United Kingdom Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.47 Billion |

| Market Size (2026) | USD 30.14 Billion |

| Market Size (2031) | USD 38.85 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

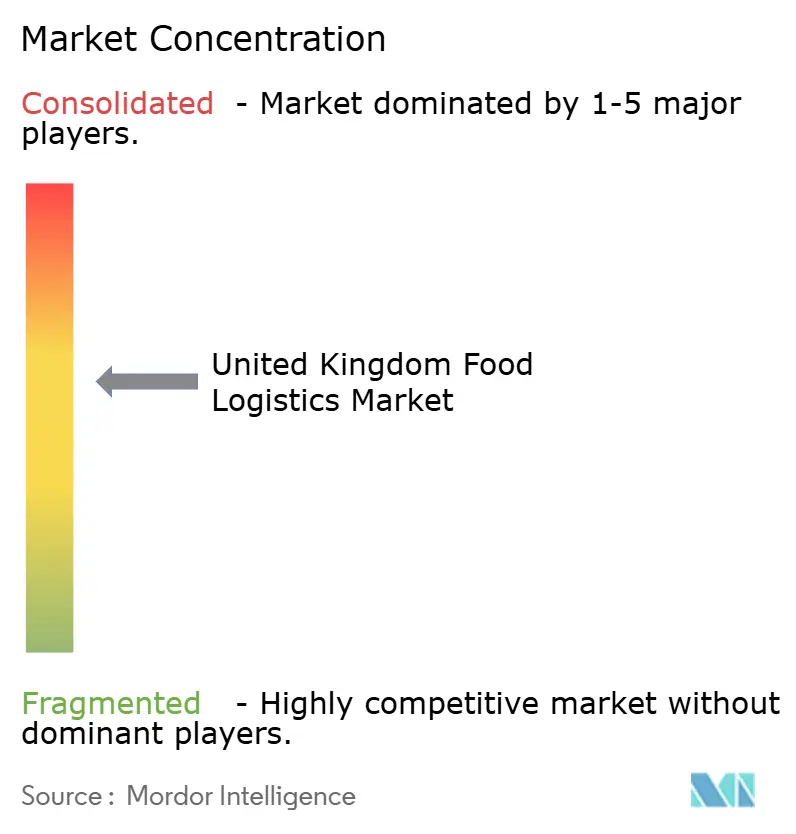

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Food Logistics Market Analysis by Mordor Intelligence

The United Kingdom food logistics market size was valued at USD 28.47 billion in 2025 and estimated to grow from USD 30.14 billion in 2026 to reach USD 38.85 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031).

Intermodal refrigerated transport along the Felixstowe–Midlands corridor, mandatory digital waste-tracking, and regional processing hubs funded by the government’s levelling-up program anchor this growth. Investments in predictive maintenance and insurer-driven temperature-compliance systems are widening the capability gap between technology-enabled operators and traditional hauliers[1]“Levelling Up Fund Prospectus,” HM Government, gov.uk. Rail-based cold chain expansion is beginning to divert long-distance volumes from road, while currency volatility and F-gas retrofits are reshaping cost structures. Overall, operators that combine data visibility, multimodal reach, and working-capital resilience are best placed to capitalize on export-oriented chilled food flows, premium pet-food demand, and rising pharmaceutical volumes.

Key Report Takeaways

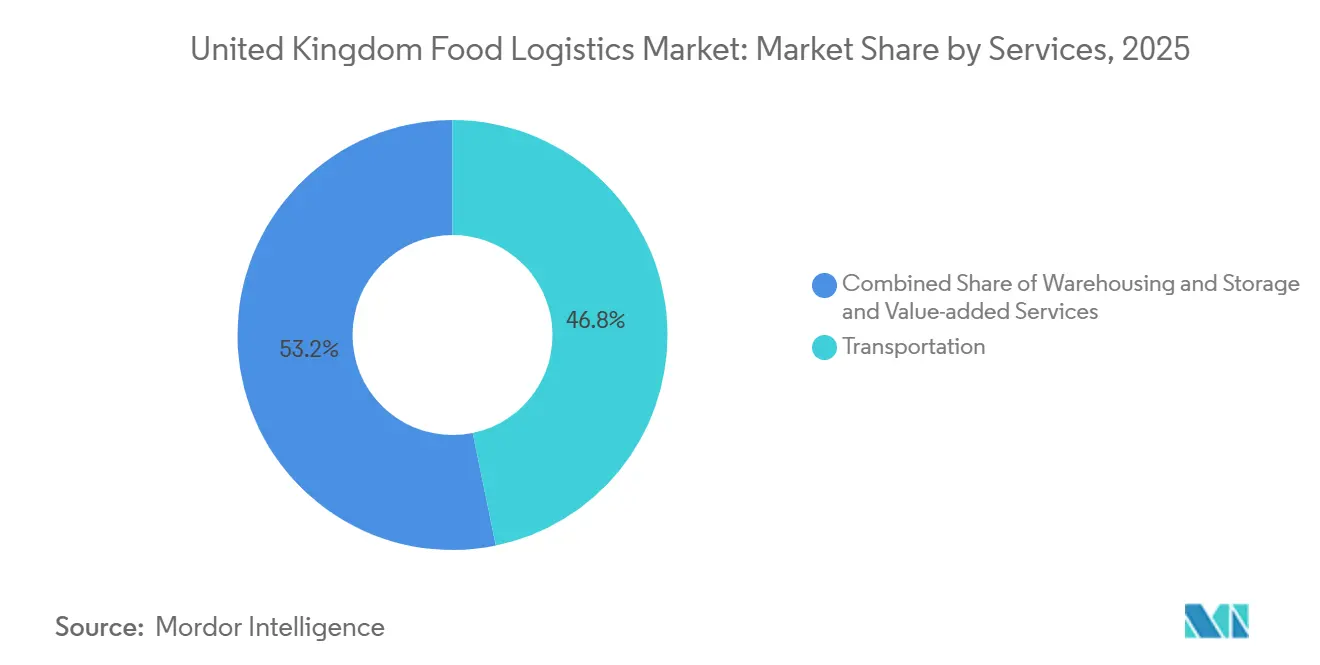

- By service type, transportation services led with 46.77% of the United Kingdom food logistics market share in 2025, while value-added services are projected to expand at a 7.78% CAGR through 2031.

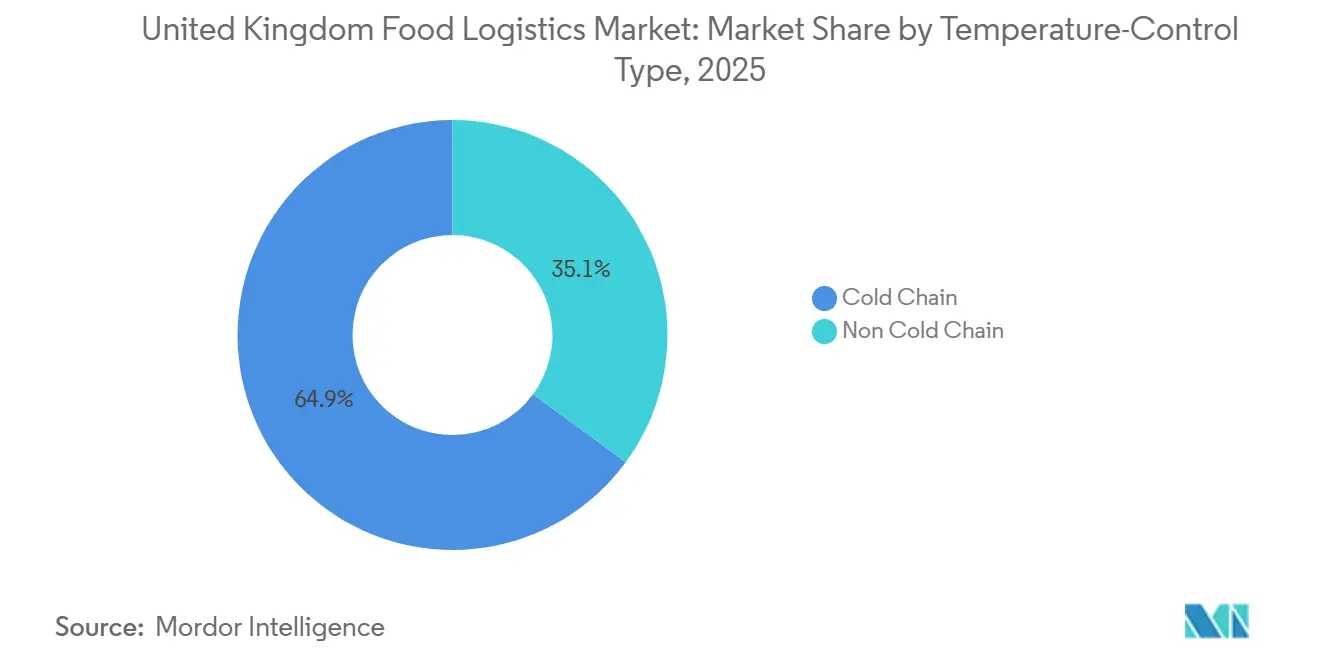

- By temperature-control type, cold chain operations commanded 64.92% of the United Kingdom food logistics market size in 2025 and are advancing at a 6.64% CAGR to 2031.

- By end-product category, dairy products and frozen desserts held 28.90% share in 2025, whereas pet-food logistics is forecast to grow at an 8.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-oriented chilled-food surge amplifying intermodal demand | +1.1% | National, focused on Felixstowe, Southampton, Dover corridors | Medium term (2-4 years) |

| Mandatory digital waste-tracking expanding reverse-logistics flows | +0.8% | London, Manchester, Birmingham metros | Short term (≤ 2 years) |

| Regional processing hubs under levelling-up agenda | +0.7% | Northeast England, Wales, Midlands | Long term (≥ 4 years) |

| Predictive-maintenance deployment for refrigerated assets | +0.6% | National | Short term (≤ 2 years) |

| Expansion of rail-based refrigeration on Felixstowe–Midlands corridor | +0.5% | East Anglia-Midlands-Northwest rail corridor | Medium term (2-4 years) |

| Insurer-led temperature-compliance requirements | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-Oriented Chilled-Food Surge Amplifying Intermodal Demand

Record dairy export volumes in 2025 accompanied a double-digit rise in chilled meat and ready-to-eat products moving to Asia-Pacific markets, driving incremental demand for temperature-controlled containers and rail access to deep-water ports. Chilled items require tighter 2-8 °C windows and shorter transit times than frozen cargo, which pushes shippers toward integrated road–rail solutions that cut end-to-end journeys by up to 12 hours. GB Railfreight’s dedicated reefer services on the Felixstowe–Midlands spine illustrate how rail captures long-haul volumes once carbon abatements and fuel savings are quantified. Exporters gain sustainability credentials as modal shift cuts 76% of associated emissions. However, widespread take-up relies on a larger refrigerated wagon fleet and automated container-tracking to pre-empt temperature excursions.

Mandatory Digital Waste-Tracking Expanding Reverse-Logistics Flows

Compulsory food-waste reporting from April 2025 has formalized reverse-logistics requirements for every major grocer and food-service player. Separate household food-waste collection mandated by March 2026 is adding collection routes that mirror forward distribution lanes, boosting fleet utilization. Retailers such as Tesco now pair last-mile deliveries with surplus pick-ups, routing them to redistribution NGOs aided by QR-coded data trails. Operators with mixed-load refrigerated vans and API-linked scheduling tools can turn what was once empty back-haul into a revenue-generating service, trimming emissions and securing regulatory credits. Early adopters enjoy first-mover advantage as compliance audits increasingly demand end-to-end digital visibility.

Regional Processing Hubs under Levelling-Up Agenda Boosting Mid-Mile Reefer Routes

A GBP 4.8 billion infrastructure fund is pushing new cold stores and food factories into Northeast England, Wales, and the Midlands, decentralizing flows historically centered on the South-East[2]“National Infrastructure Strategy,” HM Treasury, gov.uk. The North-East food cluster alone attracted GBP 250 million (USD 335 million) in fresh capital through 2025, creating demand for reefer shuttles linking farms, processors, and urban DCs. Logistics providers that can flex vehicles, drivers, and depot capacity into secondary cities gain access to new contract volumes and lower-cost warehouse space. Culina Group’s cold-store in Darlington demonstrates how scaling ahead of regional demand locks in occupancy and underpins multi-year service agreements. While the hubs ease congestion in the South-East, they also require IT platforms that orchestrate multi-node inventory and dynamic pick-ups across fragmented production bases.

Predictive-Maintenance Deployment for Refrigerated Assets Cutting Downtime

Sensor-based maintenance now covers trailer units, compressors, and dock doors, flagging anomalies before a temperature breach risks load rejection. Industry benchmarking shows predictive programs cut unplanned downtime 30-40% versus run-to-fail approaches. Supply Chain trimmed repair costs 25% across its United Kingdom reefer fleet during 2025 after feeding telematics data into machine-learning algorithms. Carriers achieving sub-1 °C variance and 99% on-time delivery now secure premium contracts with exporters and pharma majors. The investment hurdle sensors, cloud analytics, and technician retraining tilt the playing field toward large operators, accelerating consolidation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening F-gas and ammonia rules inflating retrofit costs | -0.7% | National, older warehouses | Medium term (2-4 years) |

| Shortage of refrigerated rail wagons limiting modal shift | -0.5% | Key intermodal corridors | Short term (≤ 2 years) |

| Currency volatility elevating fuel and equipment import costs | -0.4% | National | Short term (≤ 2 years) |

| Rising SME haulier insolvencies linked to customs cash-flow stress | -0.3% | National, export routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening F-Gas and Ammonia Regulations Inflating Cold-Store Retrofit Costs

HFC quotas fall 79% by 2030, forcing two-thirds of the United Kingdom cold stores still running legacy refrigerants to retrofit or replace systems at USD 0.6-2.5 million per site. Ammonia and CO₂ designs slash energy bills but require leak-detection, ventilation upgrades, and skilled engineers[3]“Technical Resources,” Institute of Refrigeration, ior.org.uk. For cash-constrained independents the capex outlay is prohibitive, incentivizing sale-and-leaseback deals with REITs such as Lineage Logistics that bundle financing, build, and long-term operating contracts.

Shortage of Refrigerated Rail Wagons Constraining Modal-Shift Capacity

Only 450 reefers exist in the national wagon pool versus latent demand of 1,200, so GB Railfreight’s Felixstowe reefer service runs at capacity with multi-week waiting lists. New builds cost up to USD 0.32 million each and need 18-24 months lead time, delaying modal switch despite 15-20% operating cost savings over diesel road moves. Without leasing schemes or manufacturer ramp-ups, modal share gains will stall and keep long-haul carbon footprints stubbornly high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Capabilities Redefine Profit Pools

In service type, transportation commanded 46.77% of the United Kingdom food logistics market share in 2025. Road remains indispensable for last-mile coverage, but labor shortages and diesel costs compress margins, steering operators toward higher-yield ancillary work. Value-added services such as blast freezing, inventory management, co-packing, and organised reverse-logistics are on track for a 7.78% CAGR, almost 2 percentage points above the overall United Kingdom food logistics market CAGR. Clients reward providers capable of native WMS-TMS integration, SKU-level visibility, and multi-temperature order assembly. Sea and inland-water moves tie closely to port-centric chill-tunnel storage, while rail’s share inches forward on intermodal corridors once capacity bottlenecks ease.

Automation is the performance equalizer. NewCold’s automated AS/RS facility in Wakefield lifts pallet-throughput per square meter 40% above manual designs, compressing energy per unit handled and meeting near-zero-touch safety protocols. As supermarkets renew logistics tenders, bundled contracts that fuse transport, warehousing, and compliance reporting beat siloed offerings[4]“Industrial Strategy: Automation and Data Economy,” HM Government, gov.uk. DFDS Logistics illustrates the pivot: cross-dock redesigns now include blast-freezers, order-assembly robots, and RFID-enabled waste-capture gates. Over the forecast horizon, earnings growth will be skewed toward fleets that convert traditional “haul and store” models into data-rich, compliance-embedded service platforms.

By Temperature-Control Type: Cold Chain Stays Core Amid Tech-Driven Upgrades

Cold chain activities accounted for 64.92% of the United Kingdom food logistics market size in 2025 and are forecast to expand at 6.64%, outpacing the non-cold segment even after retrofit headwinds. Frozen storage currently dominates volume, yet chilled products tied to fresh meat, dairy, and biologics build momentum as export markets and prepared-meal demand climb. Energy-optimization pilots that operate frozen rooms closer to -15 °C rather than -18 °C cut power bills 10% with no food-safety sacrifice. Ambient-controlled units targeting chocolate and wine balance the portfolio, offering margin cushioning when refrigeration prices surge.

Predictive maintenance enhances uptime: DHL’s 8-percentage-point rise in on-time delivery since deploying analytics underscores the stakes in temperature assurance. At the premium tier, real-time blockchain logging satisfies insurers and pharma GMP audits, letting carriers bill 20-30% more per lane hour. The United Kingdom food logistics market size attributable to cold chain services is led by equipment upgrades, energy-efficient refrigerants, and audit-ready data platforms.

By End-Product Category: Pet-Food Outperformance Relies on Refrigerated Diets

Dairy and frozen desserts anchored 28.90% of the United Kingdom food logistics market share in 2025, leveraging stable household demand and outbound cheese exports to Asia. Yet pet-food logistics, once an ambient afterthought, is racing ahead at an 8.07% CAGR as owners shift toward raw and chilled formulations requiring the same cold-chain fidelity as human meals. Kammac’s dedicated pet-food network demonstrates category-specific protocols, separate hygiene zones, rapid thaw prevention, and allergen segregation that command premium fees.

Meat, seafood, and poultry volumes ride chilled shelf-life gains as ultra-low-oxygen packaging extends domestic delivery windows. Horticulture remains seasonal; greenhouse expansion and controlled-environment agriculture may temper import reliance, but will not erase the 47% fruit-deficit gap before 2031. Processed foods and functional ingredients hold steady, their growth tethered to convenience diets and fitness-led fortification trends.

Geography Analysis

Southeast England retains the largest slice of the United Kingdom food logistics market share, thanks to London’s consumption density and the twin gateways at Felixstowe and Dover, handling 40% of container flows. Lineage Logistics’ automated cold stores in Essex and Kent shorten inland drayage and slash port dwell times, enabling importers to move pallets from ship-side to outbound lorry in under two hours. However, congestion, land scarcity, and premium real-estate costs are nudging providers toward the Midlands triangle of Birmingham, Nottingham, and Leicester, where property is up to 35% cheaper and offers “Goldilocks” reach to both northern and southern metro zones.

The Midlands has become the intermodal linchpin of the United Kingdom food logistics market, hosting GB Railfreight’s flagship reefer shuttle that trims 162 road miles off a typical Felixstowe-Manchester move. Regional processing incentives under the leveling-up program accelerate this re-centering: new meat-processing plants in Derbyshire and dairy fillers in Shropshire divert volumes once consolidated in the South-East. Northern England, meanwhile, is moving from peripheral to priority status. Investments of GBP 250 million (USD 335 million) across Tyne & Wear cold storage and packaging projects through 2025 promise a jump in mid-mile reefer lanes bridging farms, factories, and city depots.

Scotland’s salmon exports and Wales’ meat processors inject additional cross-border traffic. DFDS’s Liverpool-Belfast ferry corridors and Kuehne+Nagel’s Irish Sea links underpin temperature-assured flows into Northern Ireland, where grace-period customs arrangements still require EU-compliant phytosanitary checks. As rail capacity scales and regional hubs multiply, a more balanced geographic footprint is expected to emerge, mitigating over-reliance on South-East nodes and spreading infrastructure risk.

Competitive Landscape

Competition inside the United Kingdom food logistics market is shaped by a dual track of consolidation and technology differentiation. DHL Group, GXO Logistics, and Lineage Logistics leverage IoT-monitored fleets, automated warehouses, and blockchain audit trails to promise 99% temperature integrity, positioning themselves for premium, penalty-sensitive contracts. CEVA’s takeover of Wincanton and DSV’s acquisition of DB Schenker expand multimodal reach, giving customers one-stop contracts covering road, rail, sea, and air moves with a single KPI dashboard. The combined entities now negotiate long-run power-purchase agreements and build vertical solar arrays over chill docks to buffer energy costs.

Mid-tier specialists defend their niches. Culina Group concentrates on regional density rather than global scale, locating cold stores next to emerging processors, which cuts empty back-hauls and speeds farm-to-fork cycles. Turners (Soham) invests in battery-electric reefers to navigate city‐center emission zones due in 2027, courting supermarkets that face steep fines for diesel deliveries. Railfreight-led challengers such as Newell and Wright partner with GB Railfreight to co-fund reefer wagons, carving a sustainability wedge against diesel-only rivals.

The barriers to entry are climbing. F-gas retrofits, insurer-mandated monitoring, and 24/7 data compliance raise capex thresholds beyond the reach of many SME hauliers already squeezed by 60-day payment terms. Private-equity funds eye distressed cold-store assets for roll-up plays, betting that scale will unlock lower energy tariffs and bank credit lines. Meanwhile, digital freight start-ups pivot toward asset-light coordination layers, acknowledging that owning and maintaining temperature-controlled infrastructure remains capital intensive and regulation heavy.

United Kingdom Food Logistics Industry Leaders

DHL Group

GXO Logistics

Culina Group

Seafrigo Group

Turners (Soham) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GXO Logistics extended its NHS England contract to handle distribution of bowel-cancer home-testing kits, underscoring the firm’s capability in regulated temperature-controlled healthcare flows.

- July 2025: DHL Supply Chain reported an 8 percentage-point improvement in on-time delivery after scaling predictive-maintenance algorithms across its United Kingdom reefer fleet.

- April 2025: DPD UK unveiled an 8,000-locker rollout to enhance out-of-home parcel fulfilment, indirectly easing final-mile congestion for grocery e-commerce.

- April 2025: Lineage Logistics acquired three Bellingham Cold Storage warehouses, adding 24 million ft³ and 85,000 pallet slots to its United Kingdom network.

United Kingdom Food Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Water | |

| Air | |

| Warehousing and Storage | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat, Seafood, and Poultry |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) |

| Horticulture (Fresh Fruits and Vegetables) |

| Processed Food Products |

| Pet Food |

| Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.) |

| By Services | Transportation | Road |

| Rail | ||

| Sea and Inland Water | ||

| Air | ||

| Warehousing and Storage | ||

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat, Seafood, and Poultry | |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) | ||

| Horticulture (Fresh Fruits and Vegetables) | ||

| Processed Food Products | ||

| Pet Food | ||

| Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.) | ||

Key Questions Answered in the Report

How big will chilled-food exports become by 2031?

Rising demand from Asia-Pacific markets and expanded rail-port connectivity position chilled goods to remain the fastest-growing export flow, helping lift the United Kingdom food logistics market size to USD 38.85 billion by 2031.

What segment offers the highest growth opportunity for service providers?

Value-added services such as blast freezing, inventory management, and reverse logistics are forecast to grow at 7.78% CAGR, outpacing basic transportation.

Why is the pet-food category attracting cold-chain investment?

Premium raw and chilled formulations need the same 2-8 °C integrity as human meals, pushing pet-food logistics to an 8.07% CAGR and incentivizing dedicated reefer capacity.

Will rail overtake road for long-haul food moves?

Rail will gain share on corridors like Felixstowe–Midlands once the refrigerated wagon fleet expands, but road will still dominate last-mile and regional hauls through 2031.

How are insurers influencing cold-chain standards?

Stricter underwriting now demands real-time temperature logging and blockchain auditable records, allowing compliant carriers to command 20-30% rate premiums.

What is the biggest regulatory cost pressure facing operators?

The phasedown of HFC refrigerants under F-gas rules is forcing USD 0.6-2.5 million retrofits per cold store, especially impacting older facilities.

Page last updated on: