Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

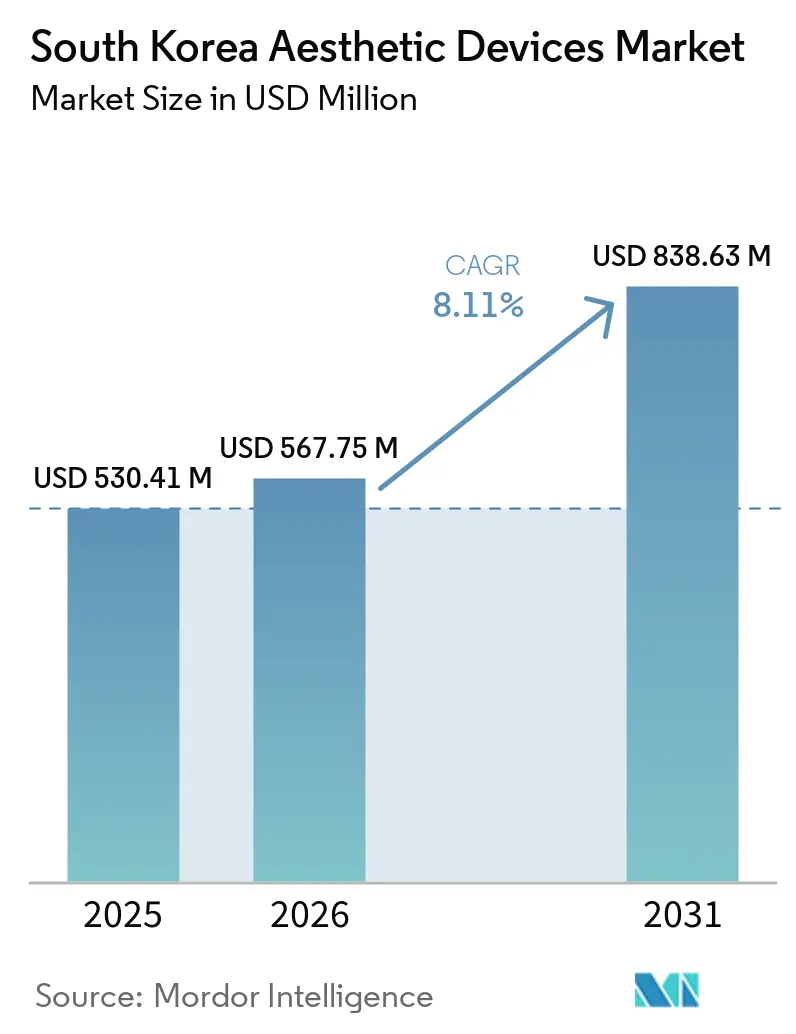

| Base Year Market Size (2025) | USD 530.41 Million |

| Market Size (2026) | USD 567.75 Million |

| Market Size (2031) | USD 838.63 Million |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Aesthetic Devices Market Analysis by Mordor Intelligence

The South Korea Aesthetic Devices Market size was valued at USD 530.41 million in 2025 and is estimated to grow from USD 567.75 million in 2026 to reach USD 838.63 million by 2031, at a CAGR of 8.11% during the forecast period (2026-2031).

The South Korea aesthetic devices market benefits from Seoul’s role as a manufacturing and consumption hub, where energy-based platforms are trialed in Gangnam clinics before wider roll-outs. Inbound medical tourism, which brought 1.17 million foreign patients in 2024, continues to funnel demand into the South Korea aesthetic devices market as K-beauty social media turns clinics into live showrooms.[1]Staff Writer, “Medical Tourism Statistics 2024,” Korea Health Industry Development Institute, khidi.or.kr The South Korea aesthetic devices market also gains momentum from rising adoption among men and from preventive procedures sought by 18-34-year-olds, a cohort that values minimal downtime and employer-subsidized benefits. Yet high capital costs for advanced platforms and stringent MFDS compliance slow purchase cycles, tempering near-term growth in the South Korea aesthetic devices market.

Key Report Takeaways

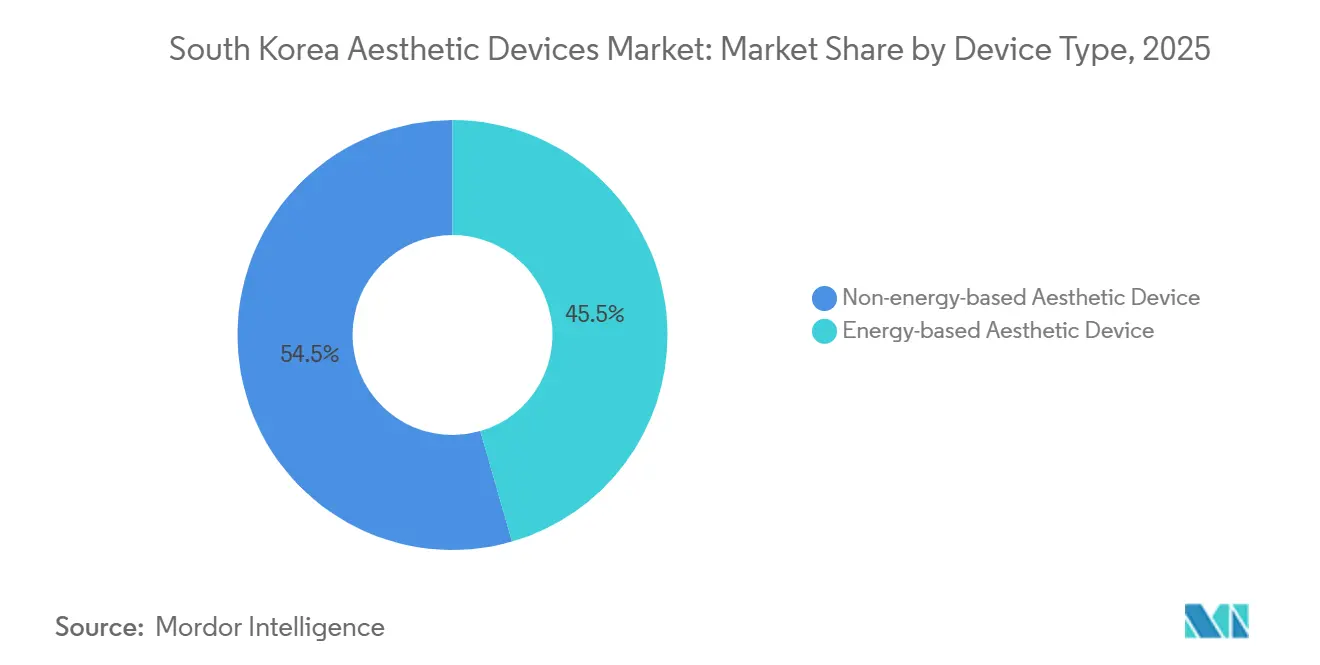

- By device type, non-energy devices led with 54.52% share of the South Korean aesthetic devices market size in 2025, and energy-based devices are anticipated to register the fastest CAGR of 8.56% during the forecast period.

- By application, skin rejuvenation & tightening held 32.51% of the South Korean aesthetic devices market size in 2025, and body contouring & cellulite reduction is advancing at a 9.12% CAGR to 2031.

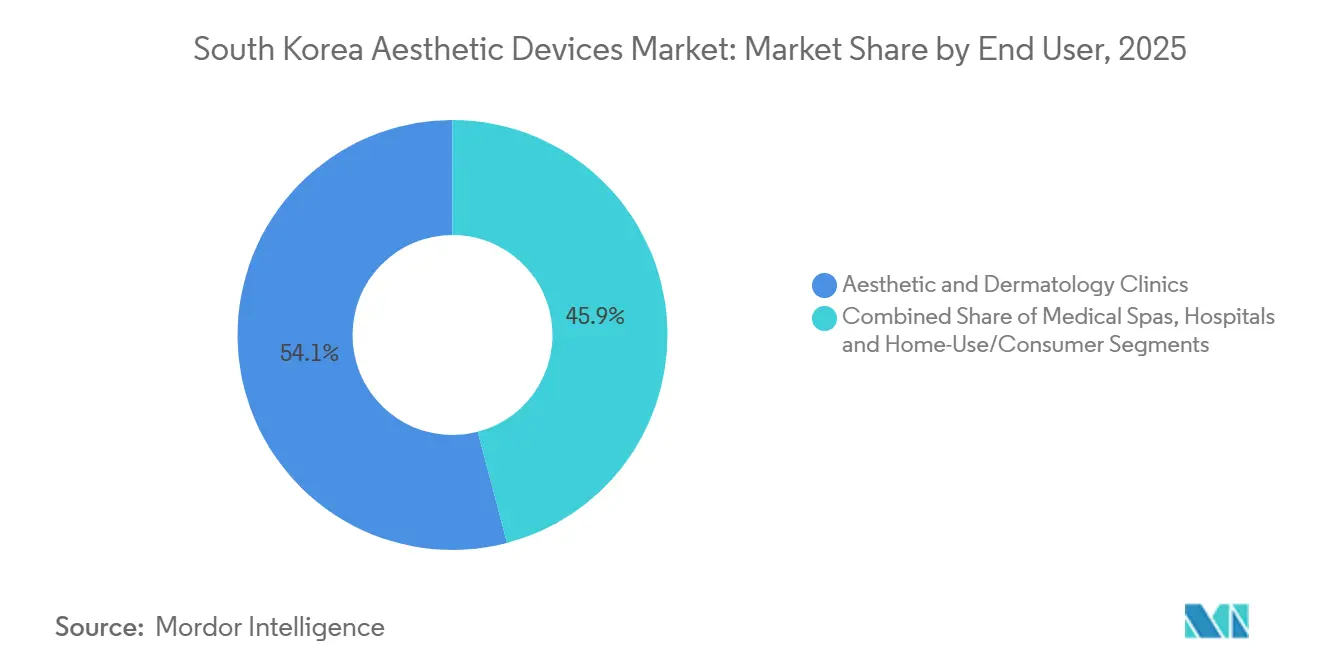

- By end user, aesthetic and dermatology clinics controlled 54.07% revenue share in 2025, and is anticipated to record the fastest CAGR at 8.65% through 2031.

- By gender, the female segment accounted for 82.01% of the market size in 2025, whereas the male segment posted a 8.79% CAGR during the forecast period.

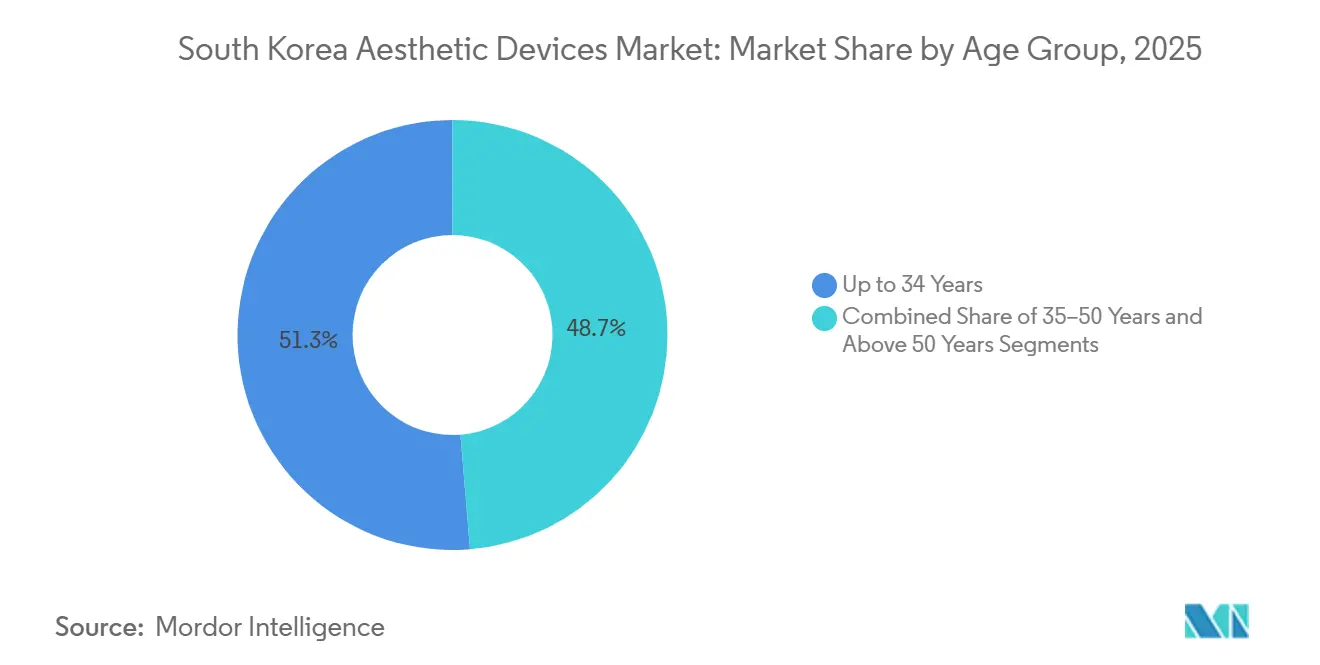

- By age group, the up to 34 years segment commanded 51.29% share of the South Korea aesthetic devices market size in 2025 and the 35–50 years segment is growing at 8.73% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Inbound Medical Tourism & K-Beauty Influence | +1.2% | Seoul, Busan | Medium term (2-4 years) |

| Rapid Adoption of Minimally Invasive & Energy-Based Technologies | +1.5% | Nationwide, metro clinics | Short term (≤ 2 years) |

| Aging Population Drives Anti-Aging Demand | +0.9% | Urban centers | Long term (≥ 4 years) |

| Growing Male Aesthetics Market Segment | +0.8% | Seoul, Incheon | Medium term (2-4 years) |

| Rising Demand for Personalized & Preventive Aesthetic Treatments | +0.7% | Major cities | Medium term (2-4 years) |

| Private-Equity-Backed Clinic-Chain Expansion | +0.6% | Tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Inbound Medical Tourism & K-Beauty Influence

Foreign patient arrivals reached 1.17 million in 2024, and 56.6% sought dermatologic or plastic surgery treatments, injecting USD 2.3 billion in direct spending into the South Korea aesthetic devices market. Chinese and ASEAN visitors, who generate 68% of inbound volume, often request devices they see in K-beauty social media, turning clinics into export-facing showrooms.[2]Hyun-Woo Lee, “K-Beauty Medical Tourism Drives Device Demand,” The Korea Herald, koreaherald.com Manufacturers now co-develop marketing kits with tourism agencies to align clinical evidence with lifestyle branding. The 2025 revision of the Medical Korea visa extends aesthetic stays to 90 days, which should keep the South Korea aesthetic devices market on a double-digit visitor growth path.[3]Ministry of Health and Welfare, “Medical Korea Visa Program Expansion,” Ministry of Health and Welfare, mohw.go.kr Still, 22% of foreign patients faced complications from unlicensed providers, highlighting accreditation gaps that could dampen future referrals.

Rapid Adoption of Minimally Invasive & Energy-Based Technologies

Energy-based modalities such as picosecond lasers and monopolar radiofrequency shorten recovery to 48 hours, displacing surgical lifts in urban clinics. Lutronic’s PicoPlus and Cynosure’s PicoSure dominated 2024 installations, underscoring clinician preference for pigment-selective platforms. MFDS fast-track review, introduced in 2025, now clears proven hybrid devices in 12 months, six months faster than before. Hironic’s Infini RF, which couples controlled depth with microneedling, shows how smaller firms exploit the pathway to win niche indications. These shifts funnel steady replacement demand into the South Korea aesthetic devices market, especially among clinics chasing premium procedure pricing.

Aging Population Drives Anti-Aging Demand

Adults 65+ will reach 20.6% of population by 2026, intensifying demand for radiofrequency tightening and collagen-stimulating fillers. The 50-65 group alone accounted for 31% of Botulinum toxin injections in 2025, a share that supports recurring revenue inside the South Korea aesthetic devices market. Products that promote gradual biostimulation, like Galderma’s Sculptra, grew 18% YoY in 2025. Preventive “prejuvenation” among 25-35 year-olds means two demand peaks, smoothing utilization curves for clinics. Over time, Korea’s low fertility rate could shrink future patient inflow, making inbound tourism more critical to sustain the South Korea aesthetic devices industry.

Growing Male Aesthetics Market Segment

Procedures for men are rising at 9.01% CAGR to 2031, with 34% of urban males viewing treatments as a career assets. Masseter reduction and abdominal contouring dominate, spurring Classys to launch a “Men’s Contour” protocol that bundles cryolipolysis with electromagnetic stimulation. Clinics price male sessions 15% higher, citing longer chair time and anesthetic needs, a premium that lifts average revenue per procedure in the South Korea aesthetic devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs of Advanced Devices | -0.8% | Nationwide, tier-2 clinics | Short term (≤ 2 years) |

| Stringent MFDS Approval Timelines & Compliance Costs | -0.6% | All manufacturers | Medium term (2-4 years) |

| Demographic Stagnation Limits Long-Term Domestic Growth | -0.5% | Rural provinces | Long term (≥ 4 years) |

| Proliferation of Counterfeit & Uncertified Devices | -0.4% | Online channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Advanced Devices

Thermage FLX and Ultherapy systems list above USD 150,000, while annual service contracts add 12-15% of purchase value. Hospital-backed groups absorb these costs, but many stand-alone clinics in Daejeon or Gwangju resort to refurbished units that extend ROI horizons. Only 18% of 2025 installations used third-party leasing, far below Japan’s 42%, reflecting conservative lending by Korean banks. Extended payback discourages clinics from early adoption, stretching the upgrade cycle in the South Korea aesthetic devices market.

Stringent MFDS Approval Timelines & Compliance Costs

Class III lasers need trials with 60 subjects and 12-month follow-up, adding up to USD 1 million per device. Annual safety reporting led to 14 recalls in 2025, mainly for RF units with inconsistent energy delivery. Smaller firms such as Wontech allocate 8.2% of revenue to regulatory affairs, double the share of global peers that spread costs worldwide. The mandatory ISO 13485:2016 certification from 2025 raises entry barriers, slowing innovation throughput in the South Korea aesthetic devices industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Non-Energy Injectables Outpace Energy Leaders

The non-energy devices segment accounts for 54.52% share within the South Korea aesthetic devices market, as Class II approval times have shortened by four months. Dermal fillers anchored by Hugel and Medytox now last 8-10 months, driving repeat traffic among 35-50-year-olds. Biodegradable threads gain favor with male patients seeking jawline refinement without surgery. Home-use microdermabrasion tools from Dr. Jart+ extend the care continuum, although margins remain lower than clinic-grade hardware.

The energy-based devices segment is anticipated to register the fastest CAGR of 8.56%, thanks to high-priced lasers and RF units that underpin clinic differentiation. Picosecond platforms own 38% of energy sales, and Jeisys’s Ultraformer series raises the bar with depth-customized HIFU. Average selling prices for IPL units dropped 12% in 2025 as Alma and Lumenis launched entry models targeting medical spas. Combination systems that fuse RF with ultrasound gained six MFDS clearances in 2025, signaling a hybrid future for the South Korea aesthetic devices market.

By Application: Body Contouring Redefines Growth Mix

Skin rejuvenation & tightening segment led with 32.51% share, yet body contouring & cellulite reduction is expanding at 9.12% CAGR through demand for cryolipolysis and electromagnetic muscle stimulation. Classys’s Clatuu Alpha shipped 28% more units in 2025, reflecting consumer appetite for non-surgical fat reduction. Diode lasers are overtaking alexandrite in hair removal, improving efficacy for darker skin. Scar and pigmentation care benefits from fractional lasers like Lutronic’s eCO2 Plus, which cuts overheating events by 34% through thermal imaging. Tattoo & vascular lesion removal grows 5.80% annually as picosecond systems break down resistant ink shades, widening clinical indications inside the South Korean aesthetic devices market.

By End User: Aesthetic & Dermatology Clinics Capture Momentum

The aesthetic & dermatology clinics segment held 54.07% share in 2025, with the fastest CAGR of 8.65% CAGR by bundling standardized packages at prices 20-25% below Seoul averages. Chains leverage bulk consumable purchases and cross-trained staff to reach 22% EBITDA, prompting manufacturers to craft volume-based deals. Hospitals retain reconstructive dominance yet concede elective ground to outpatient venues, while home-use devices capture the convenience-oriented segment that views aesthetics as daily self-care.

By Gender: Male Adoption Accelerates Revenue Diversity

The female segment generated 82.01% revenue, but the male segment drives incremental growth with a 8.79% CAGR. Masseter toxin injections and Clatuu-based abdominal sculpting top male demand, supported by employer wellness budgets in tech and finance. Hugel’s Botulax formulation with higher protein concentration shortens sessions on thicker male dermis, enhancing throughput for clinics in the South Korea aesthetic devices market.

By Age Group: Up to 34 Years Age Group Leads the Market

The up to 34 years segment accounted for the major share of 51.29% in the market, owing to strong beauty consciousness among younger consumers, widespread adoption of preventive aesthetic treatments, high influence of social media and K-beauty trends, and increasing demand for skin enhancement procedures such as laser treatments and acne scar reduction. On the other hand, the 35–50 years segment is anticipated to register the fastest CAGR of 8.73%, owing to rising demand for anti-aging treatments, greater spending capacity, increasing preference for non-invasive aesthetic procedures, and growing focus on maintaining a youthful appearance for professional and social purposes.

Geography Analysis

Seoul accounted for 62% of 2025 procedures, fueled by high-income households and the clinic density that makes Gangnam a proving ground for every new device launch. Busan emerges as a secondary hub as medical spas tap port-city professionals and Chinese tourists. Incheon leverages airport proximity, adding 19% more clinics since 2024 and absorbing short-stay visitors from Japan and Taiwan.

Tier-2 cities, Daegu, Gwangju, Daejeon, grow 7.1% CAGR, surpassing Seoul’s 5.8%, as private-equity chains exploit lower rents and limited competition. Yet only 34% of their clinics own picosecond lasers versus 68% in Seoul, underscoring capital constraints. Rural Jeolla and Gangwon face average travel times of 45 minutes to the nearest aesthetic facility, limiting penetration of the South Korea aesthetic devices market.

Government export programs matter: Korean manufacturers shipped USD 420 million of devices in 2024, and ISO 13485 alignment seeks mutual recognition with Japan and the EU to cut duplicate testing. China’s extra 2025 safety certifications raise compliance costs, so firms pivot to ASEAN markets to hedge geopolitical risk.

Competitive Landscape

The top suppliers include HUGEL, Inc., Medytox, Cynosure Lutronic, CLASSYS Inc., and AbbVie Inc. (Allergan Aesthetics), placing the South Korean aesthetic devices market in the moderately concentrated zone. Domestic firms dominate energy segments through vertical integration that blends component sourcing with in-house service, enabling faster 18-month upgrade cycles. Multinationals leverage regulatory moats and surgeon relationships to secure injectable contracts at major hospitals.

Innovation intensity is evident: Korean firms filed 142 device patents in 2024, up 23% YoY, with many aimed at real-time feedback systems. Lutronic’s 2025 impedance-based tissue monitoring patent helps clinicians avoid burns while maximizing collagen stimulation, reinforcing its premium positioning. Home-use disruptors such as LG Household & Health Care and AmorePacific exploit consumer electronics channels to reach the 25-35 demographic, expanding the competitive set beyond traditional med-tech.

Early movers in AI-guided treatment mapping may capture white-space by integrating facial analytics with filler viscosity databases. Manufacturers holding ISO 13485:2016 certificates can release new models six to nine months faster than entrants, a speed edge that could widen share over the forecast period.

South Korea Aesthetic Devices Industry Leaders

HUGEL, Inc.

Medytox

Cynosure Lutronic

CLASSYS Inc.

AbbVie Inc. (Allergan Aesthetics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: HUGEL, Inc. launched CellREDM, an injectable treatment based on human acellular dermal matrix (hADM). Designed to promote skin regeneration by replenishing key extracellular matrix components like collagen and elastin, the new product aims to enhance Hugel’s portfolio beyond traditional wrinkle and volume treatments, offering more comprehensive skin rejuvenation solutions.

- March 2026: Medytox launched Nuviju, a new fat reduction injection targeting submental fat. Nuviju is Korea's first domestically developed fat reduction injection utilizing cholic acid as its main ingredient and has been approved as the 40th locally developed new drug by the Ministry of Food and Drug Safety. The treatment is intended for individuals with a moderate-to-severe double chin.

- September 2025: Sciton, Inc., launched HALO TRIBRID, the first 3-in-1 customizable resurfacing laser. The new system combines the company’s flagship technologies, HALO, MOXI, and Erbium Resurfacing, into a single platform, enabling enhanced flexibility and efficiency for practitioners. Built on decades of innovation, the device is designed to deliver improved treatment outcomes while streamlining clinical workflows.

South Korea Aesthetic Devices Market Report Scope

As per the scope of the report, Aesthetic devices are tools used for non-surgical or minimally invasive cosmetic procedures to improve appearance through technologies like lasers, radiofrequency, ultrasound, and light.

The South Korea Aesthetic Devices Market Report is segmented by Device Type, Application, End User, Gender, Age Group, and Geography. By Device Type, the market is segmented into Energy-based Devices (Laser-based, Radiofrequency, IPL & Light-based, Ultrasound/HIFU) and Non‑energy Devices (Dermal Fillers & Injectables, Implants, Microdermabrasion & Dermarollers). By Application, the market is segmented into Skin Rejuvenation & Tightening, Body Contouring & Cellulite Reduction, Hair Removal, Scar/Acne/Pigmentation Treatment, Tattoo & Vascular Lesion Removal, and Others. By End User, the market is segmented into Hospitals, Aesthetic & Dermatology Clinics, Medical Spas, and Home‑Use/Consumer. By Gender, the market is segmented into Female and Male. By Age Group, the market is segmented into 18–34 Years, 35–50 Years, and Above 50 Years. Market Forecasts are Provided in Terms of Value (USD).

By Device Type

| Energy-based Devices | Laser-based |

| Radiofrequency | |

| IPL & Light-based | |

| Ultrasound / HIFU | |

| Non-energy Devices | Dermal Fillers & Injectables |

| Implants | |

| Microdermabrasion & Dermarollers |

By Application

| Skin Rejuvenation & Tightening |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Scar, Acne & Pigmentation Treatment |

| Tattoo & Vascular Lesion Removal |

| Others |

By End User

| Hospitals |

| Aesthetic & Dermatology Clinics |

| Medical Spas |

| Home-Use / Consumer |

By Gender

| Female |

| Male |

By Age Group

| 18–34 Years |

| 35–50 Years |

| Above 50 Years |

| By Device Type | Energy-based Devices | Laser-based |

| Radiofrequency | ||

| IPL & Light-based | ||

| Ultrasound / HIFU | ||

| Non-energy Devices | Dermal Fillers & Injectables | |

| Implants | ||

| Microdermabrasion & Dermarollers | ||

| By Application | Skin Rejuvenation & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Scar, Acne & Pigmentation Treatment | ||

| Tattoo & Vascular Lesion Removal | ||

| Others | ||

| By End User | Hospitals | |

| Aesthetic & Dermatology Clinics | ||

| Medical Spas | ||

| Home-Use / Consumer | ||

| By Gender | Female | |

| Male | ||

| By Age Group | 18–34 Years | |

| 35–50 Years | ||

| Above 50 Years | ||

Key Questions Answered in the Report

What is the current value of the South Korea aesthetic devices market?

The market is valued at USD 567.75 million in 2026 and is set to reach USD 838.63 million by 2031.

Which device type is growing fastest in South Korea?

Energy-based devices segment is expected to grow at 8.56% CAGR owing to rising demand for minimally invasive procedures, increasing adoption of laser and radiofrequency technologies, growing preference for skin rejuvenation treatments, and continuous technological advancements enhancing treatment efficacy and safety.

Why is body contouring in high demand?

Consumer preference for non-surgical fat reduction via cryolipolysis and muscle-toning electromagnetic systems pushes body contouring growth at 9.12% CAGR.

How significant is male participation in aesthetic procedures?

Male segment is anticipated to growth at fastest CAGR 8.79% CAGR and accounting for a growing share of clinic revenues.

What regulatory factors shape device launches?

MFDS fast-track review shortens approval to 12 months for hybrid devices, but Class III lasers still face costly trials and strict post-market surveillance.

Which cities outside Seoul show strong growth potential?

Busan, Incheon, Daegu, and Gwangju grow faster than the capital thanks to clinic-chain expansion and lower real-estate costs.

Page last updated on: