Malaysia Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

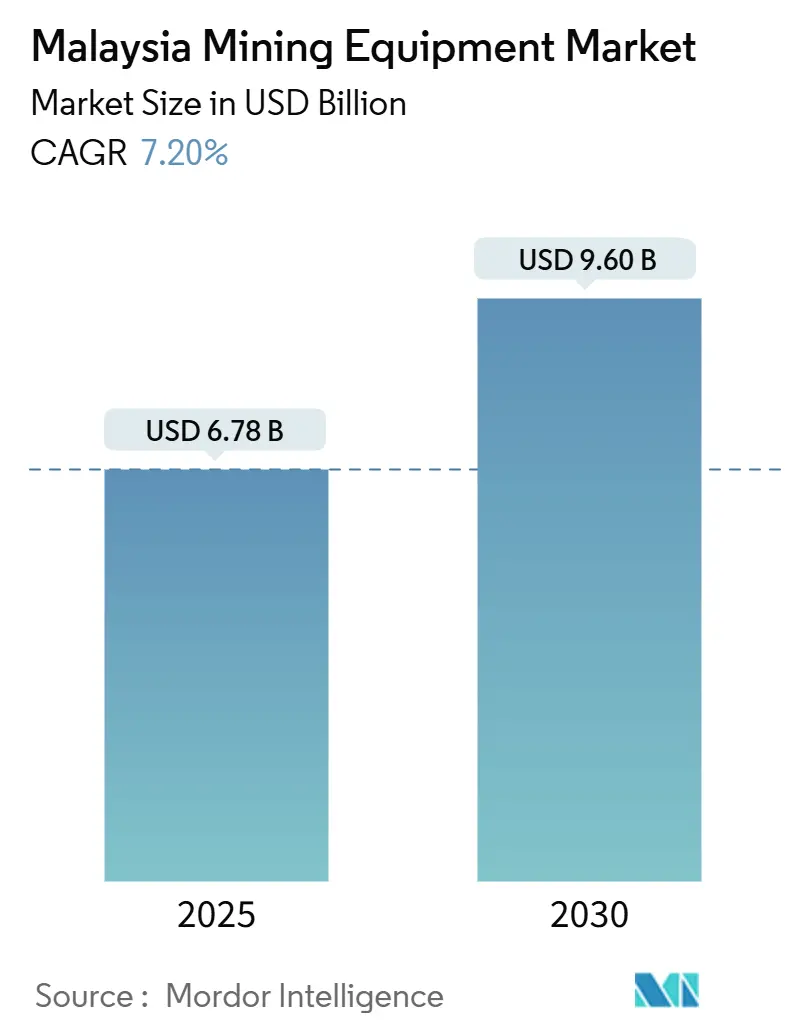

| Market Size (2025) | USD 6.78 Billion |

| Market Size (2030) | USD 9.60 Billion |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Mining Equipment Market Analysis by Mordor Intelligence

The Malaysia mining equipment market was valued at USD 6.78 billion in 2025 and is projected to reach USD 9.60 billion by 2030, growing at a robust 7.20% CAGR during the forecast period. This growth is fueled by the rising demand for critical minerals required for electric-vehicle supply chains. Additionally, Petronas' substantial investments in brownfield projects and increasing automation expenditures have driven this expansion.

The demand for specialized offshore drilling units is supported by deepwater oil-and-gas extensions, while record-high gold prices of USD 3,036.74 per troy ounce have driven interest in precious-metal processing lines.

Malaysia's construction machinery sector currently fulfills less than 20% of domestic demand, underscoring a significant reliance on imports. This dependency creates opportunities for global brands to establish local assembly or sourcing operations, reducing lead times. Furthermore, stricter environmental regulations, exemplified by the bauxite moratorium, are encouraging operators to invest in dust-suppression, water-treatment, and real-time monitoring attachments to meet updated permitting requirements.

Key Report Takeaways

- By equipment type, surface mining equipment accounts for 47.20% of the Malaysia mining equipment market share in 2024, whereas the loaders and haul trucks are projected to grow at a CAGR of 19.20% through 2030.

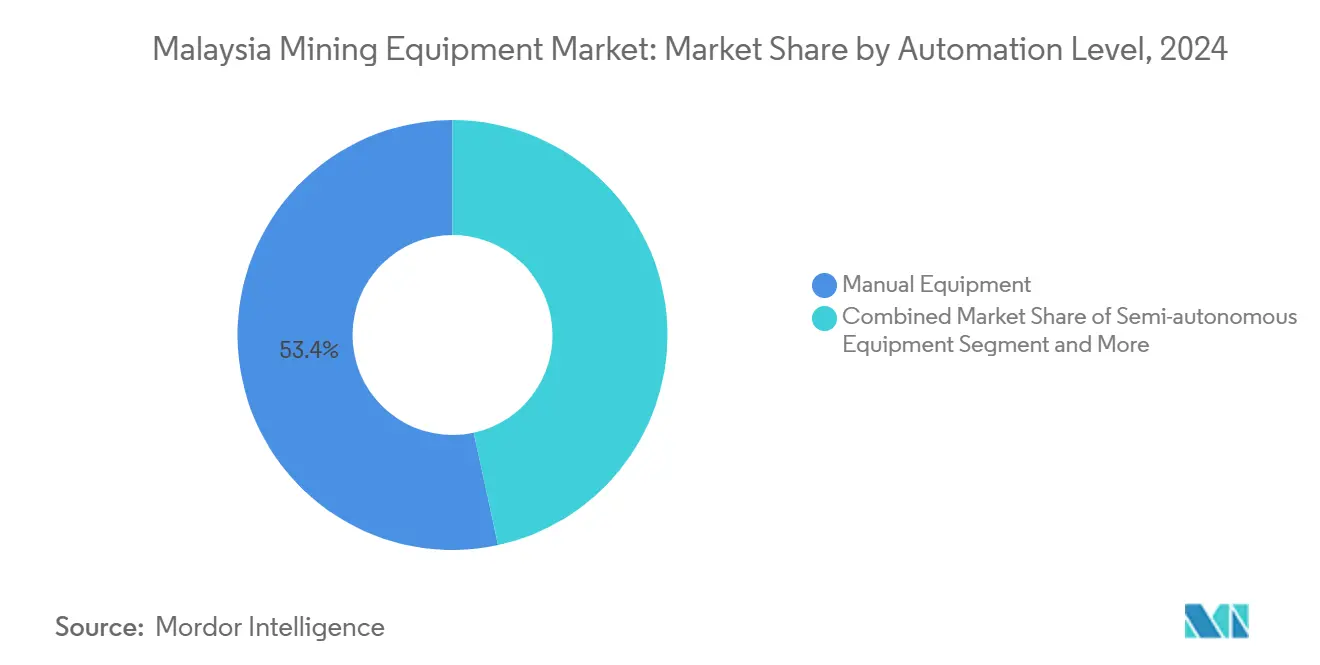

- By automation type, the manual equipment holds around 53.40% of the Malaysia mining equipment market share in 2024, whereas the fully autonomous equipment is expected to grow at a CAGR of 18.30% during the forecast period.

- By powertrain type, the internal combustion engine (ICE) vehicles led with 76.50% of the Malaysia mining equipment market share in 2024, even though the battery electric vehicles are forecast to surge at a CAGR of 19.50% by 2030.

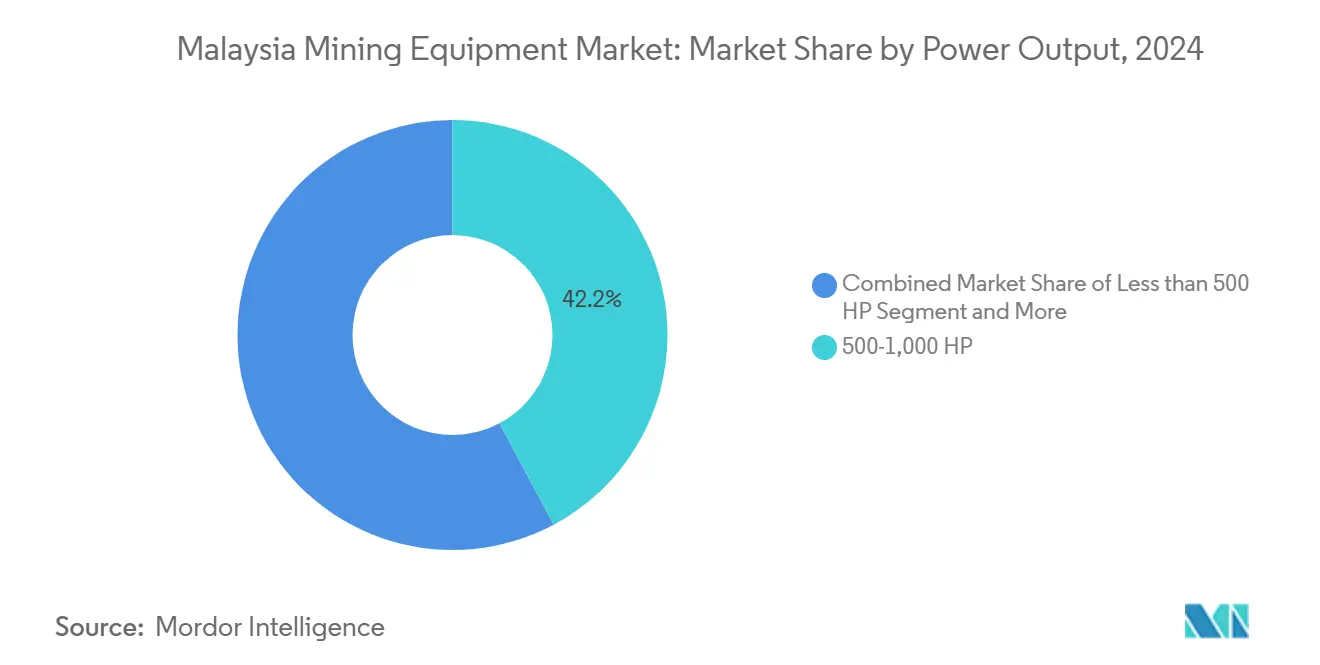

- By power output, the 500-1,000 HP held 42.20% of the Malaysia mining equipment market share in 2024, whereas>1,000 HP is projected to grow at a CAGR of 15.20% during 2025-2030.

- By application, metal mining accounts 53.20% of the Malaysia mining equipment market share in 2024, however rare earth mining is expected to grow at a CAGR of 20.60% during the forecast period.

- By geography, Peninsular Malaysia is the largest region, accounting for 72.23% of 2024 revenue while East Malaysia (Sabah–Sarawak–Labuan) is the fastest-growing at 9.12% CAGR during the forecast period.

Malaysia Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical Minerals Demand for EV Supply Chain | +2.1% | National, with concentration in Terengganu, Kelantan, Pahang | Medium term (2-4 years) |

| Smart Mining & Automation Adoption | +1.8% | National, with early adoption in Peninsular Malaysia | Long term (≥ 4 years) |

| Government CAPEX in Oil & Gas | +1.5% | National, with focus on offshore Sarawak and Sabah | Short term (≤ 2 years) |

| Phytomining for Nickel Extraction | +0.9% | Sabah, with potential expansion to Peninsular Malaysia | Long term (≥ 4 years) |

| Growth in Bauxite & Ilmenite Mining | +0.7% | Johor, Pahang, with spillover to Terengganu | Medium term (2-4 years) |

| Tax Incentives for Local Machinery | +0.6% | National, with manufacturing hubs in Selangor, Johor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Critical Minerals for EV Supply Chain

Kelantan's rare earth reserves, valued at RM 125 billion (USD 29.3 billion), have spurred a surge in orders for specialized plants focused on crushing, screening, and solvent extraction. Lynas Rare Earths, with its proven capability to supply dysprosium oxide outside of China, has set processing benchmarks. These benchmarks are now being adopted by other miners, who are implementing stricter impurity controls and closed-loop water systems.

Recent enforcement actions against illegal operations, resulting in 55 arrests in Kelantan and Selangor, have tightened the grip on the informal sector. This crackdown has redirected investments towards compliant machinery, specifically designed for regulated sites. Equipment vendors are now prioritizing low-noise drills, enclosed cab dozers, and data-logging tools. These innovations assist operators in meeting audit requirements set by the Minerals and Geoscience Department. Given the heavy reliance of EV batteries on dysprosium and terbium, the demand for rare-earth refiners suggests robust growth prospects extending well beyond 2030.

Accelerating Adoption of Smart-Mining & Automation Solutions

Komatsu's WX04B LHD, a battery-electric model with rapid-swap packs, does away with idle-time charging, boosting underground utilization rates. Meanwhile, Caterpillar's Precision Mining suite, by integrating IMA Engineering's ore-sensor heads on conveyors, achieves real-time grade control, leading to an average waste reduction of 8% across pilot sites.

In Malaysia, miners combining semi-autonomous haulage with augmented-reality operator stations are witnessing productivity gains in the double digits and a decline in accident rates. Yet, a mere 23% of mines have personnel certified in autonomous systems. This is surprising given that Technical and Vocational Education and Training institutes boast a 99% graduate employability rate. Clearly, workforce skilling is the pivotal challenge influencing the pace of automation adoption in the coming three years.

Government CAPEX in Oil & Gas Brown-field Extensions

Petronas is set to develop 69 wells in 2025 and implement 367 annual Facilities Improvement Plans, boosting the demand for tool joints, mud-pumps, and subsea trees until 2027. Opting for brownfield reuse slashes capital costs by 25-30% compared to greenfield standards, driving the demand for retrofit kits like rig leg extensions, low-emission diesel generators, and real-time reservoir imaging modules.

In offshore Sarawak's deepwater blocks, 3,000-meter rated drillships and dynamically positioned support vessels are essential to navigate the high-current conditions. To align with Malaysia’s net-zero goals, tender lists now prominently feature carbon-capture skid packages and upgrades for high-efficiency gas-turbine drivers.

Phytomining Pilots for Low-Impact Nickel Extraction

Field trials in Sabah have validated the commercial prospects of Phyllanthus rufuschaneyi, with sap nickel concentrations reaching as high as 16.9 wt%. Phytomining, unlike traditional open-pit methods, relies on tractor-mounted harvesters, biomass dryers, and hydrometallurgical leach digesters, steering clear of large excavators.

Equipment manufacturers are developing dual-purpose agricultural graders equipped with sensor arrays to enhance plant density and sap yield. This model not only facilitates the reclamation of degraded lands but also provides revenue streams through community co-cultivation, in line with Malaysia’s National Energy Transition Roadmap. If adopted on a national scale, phytomining could shift investments from high-HP haul trucks to machinery specifically designed for hyper-accumulator crops.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Environmental Permitting & Bauxite Bans | -1.2% | National, with acute impact in Pahang, Johor | Short term (≤ 2 years) |

| Commodity Price Volatility | -0.8% | National, with sector-specific variations | Medium term (2-4 years) |

| Skills Gap in Autonomous Equipment | -0.6% | National, with concentration in Peninsular Malaysia | Medium term (2-4 years) |

| Shortage of High-Capacity BEV Batteries | -0.4% | National, with supply chain dependencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tougher Environmental Permitting & Bauxite Moratoriums

Operators, facing a bauxite ban from 2016 to 2019, had to adopt measures like sedimentation ponds, sealed truck beds, and GPS fleet monitors to continue shipments[1]“Gov’t to Impose Export Ban on Bauxite Ore June Next Year,” Cabinet Secretariat of the Republic of Indonesia, setkab.go.id . Now, a regulatory baseline has been established, featuring monthly export quotas set at 600,000 tons and a 1 km buffer zone from residential areas. Bukit Goh bauxite, with a moisture content of 20.64%, exceeding the maritime limit of 10%, necessitates the use of extra dewatering screens and covered stockyards. This requirement amplifies capital intensity, posing challenges for new entrants. Furthermore, enforcement raids, coupled with obligatory Environmental Impact Assessments, not only inflate compliance costs but also prolong decision-making cycles, deterring smaller license applicants.

Commodity-Price Volatility Limiting Cap-ex Cycles

In March 2025, a surge in gold prices bolstered margins for precious-metal mines. However, this uptick also led to heightened expenses in reagents and insurance, causing a more cautious approach to fleet expansion in other areas. Operators in tin, copper, and iron ore are holding off on major purchases during price dips, resulting in inconsistent order flows for OEMs.

With 80% of heavy machinery being imported, fluctuations in currency values against the U.S. dollar can lead to significant increases in landed costs, further delaying procurement decisions. The resumption of bauxite exports from Indonesia poses a threat to Malaysian export volumes. This situation leaves local miners vulnerable to sudden shifts in revenue, dampening their confidence in capital expenditures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Mining Retains Lead in Shallow-Deposit Extraction

Surface systems accounted for 47.20% of the Malaysian mining equipment market in 2024. This dominance was primarily driven by Johor's bauxite and Terengganu's rare-earth pits, which rely on bulldozers, hydraulic excavators, and 90-tonne haul trucks designed for shallow overburden.

Loaders and haul trucks recorded the highest growth, with a notable 19.20% CAGR during the forecast period, as the adoption of autonomous haulage retrofits expanded. Underground rigs experienced steady growth, supported by renewed shaft investments in Perak's deeper tin reefs. Processing equipment, including crushers, separators, and flotation cells, gained importance as export clients demanded higher concentrate grades to reduce downstream carbon footprints.

Medium-scale mines increasingly utilize mobile in-pit crushers integrated with online particle-size cameras. These systems help reduce haulage distances and diesel consumption. Such hybrid solutions achieve both efficiency and emissions goals, highlighting Malaysia's shift from focusing on pure tonnage to prioritizing value-dense metallurgy.

By Automation Level: Manual Dominance Faces Gradual Erosion

Manual equipment continues to dominate Malaysia's mining equipment market, accounting for 53.40% of the market share in 2024. This is primarily due to the prevalence of small, family-operated leases that focus on minimizing upfront costs. Semi-autonomous retrofits, such as camera-assisted dozing and operator-alert systems, are gaining traction among mid-tier firms.

Fully autonomous fleets, growing at a robust 18.30% CAGR during the forecast period (2025-2030), are primarily deployed in major rare-earth and iron ore hubs, where labor shortages and strict safety regulations drive investments. Original Equipment Manufacturers (OEMs) are now offering remote operations centers bundled with 4G/LTE private networks, allowing buyers to achieve incremental autonomy without replacing their entire fleet.

Nonetheless, a persistent skills shortage remains a significant obstacle. Nationwide, only 12 accredited centers offer advanced robotics certifications, and travel restrictions further hinder hands-on training provided by OEMs. To address these skill gaps and accelerate fleet modernization, government-sponsored subsidies under the New Industrial Master Plan 2030 are essential.

By Powertrain Type: Electric Entries Challenge ICE Supremacy

ICE platforms dominated Malaysia's mining equipment market, capturing a substantial 76.50% share in 2024. Their success is attributed to well-established diesel logistics, a comprehensive spare-parts network, and the ability to deliver robust torque even in humid conditions. Meanwhile, battery-electric units are witnessing a remarkable 19.50% CAGR during the forecast period, driven by innovations like modular pack designs and supportive policy incentives, including import-duty relief for zero-emission machinery.

Komatsu's WX04B, equipped with 55 kWh interchangeable batteries, has emerged as a top choice for narrow-vein operations, comfortably powering an eight-hour shift. However, the charging infrastructure remains in its infancy outside major concessions. This limitation has led some operators to pivot towards hybrid-diesel systems, which not only extend operational range but also reduce emissions.

Financial institutions are increasingly tying lending rates to ESG performance metrics, subtly pushing adopters towards greener, low-carbon fleets. Additionally, as grid-connected solar-plus-storage systems begin to emerge close to mine gates, the power generated on-site is poised to further bolster the shift towards electric machinery.

By Power Output: Mid-Range Machines Anchor Core Operations

The 500-1,000 HP class dominated Malaysia's mining equipment market, capturing 42.20% share in 2024. This range strikes a cost-to-payload balance, ideal for mid-depth bauxite and tin seams. Meanwhile, machines boasting over 1,000 HP are witnessing a surge, growing at a 15.20% CAGR during the forecast period. This uptick underscores the importance of scale economies as critical-mineral mines boost their output.

On the other hand, the sub-500 HP segment remains vital for exploration and selective ore-cutting, prioritizing maneuverability over sheer tonnage. Additionally, with regulatory concerns spotlighting dust and vibration, there's a marked preference for mid-power excavators. These machines not only deliver sufficient breakout force but also adhere to stringent noise standards.

By Application: Metal Mining and Rare Earths Drive Order Books

Metal mines held a dominant 53.20% share of Malaysia's mining equipment market in 2024, driving consistent demand for drill rigs, mineral jigs, and smelting feeders. While ore grades may be declining, Malaysia's rich tin heritage and emerging copper prospects in Sabah ensure a steady baseline volume.

Rare-earth extraction is on the rise, boasting a robust 20.60% CAGR during the forecast period. This surge is fueling investments in high-intensity magnetic separators and solvent-extraction mixer-settlers, both crucial for the recovery of dysprosium and terbium.

While coal continues to be mined for industrial boilers, its application has become more niche. Suppliers are increasingly pivoting towards advanced markets, where technological innovation and profit margins are significantly higher.

Geography Analysis

Peninsular Malaysia is the largest market, contributing 72.23% of 2024 revenue. Dense installed base across tin/bauxite/rare-earth sites plus proximity to ports, highways, and OEM/dealer hubs enables faster service and higher replacement cycles, keeping revenue share highest.

East Malaysia (Sabah–Sarawak–Labuan) is the fastest-growing, at 9.12% CAGR during the forecast period. Sarawak deepwater O&G CAPEX and Sabah’s emerging rare-earth/nickel projects—supported by Labuan FTZ logistics—are driving outsized new equipment orders and the quickest CAGR. Offshore deepwater projects in Sarawak are on the lookout for advanced blowout preventers and remotely operated vehicle fleets to align with Petronas' ambitious production targets[2]“Malaysia’s Petronas Aims to Boost Oil and Gas Output over Next Three Years.” Reuters, www.reuters.com. Meanwhile, Sabah's phytomining initiatives are turning to tractor-pulled harvesters and mobile bio-ore kilns, highlighting a unique demand trajectory. The Federal Territory of Labuan, with its free-trade facilities slashing import duties on heavy units, is becoming a magnet for OEMs. These companies are establishing bonded warehouses, significantly reducing lead times for crucial subsea parts.

Inland, the Twelfth Malaysia Plan's logging-road upgrades are unlocking copper and gold prospects that once faced access challenges. To bridge service gaps and maintain fleet uptimes above 90%, equipment dealers are deploying modular workshop containers, conveniently helicopter-lifted into remote concessions.

Competitive Landscape

While global giants dominate the headlines, local assemblers and niche suppliers are reshaping the landscape. In August 2024, Komatsu's acquisition of UMW Komatsu Heavy Equipment transformed the latter into a wholly owned subsidiary. This move accelerates part-number localization and integrates offerings with Komatsu's Smart Construction telematics.

Caterpillar, on the other hand, is harnessing Sime Darby Industrial's expansive network to roll out the Cat MineStar platform. This platform seamlessly merges fleet dispatch, terrain tracking, and health analytics, all aimed at bolstering integrated uptime contracts.

Meanwhile, Liebherr's landmark USD 2.8 billion zero-emission agreement with Fortescue has set a precedent, one that Malaysian miners are keenly observing as they chart their 2030 ESG strategies.

Despite a heavy reliance on imports, regional OEMs from China and South Korea are seizing the opportunity. They offer lower-spec units at a tempting 10-15% discount. However, concerns linger over warranty coverage and parts availability. The tightening grip of environmental regulations has birthed a new competitive arena.

Suppliers are now aggressively promoting Stage V equivalent diesel engines, dust-suppression cannons, and closed-loop cooling systems, all in a bid to expedite permit approvals. Service innovation is another critical differentiator. Epiroc's establishment of a remote troubleshooting hub in Kuala Lumpur has slashed mean-time-to-repair by an impressive 28%, making it a coveted advantage for clients with high utilization. As phytomining gains traction, it could lure agri-machinery titans like Kubota into unexpected cross-sector partnerships, further intensifying the competitive landscape.

Malaysia Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr Group

Hitachi Construction Machinery Co., Ltd.

Sandvik AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Petronas aims to hit a production target of 2 million barrels of oil equivalent daily by 2027. As part of this strategy, the company will drill 69 new development wells in 2025 to boost output. Furthermore, Petronas is set to lead around 367 innovative Facilities Improvement Plans annually, emphasizing operational efficiency and infrastructure enhancement.

- October 2024: Liebherr and Fortescue have announced a significant partnership valued at USD 2.8 billion. This collaboration aims to transform the mining sector by deploying 475 advanced autonomous machines powered entirely by battery-electric technology. The alliance represents a major step toward sustainability and innovation, with cutting-edge machinery contributing to a cleaner and more efficient mining industry.

- August 2024: Komatsu finalized the acquisition of the remaining shares in UMW Komatsu Heavy Equipment, establishing it as a wholly owned subsidiary. This strategic move strengthens Komatsu's position in the heavy equipment market and represents a crucial step toward achieving greater operational control and synergy within the industry.

- May 2024: Sandvik opened a new load and haul factory in Malaysia. The inaugural assembly at the factory featured Sandvik's Toro™ LH517i loader, with production set to increase in the upcoming year. Additionally, the facility plans to start producing Toro™ TH545i trucks later this year, aligning with a broader cross-manufacturing strategy.

Malaysia Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Loaders & Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Rare Earth Mining |

| Peninsular Malaysia | Perak |

| Pahang | |

| Terengganu | |

| Johor | |

| Selangor | |

| East Malaysia | Sabah |

| Sarawak | |

| Federal Territory of Labuan |

| By Equipment Type | Surface Mining Equipment | |

| Underground Mining Equipment | ||

| Mineral Processing Equipment | ||

| Drills & Breakers | ||

| Crushing, Pulverizing & Screening | ||

| Loaders & Haul Trucks | ||

| By Automation Level | Manual Equipment | |

| Semi-Autonomous Equipment | ||

| Fully Autonomous Equipment | ||

| By Powertrain Type | Internal-Combustion Engine Vehicles | |

| Battery-Electric Vehicles | ||

| Hybrid Vehicles | ||

| By Power Output | Less than 500 HP | |

| 500 - 1,000 HP | ||

| Above 1,000 HP | ||

| By Application | Metal Mining | |

| Mineral Mining | ||

| Coal Mining | ||

| Rare Earth Mining | ||

| By Geography | Peninsular Malaysia | Perak |

| Pahang | ||

| Terengganu | ||

| Johor | ||

| Selangor | ||

| East Malaysia | Sabah | |

| Sarawak | ||

| Federal Territory of Labuan | ||

Key Questions Answered in the Report

What is the forecast value of Malaysia’s mining-equipment demand by 2030?

The Malaysia mining equipment market is projected to reach USD 9.60 billion by 2030.

Which equipment power range sells the most units locally?

Machines in the 500-1,000 HP class held 42.20% share in 2024, reflecting medium-scale mine requirements.

How fast are battery-electric mining vehicles growing?

Battery-electric models are expanding at a 19.50% CAGR during 2025-2030.

Why does automation adoption vary across Malaysian mines?

Skill shortages and capital constraints slow uptake among small operators, while large mines deploy autonomous fleets for productivity and safety gains.

Page last updated on: