Hybrid Adhesives And Sealants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

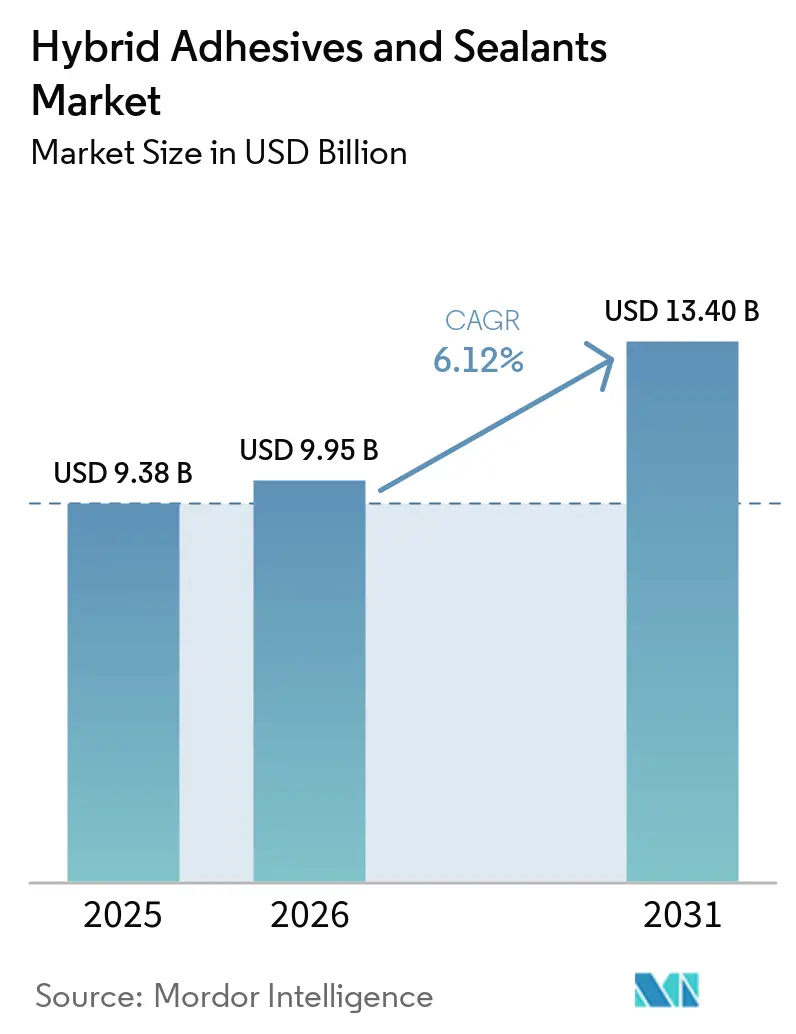

| Market Size (2026) | USD 9.95 Billion |

| Market Size (2031) | USD 13.40 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

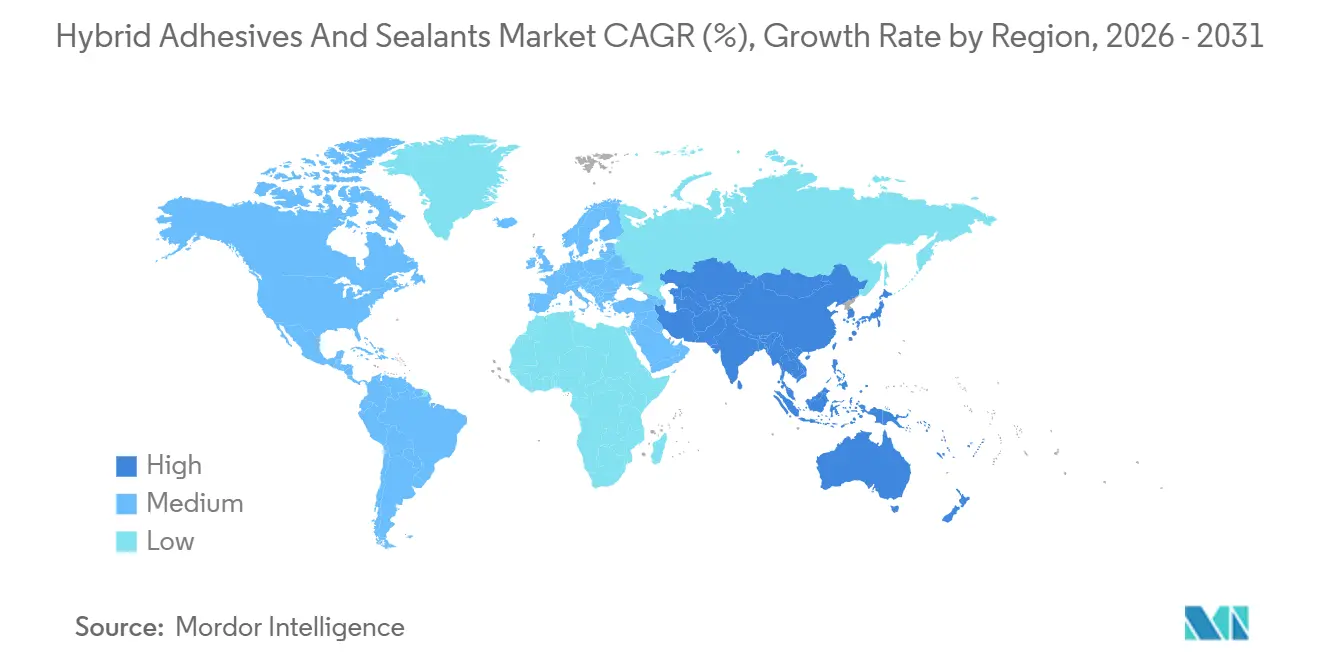

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Adhesives And Sealants Market Analysis by Mordor Intelligence

The Hybrid Adhesives and Sealants Market size is expected to increase from USD 9.38 billion in 2025 to USD 9.95 billion in 2026 and reach USD 13.40 billion by 2031, growing at a CAGR of 6.12% over 2026-2031. Robust demand from electric-vehicle (EV) battery assembly, modular construction, and electronics packaging is accelerating the displacement of mechanical fasteners with bonding systems that spread stress more evenly and cut assembly time. Regulatory limits on volatile organic compound (VOC) emissions and diisocyanates are hastening the move toward moisture-cure, isocyanate-free chemistries, particularly silyl-terminated polyether (MS polymer) hybrids. Automakers value these formulations for ambient-temperature cure, high lap-shear strength, and compatibility with aluminum, carbon fiber, and thermally conductive fillers, while contractors adopt them to waterproof façades and seal precast concrete joints without prolonged shut-downs. Supply-chain rationalization is another growth lever: regional silicone expansions in China, India, and Indonesia shorten lead times and reduce the landed cost of specialty silanes, encouraging local tier-one suppliers to specify hybrid systems in place of commodity polyurethane sealants.

Key Report Takeaways

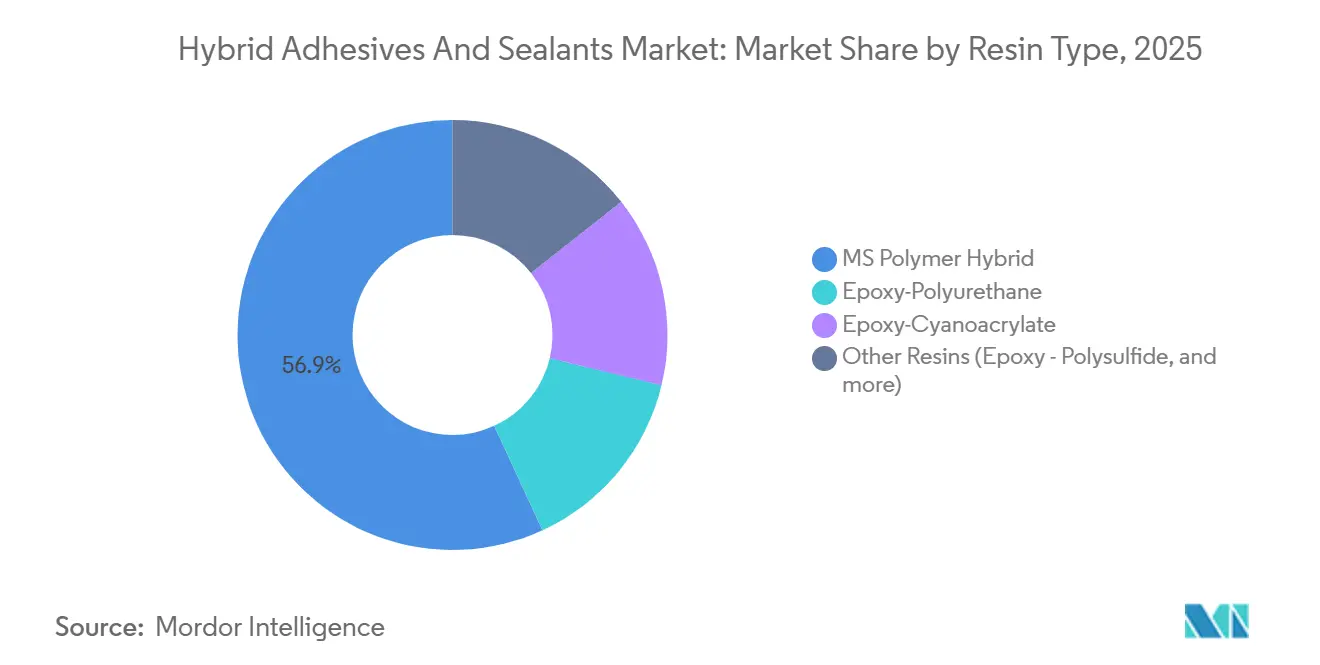

- By resin type, the MS polymer hybrid held the largest share of 56.87% in 2025, and this share is expected to grow with a CAGR of 7.30% duirng the forecast period (2026-2031).

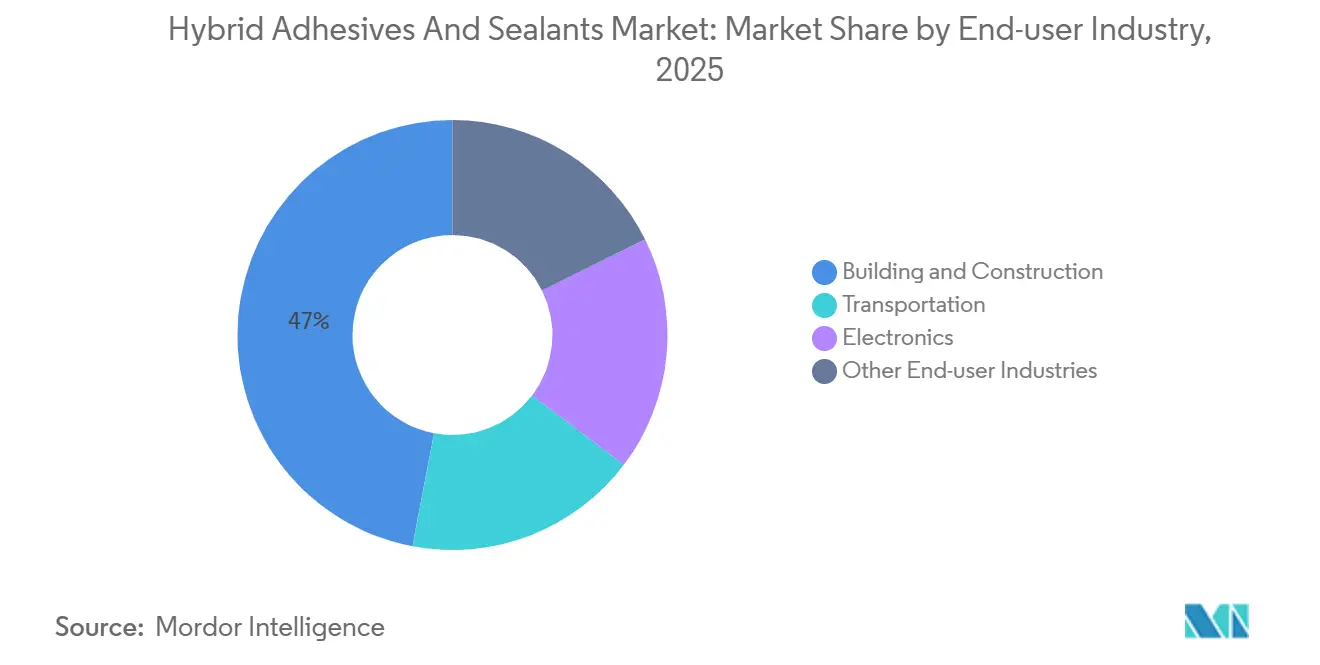

- By end-user industry, building and construction had the largest market share of 47.02% in 2025, and the share of transportation is expected to grow at a CAGR of 8.15% duirng the forecast period (2026-2031).

- By geography, Asia-Pacific held the largest share of 45.44% in 2025, and its share is expected to grow at a CAGR of 8.41% duirng the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid automotive and construction demand | +1.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Stricter global VOC and isocyanate regulations | +1.2% | Europe & North America; spillover to APAC | Short term (≤ 2 years) |

| Shift toward multifunctional bonding | +1.0% | Global, concentrated in automotive and aerospace | Medium term (2-4 years) |

| APAC infrastructure boom | +1.5% | APAC core, spillover to Middle East | Long term (≥ 4 years) |

| Modular and prefabricated building uptake | +0.7% | North America, Europe, emerging APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Automotive and Construction Demand

Electric-vehicle battery packs now incorporate cell-to-pack architectures that require adhesives to dissipate heat, tolerate 150°C excursions, and debond on command for recycling. DuPont’s Betaforce elastic structural series bonds aluminum-laminated pouch cells without surface pretreatment, trimming 15-20 minutes from each module assembly cycle. Parallel momentum is visible in high-rise Asian projects where rapid-cure MS polymer hybrids let façades be hung and waterproofed on the same day, cutting crane rental and labor expense. North American residential builders favor prefabricated panels held together with two-component polyurethane systems; eliminating steel-stud thermal bridges improves wall U-values and qualifies projects for green-building credits. H.B. Fuller’s 2024 purchase of HS Butyl added waterproofing tapes that double the throughput of curtain-wall installers across Europe. As electrification and modular construction converge, procurement teams increasingly evaluate adhesives on total cost of ownership rather than upfront material price.

Stricter Global VOC and Isocyanate Regulations

The European Union’s REACH Annex XVII amendment obliges any worker handling more than 0.1% diisocyanate content to complete certified training, pushing converters toward isocyanate-free MS polymer and epoxy-acrylic hybrids. Concurrently, the EU Packaging and Packaging Waste Regulation caps total fluorine at 50 ppm from August 2026, compelling reformulation away from fluorinated release agents that hinder recyclability[1]European Commission, “Regulation on Packaging and Packaging Waste,” eur-lex.europa.eu. California’s Safer Consumer Products program flags several diisocyanates as priority chemicals, echoing European pressure. 3M pre-empted liability by exiting all PFAS production by end-2025, sacrificing USD 890 million in annual adhesive revenue but launching a low-hazard acrylic replacement, Scotch-Weld DP8507NS, in September 2025. Suppliers able to certify VOC-free, isocyanate-free hybrids win specifications without forcing plant ventilation upgrades or extensive worker retraining.

Shift Toward Multifunctional Bonding

Vehicle lightweighting replaces rivets with structural adhesives that spread crash loads over larger areas, improving side-impact energy absorption by 15-25%. ITW Performance Polymers’ Plexus line, approved by heavy-duty truck OEMs (original equipment manufacturers), eliminates drilling through galvanized steel, postponing corrosion onset and extending trailer life by up to five years. Sika’s SikaDamp Ultralite cuts interior noise-damping mass by 80%, helping automakers meet stringent fuel-economy rules without compromising acoustics[2]Sika AG, “SikaDamp Ultralite Technical Data,” sika.com. Aerospace engineers are qualifying epoxy-polyurethane interpenetrating networks with disulfide crosslinks that self-heal micro-cracks, slicing scheduled maintenance in high-vibration zones. As labor costs rise, robotic dispensing cells apply meter-long beads at speeds mechanical fastening cannot match, improving takt time and ensuring reproducible bond lines essential for automated quality control.

APAC Infrastructure Boom

China, India, and Indonesia collectively plan more than USD 420 billion in infrastructure outlays through 2030, all favoring prefabricated modules joined with rapid-cure hybrids. Wacker’s EUR 150 million silicone expansion in Zhangjiagang came online in early 2025, adding high-purity fluids and gels that shorten lead times for regional customers. EV programs amplify demand: battery electric cars require three to four times more silicone per unit than internal-combustion vehicles for potting, gap-filling, and thermal management. Japan and South Korea have likewise upgraded capacity, with new Wacker lines in Tsukuba and Jincheon delivering the region’s largest silicone sealant throughput. As APAC construction absorbs silane feedstocks, North American buyers face allocation limits, prompting localized production investments and reinforcing the global pivot toward regional supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material and silane price volatility | -0.9% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Higher unit cost vs. commodity sealants | -0.6% | Emerging markets in APAC, South America, MEA | Medium term (2-4 years) |

| Bottlenecks in specialty silane capacity | -0.4% | Global, supply concentrated in China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material and Silane Price Volatility

Wacker announced up to 25% price hikes on silicone goods in February 2026 after platinum catalyst costs doubled, pressuring adhesive gross margins by as much as 400 basis points. Spot silane prices stayed elevated when China’s photovoltaic boom absorbed new electronic-grade capacity and US tariffs of up to 245% restricted imports. Adhesive formulators must either swallow the increases or risk share loss by passing them through. Vertical integration is one mitigation path: Sika invested USD 90 million in a roofing-membrane plant in Texas and expanded polyurethane technologies in Suzhou to secure feedstock flows. Nonetheless, unpredictability in platinum and specialty silanes will restrain short-run profitability until additional capacity stabilizes the market.

Higher Unit Cost Versus Commodity Sealants

Hybrid systems typically command a 30-60% premium over commodity polyurethane or acrylic sealants because of costly MS polymer resins and specialty additives. In low-wage regions, a USD 0.50 rivet remains cheaper than a USD 2.00 adhesive bead that needs surface preparation and full cure time. Demand is therefore strongest in applications where lifecycle economics offset the sticker price: automakers report 40-60% fewer corrosion-related warranty claims when adhesives replace fasteners, and commercial-vehicle fleets gain up to 4% fuel savings from lighter trailers. Until price spreads narrow through scale and raw-material deflation, uptake across budget-sensitive residential construction and consumer goods will lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: MS Polymer Hybrids Dominate the Isocyanate-Free Shift

MS polymer hybrids captured 56.87% of the Hybrid Adhesives and Sealants market share in 2025 and are set to grow at 7.30% CAGR to 2031. The segment’s leap reflects regulatory favor, because moisture-cure silyl backbones release no VOCs or isocyanates. Henkel’s Loctite MS 9650, unveiled in December 2025, targets in-car display bonding and sidesteps REACH Annex XVII training mandates. Epoxy-polyurethane interpenetrating networks retain a foothold in wind-turbine and aerospace structures, trading 15-25% higher prices for self-healing and fatigue resistance. Epoxy-cyanoacrylate blends fill medical and electronics niches demanding less than or equal to 60-second fixture speeds; H.B. Fuller’s 2024 purchase of Medifill and GEM added wound-closure adhesives that expand its surgical franchise.

Across 2026-2031, volume tilts toward MS polymers as formulators close the historic gap in lap-shear strength, now surpassing 2 MPa in ambient-cure tests. Epoxy-based hybrids keep a specialized territory where ultra-high modulus or extreme heat resistance outweigh regulatory constraints. Hot-melt hybrids and epoxy-polysulfide marine sealants serve even narrower roles, constrained by application-specific performance envelopes.

By End-User Industry: Transportation Leads Growth Despite Construction’s Larger Base

Building and construction commanded 47.02% of 2025 revenue, yet transportation is forecast to post the fastest 2026-2031 CAGR at 8.15%. Battery electric vehicles use three to four times more adhesive per unit than legacy drivetrains for module potting, structural bonding, and gap-filling thermal materials. ThreeBond’s TB3926 two-part acrylic enables 1:1 mix ratios and bonds aluminum, carbon fiber, and composites in under 15 minutes, streamlining EV final assembly. Sika’s SikaForce Powerflex variant stays elastic at low temperatures, solving differential-expansion challenges in body-in-white. In construction, prefabricated sandwich panels bonded in factories slice on-site labor by up to 50%, a decisive advantage in markets constrained by skilled-worker shortages. H.B. Fuller bundled its insulated glass, roofing, and woodworking lines into one Building Adhesive Solutions unit that generated USD 850 million net revenue in 2025 to exploit this modular wave. Marine, aerospace, and renewable-energy segments remain volume-light but margin-rich thanks to severe environmental and structural requisites.

Geography Analysis

Asia-Pacific retained 45.44% of the Hybrid Adhesives and Sealants market revenue in 2025 and is projected to expand at an 8.41% CAGR during the forecast period (2026-2031). Wacker’s Zhangjiagang investment boosted regional silicone capacity by roughly 20 percentage points, giving local OEMs faster access to high-purity fluids for construction sealants and EV thermal management. India’s USD 120 billion infrastructure pipeline and Indonesia’s USD 150 billion allocation funnel adhesive demand into precast bridge decks, metro systems, and glass façades. Japanese and South Korean expansions in Tsukuba and Jincheon further tighten Asia’s grip on functional silicones.

North America and Europe exhibit mid-single-digit growth, buoyed by strict emissions caps that favor isocyanate-free hybrids. The EU Packaging and Packaging Waste Regulation forces converters to redesign multilayer laminates for recyclability, boosting demand for water-based tapes and solvent-free laminating adhesives. Henkel’s 2026 acquisition spree, Stahl Group, and ATP Adhesive Systems, added EUR 1.2 billion in revenue and deepened water-based technology platforms serving both regions. Meanwhile, 3M’s complete PFAS exit repositions its portfolio around safer acrylics.

The Middle East and Africa benefit from Saudi Arabia’s Vision 2030, which earmarks 6.7 million tons of specialty-chemical capacity and SAR 93.5 billion annual revenue by 2030, raising the region’s share of Hybrid adhesives and sealants market to an estimated 22% by 2035. Sika’s Moroccan, Tanzanian, and South African plants prepare for infrastructure spending in renewable energy, water treatment, and transit corridors. South America remains the slowest-growing territory, restrained by currency swings, yet capacity builds in Brazil and Argentina by Sika and H.B. Fuller position the region for cyclical rebounds.

Competitive Landscape

The Hybrid Adhesives and Sealants Market is moderately fragmented. Innovation centers on debond-on-demand, bio-based hybrids, and thermally conductive adhesives. Henkel’s prototype cured to 12 MPa lap-shear yet disassembles under targeted heat or current, easing EV battery recycling. Smaller firms like Kiilto differentiate through agile production and 24-hour technical support, stealing share from multinationals whose portfolios lack tailored SKUs. Digital quality tools, such as 3M’s Adhesive Mix Monitor, guarantee mix ratios in real time, lowering scrap in automated lines.

Hybrid Adhesives And Sealants Industry Leaders

3M

Arkema

Henkel AG & Co. KGaA

Sika AG

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Henkel AG & Co. KGaA introduced Teroson MS 949 FR, a high-performance, flame-resistant, and sustainable hybrid adhesive/sealant designed for railcar interior and exterior applications. This product enhances safety and sustainability by being primer-free and free of tin, phthalates, isocyanates, and solvents, while adhering to fire safety standards such as EN 45545-2.

- May 2025: Wacker Chemie AG began producing hybrid polymers at its facility in Nünchritz, Germany. These hybrid polymers act as binders for hybrid adhesives and sealants. Manufacturers are increasingly using these binders in construction and assembly adhesives, parquet-flooring adhesives, and liquid waterproofing membranes for roofs and balconies.

Global Hybrid Adhesives And Sealants Market Report Scope

Hybrid adhesives and sealants, often derived from Modified Silane (MS) polymers, merge the robust strength and paintability of polyurethane with the enhanced UV and weather resistance of silicone. These single-component, moisture-curing products bond flexibly and durably to nearly all surfaces, eliminating the need for a primer.

The Hybrid Adhesives and Sealants market report is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into MS polymer hybrid, epoxy-polyurethane, epoxy-cyanoacrylate, and other resins (epoxy-polysulfide, and more). By end-user industry, the market is segmented into building and construction, transportation, electronics, and other end-user industries. By geography, the market is segmented into Asia-Pacific, North America, South America, Europe, and the Middle East and Africa. The market sizes and forecasts for the Hybrid Adhesives and Sealants market are provided in terms of value (USD) for all the above segments.

| MS Polymer Hybrid |

| Epoxy-Polyurethane |

| Epoxy-Cyanoacrylate |

| Other Resins (Epoxy - Polysulfide, and more) |

| Building and Construction |

| Transportation |

| Electronics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | MS Polymer Hybrid | |

| Epoxy-Polyurethane | ||

| Epoxy-Cyanoacrylate | ||

| Other Resins (Epoxy - Polysulfide, and more) | ||

| By End-user Industry | Building and Construction | |

| Transportation | ||

| Electronics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Hybrid adhesives and sealants market?

The Hybrid adhesives and sealants market size reached USD 9.95 billion in 2026 and is forecast to hit USD 13.40 billion by 2031.

Which resin type is growing fastest?

MS polymer hybrids are expanding at 7.30% CAGR through 2031, driven by VOC-free, isocyanate-free compliance advantages.

Why are EV manufacturers shifting to hybrid adhesives?

Battery packs need gap-filling, thermal conductivity, and debond-on-demand features that mechanical fasteners cannot provide, leading to three to four times more adhesive usage per vehicle.

Which region will deliver the highest growth through 2031?

Asia-Pacific is projected to advance at an 8.41% CAGR as China, India, and Indonesia scale infrastructure and EV production.

How volatile are raw-material costs?

Silicone and silane prices rose up to 25% in early 2026 due to platinum catalyst inflation and tight specialty-silanes, squeezing adhesive margins until new capacity comes online.

Page last updated on: