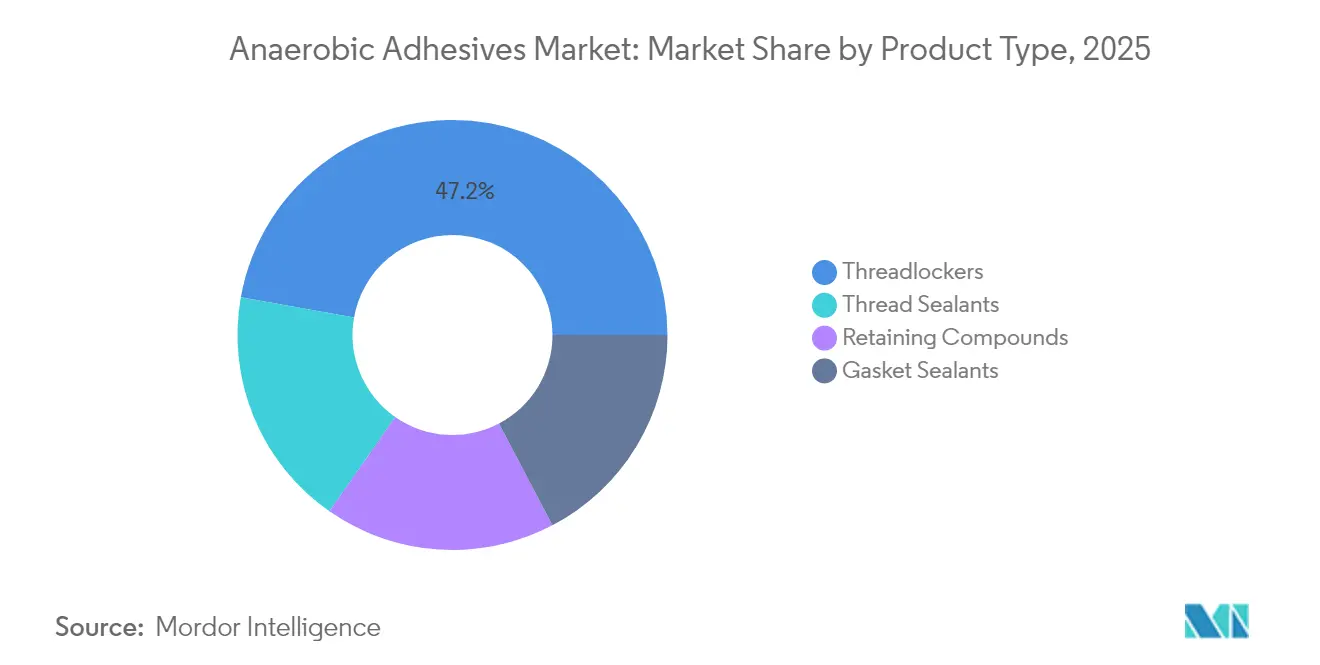

- By product category, threadlockers led with 47.20% revenue share in 2025, while thread sealants are forecast to expand at a 6.85% CAGR to 2031.

- By substrate material, metal parts commanded 70.30% of the anaerobic adhesives market share in 2025; plastics and composites are projected to grow at an 8.35% CAGR through 2031.

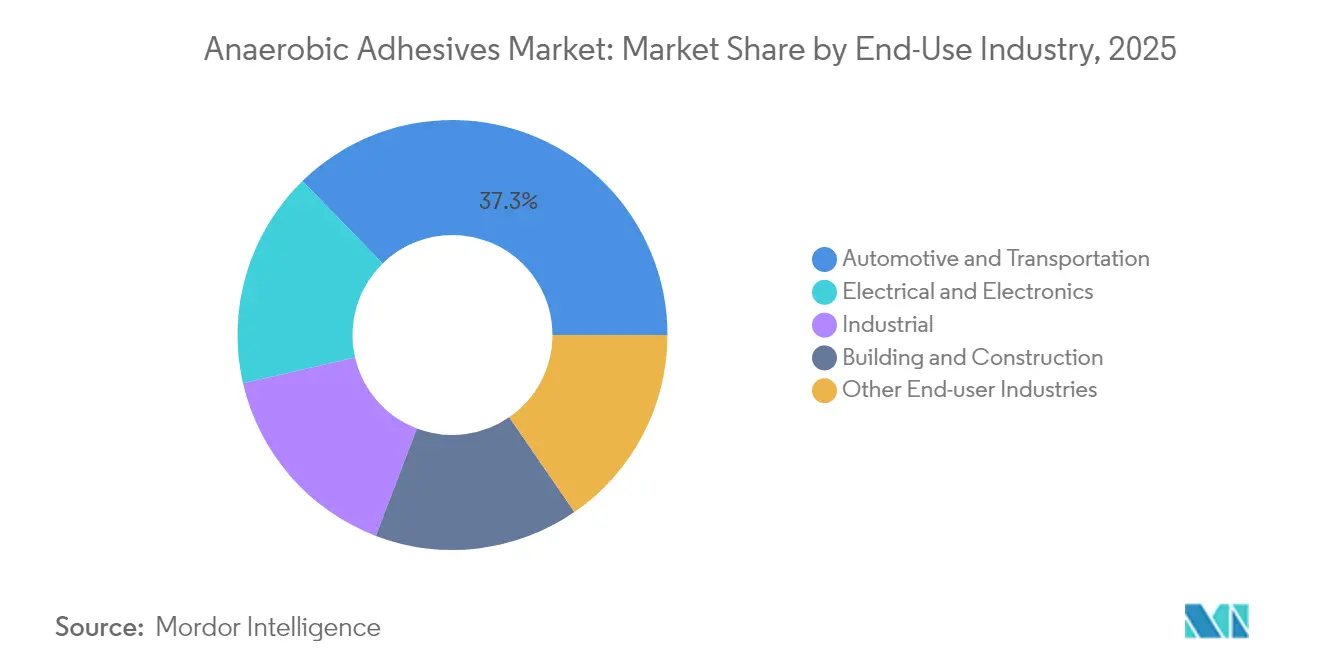

- By end-use industry, automotive and transportation held 37.30% share of the anaerobic adhesives market size in 2025, whereas electrical and electronics is advancing at an 7.74% CAGR through 2031.

- By geography, Asia-Pacific accounted for 47.60% of the anaerobic adhesives market in 2025 and is set to grow at an 8.02% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anaerobic Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovering Automotive Production in China, India & Mexico | +1.8% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Rapid Miniaturisation in Consumer & Automotive Electronics Raising Demand for Threadlockers | +1.5% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| Accelerating Shift Toward Predictive Maintenance in Wind Turbines Boosting Retaining Compounds | +1.2% | Europe, North America | Medium term (2-4 years) |

| Growing OEM Preference for Lightweight, Vibration-Resistant Fastening Solutions in E-Mobility | +1.4% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Increased adoption in aerospace for critical, high-stress joints | +0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recovering automotive production in China, India and Mexico

Electric-vehicle output rose sharply in 2024, with China surpassing 35% EV production share. Battery packs and traction motors now rely on anaerobic threadlockers that withstand intense thermal cycling and vibration. Modular vehicle platforms magnify the need for uniform clamp load, and chemical fasteners provide the required concentricity at scale. Henkel notes specification of automotive-grade anaerobic formulations in more than 60% of new EV designs in Asia, underscoring the indispensability of chemical locking for next-generation drivetrains. These factors anchor a multi-year demand surge and reinforce the Asia-Pacific leadership in the anaerobic adhesives market.

Rapid miniaturisation in consumer and automotive electronics

Average thread diameters in handheld gadgets and in-vehicle controllers continue to shrink, compelling manufacturers to adopt low-viscosity, capillary threadlockers that flow into micro-threads without excess squeeze-out. A modern passenger car now contains about 3,000 electronic sub-assemblies, each vulnerable to vibration-induced loosening. Purpose-built anaerobic grades with controlled breakaway strength preserve serviceability while safeguarding high-density boards. Suppliers capitalise by launching micro-dispense packaging and precision dosing equipment, speeding adoption across contract manufacturing lines throughout the anaerobic adhesives market.

Accelerating shift toward predictive maintenance in wind turbines

Wind-farm operators pair IoT sensors with high-strength anaerobic retaining compounds to secure bearings and gear couplings exposed to forces exceeding 100 tons. Integration of LOCTITE Pulse monitoring systems cut unscheduled outages by 37% in European fleets, demonstrating how adhesive reliability underpins data-driven uptime strategies[1]Henkel, “Threadlockers Blow Wind of Change in Renewables Sector,” henkel-adhesives.com. As turbine owners extend life cycles beyond 20 years, long-term adhesion and corrosion resistance become mission-critical, further boosting compound consumption across the anaerobic adhesives market.

Growing OEM preference for lightweight, vibration-resistant fastening in e-mobility

Premium EV programs now specify anaerobic threadlockers for over 70% of threaded joints in traction assemblies. Eliminating lock washers and split pins trims 3-5 kg from a mid-size EV, directly improving range. Adhesive-secured joints also deliver superior damping, minimising audible rattle and micro-fretting during vehicle life. Tier-one suppliers are co-developing custom grades that cure rapidly on aluminum housings, ensuring line-rate throughput while hitting stringent torque-to-yield targets. This cross-discipline partnership cements the role of advanced formulations in the evolving anaerobic adhesives market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Feedstock Prices | -0.7% | Global, with higher impact in Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Pressure to Reduce Hazardous Stabilisers in Formulations (EU REACH, TSCA) | -0.9% | Europe, North America | Medium term (2-4 years) |

| Skilled-Labour Gap in Emerging Economies for Precision Assembly Applications | -0.5% | Asia-Pacific, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile feedstock prices

Frequent swings in methacrylate-monomer costs squeeze gross margins, particularly for regional formulators lacking hedging capability. Production disruptions in key Asian chemical parks raise supply-chain risk and prompt inventory inflation across the anaerobic adhesives market. Large players counter with alternative raw-material recipes that hold shear strength while dampening cost volatility, giving them pricing leverage over smaller rivals.

Regulatory pressure to reduce hazardous stabilisers

The 2025 EPA ruling on trichloroethylene bans a common solvent in legacy formulations, forcing costly reformulation[2]Environmental Protection Agency, “Trichloroethylene (TCE); Regulation under the Toxic Substances Control Act (TSCA),” jjkellercompliancenetwork.com . EU restrictions on phthalate-based stabilisers take full effect in 2026, compressing compliance timelines. Tier-one producers have budgeted USD 2-3 million per product line to qualify safer chemistries and avoid production downtime. While short-term costs weigh on profit, the pivot unlocks premium “label-free” ranges that strengthen brand equity and enhance user safety across the anaerobic adhesives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Threadlockers Dominate Critical Applications

Threadlockers generated 47.20% revenue in 2025, reflecting entrenched preference for chemical locking over mechanical devices. Their unmatched ability to maintain clamp load under vibration keeps them integral to drivetrain, heavy-machinery, and precision instrumentation assembly. Specialty variants now target stainless steel, high-temperature zones, and micro-threads, widening the addressable pool. Thread sealants, although smaller, will outpace all other products with a 6.85% CAGR as fluid-handling systems demand simultaneous sealing and fastening. This double-functionality gives plant engineers a compelling cost-of-ownership advantage.

Manufacturers intensify research and devlopment on dual-cure systems blending anaerobic and UV triggers, enabling fixture within seconds yet delivering final anaerobic strength in enclosed metal joints. These innovations shorten takt times and support high-volume electronics production. Retaining compounds are scaling beyond traditional bearing bonds into wind-turbine assemblies, creating fresh revenue layers. Gasket sealants, though niche, solve rigid-flange challenges where legacy elastomer gaskets fail under high pressure, further diversifying the anaerobic adhesives market.

By Substrate Material: Metal Dominance Faces Composite Challenge

Metal parts commanded 70.30% of global consumption in 2025 as ferrous and non-ferrous ions catalyse rapid cure. Enhanced primers now speed set-time on passive alloys such as stainless steel and zinc-plated fasteners, unlocking broader deployment in food-grade machinery where chrome steels prevail. The metal segment’s scale underpins economies that keep unit prices competitive, reinforcing its central role in the anaerobic adhesives market.

Plastics and composites, however, are the fastest-expanding substrate, projected at an 8.35% CAGR. Hybrid formulations introduce alternative redox initiators that cure reliably on non-metallic surfaces, enabling chemical fastening in lightweight battery enclosures and consumer-electronics frames. As electric-vehicle battery packs combine aluminum endplates with glass-fiber separators, multi-substrate adhesives bridge the gap and protect against galvanic corrosion, elevating the overall anaerobic adhesives market share for next-generation mixed-material assemblies.

By End-Use Industry: Automotive Leadership Meets Electronics Growth

Automotive and transportation sustained 37.30% revenue share in 2025, buoyed by the transition to electric drivetrains. Critical joints in e-axles, inverter housings, and battery trays depend on robust threadlocking to endure vibration amplitudes exceeding 15 g. Vehicle makers progressively substitute mechanical locks with anaerobic securing, saving weight and assembly steps while boosting warranty confidence. The segment’s scale sells production volumes that anchor baseline demand for the anaerobic adhesives market.

Electrical and electronics, though smaller in 2025, will climb fastest at an 7.74% CAGR through 2031. Miniaturized consumer devices and ADAS modules require accurate micro-fastener torque retention. Low-outgassing, electrically insulating variants now protect die-attach areas and sensor enclosures. EMS providers pair automated dispensers with vision systems to guarantee sub-milligram dosing accuracy, solidifying supply agreements that broaden the anaerobic adhesives industry footprint.

Geography Analysis

Asia-Pacific led with 47.60% consumption in 2025, a dominance underpinned by China’s EV surge and India’s electronics push. Chinese OEMs embed anaerobic threadlockers in over 60% of new EV platforms, and policy incentives accelerate local sourcing, deepening regional expenditure. India’s Make-in-India initiative draws multinational smartphone and auto suppliers that import dispensing lines alongside adhesive consumables, advancing the anaerobic adhesives market size for South Asia. Mature Japanese and South Korean factories maintain top-tier specification standards, spurring demand for premium high-temperature grades.

North America remains pivotal for aerospace, defense, and wind-energy projects that require certified formulations. The United States fuels high-margin sales in satellite hardware, where low-outgassing grades meet NASA and ESA specifications. Mexico’s expanding car-assembly corridor attracts Tier-1 fastener coaters applying pre-applied threadlock films, lifting cross-border volumes. Canada, though smaller, buys large packages of retaining compounds for wind-turbine refurbishments across the Atlantic corridor.

Europe ranks as an innovation leader. Stringent REACH rules motivate investment in label-free chemistries that shun phthalates and TCE. Germany’s premium carmakers co-develop solvent-free threadlockers, anchoring future revenue for the anaerobic adhesives market. France and the United Kingdom deploy predictive maintenance in onshore wind fleets, pairing sensor arrays with high-reliability retaining compounds. South America and Middle East and Africa remain nascent but see steady uptake in mining and energy infrastructure, signalling long-run potential once local skills and regulations mature.

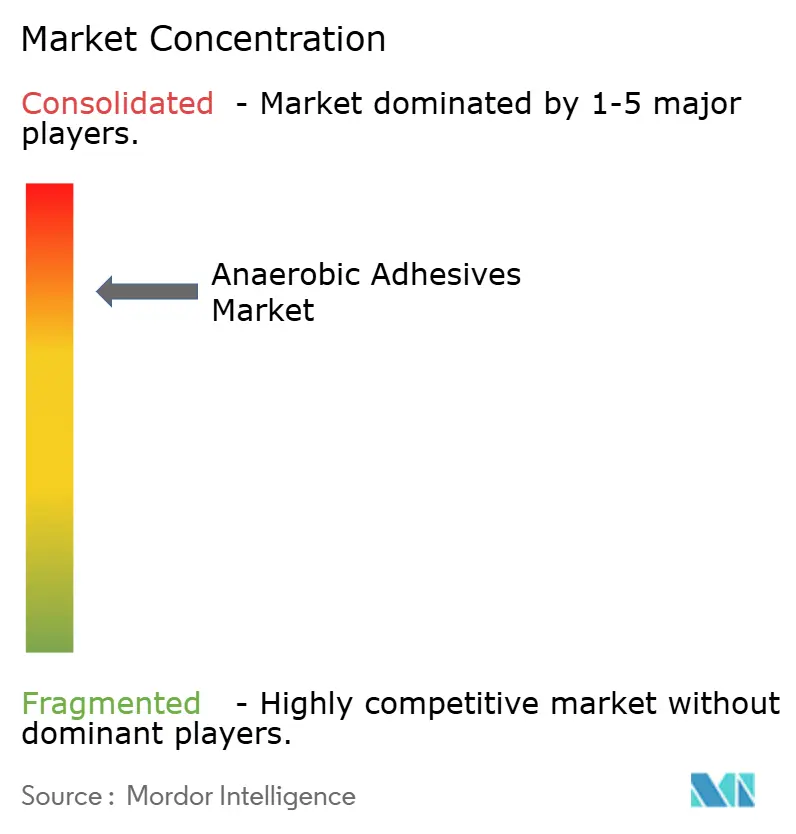

Competitive Landscape

The anaerobic adhesives market is consolidated, with the top five manufacturers—Henkel, 3M, H.B. Fuller, Permabond LLC, and ThreeBond. Henkel provides anaerobic adhesives through its LOCTITE portfolio, supported by 130 country channels and field-service academies that train plant technicians on correct usage. 3M, H.B. Fuller, Permabond, and ThreeBond round out the top tier, collectively shaping a consolidated structure in which scale drives resin sourcing advantages and rapid regulatory compliance. H.B. Fuller’s 2024 purchase of ND Industries widened its pre-applied fastener range and added the Vibra-Tite product line, giving customers turnkey mechanical-plus-chemical fastening solutions[3]H.B. Fuller Company, “H.B. Fuller Acquires ND Industries,” inddist.com.

Mid-sized specialists pursue white-space niches. Permabond focuses on aerospace-qualified grades, Hernon Manufacturing targets low-outgassing satellite compounds, and Bondloc refines dual-cure systems. These firms leverage nimble research and development cycles to win programs where larger suppliers prioritize volume. Patent filings reached 150 in 2024, centering on hybrid photoinitiator blends and bio-based monomers. Such IP accumulation cements entry barriers and shapes negotiating power across the anaerobic adhesives market.

Sustainability is the next competitive front. Leading suppliers unveiled “green” product lines that eliminate label-trigger chemicals yet match tensile shear performance. Smaller formulators face capital strain meeting similar benchmarks, hastening consolidation as regulatory complexity deepens.

Anaerobic Adhesives Industry Leaders

Henkel AG & Co. KGaA

3M

H.B. Fuller Company

Permabond LLC

ThreeBond Holdings Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: H.B. Fuller launched the Cyberbond Eco Line, a label-free anaerobic portfolio that removes hazardous chemicals and VOCs, meeting ISO 14001/9001 and EU ESG regulations.

- May 2024: H.B. Fuller expanded its pre-applied fastener technologies by acquiring ND Industries, including the Vibra-Tite brand. This acquisition is expected to strengthen H.B. Fuller's position in the anaerobic adhesives market by enhancing its product portfolio and technological capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the anaerobic adhesives market as all single-component, metal-ion-activated formulations that harden in oxygen-free gaps to lock, seal, or retain threaded, cylindrical, and flanged parts. Revenue captures factory sales of new thread-lockers, thread-sealants, retaining compounds, and form-in-place gasket materials supplied to original equipment makers and maintenance, repair, and operations channels.

Scope exclusion: Products that rely on dual UV + anaerobic cures, cyanoacrylates, and fasteners pre-coated off-line are outside the sizing.

Segmentation Overview

- By Product Type

- Threadlockers

- Thread Sealants

- Retaining Compounds

- Gasket Sealants

- By Substrate Material

- Metal

- Plastics and Composites

- Others (Ceramic, Glass)

- By End-Use Industry

- Automotive and Transportation

- Electrical and Electronics

- Industrial

- Building and Construction

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with formulation chemists and purchasing managers at automotive, wind-equipment, and electronics firms across Asia-Pacific, North America, and Europe, plus distribution partners handling MRO lines. These interviews refined metal-to-plastic substrate splits, average selling prices, and typical joint-fill rates, then validated early model outputs.

Desk Research

We began with public datasets that trace the end-markets where these adhesives flow. UN Comtrade trade codes for acrylate reactive glues, OICA motor-vehicle output, IPC electronics production indices, and IEA wind-turbine install data helped us set demand pools. Standards and failure-mode papers from SAE International and ASTM clarified typical fill volumes per joint, while patent analytics from Questel flagged emerging formula families. Financials in D&B Hoovers, supplier 10-Ks, and quarterly investor decks anchored price trends and margin spreads.

Complementary insight was drawn from region-specific sources such as China Customs, Eurostat PRODCOM, the U.S. Bureau of Labor Statistics Producer Price Index for adhesives, and trade-association bulletins from the Adhesive and Sealant Council. The sources listed are illustrative; many additional publications were reviewed for verification and context.

Market-Sizing & Forecasting

A top-down build began with production volumes of vehicles, electric motors, printed circuit boards, and industrial gearboxes, which are then multiplied by adhesive usage coefficients gathered from primary calls. Results are cross-checked through selective bottom-up snapshots, supplier sales roll-ups, and channel checks to adjust totals. Key variables feeding the five-year multivariate regression include global light-vehicle assemblies, EV penetration, electronics PMI, industrial maintenance outlays, and average acrylic-monomer prices, enabling scenario analysis around macro cycles. Gap pockets where bottom-up evidence is thin are bridged through validated analogs from adjacent fast-curing chemistries.

Data Validation & Update Cycle

Outputs pass variance scans versus historical series, peer signals, and prior editions before a senior reviewer signs off. Mordor Intelligence refreshes the full model annually and issues interim tweaks when material events, such as feedstock shocks or major capacity additions, shift the baseline.

Why Mordor's Anaerobic Adhesives Baseline Commands Reliability

Published figures often diverge because firms choose differing product mixes, price nets, and refresh cadences.

By anchoring on application-level usage factors that our experts confirm each year, our baseline stays closest to how the market truly buys and consumes these adhesives.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 621.7 M (2025) | Mordor Intelligence | - |

| USD 715.4 M (2024) | Global Consultancy A | Includes hybrid UV-assisted grades and gross factory shipments before rebates |

| USD 637.3 M (2024) | Industry Journal B | Uses straight-line CAGR extrapolation; limited country splits; no currency normalization |

| USD 612.4 M (2024) | Analytics Firm C | Applies uniform ASP across product types and retains sealant-only grades |

These contrasts show that Mordor's disciplined scope choices, yearly primary checks, and transparent variable trail deliver a balanced, decision-ready baseline that clients can retrace and challenge with confidence.

Key Questions Answered in the Report

What is driving the growth of the anaerobic adhesives market through 2031?

Demand for vibration-resistant fastening in electric vehicles, miniaturized electronics, and predictive-maintenance-ready wind turbines underpins a 6.22% CAGR outlook.

Which product type holds the largest share of the anaerobic adhesives market?

Threadlockers accounted for 47.20% of 2025 revenue because they reliably prevent loosening in threaded joints across industries.

Why is Asia-Pacific the leading regional market for anaerobic adhesives?

China’s EV boom and India’s expanding electronics production push Asia-Pacific to 47.60% share in 2025, with growth projected at 8.02% CAGR.

How are regulations shaping product development in the anaerobic adhesives industry?

EU REACH and US TSCA restrictions on solvents and stabilisers are forcing reformulation, accelerating the launch of label-free, VOC-free grades.

Which end-use industry is expected to grow fastest?

Electrical and electronics will expand at an 7.74% CAGR as device miniaturisation demands precision micro-thread securing solutions.

What strategic moves are leading companies making?

Major players pursue acquisitions, such as H.B. Fuller’s purchase of ND Industries, and introduce eco-label ranges to comply with evolving ESG requirements.

What is the current size of the anaerobic adhesives market?

The anaerobic adhesives market size is estimated at USD 657.73 million in 2026, and is expected to reach USD 889.29 million by 2031, at a CAGR of 6.22% during the forecast period (2026-2031).

Page last updated on: