China Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

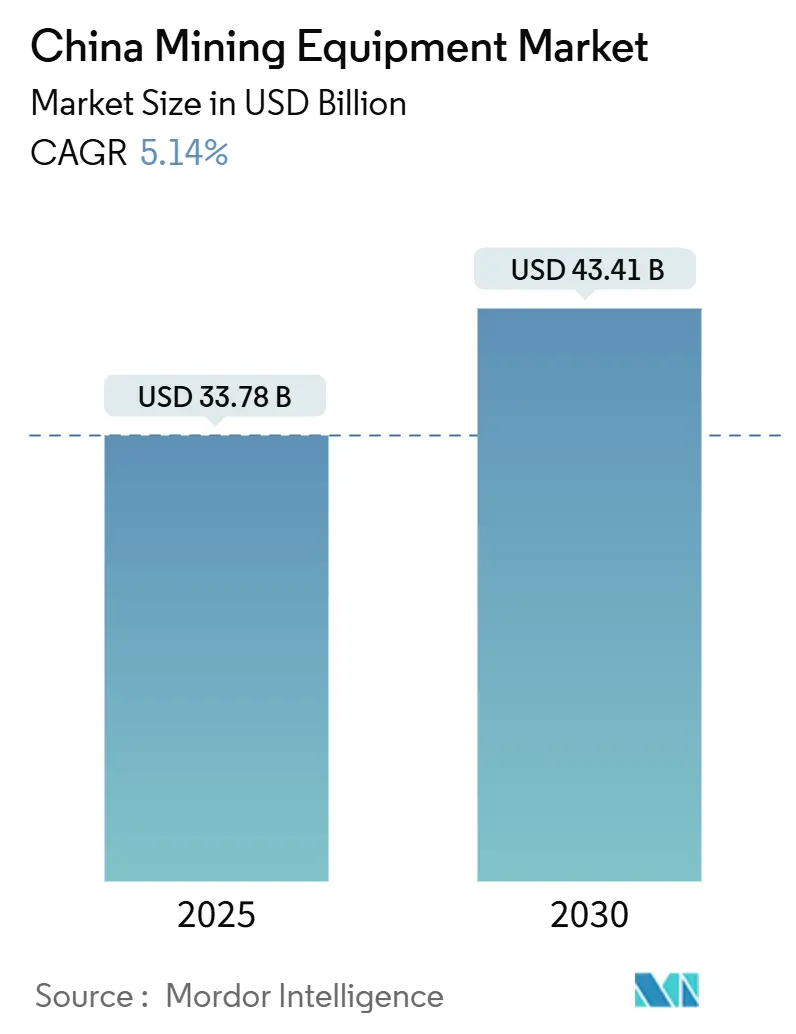

| Market Size (2025) | USD 33.78 Billion |

| Market Size (2030) | USD 43.41 Billion |

| Growth Rate (2025 - 2030) | 5.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mining Equipment Market Analysis by Mordor Intelligence

The China mining equipment market size is USD 33.78 billion in 2025 and is projected to reach USD 43.41 billion in 2030, exhibiting a 5.14% CAGR during 2025-2030, underscoring the central role the sector plays in national industrial modernization. This trajectory is driven by government capital expenditure on strategic metals, rapid automation, and the electrification of haulage fleets, all of which deepen the technological intensity of mining operations and stimulate constant equipment renewal cycles. Central state-owned enterprises have already earmarked more than CNY 3 trillion for fleet upgrades, a spending stream that enhances demand for high-precision drills, sensor-laden loaders, and AI-enabled haul trucks. Digitalization initiatives such as “Intelligent Mine” pilots increase the installed base of 5G-connected machinery, while breakthroughs in electro-kinetic rare-earth extraction reshape requirements for mineral-processing lines. The cumulative effect is a shift from legacy diesel fleets toward semi- and fully autonomous battery-electric vehicles, giving local manufacturers a first-mover edge and reinforcing Beijing’s resource-security agenda.

Key Report Takeaways

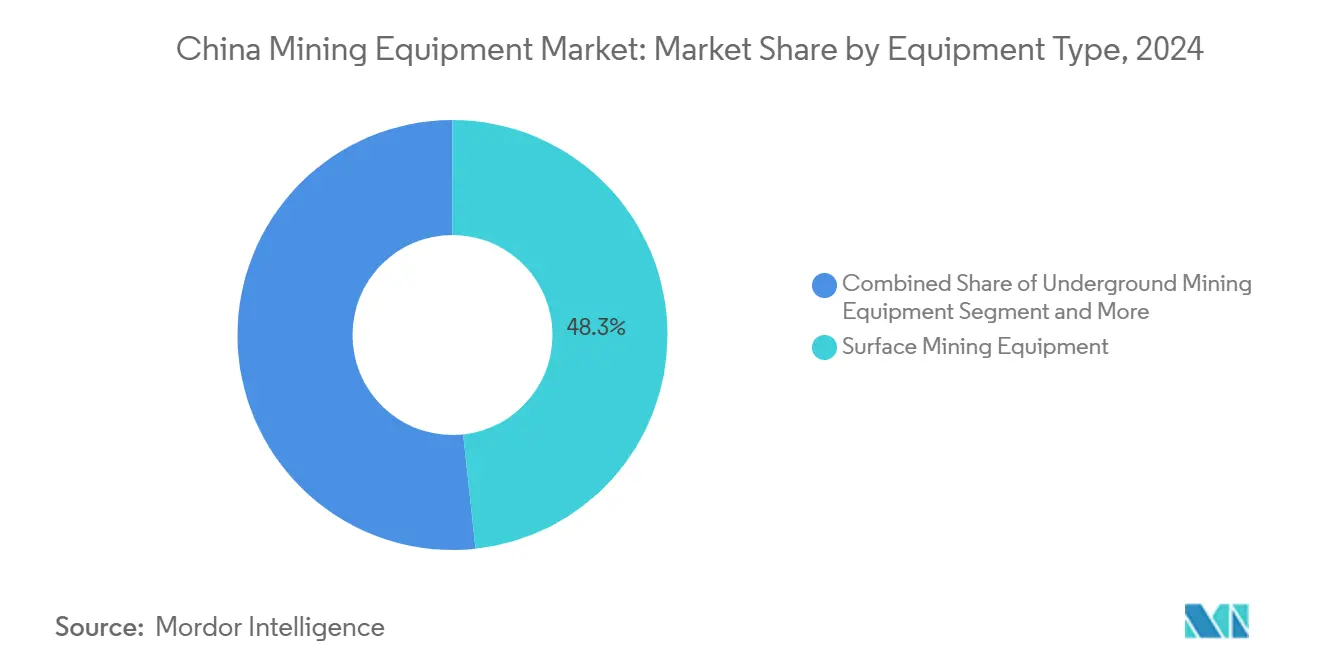

- By equipment type, Surface Mining Equipment led with a 48.33% share of the China mining equipment market in 2024, whereas Loaders and Haul Trucks recorded the fastest 6.36% CAGR forecast through 2030.

- By automation level, Manual Equipment held 60.15% of the China mining equipment market share in 2024; Fully Autonomous Equipment is projected to advance at an 8.24% CAGR to 2030.

- By powertrain type, Internal-Combustion Engine Vehicles accounted for 70.42% of the China mining equipment market size in 2024, while Battery-Electric Vehicles will expand at a 9.07% CAGR during 2025-2030.

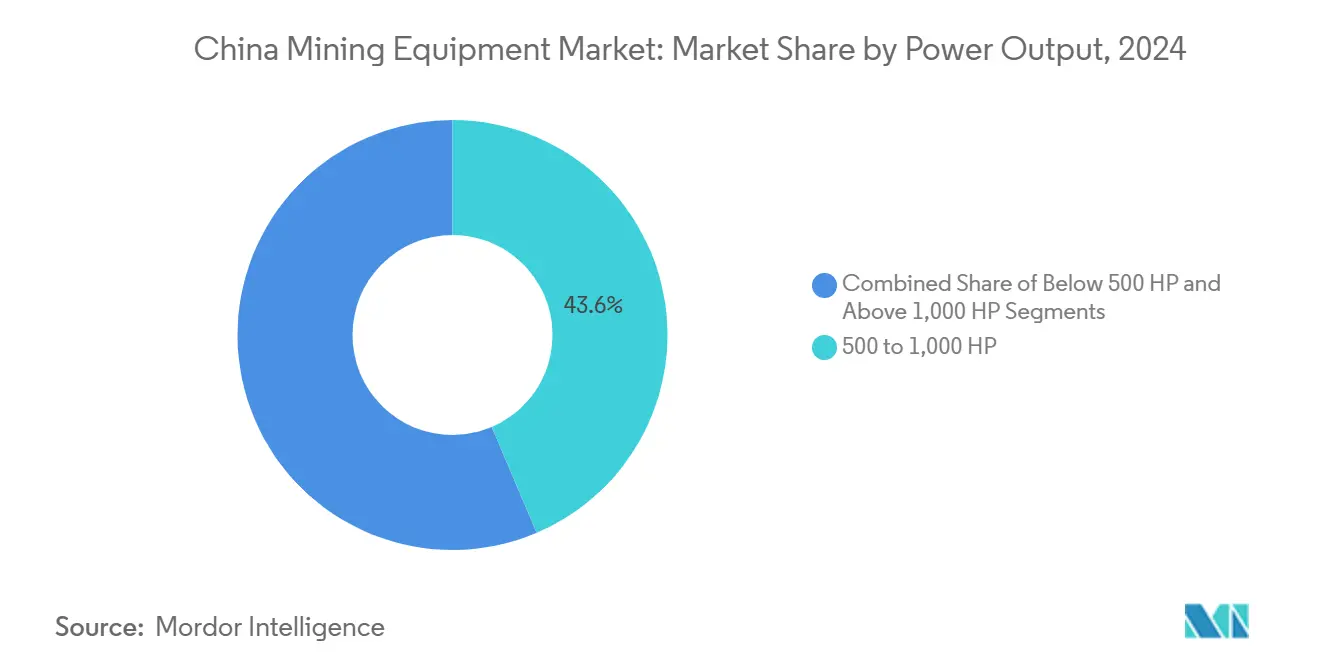

- By power output, the 500-1,000 HP class captured 43.55% of the China mining equipment market size in 2024; sub-500 HP machines will post the quickest 5.94% CAGR.

- By application, Coal Mining commanded 54.61% of the China mining equipment market share in 2024; Non-metallic Mineral Mining exhibits the highest 7.16% CAGR outlook.

- By region, North China dominated with 29.44% of the China mining equipment market in 2024, whereas Southwest China is forecast to grow fastest at 6.13% CAGR through 2030.

China Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic Metals Infrastructure Spend | +1.2% | National, North China and Inner Mongolia | Medium term (2-4 years) |

| Shift to Battery-Electric Fleets | +0.9% | Nationwide, early uptake in Inner Mongolia & Xinjiang | Medium term (2-4 years) |

| Automation for Safety & Productivity | +0.8% | National; pilots in Shanxi & Inner Mongolia | Long term (≥ 4 years) |

| Rare-Earth Expansion for Clean Tech | +0.7% | Southwest China | Long term (≥ 4 years) |

| “Intelligent Mine” Pilot Subsidies | +0.6% | Coal-producing provinces | Medium term (2-4 years) |

| LFP Battery Recycling Demand | +0.4% | East and South-Central China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Spend on Strategic Metals

State-backed investment is the single largest demand catalyst for mining machinery. More than CNY 3 trillion in fleet modernizations are being executed by central SOEs, specifically to improve the extraction of cobalt, copper, nickel, and lithium. Strategic stockpile targets accelerate purchasing of automated drills and AI-driven separation lines as the National Food and Strategic Reserves Administration widens tenders through 2027. Export controls on tungsten, tellurium, and other niche metals redirect processing in-country, creating capacity gaps that local equipment suppliers rush to fill. Inner Mongolia alone has boosted its mineral exploration budget to CNY 750 million for 2025, prompting orders for high-tonnage loaders and high-precision coring rigs. The result is a predictable multi-year equipment procurement cycle underpinning revenue visibility for OEMs.

Shift Toward Battery-Electric Mine Fleets

Electrification mitigates diesel price volatility and cuts ventilation costs in underground sites. Huaneng’s deployment of 100 self-driving, LFP-powered trucks at the Yimin mine improves haul efficiency by 20% compared with manned diesel variants [1]South China Morning Post, “World’s Biggest Autonomous Electric Mining Fleet Debuts,” scmp.com. Local OEMs such as XCMG and Sany have commercialized above 120 t battery-electric dumpers that withstand harsh temperature swings on the Ordos plateau. Xinjiang’s Shitoumei pit now runs 91 autonomous trucks using BeiDou and 5G for centimeter-level guidance, trimming 200 operator positions and driving lower OPEX. Collaboration between Rio Tinto and State Power Investment on battery-swap technologies validates China’s export potential for next-generation mine haulage. Subsidized charging corridors and a nationwide push for renewable electricity further reinforce the total-cost-of-ownership advantage of electric fleets.

Automation Push for Safety and Productivity

China’s mines are moving from man-led to machine-centric operations. The Dahaize Mine’s AI overhaul elevated net profit margins to 40% in 2024 on 20 Mt output, highlighting the ROI of digitization. Shanxi operates 118 intelligent coal mines plus 1,491 automated faces, where real-time data lowers energy use and narrows output variance. The YuGong system delivers 24-hour haulage with 12% less fuel per ton, thanks to self-learning algorithms supervising route optimization. National Energy Administration directives mandate digital twins and industrial internet nodes, standardizing automation architectures nationwide. A robust 5G-Advanced backbone ensures packet-loss-free control, making autonomous payload optimization technically viable and commercially attractive.

Rare-Earth Expansion for Clean-Tech Supply Chains

China mines 68.57% of global rare earths and has lifted 2024 quotas by 12.5%, intensifying equipment demand in Southwest deposits. Electro-kinetic field extraction raises recovery to 95%, slashing ammonia effluents by 95% and cutting cycle time by 70%. Mianning-Dechang holds 250 kt high-grade reserves, necessitating precision excavators, ion-exchange separators, and low-impact tailings systems. April 2025 export halts on heavy REE signal tighter domestic processing, triggering surge orders for high-throughput roasters and solvent-extraction modules. Rising PrNd oxide deficits forecast for 2025 further motivate capacity additions in beneficiation and metallurgical lines tailored to light-REE streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity Price Volatility | -0.8% | Export-oriented regions | Short term (≤ 2 years) |

| High Environmental Compliance Costs | -0.6% | Nationwide, eastern provinces | Medium term (2-4 years) |

| Chip Shortages for Autonomy Systems | -0.5% | Nationwide, global supply chains | Short term (≤ 2 years) |

| Carbon Pricing Increasing OPEX | -0.4% | Key industrial provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Dampening CAPEX

Weak iron-ore prices amid real-estate corrections encourage miners to defer replacement cycles. Although energy-transition metals enjoy structural demand, synchronized slowdowns across China, the US, and Europe inject uncertainty into equipment ROI calculations. Low rare-earth spot prices render many private ventures non-bankable, tightening finance for specialized machinery. Global survey data shows 84% of mining executives regard geopolitical fragmentation as an investment impediment. Market swings compel operators to favor modular equipment capable of cross-commodity deployment, heightening competition among OEMs for versatile designs.

Stringent Environmental Compliance Costs

Carbon-neutrality pledges raise both CAPEX and OPEX. The EU Carbon Border Adjustment Mechanism covers 31.14% of Chinese exports to Europe, pressuring high-carbon steel and aluminum supply chains that feed mining equipment fabrication. Extensions to China’s ETS could capture nearly 80% of national CO₂ output, forcing mines to buy allowances or retrofit fleets with low-emission powertrains [2]International Monetary Fund, “China ETS Reform Scenarios,” imf.org. An estimated USD 700 billion in coal-plant transition costs illustrate the scale of decarbonization burdens spilling into mining. Consequently, buyers prioritize machinery with embedded emissions-monitoring modules and higher energy efficiency, lengthening sales cycles for legacy diesel platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Dominance Aligns With Open-Pit Strategy

Surface Mining Equipment accounts for a 48.33% share of the China mining equipment market in 2024, testament to the prevalence of bulk open-pit operations in coal, iron-ore, and rare-earth belts. High-capacity shovels, draglines, and 240 t-plus dumpers provide economies of scale, while automation modules enhance shift utilization. Loaders and Haul Trucks are projected to clock a 6.36% CAGR, underpinned by battery-electric variants that reduce ventilation costs and comply with regional carbon-pricing schemes. Underground equipment retains relevance in the Yangquan and Pingdingshan coalfields, yet ventilation expenses and safety mandates curb its growth outlook.

Demand for mineral-processing lines accelerates as electro-kinetic extraction lifts rare-earth recovery to 95%. Crushing and screening machines witness parallel upticks as government stockpiles expand. Drills and breakers benefit from Inner Mongolia’s CNY 750 million exploration budget, spurring directional-coring and geostatistical sampling activities. Sophisticated on-board telematics become standard, converting once-mechanical shovels into nodes on a 5G edge-cloud architecture, a shift that deepens China's mining equipment market digital entanglement.

By Automation Level: Rapid Shift From Manual To Autonomous

Manual fleets still dominate, holding 60.15% of 2024 shipments, but their share is set to slide as operators chase productivity dividends. Fully autonomous rigs are poised for an 8.24% CAGR, catalyzed by NEA mandates for intelligent coal mines and national safety campaigns against gas explosions. Semi-autonomous equipment offers a lower entry hurdle, combining operator cabins with AI collision-avoidance to accelerate learning curves.

Pilot projects such as the YuGong 24-hour haulage system confirm fuel savings of 12% per ton. Meanwhile, Xinjiang’s 91-unit truck fleet demonstrates head-count reductions of 200 roles, validating immediate labor-cost arbitrage. These data points justify the premium for autonomy packages, particularly when paired with optimized battery utilization. As AI algorithms mature, predictive maintenance further lowers lifecycle costs, reinforcing the technology’s long-term economics within the China mining equipment market.

By Powertrain Type: ICE Dominance, Electric Acceleration

Internal-combustion drive trains represented 70.42% of deliveries in 2024, reflecting historical fuel infrastructure and upfront cost advantages. Yet the 9.07% CAGR outlook for Battery-Electric Vehicles underscores a tipping point catalyzed by 5G connectivity, falling LFP costs, and zero-emission mandates. Hybrid formats provide interim decarbonization, combining diesel gensets with regenerative braking to cut fuel by 20% on downhill hauls.

Battery-swap architectures, as piloted by Rio Tinto and State Power Investment, shrink charging downtime to 6 minutes, narrowing utilization gaps with diesel fleets. Moreover, underground mines prize the absence of exhaust particulates, which halves ventilation energy and complies with stricter occupational-health codes. The evolving grid mix—where renewables exceed 40% in Inner Mongolia—further sweetens the total-cost curve for electric drive chains, cementing their role in future China mining equipment market trajectories.

By Power Output: Mid-Range Sweet Spot With Low-hp Outperformance

Equipment rated 500-1,000 hp captures 43.55% of the China mining equipment market size, balancing maneuverability and payload across varied ore bodies. High-hp giants above 1,000 hp remain essential for ultra-deep stripping ratios in Ordos coal basins, yet their operating cost intensity dampens growth.

Conversely, sub-500 hp machines will post a 5.94% CAGR, fueled by precision tasks in rare-earth beneficiation and narrow-vein gold lodes. Advances in high-torque electric motors shrink the performance penalty at lower hp bands, enabling smaller rigs to tackle jobs once reserved for mid-range diesels. As autonomy reduces operator-skill constraints, fleet managers opt for right-sizing strategies that maximize tonnage shipped per kWh, translating into demand clustering around the mid- to low-hp spectrum.

By Application: Coal Dominance Amid Diversification

Coal commands 54.61% of the 2024 China mining equipment market share, underpinned by 118 intelligent coal mines in Shanxi alone. Yet policy signals favor strategic minerals; Non-metallic Mining led by rare-earths is set for a 7.16% CAGR, absorbing capital into ion-exchange columns and selective-leaching reactors.

Metal Mining remains a capex priority as Beijing hedges against nickel and copper import dependence. Inner Mongolia’s 52,400 t molybdenum find and 591 Mt iron-ore discovery necessitate blast-hole drills and high-throughput crushers. The structural pivot to clean-tech inputs reshapes the China mining equipment market landscape, making multi-commodity adaptability a key OEM differentiator.

Geography Analysis

North China leads with 29.44% of domestic demand, buoyed by Inner Mongolia’s prolific ore discoveries and a CNY 750 million exploration push in 2025 [3]China Tungsten Industry Association, “Inner Mongolia Geological Budget 2025,” ctiwcn.com. Autonomous haul trials on the grasslands cut labor intensity and align with provincial carbon caps. Shanxi’s large fleet of intelligent mines acts as a showcase for AI controls, spurring spill-over investments in neighboring Hebei and Shaanxi.

Southwest China is forecast to accelerate at a 6.13% CAGR, propelled by Mianning-Dechang’s 250 kt world-class rare-earth cache. High-altitude porphyry copper on the Qinghai-Xizang Plateau adds 60 Mt of probable resources, requiring oxygen-enriched engines and weather-proof electrics. Breakthrough electro-kinetic recovery technology, born in Guangzhou, finds ideal pilot terrain here, raising equipment orders for HV-DC generators and electrode arrays.

East and South-Central China ride on battery-recycling imperatives, with new shredding-and-leaching lines serving 45% of global NEV retirements. Manufacturing hub proximity keeps lead times short, while port access supports component export. The Northeast sustains baseline demand through steel-basin revamps, and Northwest provinces tap Xinjiang’s autonomous dump-truck ecosystems for greenfield coal expansion. These region-specific vectors coalesce into a diversified demand matrix that underpins steady nationwide growth for the China mining equipment market.

Competitive Landscape

The market is moderately fragmented yet tilting toward consolidation as technological barriers rise. Domestic champions—Sany, XCMG, and Zoomlion—leverage deep government ties, vertically integrated supply chains, and high R&D intensity. Sany’s 300 t diesel-electric truck rollout signals upstream migration into ultra-class segments, while XCMG’s 120 kW hydrogen dump truck trims CO₂ by 99 kg per day, illustrating clean-fuel optionality.

Global majors respond with localization. Caterpillar maintains a 59.62% global machinery share and invests in Qingzhou for mid-range loader assembly. Komatsu partners with local universities on autonomous algorithms calibrated for Chinese strata conditions. Sandvik enhances its aftermarket presence via bonded warehouses in Tianjin, shortening parts lead times for underground drills.

White-space competition heats up in rare-earth separation lines and sensor suites. Domestic AI start-ups bundle machine vision with cloud analytics, wooing mines that lack in-house data science teams. International control-system vendors counter with safety-certified software stacks compatible with NEA guidelines. The interplay of scale economics, policy alignment, and IP depth defines the evolving power balance within the China mining equipment market.

China Mining Equipment Industry Leaders

Sany Heavy Equipment

Xuzhou Construction Machinery Group Co., Ltd. (XCMG)

Caterpillar Inc. (China)

Komatsu Ltd. (China)

Zoomlion Heavy Industry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Huaneng Group deployed 100 autonomous battery-electric trucks at the Yimin mine, harnessing Huawei 5G-Advanced to lift haul efficiency by 20%.

- July 2024: Sany Heavy Equipment launched the 300-t SET320S diesel-electric hybrid mining truck at its Shenyang plant.

- June 2024: XCMG introduced the EHSL552F hydrogen-fuel-cell dump truck featuring a 120 kW stack and high-power battery system.

- January 2024: Shandong Gold Group ordered a fleet of Epiroc drills and loaders for three domestic gold mines.

China Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening Machines |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Below 500 HP |

| 500 to 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining (Non-metallic) |

| Coal Mining |

| East China |

| North China |

| South-Central China |

| Northeast China |

| Southwest China |

| Northwest China |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening Machines | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output (HP) | Below 500 HP |

| 500 to 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining (Non-metallic) | |

| Coal Mining | |

| By Region (China) | East China |

| North China | |

| South-Central China | |

| Northeast China | |

| Southwest China | |

| Northwest China |

Key Questions Answered in the Report

What is the 2025 value of the China mining equipment market?

The market is valued at USD 33.78 billion in 2025.

How fast will demand for battery-electric mining trucks grow?

Battery-electric fleets are projected to post a 9.07% CAGR between 2025 and 2030.

Which segment holds the largest share of equipment demand?

Surface Mining Equipment accounts for 48.33% of 2024 revenue, reflecting the scale of open-pit operations.

Which region shows the highest growth outlook?

Southwest China is expected to expand at a 6.13% CAGR through 2030 due to its rare-earth project pipeline.

How significant is automation adoption?

Fully autonomous equipment is forecast to grow at an 8.24% CAGR, rapidly eroding manual fleet dominance.

Page last updated on: