Germany Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

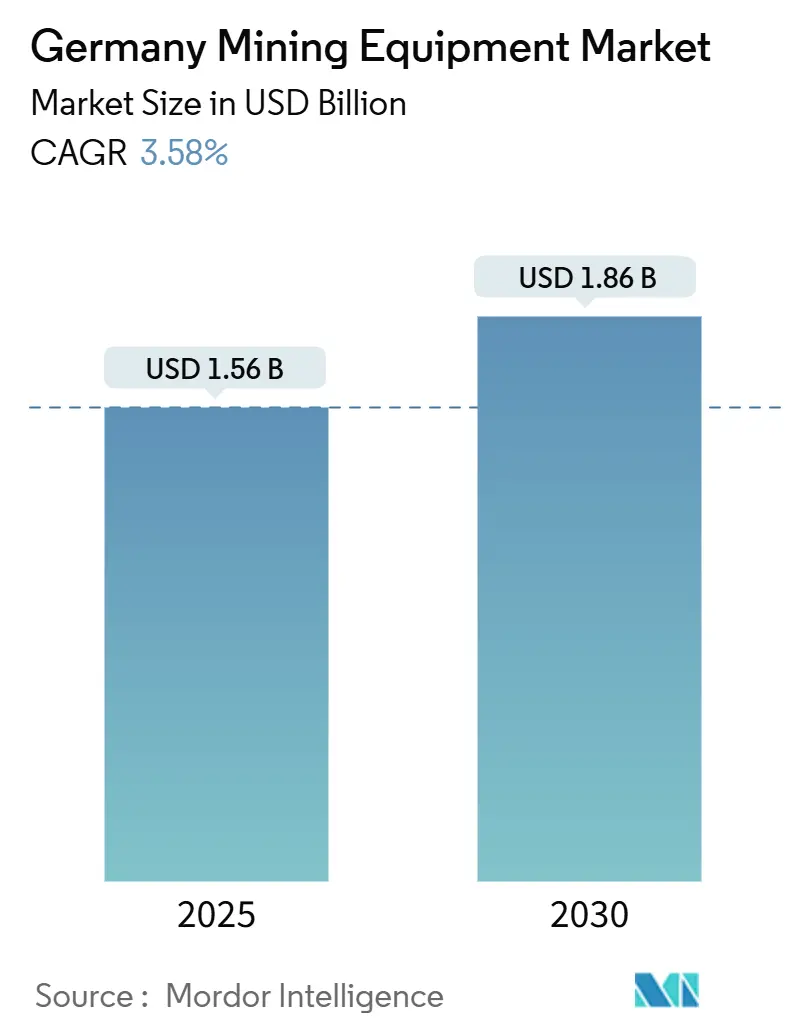

| Market Size (2025) | USD 1.56 Billion |

| Market Size (2030) | USD 1.86 Billion |

| Growth Rate (2025 - 2030) | 3.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Mining Equipment Market Analysis by Mordor Intelligence

The Germany mining equipment market size stands at USD 1.56 billion in 2025 and is forecast to climb to USD 1.86 billion by 2030, reflecting a 3.58% CAGR during 2025-2030. This steady trajectory stems from structural moves away from coal toward critical minerals and geothermal resources, backed by the federal coal-phase-out law and the EU Critical Raw Materials Act. Surface operations still dominate spending, yet underground projects—especially lithium, salt cavern and potash developments—pull in new orders for specialized loaders, jumbos and retrofit drilling systems. Concurrently, the labor squeeze is accelerating automation, while federal R&D grants and strict EU emission limits spur electrification and digital fleet-management upgrades across the Germany mining equipment market. Competitive intensity remains moderate: large incumbent OEMs chase zero-emission mega-orders, niche German specialists safeguard high-tech tunneling and shaft-boring niches, and a wave of refurbished Eastern-European machines adds price pressure—forcing differentiation through autonomy, service contracts, and lifecycle efficiency guarantees.

Key Report Takeaways

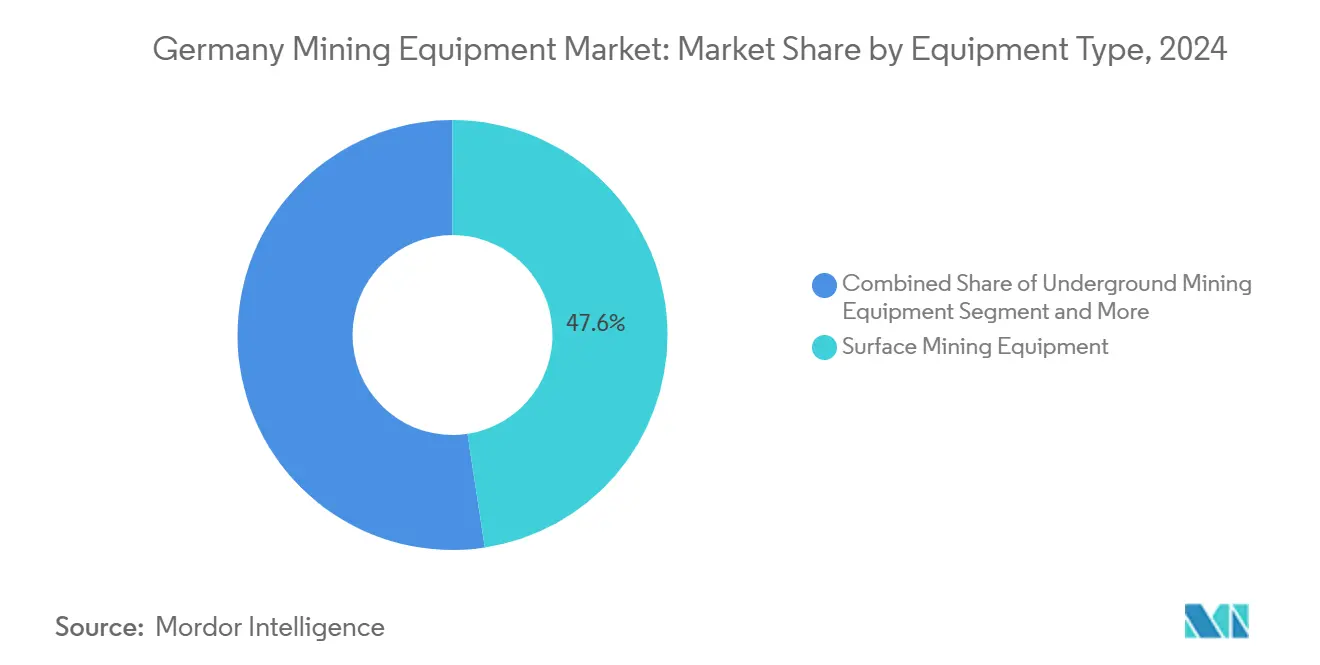

- By equipment type, surface mining equipment captured 47.55% of Germany mining equipment market share in 2024; underground mining equipment is set to expand at a 4.35% CAGR to 2030.

- By automation level, manual equipment held 65.33% of the Germany mining equipment market size in 2024, while fully autonomous fleets are projected to surge at a 20.15% CAGR through 2030.

- By powertrain, internal-combustion models accounted for 86.24% of the Germany mining equipment market size in 2024, yet battery-electric units will grow at a 6.57% CAGR to 2030.

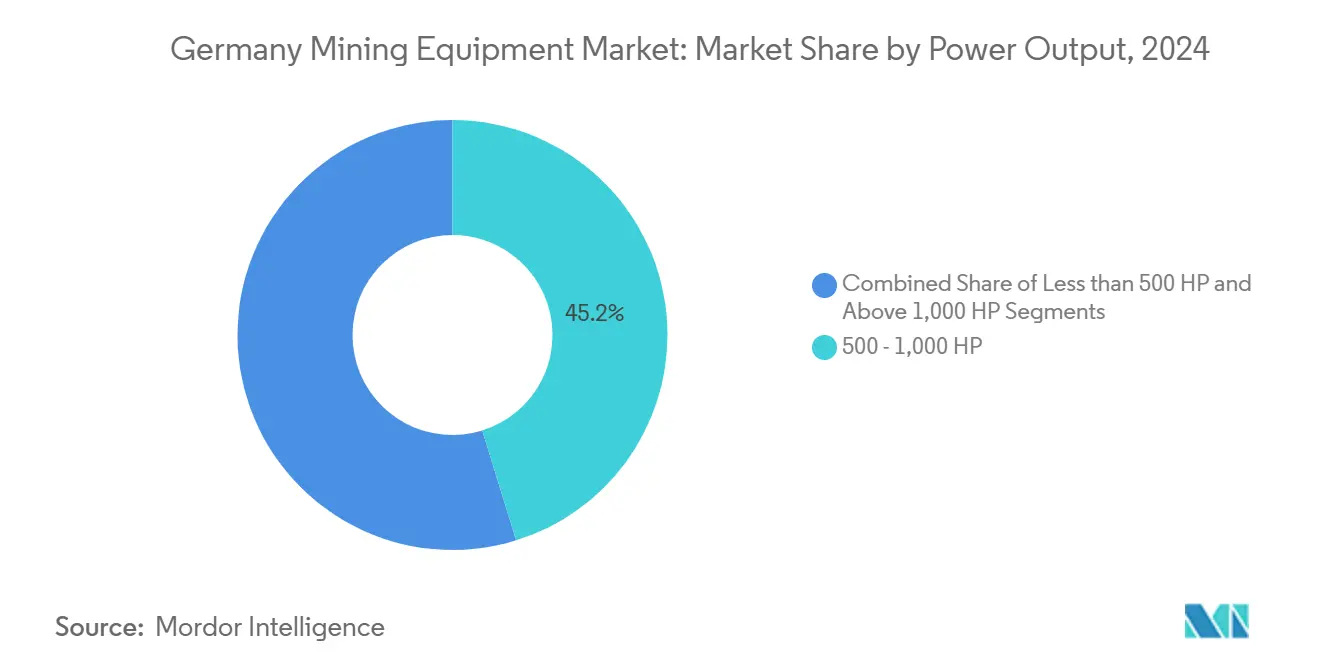

- By power output, the 500-1,000 HP bracket led with 45.18% share of the Germany mining equipment market size in 2024; machines above 1,000 HP register the highest 5.43% CAGR outlook.

- By application, metal mining commanded a 54.35% share of the Germany mining equipment market size in 2024, while mineral mining is advancing at a 4.92% CAGR toward 2030.

Germany Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-Mineral Demand for EU Battery Chain | +0.8% | Saxony, Brandenburg, Bavaria; spillover across EU | Medium term (2-4 years) |

| Automation and Digitalization | +0.7% | National mining districts | Long term (≥ 4 years) |

| Lignite and Hard-Coal Mine Modernization | +0.6% | Lusatia, Rhenish coalfield | Short term (≤ 2 years) |

| Federal R&D for Battery-Electric Equipment | +0.4% | Nationwide | Medium term (2-4 years) |

| Underground Salt and Potash for H₂ Storage | +0.3% | North German Basin, Lower Saxony | Long term (≥ 4 years) |

| Geothermal Shaft Repurposing | +0.2% | Bavaria, Upper Rhine Valley | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Critical Minerals for EU Battery Supply Chain

The Germany mining equipment market is benefiting from the EU mandate to source at least 10% of strategic raw materials domestically by 2030, heightening urgency around lithium, rare-earth, and copper extraction [1]European Central Bank, “Securing critical raw materials in Europe,” ecb.europa.eu. Zinnwald Lithium’s Saxony project, slated to yield 18,000 t of lithium hydroxide annually with lifetime cash flows of EUR 12.1 billion, requires large-diameter drill rigs, continuous miners, and on-site processing lines. KfW data shows 30% of German manufacturing value-added relies on copper, and one-third of lithium imports remain at risk, intensifying domestic equipment orders. Rare-earth demand hit 6,000 t in 2023, fully imported from China, spurring exploratory contracts for German OEMs on sensor-based sorting and selective leaching units. The EUR 1 billion federal Raw Materials Fund, active since October 2024, offers EUR 50-150 million co-financing per mining venture, underwriting capex for advanced haulage, ventilation, and beneficiation systems.

Automation and Digitalization to Mitigate Skilled-Labor Crunch

Germany recorded 1.24 million skilled unemployed versus 1.15 million open roles in 2025, highlighting structural gaps that automation must bridge. Mining, therefore, allocates rising capex to LiDAR-guided drills, collision-avoidance loaders, and AI-enabled fleet-management software. Epiroc’s Q1 2025 bookings grew 17% to MSEK 16,586, buoyed by a MAUD 350 contract for fully autonomous blasthole rigs in Saxony. Herrenknecht’s tunnel-boring line now embeds 400+ automated functions, lowering cycle times by up to 30% and cutting crew sizes in potash and geothermal projects [2]Herrenknecht AG, “Automation Features in Modern TBMs,” herrenknecht.com. Academic studies suggest the near-term sweet spot is “collaborative autonomy,” where machines perform repetitive cycles while remote operators intervene on exceptions—balancing safety, regulation, and productivity.

Modernization of Lignite and Hard-Coal Mines for Emissions Compliance

Methane from lignite pits may be 184 times higher than official inventories, forcing operators to adopt real-time monitoring sensors, high-capacity flaring units, and autonomous dozers to speed remediation. The Coal Phase-Out Act cuts coal generation to 17 GW by 2030, triggering shutdown equipment demand—draglines, stacker-reclaimers, slurry pumps—for decommissioning while installing methane capture skids and reed-bed water-treatment modules. Lusatia’s projected 20% population drop by 2038 magnifies the need for autonomous shovels and remote-operated drill jumbos that reduce headcount, a dynamic already visible at the Cottbus pit lake heat-pump retrofit requiring specialized pipe-laying rigs to support a 35 MW thermal plant. Environmental remediation mandates expand orders for amphibious excavators, sediment dredgers, and in-situ biosparging systems, as evidenced by the Hausham colliery rehab program that relies on continuous geochemical monitoring arrays.

Federal R&D Incentives for Battery-Electric Mining Equipment

The 2025 federal budget allocates EUR 176 million to high-tech start-ups plus dedicated BMBF battery programs aimed at European cell sovereignty, boosting prototype orders for stator-cooled electric motors and 1-MW fast-charging skids. The KMU-innovative scheme simplifies grant paperwork for SMEs building power electronics and autonomous driving modules adaptable to mining haulers. BAFA’s energy-efficiency fund reimburses up to 50% of purchase costs for high-efficiency drivetrain upgrades, a lever for mid-size German quarries to replace Tier-3 engines with electric-ready platforms. Steel producer ArcelorMittal secured EUR 1.27 billion for electric-arc furnace rollout, illustrating political will to underwrite industrial electrification that cascades to mine-site vehicle demand.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU Emissions & Noise Rules | -0.5% | All German mine sites | Short term (≤ 2 years) |

| Commodity Price Volatility | -0.4% | Global, reflected in German projects | Medium term (2-4 years) |

| Refurbished Eastern-European Equipment Influx | -0.3% | Germany | Short term (≤ 2 years) |

| Tough Permitting & Local Opposition | -0.2% | Saxony, Bavaria, North Rhine-Westphalia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter EU Emissions and Noise Limits Raising Equipment Costs

EU Regulation 2024/1257 tightens off-road vehicle rules on CO₂, NOx, particulate, and noise, compelling OEMs to integrate advanced SCR after-treatment, battery durability monitoring, and acoustic dampening panels, adding double-digit percentage cost uplifts per unit [3]EUR-Lex, “Regulation 2024/1257 of the European Parliament,” eur-lex.europa.eu. The European Parliament estimates green-compliance outlays of EUR 28 billion for SMEs in the first year alone, a heavy burden for Germany’s fragmented supplier base. Domestic construction machinery revenues fell 21% in 2024, partly as customers delayed purchases amid cost spikes, underscoring parallel risk for mining equipment vendors. Compliance also cascades through supply chains: gearbox or hydraulic suppliers must document Scope 3 emissions, raising administrative overhead. As a result, fleet owners weigh second-hand imports against new low-emission units, dampening near-term replacement sales.

Commodity-Price Volatility Delaying CAPEX

Geopolitical shocks, from Red Sea shipping attacks to Indonesian export levies, keep copper, nickel, and lithium prices gyrating, with 45% of mining executives citing geopolitics as the prime uncertainty in 2025. Miners postpone German orders for shovel upgrades or processing-plant retrofits until pricing stabilizes, lengthening OEM sales cycles. Cash-rich majors in gold and iron ore sustain procurement, but mid-tier battery-metal hopefuls curb discretionary spending, hitting mid-size German fabricators hardest. Rising interest rates and EPC contractor shortages add further hesitation, leaving rental houses and refurbishers to bridge short-term fleet gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Diversified Underground Momentum Counters Surface Dominance

Surface units represented 47.55% of Germany's mining equipment market share in 2024, anchored by large lignite pits and open-pit aggregates. The segment’s unit shipments tread water as coal closures roll onward, yet overburden removal, slope stabilization, and landfill cover work keep draglines, electric rope shovels, and dozers busy. Underground equipment is on a faster 4.35% CAGR track, propped up by lithium, salt-cavern, and potash developments; orders favor low-profile LHDs, 30-tonne battery-electric trucks, and rapid-advance jumbos capable of bolting and boring in a single pass. Mineral-processing lines grow steadily, with German EPC firms delivering rotary calcination kilns and hydromet modules for battery-grade lithium carbonate. Drills and breakers ride the geothermal wave: down-the-hole hammers rated to 240 °C and sonic corers draw demand. Crushing and screening sets enjoy dual-use appeal, servicing both demolition recycling and critical-mineral pre-concentration streams.

Komatsu’s 2024 takeover of GHH adds narrow-vein articulated dumpers and 22-tonne loaders to its European catalog, widening competitive pressure in underground niches. Liebherr trials autonomous T 264 battery trucks alongside R 9400 E electric excavators, validating zero-emission bulk-haul solutions for lignite back-filling and overburden re-contouring. As the Germany mining equipment market transitions, OEM revenues tilt toward high-spec underground suites, field-retrofit automation kits and digitally-enabled spares contracts.

By Automation Level: Collaborative Autonomy Accelerates

Manual machines still dominate at 65.33% of the 2024 Germany mining equipment market size, reflecting legacy fleets and regulatory caution. Semi-autonomous rigs—remote-controlled bulldozers, tele-operated LHDs—gain quicker approvals, easing miners into hands-off workflows. Fully autonomous assets show a breakout 20.15% CAGR to 2030 as workforce gaps widen and AI perception stacks mature. Saxon lithium pilot pits now deploy radar-fused collision-avoidance algorithms, enabling loader stope cycles without line-of-sight operators. Real-time kinematics networks and 5G private LTE blankets sharpen positioning to ±5 cm, sustaining high-speed haul profiles while cutting idle fuel burn.

Investment economics favor autonomy: a fully autonomous surface drill cassette can trim hole deviation by 40% and raise powder-factor efficiency, offsetting capital premiums inside two years, according to operator case logs. Safety regulators also weigh in: fewer human-machine interfaces reduce incident rates, aiding permit renewals. Consequently, OEMs bundle autonomy software, LiDAR towers, and digital-twin training simulators in subscription models that guarantee annual productivity gains—a revenue pool set to eclipse hardware margins by 2028.

By Powertrain Type: Battery-Electric Gains Steady Ground

Internal-combustion engines cover 86.24% of working units in 2024, but looming low-emission zones and diesel phase-out debates push miners to hedge with electric fleets. Battery-electric trucks post a 6.57% CAGR through 2030, propelled by EUR 29 million KfW grants and TCO studies showing 20-30% maintenance savings over diesel in multi-shift underground duty. Hybrid genset machines fill interim roles, pairing small diesel primes with super-capacitor assist to flatten load spikes and reduce ventilation loads underground.

Liebherr’s USD 2.8 billion, 475-unit supply to Fortescue underlines market confidence: 360 autonomous battery trucks, 24 large electric excavators, and supporting chargers slated for global deployment, including a European pilot venue. Supply-chain pinch points persist—cell availability, thermal-propagations safety rules—but German tier-two suppliers ramp cathode-active-material and silicon-anode production, underpinning domestic battery pack assembly lines. By 2030, the Germany mining equipment market size tied to battery-electric units could approach USD 250 million, contingent on grid upgrades and standardized megawatt charging docks.

By Power Output: High-Horsepower Uptick Reflects Productivity Push

Equipment rated 500-1,000 HP accounts for 45.18% of active capacity, balancing maneuverability and drawbar pull across mixed coal, salt, and limestone settings. Machines above 1,000 HP outpace all other classes with a 5.43% CAGR; steep stripping ratios and autonomous haulage demand bigger payloads and ribbon-conveyor-friendly profiles. Less-than-500 HP niches persist for selective mineral stoping, urban geothermal coring, and reclamation dredging.

Herrenknecht’s Reef Boring Machine illustrates power escalation: its 1.8 m diameter, 60 m reach borers deploy 1,200 kW electric drives, enabling sub-level start drilling in hard rock reefs at double legacy rates. Autonomous payload-optimized wheel loaders require higher hydraulic horsepower overheads to backfill at the pace of driverless truck cycles, cementing the drift toward upper-tier power bands.

By Application: Mineral Extraction Surges as Coal Winds Down

Metal mining clings to 54.35% of 2024 revenues, anchored in iron-ore import blending, copper recycling furnaces, and specialty stainless feedstocks. Yet mineral extraction—lithium, rare-earths, fluorspar, kaolin—registers a brisk 4.92% CAGR as the EU battery chain localizes. Coal’s twilight frees capacity: redundant bucketwheel excavators migrate to overburden back-fill contracts, while cast-off conveyor galleries find second life in aggregate plants.

Zinnwald’s lithium hydroxide refinery will anchor a EUR 450 million CAPEX program requiring ball mills, vertical shaft kilns, and microwave crystallizers. Geothermal-coupled brine extraction in the Upper Rhine Valley showcases integrated value: one well pair delivers 5 MW thermal plus 2,000 t lithium carbonate, warranting dual-purpose pump trains and brine separators. These diversified mineral-plus-energy plays future-proof German OEM order books and soften coal-phase-out shocks.

Geography Analysis

Eastern Germany remains the epicenter of equipment deployments as Lusatia and Saxony juggle lignite remediation, critical-mineral digs, and hydrogen-ready salt cavern studies. Here, Germany's mining equipment market size linked to reclamation earthworks alone surpassed USD 210 million in 2025, dominated by dragline refurbishments and autonomous grader fleets. Saxony’s lithium corridor attracts high-spec underground loaders and hydromet modules, while Brandenburg’s opencast pits still need megawatt-class pumps and slope-stabilization drills through 2030.

Northern regions leverage mature salt and gas formations. Lower Saxony’s Etzel and Rüdersdorf caverns prompt demand for raise-borers and brine-salting pump skids, tied to Germany's mining equipment market share gains in underground construction tools. The North German Basin’s decommissioned gas wells are earmarked for 200-400 kW deep-borehole heat exchangers, stimulating orders for corrosion-proof casings and high-temperature packers. Offshore wind hooks into onshore cavern storage, so OEMs bundle hydrogen-ready compressors with condition-monitoring IoT modules.

Southern Germany pushes geothermal frontiers. Munich’s 25 km of deep boreholes deployed German-built top-drives and high-pressure mud pumps, underlining domestic supply depth. Bavaria’s legislature fast-tracks dozens of similar wells, giving retrofit drilling-system suppliers forward visibility. Industrial North Rhine-Westphalia houses a dense supplier and rebuild ecosystem, recycling decommissioned coal assets and exporting remanufactured equipment into CEE. Federal SME programs, such as Sonderprogramm Umweltwirtschaft, inject EUR-level grants into electrification, emissions-monitoring and predictive-maintenance startups—feeding the Germany mining equipment market with spinoff service revenues.

Competitive Landscape

The field shows moderate consolidation, with significant market players like Liebherr, Komatsu, Epiroc, Sandvik, and Herrenknecht. Liebherr leverages scale: its seven-year, USD 2.8 billion Fortescue contract covers 475 zero-emission pieces, adding reference deployments for future German tenders. Komatsu’s July 2024 purchase of GHH Group upgrades its narrow-vein product depth and European service centers. Epiroc continues bolt-on buys—ASI Mining for autonomy software—strengthening value-added subscription models that cushion cyclical hardware dips.

Refurbishers import post-Soviet blasthole rigs and loader chassis, retrofit Tier-4F engines, and undercut new equipment by up to 40%, pressuring OEM list prices. German mid-caps pivot to niche expertise: Herrenknecht in large-diameter shafts, Bauer in diaphragm walls, Manitou in pick-and-carry telehandlers for confined potash galleries. Digital service contracts gain traction: uptime guarantees tied to predictive analytics create annuities shielding OEMs from capex volatility.

Technology roadmaps converge on autonomy and electrification. Sandvik’s acquisition of Artisan Vehicles accelerates battery-electric loader rollouts, while Liebherr’s in-house pack assembly in Ehingen reduces reliance on Asian cells. Partnerships proliferate: Siemens supplies DC fast-charge substations, Deutsche Telekom pilots 5G-edge compute in Brandenburg pits, and BASF tests sodium-ion packs in underground LHD prototypes.

Germany Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr-International AG

Epiroc AB

Sandvik AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Liebherr displayed more than 100 exhibits at Bauma 2025, headlined by the battery-electric T 264 mining truck and R 9400 E excavator, and announced hydrogen infrastructure tie-ups with Fortescue and STRABAG.

- July 2024: Komatsu finalized the takeover of GHH Group GmbH, adding German underground loaders and dumpers to its portfolio and expanding regional service reach.

- May 2024: Komatsu Germany Mining Division and SMS Equipment jointly unveiled the PC9000, now the largest hydraulic mining excavator in Komatsu’s global range.

Germany Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 – 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 – 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

What revenue is projected for Germany’s mining equipment suppliers by 2030?

The Germany mining equipment market size is forecast to reach USD 1.86 billion by 2030.

Which equipment category should manufacturers prioritize for growth?

Underground mining equipment shows the fastest 4.35% CAGR, aided by lithium and hydrogen-storage projects.

Are battery-electric trucks commercially viable in German mines?

Yes, Liebherr’s large battery-electric fleet orders and federal R&D incentives are pushing a 6.57% CAGR for electric units.

How critical is autonomy for German operators?

Acute labor shortages and safety rules drive a 20.15% CAGR for fully autonomous fleets, especially in surface pits.

Page last updated on: