India Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

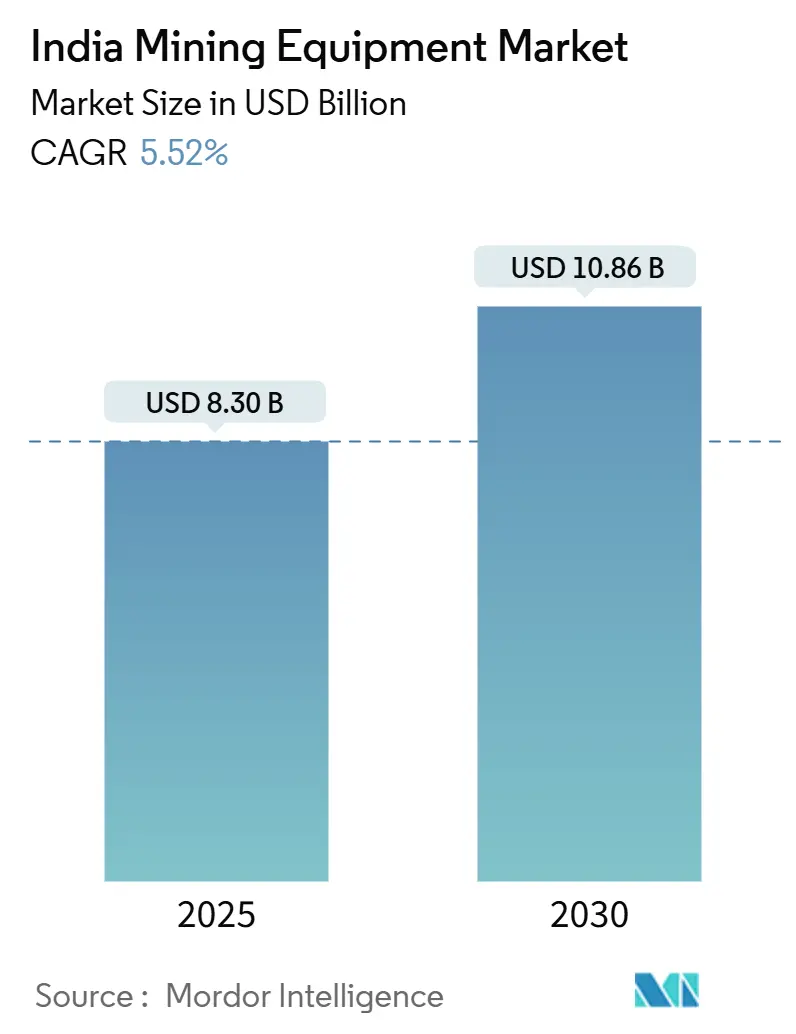

| Market Size (2025) | USD 8.30 Billion |

| Market Size (2030) | USD 10.86 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Mining Equipment Market Analysis by Mordor Intelligence

The India mining equipment market size stands at USD 8.30 billion in 2025 and is forecast to reach USD 10.86 billion by 2030, expanding at a 5.52% CAGR. This outlook reflects a maturing sector in which digitalization, safety regulation, and decarbonization imperatives outweigh pure volume expansion. Government infrastructure outlays, led by the USD 759.76 billion National Infrastructure Pipeline, continue to propel equipment demand while Coal India Limited’s mechanization roadmap accelerates fleet renewal. The launch of a 5G test laboratory by the Central Mine Planning & Design Institute (CMPDI) underlines a pivot toward real-time data, predictive maintenance, and automation that can trim unplanned downtime by up to 20%. Investment clustering in Eastern India—anchored by billion-dollar steel and aluminum projects—keeps surface machines dominant, yet the fastest growth is shifting toward underground, electric, and autonomous solutions that help operators comply with tightening ESG rules and mitigate acute skilled-labor shortages.

Key Report Takeaways

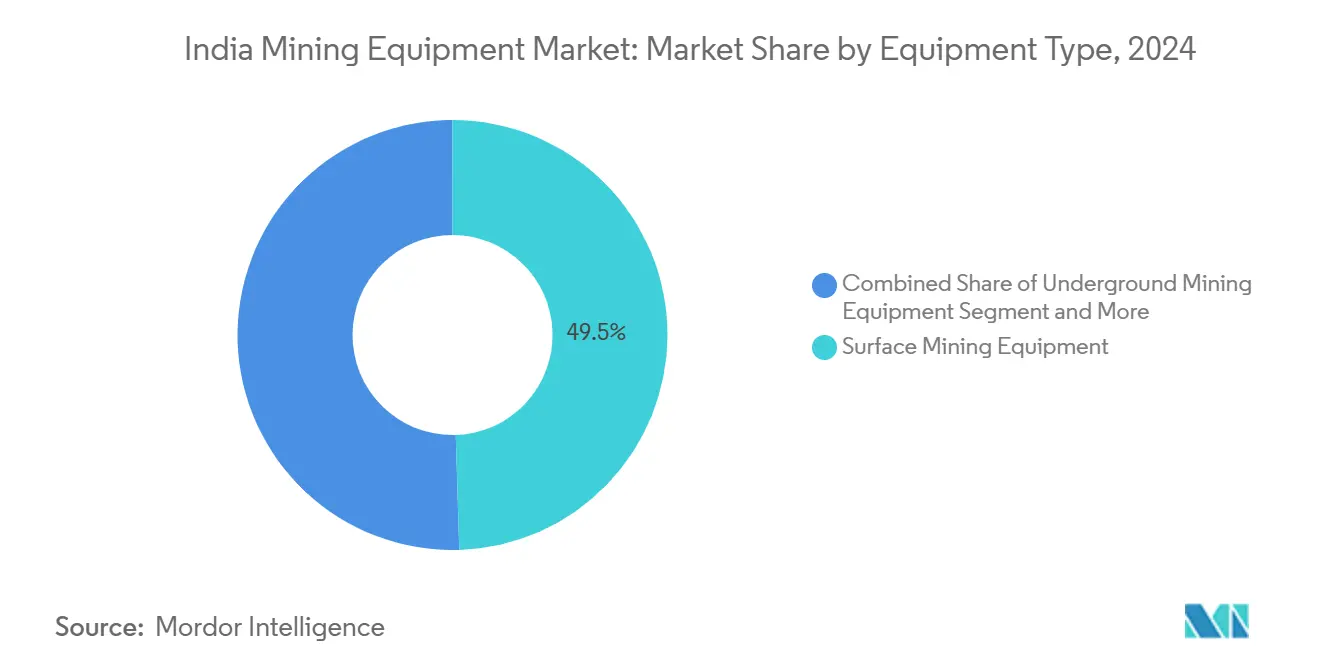

- By equipment type, surface mining commanded 49.51% of India mining equipment market share in 2024, whereas underground mining is on course for the quickest expansion at a 6.73% CAGR through 2030.

- By automation level, manual equipment held 73.66% share of the India mining equipment market size in 2024, while fully autonomous fleets are advancing at a 28.65% CAGR to 2030.

- By powertrain, internal-combustion machines accounted for 94.17% share of the India mining equipment market size in 2024; battery-electric units are projected to grow at 9.51% CAGR during the same horizon.

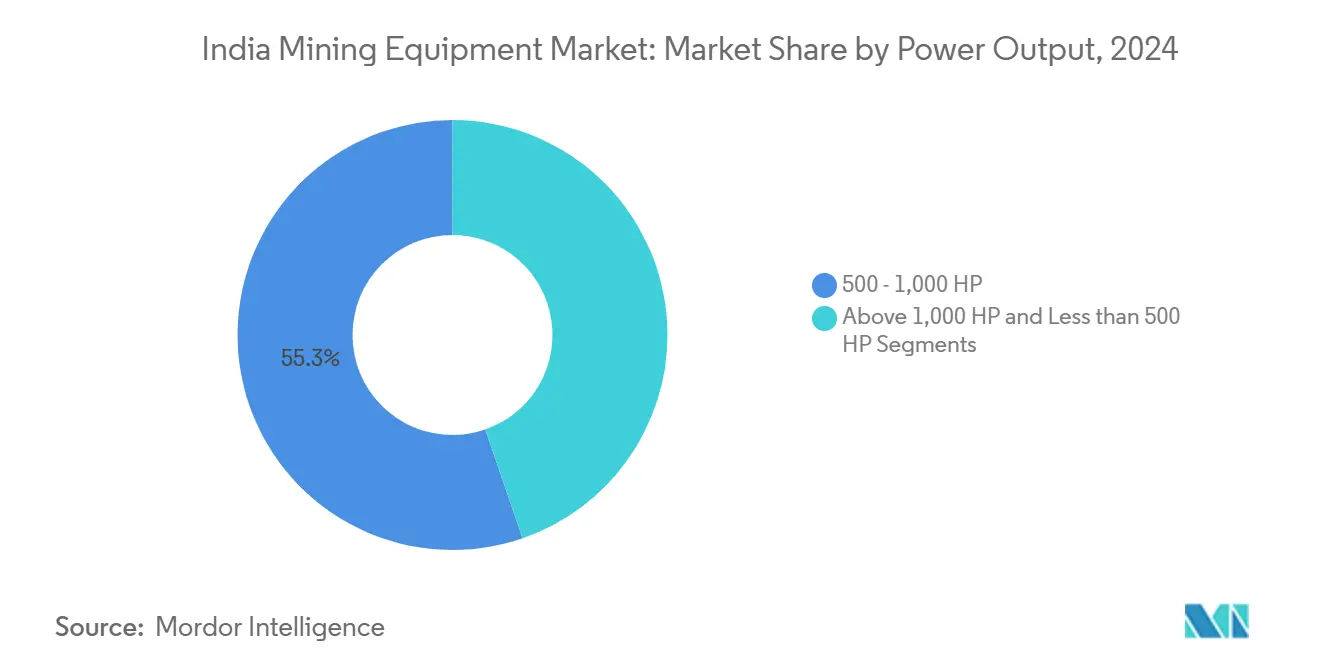

- By power output, the 500–1,000 HP bracket captured 55.26% of the India mining equipment market size in 2024, with >1,000 HP models recording the highest 6.84% CAGR.

- By application, metal mining led with a 47.13% revenue share in 2024, whereas mineral mining is expected to post a 7.63% CAGR up to 2030.

- By geography, Eastern India dominated at 45.71% share in 2024; Southern India is slated for the swiftest 6.15% CAGR through 2030.

India Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Infrastructure Build-Out Spurring Mineral Demand | +1.2% | National, Eastern and Central | Medium term (2-4 years) |

| Coal India Mechanization and Capacity Expansion | +0.9% | Eastern core, Central spillover | Short term (≤ 2 years) |

| Stricter Safety Norms Accelerating Automation | +0.7% | National, early uptake in East and West | Long term (≥ 4 years) |

| Lithium-Copper Exploration Boom | +0.5% | Central and Northern | Long term (≥ 4 years) |

| “Make in India” Push for Indigenous Output | +0.4% | National, West and South hubs | Medium term (2-4 years) |

| Rise of Rental Models Widening Access | +0.3% | Tier-1 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Build-Out Spurring Mineral Demand

Massive public works spending is amplifying mineral extraction, thereby enlarging the India mining equipment market. The Ministry of Coal aims to raise annual coal output from 773.6 million t in 2024 to 1.5 billion t by 2030, a target that compels upgrades across 113 commercial blocks with a combined peak capacity of 257.6 million t [1]Ministry of Coal, “Commercial Coal Block Auction Data,” coal.nic.in. Rail corridors worth USD 4.3 billion in Chhattisgarh are likewise reshaping haulage networks, accelerating demand for high-horsepower loaders, haul trucks, and conveyors. A USD 4 billion Critical Mineral Mission covering 1,200 exploration projects enlarges the addressable base for drills and processing gear, while the asset-monetization plan to unlock USD 344 billion in mining assets by 2025 incentivizes private participation. Together, these schemes increase multi-commodity equipment orders and compress replacement cycles, supporting sustained mid-single-digit growth in the India mining equipment market.

Coal India’s Mechanization and Capacity Expansion Roadmap

Coal India Limited invested USD 2.38 billion in FY 2024, earmarking USD 369 million solely for heavy earth-moving machinery. Subsidiaries SECL and MCL are pioneering paste-fill and continuous-miner solutions, signaling irreversible movement toward mechanized underground operations. Production is targeted to jump to 1 billion t by FY 2027, fostering sharp uptake of above 1,000 HP excavators, high-capacity surface miners, and autonomous haulage systems. Such spending strengthens OEM order books and underscores the shift from manpower-intensive to technology-intensive production across the India mining equipment market.

Stricter Safety Norms Accelerating Automation Adoption

The Directorate General of Mines Safety has refined certification protocols that explicitly favor digitally enabled and autonomous systems [2]Directorate General Of Mines Safety, "Certificate Details," www.dgms.gov.in. Compliance pushes operators toward equipment fitted with advanced collision-avoidance, fatigue monitoring, and remote-operation modules that can reduce lost-time incidents by up to 60%. CMPDI’s 5G test bed further proves the viability of latency-free control loops in deep pits, making autonomy a practical route to regulatory adherence. These developments quicken the migration from manual to semi-autonomous and eventually fully autonomous fleets, thereby altering product-mix dynamics within the India mining equipment market.

Lithium-Copper Exploration Boom Requiring Specialty Gear

Discovery of lithium in Chhattisgarh and a 5.9 million t inferred deposit in Jammu & Kashmir necessitates purpose-built clay-hosted extraction technology and precision drill rigs. International tie-ups—including India’s USD 24 million exploration pact with Argentina—import new metallurgical and hydrometallurgical methods that demand equipment beyond the coal and iron-ore canon. Government R&D grants totaling USD 384 million in FY 2025 catalyze localized manufacturing of specialty rigs and separation units, adding a nascent but high-margin layer to the India mining equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex and Financing Hurdles | -0.8% | Nationwide, acute for SMEs | Short term (≤ 2 years) |

| Tightening Emission and ESG Compliance Costs | -0.6% | National, strict in West and South | Medium term (2-4 years) |

| Skilled-Operator Deficit for Digital/Electric Machinery | -0.4% | Nationwide, severe East and Central | Long term (≥ 4 years) |

| Patchy Mine-Site Connectivity Limiting Autonomy | -0.3% | Remote Eastern and Central belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Financing Hurdles

Specialized rigs often carry unit prices topping USD 5 million, and lenders with mining risk expertise remain scarce. Non-bank financiers expanded assets 16-18% annually up to FY 2026, yet equipment loans to smaller miners remain rationed, prolonging payback horizons and delaying purchases. Rising wage bills—daily rates have reached USD 12 for site labor—absorb working capital that could otherwise fund fleet renewal. Although a proposed state-backed infrastructure NBFC may act as a guarantor for lower-rated issuers, in the interim, many operators defer or down-spec capital commitments, diluting growth potential within the India mining equipment market.

Tightening Emission and ESG Compliance Costs

SEBI’s Business Responsibility & Sustainability Report mandates Scope 3 disclosures for the top 250 listed entities from FY 2025. Electric or hybrid machines cost 15–25% more than diesel peers, yet miners face increasing pressure to adopt low-carbon technology or risk investor backlash. Compliance already consumes 4–7% of operating budgets for larger producers. OEMs such as Epiroc pledge emission-free underground fleets by 2025, but retrofit complexities and charging infrastructure gaps constrain near-term switching, tempering the India mining equipment market’s upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Dominance Meets Underground Momentum

Surface machinery held a 49.51% slice of the India mining equipment market size in 2024, anchored by open-pit coal and iron-ore operations that leverage large draglines, rope shovels, and 500–1,000 HP dozers. Record coal output of 997.826 million t in FY 2024 provided the volume base for continuous orders of high-capacity surface miners. In contrast, underground equipment is scaling rapidly at a 6.73% CAGR as reserves deepen, ground-pressure rules tighten, and paste-fill technology enters commercial service under SECL’s Singhali project.

Downstream equipment such as crushers, screens, and mineral processors benefit from Odisha-led steel expansions and the government’s Critical Mineral Mission. Drills and breakers ride on exploration budgets that encompass 1,200 greenfield surveys, while loaders and haulage trucks in the greater than 1,000 HP class grow 6.84% CAGR, reflecting Coal India’s pivot to higher tonnage payloads. Gainwell Engineering’s indigenous room-and-pillar system exemplifies how local manufacturing shifts import share and opens export lanes, further diversifying supply within the India mining equipment market.

By Automation Level: Manual Legacy Under Autonomous Disruption

Manual rigs still constitute 73.66% of the India mining equipment market size in 2024, given a historically labor-heavy mining model and an operator base well-versed in conventional machinery. However, the surge in autonomy—forecast at 28.65% CAGR—signals a critical inflection point. Skilled-labor scarcity and 5G-enabled predictive analytics now pivot purchasing decisions toward unmanned drill rigs, remote dozers, and driverless trucks capable of 20–30% cost savings and 15–20% productivity gains.

Semi-autonomous platforms allow a phased transition, combining onboard AI with human supervision for complex cut-and-fill cycles. CMPDI’s real-time data pilot validates latency requirements, accelerating the business case for fleet-wide upgrades. Although capital intensity is higher, operators weigh the trade-off against regulatory safety credits and work-hour reductions. The evolving mix should gradually rebalance revenue pools, embedding digital services and software as recurring value streams in the India mining equipment market.

By Powertrain Type: Electric Inroads within ICE Stronghold

Internal-combustion engines dominate at 94.17% share, supported by mature diesel supply chains and proven resilience in India’s dusty, high-temperature mine sites. Nevertheless, battery-electric units project a 9.51% CAGR as ESG targets tighten and underground ventilation costs rise. JCB India’s hydrogen prototypes and Hitachi’s 1.7-t zero-emission excavator reflect OEM readiness to meet these mandates.

Charging infrastructure remains embryonic, especially in isolated coal fields, but state-level renewable-energy corridors and the National Hydrogen Mission are slated to close that gap. Hybrid drivetrains serve as transitional solutions, balancing range anxiety with emissions reduction. Over the forecast horizon, equipment financing incentives tied to carbon metrics could accelerate electric uptake, recasting value pools across the India mining equipment market.

By Power Output: Mid-Range Workhorses and High-Power Upswing

Units rated 500–1,000 HP amassed 55.26% of India mining equipment market share in 2024 because they strike an optimal cost-performance balance for the country’s myriad mid-scale pits. Their parts supply chains are deep, operators are plentiful, and service technicians are widely available, ensuring high asset uptime.

Conversely, above 1,000 HP machines attract the fastest 6.84% CAGR as mega-projects such as JSW Steel’s 13.2 million t Paradip plant and Vedanta’s Jharsuguda aluminum hub demand mass-haulage efficiency. OEMs like Komatsu are rolling out large battery-electric LHDs tailored for deep hard-rock mines, extending the high-power narrative beyond diesel reliance. Sub-500 HP equipment retains a niche among narrow-seam and construction-adjacent operations, reinforcing a three-tiered power-output hierarchy within the India mining equipment market.

By Application: Metals Anchor, Minerals Accelerate

Metal mining controlled 47.13% of the India mining equipment market size in 2024, propelled by integrated steel value chains that span Odisha through Andhra Pradesh. ArcelorMittal Nippon Steel’s 7 million t mill in Andhra anchors forward demand for iron-ore extraction and processing equipment. Diversification toward copper, zinc, and gold broadens the commodity foundation.

Mineral mining, especially lithium and rare earths, captures the highest 7.63% CAGR, reflecting a strategic pivot toward energy-transition inputs. Chhattisgarh’s clay-hosted lithium and the private gold project in Kurnool illustrate how specialty geology calls for precision rigs, gravity concentrators, and hydrometallurgy kits. While coal mining continues to produce volume orders, long-run policy orientation toward renewables and critical minerals will reshape the India mining equipment market product-mix profile.

Geography Analysis

Eastern India generated 45.71% of the India mining equipment market revenue in 2024, fortified by Odisha’s USD 7.8 billion steel complex, Vedanta’s USD 12 billion aluminum expansion, and Chhattisgarh’s multi-corridor rail upgrade. Paradip Port’s 145 million t throughput provides deep-draft import capability for oversized shovels and haul trucks, reinforcing the region’s logistics advantage. CMPDI’s 5G laboratory in Ranchi cements Eastern India as the digitization frontier.

Southern India records the fastest 6.15% CAGR through 2030, buoyed by ArcelorMittal Nippon Steel’s greenfield build in Andhra and India’s first private gold mine in Kurnool. Karnataka’s USD 2.16 billion NMDC steel project and Chennai-Bangalore equipment hubs supply talent and aftermarket services, amplifying premium-segment uptake [3]Nippon Steel Corporation, “AP Integrated Steel Project,” nipponsteel.com.

Western India leverages Maharashtra’s financial base and Gujarat’s ports to sustain steady replacement demand, while Central India’s coal and nascent lithium resources support a mix of conventional and specialty gear. Northern India, though smaller, hosts Jammu & Kashmir’s 5.9 million t lithium find, setting the stage for high-spec exploration tool demand. Collectively, regional heterogeneity ensures that the India mining equipment market continues to witness localized growth pockets even as Eastern dominance persists.

Competitive Landscape

The India mining equipment market is moderately concentrated, with global majors retaining technology leadership amid vibrant domestic challengers. Caterpillar and Komatsu collectively control a significant share of global surface-equipment revenue, followed by Volvo and Tata Hitachi carving out a strong Asia–Pacific foothold. Komatsu’s July 2024 acquisition of GHH Group deepens its underground portfolio, enabling comprehensive offerings for Indian hard-rock customers.

Epiroc pledges emission-free fleets by 2030 and showcases local assembly lines, whereas Sandvik secured SEK 750 million orders for battery-electric rigs, exemplifying how sustainability steers procurement. Domestic OEMs gain ground: BEML captured USD 69.8 million in combined defense and coal contracts, and its BRS21 rope shovel showcases indigenously engineered heavy lifting.

Gainwell’s room-and-pillar launch underscores how licensing alliances can localize sophisticated technology. Tech start-ups such as 3Laws Robotics furnish AI software that bridges the gap between autonomous hardware and Indian operating conditions. Against this backdrop, OEMs differentiate through aftermarket ecosystems, digital platforms, and ESG-aligned value propositions, enriching competitive dynamics within the India mining equipment market.

India Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Sandvik AB

-

Epiroc AB

-

BEML Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BEML unveiled the BRS21, India’s largest indigenously developed electric rope shovel, delivering a zero-emission option for overburden stripping.

- April 2025: SANY India rolled out the locally built 100-t SKT130S hybrid dump truck from its Pune plant, featuring a 925 kW engine and 61 m³ heaped capacity.

- January 2025: Gainwell Engineering launched India’s first home-grown room-and-pillar package, including continuous miners and feeder breakers from its Panagarh factory.

- May 2024: Sandvik Mining & Rock Solutions won a multi-unit order from Hindustan Zinc to supply loaders, trucks, and fully automated i-series production rigs.

India Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 – 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Northern India |

| Eastern India |

| Western India |

| Southern India |

| Central India |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 – 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Region | Northern India |

| Eastern India | |

| Western India | |

| Southern India | |

| Central India |

Key Questions Answered in the Report

How large is the India mining equipment market in 2025?

The market stands at USD 8.30 billion in 2025 and is projected to reach USD 10.86 billion by 2030, reflecting a 5.52% CAGR.

Which segment leads equipment demand by type?

Surface mining machinery accounts for 49.51% revenue share, supported by high-volume coal and iron-ore extraction.

Where is demand growing fastest geographically?

Southern India shows the highest 6.15% CAGR due to greenfield steel and private gold projects requiring advanced fleets.

What is driving the adoption of autonomous equipment?

Stricter safety rules, skilled-labor shortages, and proven productivity gains of 15–20% are spurring rapid uptake of autonomous rigs.

Page last updated on: