Market Overview

| Study Period | 2020 - 2031 |

|---|---|

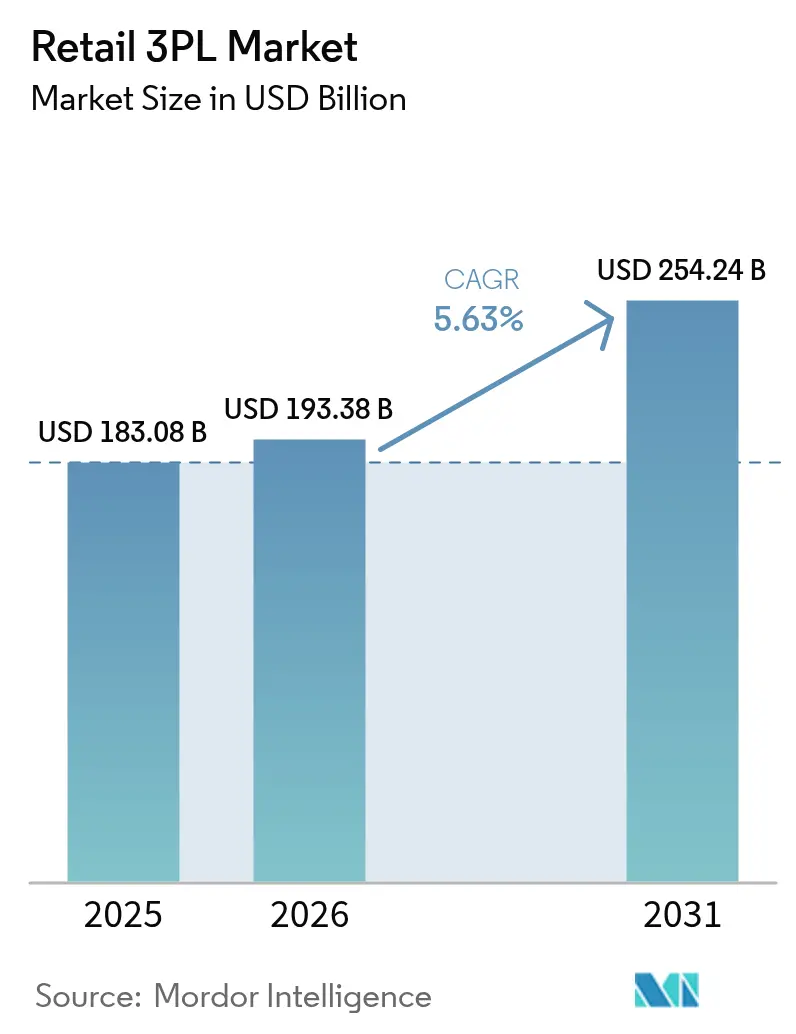

| Market Size (2026) | USD 193.38 Billion |

| Market Size (2031) | USD 254.24 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail 3PL Market Analysis by Mordor Intelligence

The Retail 3PL Market size was valued at USD 183.08 billion in 2025 and estimated to grow from USD 193.38 billion in 2026 to reach USD 254.24 billion by 2031, at a CAGR of 5.63% during the forecast period (2026-2031). Asia-Pacific leads with a 38% share in 2024 and also posts the fastest 7.62% CAGR, highlighting how retail modernisation and cross-border e-commerce concentrate growth in one region. The hybrid logistics model remains the structural cornerstone, but the asset-light approach is gaining ground, signalling a decisive shift toward variable-cost capacity, tighter technology integration, and nimble network design. Domestic Transportation Management still delivers the bulk of shipments, yet International Transportation Management grows faster as retailers pivot to global sourcing and cross-border parcel flows. Reverse logistics has moved from a peripheral service to a core differentiator because online fashion returns erode margins unless handled with specialised technology and processes. Labour shortages, wage inflation, and escalating cybersecurity threats temper growth, pushing 3PLs to automate, upskill, and harden digital defences.

Key Report Takeaways

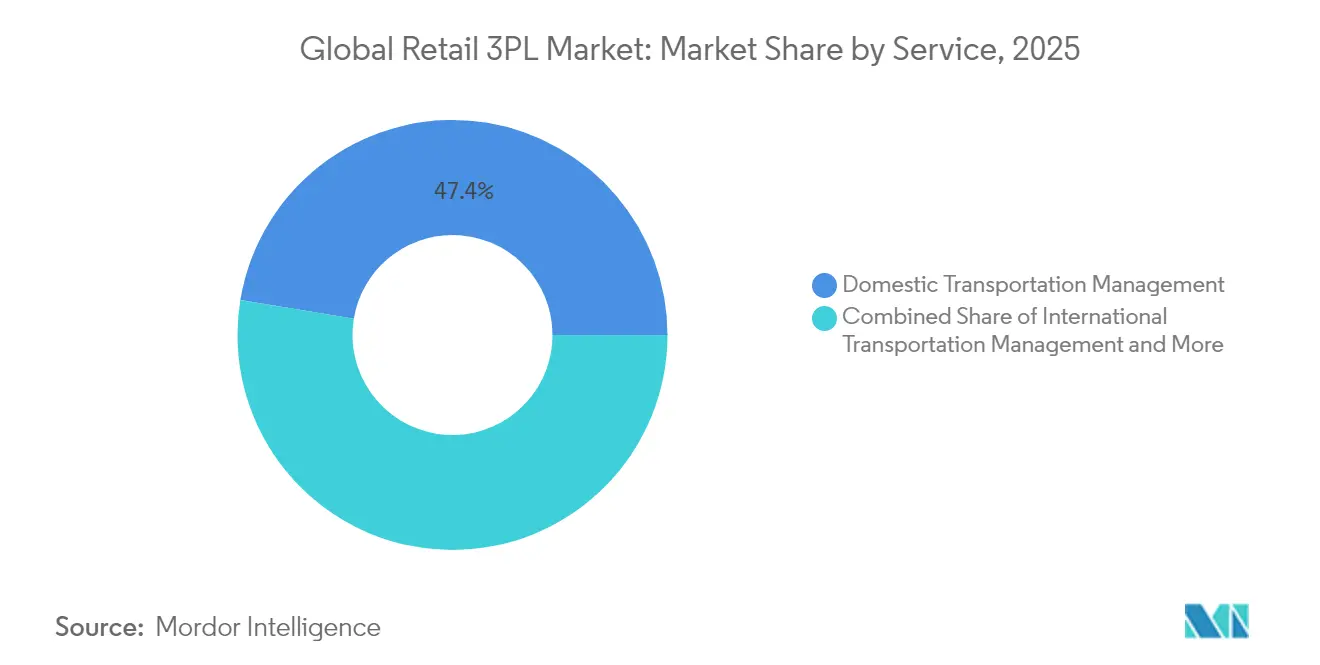

- By service, Domestic Transportation Management held 47.40% of the retail 3PL market share in 2025. The Retail 3PL Market for International Transportation Management is rising at a 6.84% CAGR between 2026-2031.

- By product category, Food & Beverages commanded a 33.55% share of the retail 3PL market size in 2025. The Retail 3PL Market for Fashion & Lifestyle is advancing at a 6.35% CAGR between 2026-2031.

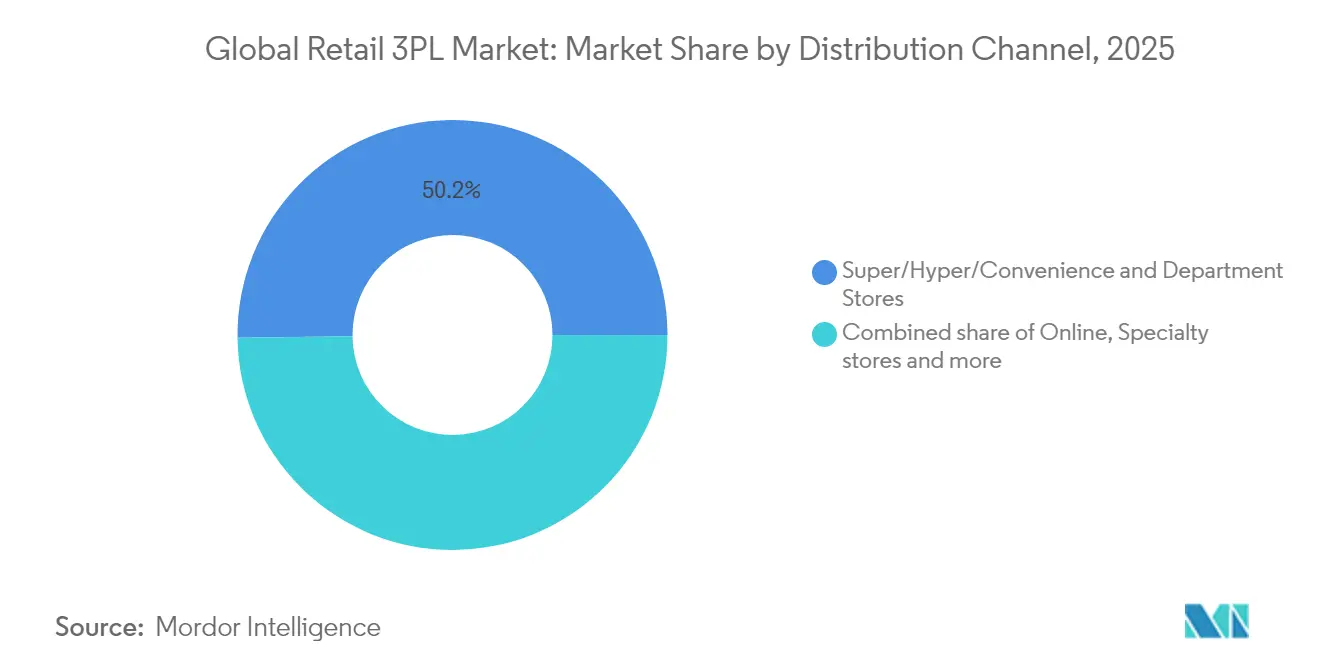

- By distribution channel, Super/Hyper/Convenience & Department Stores controlled 50.20% of the retail 3PL market size in 2025. The Retail 3PL Market for the Online channel is expanding at a 8.96% CAGR between 2026-2031.

- By the logistics model, the Hybrid model led with a 40.35% of the retail 3PL market size share in 2025. The Retail 3PL Market for the Asset-Light model is growing at 6.64% CAGR between 2026-2031.

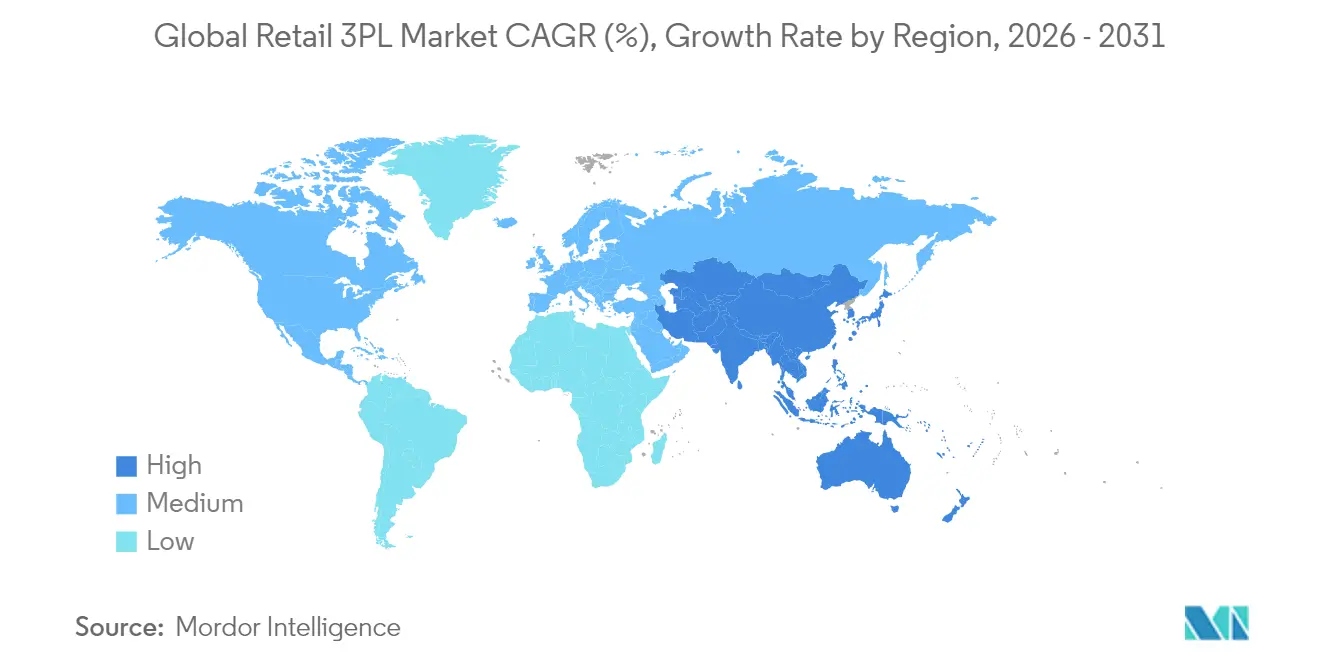

- By region, Asia-Pacific accounted for 37.60% of the retail 3PL market share in 2025. The Retail 3PL Market in Asia-Pacific continues to outpace others with a 7.34% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Retail 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in online fast-fashion returns | +1.2 | Global; strongest in North America & Europe | Medium term (3–4 years) |

| Adoption of micro-fulfilment centres | +0.9 | North America, Europe, developed Asia-Pacific | Medium term (3–4 years) |

| Cross-border e-commerce growth | +0.7 | Global; emphasis on China-to-world lanes | Long term (≥5 years) |

| Renewable-energy-powered warehouses | +0.3 | Europe, North America | Long term (≥5 years) |

| Omni-channel transformation | +1.0 | Global; led by North America | Medium term (3–4 years) |

| Near-shoring to Mexico | +0.6 | North America; spillover to Central America | Medium term (3–4 years) |

| Source: Mordor Intelligence | |||

Surge in Online Fast-Fashion Returns

Serial returners and generous return policies in online fashion retail create flux in warehouse workflows and inventory valuation. The National Retail Federation states that total retail returns hit USD 890 billion in 2024, with fashion the most affected segment. Returns now cost more than 50% of the original sales price, prompting retailers to shift the task to 3PLs that specialise in reclamation and refurbishment. Venture capital keeps flowing into technology-enabled reverse-logistics platforms, and DHL Supply Chain’s January 2025 acquisition of Inmar Supply Chain Solutions positions it as North America’s largest returns processor[1]DHL Group, “DHL Supply Chain to Acquire Inmar Returns,” group.dhl.com. Asset-light 3PLs scale swiftly in this niche because they can deploy cloud-based platforms without legacy network constraints, improving recovery rates and cycle time.

Adoption of Micro-Fulfilment Centers

Grocery chains and quick-commerce specialists compress last-mile distances by embedding 5,000-10,000 sq ft automated modules inside or beside urban stores. Hy-Vee partners with Takeoff Technologies, while Amazon pilots Fulfil’s robotics at select Whole Foods sites. The micro-fulfilment model trims unit economics: shorter picks, lower delivery miles, and higher on-shelf availability. For 3PLs, micro-fulfilment adds a new service line that blends automation engineering, maintenance, and rapid-replenishment transport. Early adopters report cycle-time reductions exceeding 30% and double-digit productivity gains, making the model a catalyst for wider network redesign.

Cross-Border E-commerce Platforms Fueling Bonded Warehousing

Retailers targeting consumers overseas rely on bonded warehouses that defer duties and simplify returns. China hosts 165 cross-border e-commerce pilot zones that have cut clearance times by 50% since 2020, accelerating throughput for brands shipping both into and out of the country. Latin American and Southeast Asian markets copy this blueprint, spurring 3PL investment in blockchain-enabled compliance and real-time customs visibility. Bonded capacity thus becomes a strategic asset that merges duty-saving benefits with speed-to-door expectations of global shoppers.

Renewable-Energy-Powered Warehouses

Solar, on-site storage, and electric-vehicle charging transform distribution hubs into micro-grids. Prologis surpasses 500 MW of installed solar and targets 1 GW in 2025. A joint Prologis–Maersk EV facility in Torrance, California, delivers 96 chargers and 18 MWh storage, supporting California’s 2035 diesel phase-out. While adoption lags in markets with lower electricity prices, regulatory incentives in Europe push 3PLs to integrate energy as part of value-added services, further differentiating providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour shortages and wage inflation | -0.8% | Global; acute in North America, Europe | Short term (≤ 2 years) |

| Cyber-security risks | -0.6% | Global | Medium term (2-4 years) |

| Fragmented trucking capacity | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Escalating warehouse rents | -0.4% | Global; urban nodes most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labour Shortages & Wage Inflation

A projected 85 million-worker gap by 2030 raises operating costs and compresses margins. Warehouse operators report a 73% labour-availability shortfall. To maintain throughput, 3PLs deploy autonomous mobile robots, labour-management software, and cross-training programs that raise productivity per hour. However, rapid wage escalation still erodes profitability in low-margin service lines, forcing providers to renegotiate contracts and pass through surcharges.

Cyber-security Risk From API-Integrated Networks

Retailers expose fulfilment APIs to 3PLs for real-time order, inventory, and transport visibility, but this openness expands the attack surface. Ninety-eight percent of organisations connect to a third party that has experienced a breach. In response, leading providers set up Security Operations Centres with AI-driven SIEM and enforce multi-factor authentication across partner ecosystems. Cyber insurance premiums rise, adding indirect cost pressure and prompting 3PLs to invest heavily in zero-trust architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: International Logistics Outpaces Domestic Growth

International Transportation Management accelerates at a 6.84% CAGR, outstripping overall retail 3PL market growth as retailers diversify sourcing and expand marketplace reach. This service line relies on optimised airfreight, duty management, and multimodal routing, helping brands shorten fashion lead times and replenish electronics during promotional spikes. UPS moves to acquire Estafeta to bolster cross-border express capacity between Mexico and the United States. The heightened demand for time-definite delivery pushes 3PLs to integrate digital freight marketplaces, intelligent routing, and carbon-efficient modal shifts.

Domestic Transportation Management still accounts for 47.40% of 2025 revenue, thanks to entrenched brick-and-mortar networks and high-volume parcel flows. Amazon shipped 9 billion same- or next-day packages in 2024, covering 140 US metro areas and setting new service benchmarks. Continuous network densification, predictive inventory placement, and regional sort centres shorten final-mile distance and lower per-parcel cost. The retail 3PL market size for domestic services will continue growing, yet its share may erode as international flows accelerate and omnichannel models demand end-to-end coverage.

By Product: Food & Beverages Dominates While Fashion & Lifestyle Accelerates

Food & Beverages holds 33.55% of the 2025 revenue. Cold-chain compliance, stringent expiry windows, and multi-temperature handling warrant specialised transport and warehousing, making this segment sticky and resilient. Blockchain pilots trace farm-to-fork provenance, cutting recall time and limiting waste. Grocery retailers push 3PLs to certify facilities, integrate IoT sensors, and deploy predictive spoilage analytics, embedding technology deeper into daily operations.

Fashion & Lifestyle grows fastest at 6.35% CAGR, riding booming online sales and high return volumes. Vertical integration gains traction as brands internalise printing, embroidery, or micro-batch manufacturing to meet rapid trend cycles. The retail 3PL market size dedicated to fashion returns processing widens because 96% of returned items handled by GXO re-enter inventory, preserving margin. Circular-economy models, including second-hand apparel marketplaces, demand meticulous grading, sanitising, and re-listing workflows that sophisticated 3PLs now embed into fulfilment logic.

By Distribution Channel: Online Segment Drives Innovation

The Online channel expands at 8.96% CAGR and forces 3PLs to engineer agile, software-rich fulfilment. DHL’s 2024 consumer survey shows 57% of shoppers use smartphones for purchases and 41% abandon carts due to costly shipping, exposing how logistics speed and transparency equal conversion. Provider differentiation thus shifts toward API-ready platforms, real-time delivery ETAs, and sustainable packaging.

Super/Hyper/Convenience & Department Stores still anchor 50.20% of 2025 revenue because physical stores retain traffic and offer immediate product access. Yet store-pickup and curbside fulfilment rely on the same orchestration software as e-commerce, blurring channel distinctions. Retailers engage 3PLs to unify inventory across online and offline nodes, ensuring accuracy and timely replenishment.

By Logistics Model: Asset-Light Approaches Gain Momentum

Hybrid models, combining owned assets with partner capacity, held a 40.35% share in 2025 and match established retailers’ need for control in core markets, plus scalability in peak seasons. These models reduce capital intensity yet retain service consistency because lead sites remain under direct management.

Asset-Light models grow fastest at 6.64% CAGR as rising interest rates and rapid demand cycles make fixed assets riskier. RXO’s USD 1.025 billion purchase of Coyote Logistics underscores the appetite for brokerage scale and data-driven capacity. Asset-heavy networks keep traction in high-compliance niches; DHL Supply Chain runs 520 North American warehouses staffed by 52,000 associates. The retail 3PL industry, therefore, features the coexistence of flexible brokerages and deep-capability operators, with convergence around common digital platforms to sync capacity and demand.

Geography Analysis

Asia-Pacific leads with a 37.60% share in 2025 and posts a 7.34% CAGR. China’s 165 e-commerce pilot zones slash customs delays, and India’s omnichannel adoption gains speed as mobile web traffic tops 60% of total sessions. Southeast Asian logistics corridors attract investment in smart sortation hubs and bonded, duty-free parks. Government incentives and booming middle-class consumption underpin sustained double-digit parcel growth, making the region a strategic imperative for global 3PLs. The retail 3PL market size in Asia-Pacific expands in tandem with electronic-goods exports and intra-Asia cross-border commerce.

North America remains technology-intensive and innovation-driven. Amazon leads the marketplace, while XPO expands less-than-truckload capacity after a major rival exited the market. High labour costs propel automation roll-outs, with Symbotic installing goods-to-person systems across Walmart’s network, adding a USD 5 billion backlog. Environmental regulations in California spur electrified drayage fleets, prompting 3PLs to invest in charging depots and renewable-powered distribution centres.

Europe features a regulatory push for carbon neutrality and continues to refine cross-border parcel compliance after Brexit. Prologis deploys rooftop solar at scale, and leading carriers trial hydrogen trucks along dense freight corridors. Escalating property rents in urban zones encourage multi-storey warehousing and robotic systems that maximise cubic utilisation. South America, the Middle East, and Africa remain smaller but show rapid e-commerce uptake, encouraging global 3PLs to pursue asset-light joint ventures, local partnerships, and targeted last-mile acquisitions.

Competitive Landscape

Global leaders concentrate on scale, technology, and vertical integration. DSV’s planned EUR 14.3 billion (USD 16.28 billion) acquisition of Schenker will deepen European penetration and integrate Schenker’s value-added warehousing into DSV’s network. GXO’s USD 718 million purchase of Wincanton strengthens UK grocery and FMCG fulfilment. DHL Supply Chain gains returns-processing leadership through the Inmar deal.

E-commerce giants morph into logistics powerhouses. Amazon generated USD 156 billion from third-party services in 2024, dwarfing traditional 3PL revenues and compelling incumbents to match Amazon’s same-day benchmarks. Walmart’s automation investments pull robotics vendors like Symbotic into mainstream 3PL conversations, elevating pick-density expectations across the sector.

Brokerage consolidation heats up. RXO’s Coyote acquisition and Knight-Swift’s Dependable Highway Express deal expand network reach and tap synergies in procurement and asset utilisation. Asset-light economics lure investors because they deliver robust returns on capital via variable-cost structures and advanced data science. Providers unable to digitise encounter a margin squeeze and risk relegation to commodity capacity suppliers. Emerging disruptors deploy AI to forecast demand, match freight, and orchestrate multi-node fulfilment, creating white-space in sustainable logistics, bonded e-commerce, and reverse logistics specialties.

Retail 3PL Industry Leaders

DHL Supply Chain & Global Forwarding

XPO Inc.

DSV A/S

C.H. Robinson Worldwide

Ryder Supply Chain Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DHL Supply Chain acquired Inmar Supply Chain Solutions, becoming the largest reverse-logistics provider in North America.

- January 2025: Symbiotic bought Walmart’s Advanced Systems and Robotics unit for USD 200 million, adding USD 5 billion to its automation backlog.

- September 2024: DSV agreed to acquire Schenker for EUR 14.3 billion (USD 15.5 billion) and expects completion in Q2 2025.

- September 2024: RXO completed the USD 1.025 billion purchase of Coyote Logistics, targeting USD 40 million cost synergies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global retail third-party logistics (3PL) market as every instance in which a retailer, whether an online pure-play or a physical chain, outsources transportation management, value-added warehousing, fulfillment, or reverse-logistics activities to an independent provider that earns fee-based revenue from those services.

Scope exclusion: in-house retailer fleets and parcel integrators acting solely as carriers are outside our count.

Segmentation Overview

- By Service

- Domestic Transportation Management

- Roadways

- Railways

- Airways

- Waterways

- International Transportation Management

- Roadways

- Railways

- Airways

- Waterways

- Value-Added Warehousing and Distribution (VAWD)

- Domestic Transportation Management

- By Product

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (accessories, apparel, footwear)

- Furniture

- Electronics and Household Appliances

- Other Products

- By Distribution Channel

- Super/Hyper/Convenience and Department Stores

- Specialty Stores

- Online

- Other Channels

- By Logistics Model

- Asset-Light (Management-Based)

- Asset-Heavy (Own Fleet and Warehouses)

- Hybrid

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Vietnam

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview contract-logistics managers at retailers, regional 3PL executives, automation vendors, and freight brokers across North America, Europe, and Asia. The conversations test preliminary numbers, surface typical pricing bands, and reveal regional quirks such as micro-fulfillment uptake or cross-border return rates, allowing us to refine assumptions before final modeling.

Desk Research

We begin with structured desk work that screens government trade statistics, customs databases, and retail sales records from sources such as UN Comtrade, the U.S. Census Bureau's Quarterly E-commerce Report, Eurostat's retail volume index, and the National Retail Federation's global returns surveys. Company 10-Ks, investor decks, and retailer annual reports supplement lane-level volumes, while news archives pulled from Dow Jones Factiva track contract awards and mergers that shift share. D&B Hoovers supplies financial splits of large 3PLs, enabling us to separate retail revenue from other verticals. These sources build the reference spine; still, many additional open datasets and industry association briefs are reviewed to validate facts and close minor gaps.

Market-Sizing & Forecasting

A top-down demand pool is first reconstructed from retail merchandise sales, e-commerce penetration, and average logistics spend ratios; these are calibrated with indicators like parcel return percentages, warehouse rental indices, cross-border online sales, fuel surcharges, and labor cost trackers. Results are then compared with selective bottom-up roll-ups of 3PL retail revenue, channel checks, and sampled average selling price times volume math to ensure realism. Forecasts to 2030 rely on a multivariate regression that blends the above drivers with scenario analysis for inflation and trade policy shifts, and each variable's trajectory is endorsed by our primary research panel.

Data Validation & Update Cycle

Outputs face multi-step variance checks against historical series and peer signals. An analyst other than the model owner reviews anomalies, and we refresh the dataset yearly, issuing interim tweaks when material events, such as major acquisitions, tariff shocks, or pandemic-type disruptions, occur.

Why Mordor's Retail 3PL Baseline Commands Reliability

Published numbers often diverge because firms mix broader logistics scopes, apply blanket multipliers, or freeze exchange rates. Our disciplined scope, live refresh cadence, and variable-level cross-checks make the Mordor baseline the dependable choice for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 183.08 B (2025) | Mordor Intelligence | - |

| USD 287.46 B (2024) | Global Consultancy A | Includes parcel integrators and gig-economy couriers, relies on revenue extrapolations without matching to retailer spend pools |

| USD 438.87 B (2022) | Trade Journal B | Merges wholesale with retail, back-casts using a flat CAGR, and omits returns-rate reconciliation |

Taken together, the comparison shows that while others adopt generous service baskets or simplified growth factors, Mordor Intelligence anchors its figures in clearly defined retail activities, cross-verified variables, and an annual refresh that keeps the baseline trustworthy for decision makers.

Key Questions Answered in the Report

What is the current size of the retail 3PL market?

The market stands at USD 193.38 billion in 2026 and is projected to reach USD 254.24 billion by 2031.

Which region drives the fastest growth in retail 3PL services?

Asia-Pacific leads both in share (37.60% in 2025) and growth, expanding at a 7.34% CAGR through 2031.

Why are reverse-logistics capabilities attracting investment?

Online fashion returns cost more than 50% of the original sale value and reached USD 890 billion industrywide in 2024, prompting 3PLs to scale specialised processing networks.

How fast is the online distribution channel growing?

The online channel posts a 8.96% CAGR over 2026-2031, almost double the overall market rate.

What is driving the shift toward asset-light logistics models?

Retailers seek variable-cost flexibility, and asset-light 3PLs outperform peers in shareholder returns, leading to 6.64% CAGR in this model.

How are big-box retailers changing their fulfilment strategies?

They integrate automation and store-based fulfilment; for example, 95% of Target’s online orders now ship from stores, reducing delivery costs 40% and cutting transit time 30%.

Page last updated on: