Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

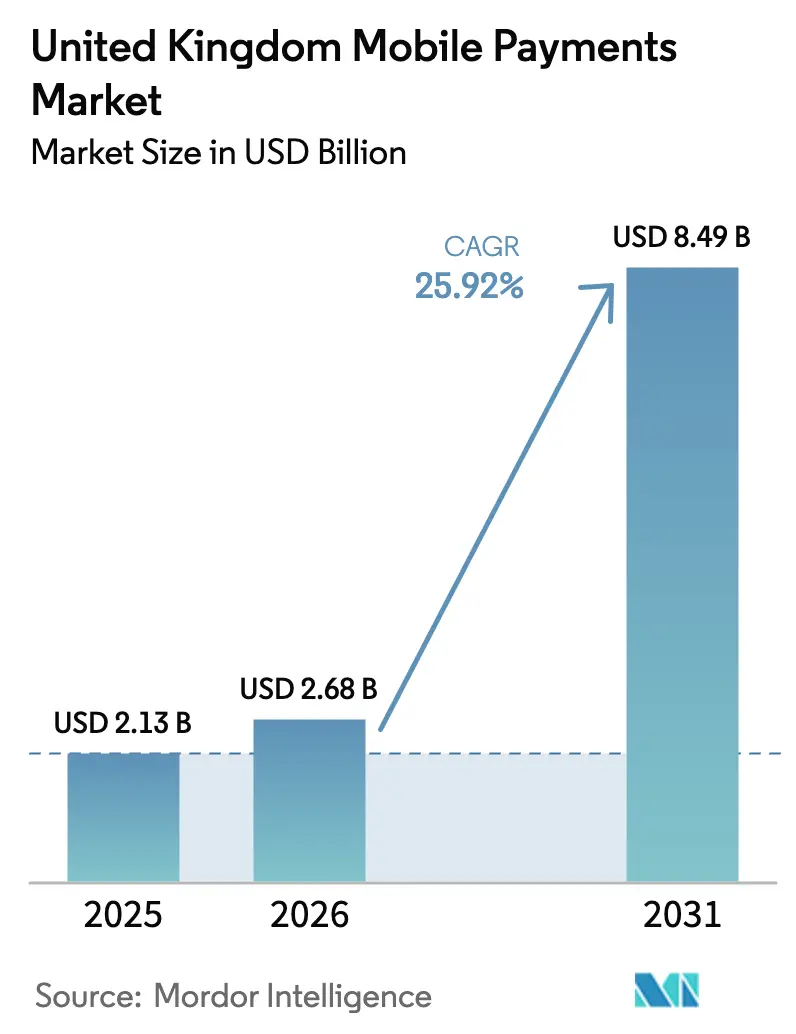

| Base Year Market Size (2025) | USD 2.13 Billion |

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 25.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Mobile Payments Market Analysis by Mordor Intelligence

The United Kingdom Mobile Payments Market size was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.68 billion in 2026 to reach USD 8.49 billion by 2031, at a CAGR of 25.92% during the forecast period (2026-2031). The expansion mirrors the country’s reputation as a payments-technology trailblazer, where open-banking mandates, instant account-to-account rails and a strong cultural bias toward contactless convenience combine to make the smartphone an everyday financial hub. High merchant acceptance of near-field communication readers, mass-market use of fingerprint and facial authentication and the regulatory green light for variable recurring payments (VRPs) have all normalised mobile checkout in grocery stores, cafés and public transport. At the same time, fintech challengers keep chipping away at incumbents’ interchange income streams, and big-tech wallets strengthen ecosystem lock-in by embedding payment credentials deep inside operating systems. On the downside, a persistent rise in authorised push-payment (APP) fraud and the long-standing cap on consumer card interchange fees are pressuring providers to double down on behavioural-analytics engines, tokenisation upgrades and diversified revenue models.

Key Report Takeaways

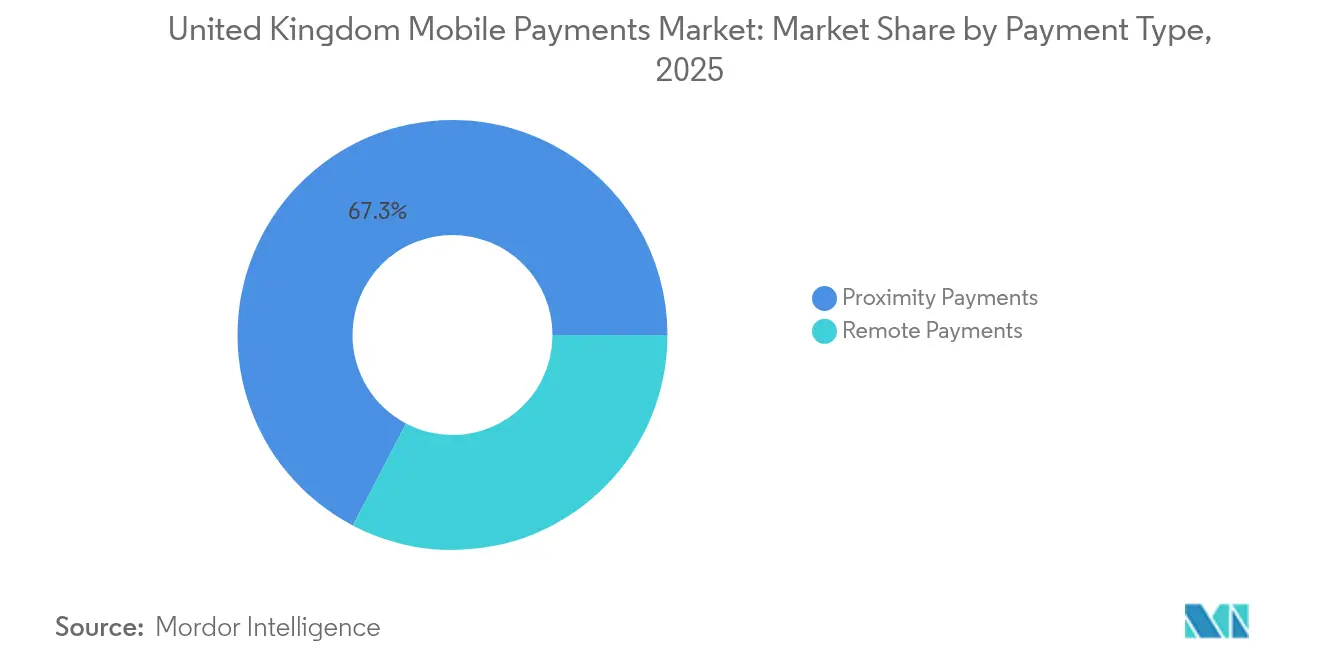

- By payment type, proximity captured 67.32% of the United Kingdom mobile payments market share in 2025; remote payments are forecast to expand at a 30.12% CAGR to 2031.

- By transaction type, the in-store POS segment led with 59.25% revenue share in 2025, while P2P transactions record the highest projected CAGR at 28.14% through 2031.

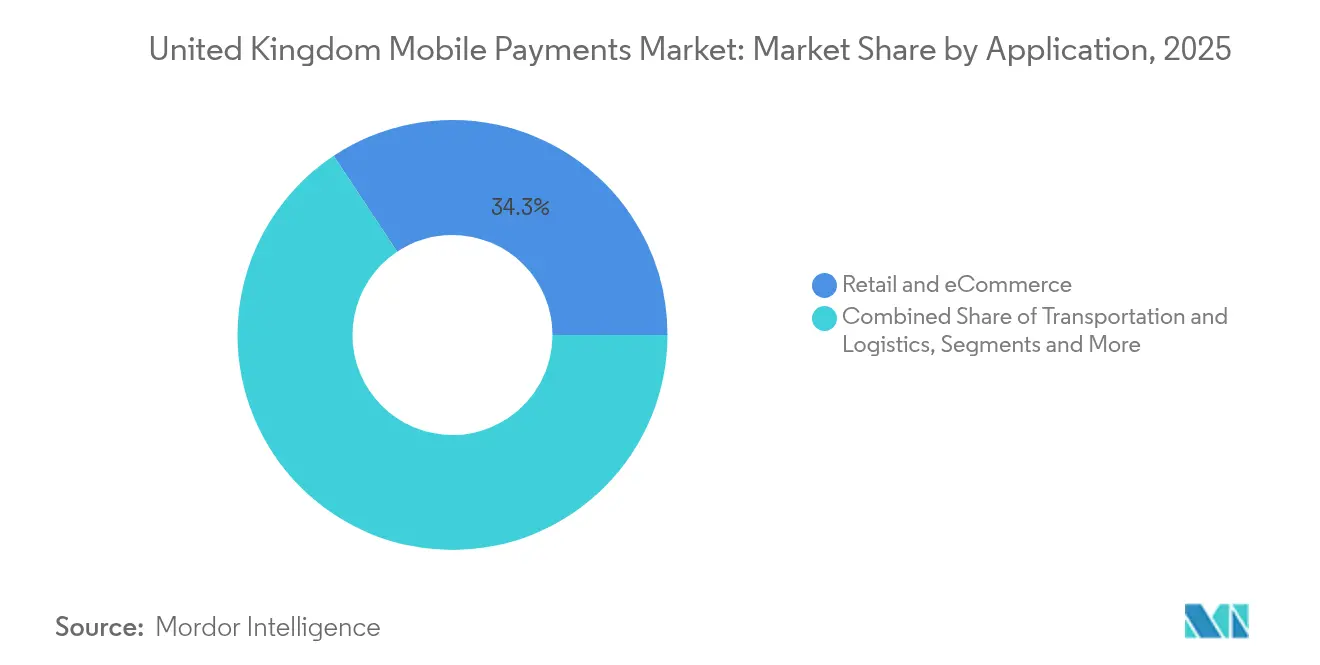

- By application, retail and e-commerce accounted for 34.32% share of the United Kingdom mobile payments market size in 2025; transportation and logistics will grow fastest at a 31.12% CAGR to 2031.

- By end-user, personal users held 81.35% of the United Kingdom mobile payments market share in 2025, whereas the business segment is advancing at a 24.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Development of open-banking-enabled wallet top-ups | +5.3% | UK-wide, urban concentration | Medium term (2–4 years) |

| U.K. Faster Payments Scheme accelerating P2P adoption | +4.8% | National, metro focus | Short term (≤2 years) |

| Surge in QR-code acceptance among SME merchants | +3.7% | England, Scotland, Wales | Medium term (2–4 years) |

| Growing wearable payments on London transport network | +2.9% | London, other cities later | Medium term (2–4 years) |

| Retailer-led super-app ecosystems | +3.2% | UK-wide | Medium term (2–4 years) |

| BNPL-integrated wallets driving basket conversion | +4.1% | National, e-commerce hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Development of Open-Banking-Enabled Wallet Top-Ups

Open-banking payment volumes reached USD 57 billion in 2024 and are forecast to climb 209% by 2029, helped by a widening circle of application-programming-interface (API) standards and consumer familiarity with “pay-by-bank” buttons. Because the model removes card networks from the funding flow, merchants pay materially lower fees while customers enjoy the extra security of bank-grade authentication. The Financial Conduct Authority’s ongoing work on VRP frameworks is accelerating product launches in which a wallet “pulls” funds straight from a user’s account without additional credential entry. As of 2024, 13% of digitally active consumers and 18% of small businesses use an open-banking service at least once a month. Providers anticipate that real-time, multi-bank top-ups will become table-stakes functionality over the next two years, anchoring wallet loyalty and raising the United Kingdom mobile payments market’s profile as a benchmark for embedded finance.

U.K. Faster Payments Scheme Accelerating P2P Adoption

The Faster Payments Scheme cleared GBP 3.7 trillion (USD 4.7 trillion) in account-to-account transfers during 2023, up 15% from 2022.[2]James Wharton, “Market Review of Card Scheme and Processing Fees,” Payment Systems Regulator, psr.org.uk Instant settlement transforms person-to-person cash flows, making it easier to split bills, gift money or settle rent within seconds. Visa’s A2A overlay service, launched in 2025, brings chargeback-style dispute management and biometric confirmation to the scheme, making higher-ticket P2P transfers safer. For banks, the surge in low-cost, high-frequency traffic is a cross-sell gateway for deposits and unsecured credit, underlining why instant rails are now a board-level priority.

Surge in QR-Code Acceptance Among SME Merchants Across England

QR-code scans once occupied a niche role in specialist retail but now represent a cost-effective card alternative for corner shops, market stalls and mobile traders. With hardware needs limited to a printed code and any camera-equipped phone, merchants keep processing costs below 0.2%, far under regulated interchange caps. Tokenisation and dynamic codes reduce the risk of credential replay attacks, helping consumer trust catch up with convenience. Analysts expect a meaningful share of 2025 smartphone users to rely on QR codes for weekly purchases, an inflection that will widen acceptance to economically sensitive rural and suburban districts where countertop PIN pads were cost-prohibitive.

Growing Wearable Payments on London Transport Network

Transport for London (TfL) now handles more than 500 million trips each year, with 10% of those journeys paid via smartwatches or fitness bands configured for contactless settlement.[1]Paul Hindle, “TfL Tops 1 Billion Contactless Journeys,” FinTech Futures, fintechfutures.com The system automatically charges the lowest possible fare and eliminates the time cost of ticket queues. Since rollout, TfL’s network has processed in excess of five billion contactless journeys using 40 million unique cards from 145 countries, proving global travellers trust the model. The success story is prompting large regional bus and rail operators to adopt the same open-loop architecture, helping keep daily ride frequency at the centre of wallet-provider growth strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange fee caps squeezing PSP margins | –2.1% | UK-wide, hits small PSPs hardest | Short term (≤2 years) |

| Rising APP fraud losses | –1.9% | Urban concentration | Short term (≤2 years) |

| Fragmented wallet loyalty-point interoperability | –1.4% | National, multi-wallet users | Medium term (2–4 years) |

| Demographic payments exclusion (55+ cohort) | –1.6% | Rural bias | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Interchange Fee Caps Squeezing PSP Margins

Debit and credit interchange fees have sat at 0.20% and 0.30% respectively since 2015, creating a margin squeeze for small and mid-tier payment service providers (PSPs).[3]Charlotte Wood, “Visa Boosts Consumer Protection With Smarter Bank Transfer Payments,” Visa, visa.co.uk Card schemes have responded by raising non-regulated ancillary fees, adding an estimated GBP 170 million (USD 206 million) to UK merchants’ cost of acceptance over seven years. Smaller PSPs without volume-based rebates face disproportionate drag and are accelerating toward consolidation or strategic partnerships. Consequently, many are pivoting to account-to-account propositions including Pay-by-Bank buttons to regain share of checkout.

Rising APP Fraud Losses

APP fraud totalled GBP 450.7 million (USD 545 million) in 2024. New reimbursement rules allow victims to recover up to 86% of lost funds within days, improving consumer trust but raising compliance and treasury costs for PSPs. Seventy-two percent of fraud originates online, with investment scams contributing the largest absolute losses. Providers are rolling out behavioural biometrics, real-time device fingerprinting and network-level scam databases, but the arms race inflates opex and can slow time-to-market for new features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Proximity Dominates While Remote Accelerates

Proximity transactions accounted for 67.32% of the United Kingdom mobile payments market share in 2025, cementing contactless as the default tender at grocery checkouts, quick-service restaurants and mass-transit gates. Biometric authentication and token-on-file storage keep the fraud-to-sales ratio below card-not-present benchmarks. Remote payments, by contrast, are on track for a 30.12% CAGR, propelled by one-click “buy now” widgets in native apps and progressive-web-app checkout. Retailers are using remote wallets to merge cart abandonment-recovery emails, micro-loyalty incentives and seamless re-orders, blurring the once clear channel lines between physical and digital retail.

As the QR-code boom continues, the boundary between proximity and remote transactions grows increasingly porous. Consumers scan a code at the table, authenticate in their wallet, and the transaction settles remotely even though both parties are in the same venue. Such hybrid experiences further expand the total addressable United Kingdom mobile payments market size.

By Transaction Type: In-Store POS Leads While P2P Grows Fastest

In-store POS claimed 59.25% of 2025 value. Visa’s Tap-to-Phone solution, live on standard Android devices, delivered 320% volume growth within a year and onboarded thousands of micro-merchants that previously relied on cash only. The democratisation of acceptance allows small businesses florists, pop-up food stalls, home-repair contractors to plug into the digital economy without hardware subsidies.

P2P, advancing at 28.14% CAGR, is reshaping social payment etiquette. Instant refunds from split ride-hailing, rent settlements across flatmates and neighbourhood fundraisers all funnel increasing aggregate value through mobile apps. As biometric-secured P2P per-transaction limits rise, the segment will eat into higher-value transfers traditionally executed via desktop banking.

By Application: Retail Retains Lead While Transportation Accelerates

Retail and e-commerce collectively delivered 34.32% of the United Kingdom mobile payments market size in 2025. Grocery chains prime customers with digital-only discounts unlocked exclusively via wallet pay-in, reinforcing app habit formation. Fashion and electronics retailers run targeted pay-with-wallet flash sales that cross-reference loyalty tiers and available BNPL credit lines.

Transport applications grow fastest, at 31.12% CAGR to 2031. TfL’s proven success has lit the path for Manchester and Birmingham pilot schemes financed under the Department for Transport’s multi-modal Pay As You Go expansion. Real-time fare capping, combined with wearables acceptance, extends mobile payments into an essential daily-frequency category, a coveted position for wallet providers aiming to dominate top-of-mind consumer preference.

By End-User: Personal Users Dominate While Business Adoption Accelerates

Personal customers generated 81.35% of 2025 volume. Six in ten adults now possess at least one mobile wallet registration, and 52% used a wallet for payment in the last 12 months. Biometric login, tokenised credentials and single-tap refunds have normalised smartphones as transactional companions for all but the most digitally excluded demographics.

Business usage, while smaller, is scaling rapidly at 24.18% CAGR. More than 60% of SME banking clients accessed accounts via a mobile app in 2024, while 56% of business banks offer mobile-only onboarding. Tap-to-Phone acceptance enables mobile invoice settlement at the point of service, accelerating receivables, and reducing reliance on physical terminals. As corporate card and expense-management providers embed wallet tokens, the United Kingdom mobile payments market size attributable to B2B flows will climb steadily.

Geography Analysis

London remains the epicentre. TfL’s open-loop network, serving over five billion contactless rides, sets benchmarks that fintechs replicate worldwide. The capital’s diverse resident and tourist mix ensures standing demand for multi-currency acceptance, propelling wallet upgrades to support cross-border token translation. In addition, London hosts the highest density of fintech incubators, making it the natural test market for “beta” wallet capabilities like digital identity credentials.

Northern and Midlands centres Manchester, Birmingham and Leeds leverage city-region partnerships to extend PAYG transit acceptance to trams and buses. Edinburgh’s technology cluster sees strong QR uptake among SMEs keen to side-step card-scheme fee inflation. Coastal hubs such as Brighton, Bournemouth and Blackpool prioritise wallet acceptance in hospitality to serve international visitors.

Conversely, rural counties face bandwidth gaps and an ageing demographic profile. Seventeen percent of adults in remote areas report problems accessing banking, and a significant proportion still rely on post-office cash services. Government funding of GBP 8.3 billion for highways and GBP 4.7 billion for local transport between 2025 and 2030 may indirectly bolster mobile coverage and POS infrastructure, but providers must bridge the interim by offering offline-authorisation modes and hybrid chip-and-mobile cards.

Competitive Landscape

Two global device makers command a majority of mobile wallet token volumes, enough to trigger concurrent inquiries by the FCA and the Payment Systems Regulator into potential competition bottlenecks. Their advantage rests on hardware-embedded secure elements and default-wallet status at the operating-system layer. Traditional card networks hold a complementary moat via tokenisation services and brand acceptance norms, but interchange caps and fee scrutiny keep profitability under the microscope.

Domestic challenger banks compete through cloud-native cores that integrate payments, savings, and invoice workflows under a single login. Mambu’s December 2024 purchase of Numeral adds a modern payment-orchestration layer to its SaaS core, allowing rapid deployment of instant-payment use cases without legacy constraints. Smaller PSPs must either acquire similar capabilities or risk relegation to white-label processing.

Loyalty interoperability, real-time credit scoring, and offline biometric authorisation remain underdeveloped niches. Players who amalgamate these functions can create defensible moats by offering end-to-end journey coverageshopping baskets, transit, peer transfers and cross-border remittances in a uniform user experience.

United Kingdom Mobile Payments Industry Leaders

Apple Inc.

Google LLC (Google Pay)

Samsung Electronics (Samsung Pay)

PayPal (Europe) S.à r.l. et Cie, S.C.A.

Amazon Payments, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UK Finance reported 3.31 million confirmed fraud cases in 2024; APP incidents fell 20%, but remote-purchase fraud climbed 22%.

- May 2025: The FCA issued its 2025/26 work programme, highlighting a data-driven supervision model and a digitised authorisation pipeline for payment firms.

- April 2025: Nuvei unveiled an omnichannel gateway for the UK gaming sector, unifying card, e-money and A2A options under a single API to streamline operator reconciliation.

- March 2025: Visa announced 320% year-on-year UK Tap-to-Phone growth; 22% of activations were first-time small businesses.

United Kingdom Mobile Payments Market Report Scope

Mobile payments refer to the different media of payments through software as a service in smart electronic devices, including smartphones, smart wearables, or any other device facilitating the supported operating system. The payment can be made in real-time or remotely through the cloud setup.

The United Kingdom mobile payments market is segmented by type (Proximity Payment and Remote Payment).

By Payment Type

| Proximity Payments |

| Remote Payments |

By Transaction Type

| Peer-to-Peer (P2P) |

| In-store Point-of-Sale (POS) |

| Person-to-Merchant (P2M/Checkout) |

| Other Transaction Types |

By Application

| Retail & eCommerce |

| Transportation and Logistics |

| Hospitality & Food-Service |

| Government & Public Sector |

| Other Applications (Education, Healthcare) |

By End-user

| Personal |

| Business |

| By Payment Type | Proximity Payments |

| Remote Payments | |

| By Transaction Type | Peer-to-Peer (P2P) |

| In-store Point-of-Sale (POS) | |

| Person-to-Merchant (P2M/Checkout) | |

| Other Transaction Types | |

| By Application | Retail & eCommerce |

| Transportation and Logistics | |

| Hospitality & Food-Service | |

| Government & Public Sector | |

| Other Applications (Education, Healthcare) | |

| By End-user | Personal |

| Business |

Key Questions Answered in the Report

What is the current size of the United Kingdom mobile payments market?

The market stands at USD 2.68 billion in 2026 and is projected to reach USD 8.49 billion by 2031.

Which segment holds the largest share of the United Kingdom mobile payments market?

Proximity payments dominate with 67.32% value share thanks to widespread tap-to-pay acceptance.

Why are variable recurring payments (VRPs) significant for UK mobile payments?

VRPs allow merchants to pull funds directly from bank accounts, bypassing card fees and giving users fine-grained control over authorisations.

How is APP fraud affecting mobile payment adoption?

APP fraud caused GBP 450.7 million in losses in 2024, prompting tighter reimbursement rules that improve consumer confidence but raise compliance costs for PSPs.

Which geography shows the fastest growth in mobile payments within the UK?

Piloted Pay As You Go transit schemes in Manchester and Birmingham indicate those regions will see the sharpest uptake, although London remains the overall leader.

How are interchange-fee caps influencing provider strategy?

Fee caps compress margins, so PSPs are investing in account-to-account rails and value-added analytics to diversify revenue away from regulated card interchange.

Page last updated on: