South Korea Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

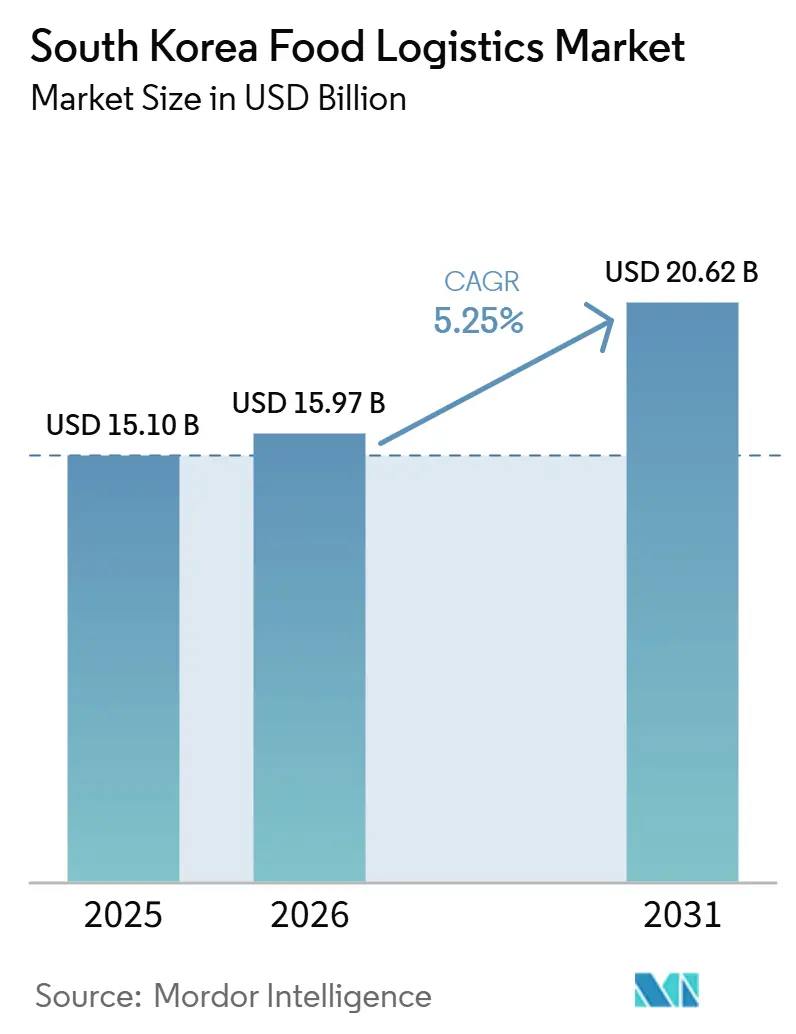

| Base Year Market Size (2025) | USD 15.10 Billion |

| Market Size (2026) | USD 15.97 Billion |

| Market Size (2031) | USD 20.62 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

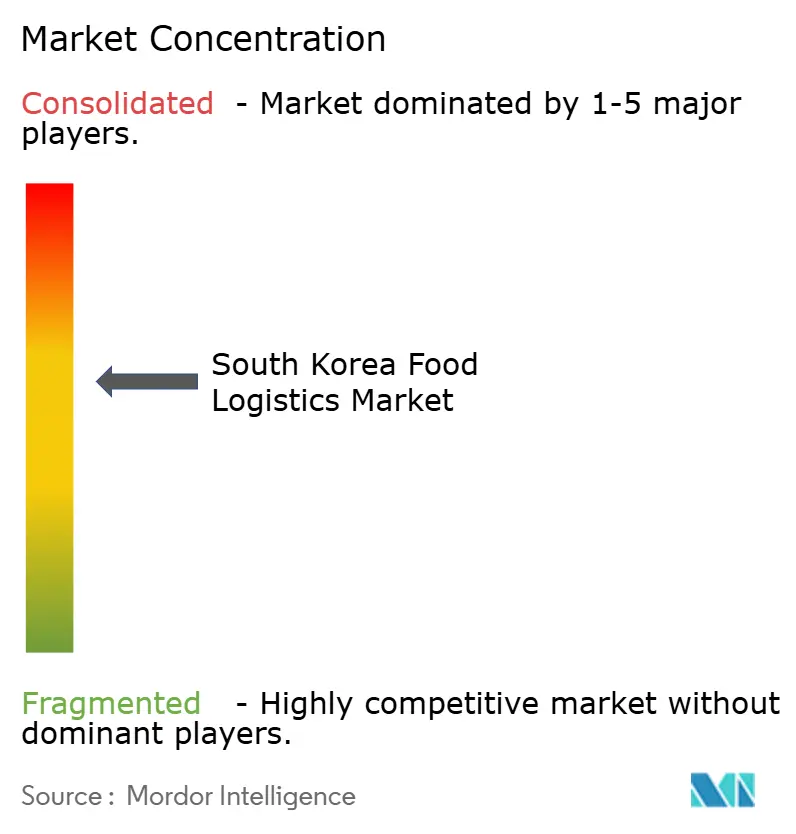

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Food Logistics Market Analysis by Mordor Intelligence

The South Korea food logistics market size was valued at USD 15.10 billion in 2025 and estimated to grow from USD 15.97 billion in 2026 to reach USD 20.62 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

Digital traceability mandates, GDP-level temperature standards, and energy-efficient retrofits collectively widen the value pool, while brownfield redevelopment releases scarce urban capacity that greenfield projects struggle to secure. Intermodal rail reefer services lower long-haul costs by up to 30%, supporting volume shifts along the Busan–Seoul corridor. Shippers increasingly pay premiums for blast freezing, inventory management, and AI-enabled monitoring, signaling a move away from commoditized freight rates. Incumbents such as CJ Logistics and LX Pantos leverage legacy infrastructure to defend share, yet technology-led entrants attack last-mile niches through micro-fulfillment hubs and subscription delivery models.

Key Report Takeaways

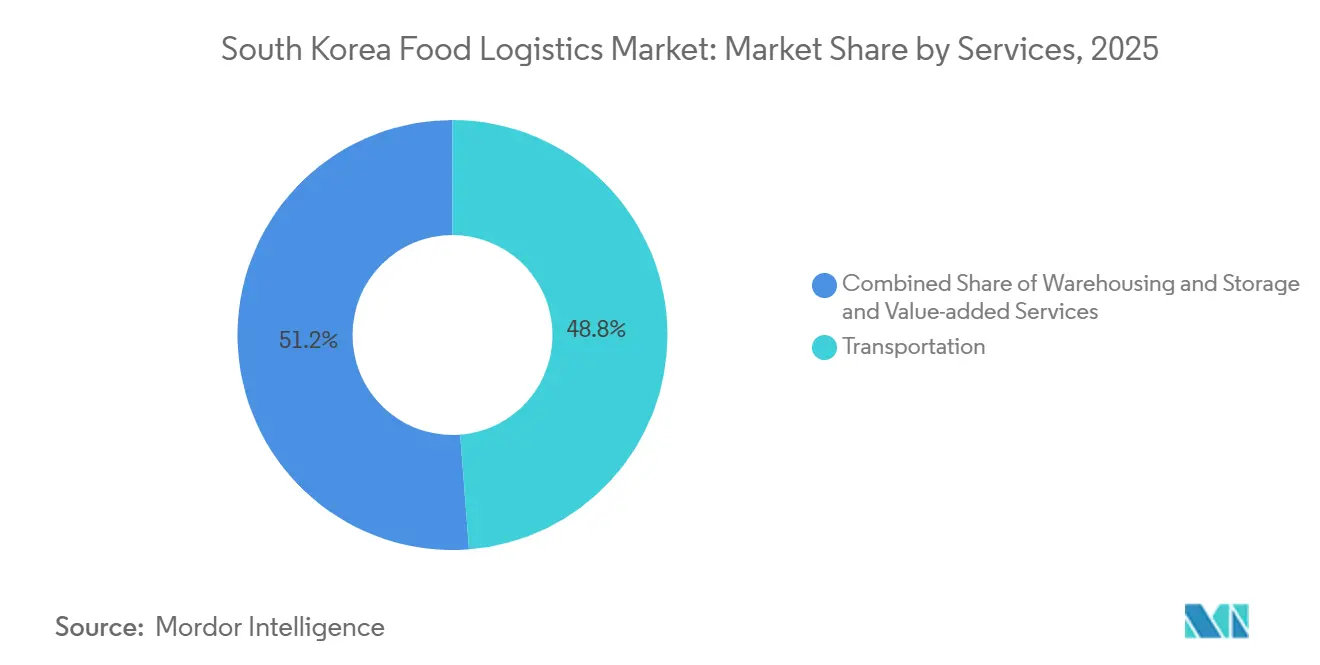

- By services, transportation accounted for 48.77% of the South Korea food logistics market share in 2025, whereas value-added offerings are projected to expand at a 7.81% CAGR through 2031.

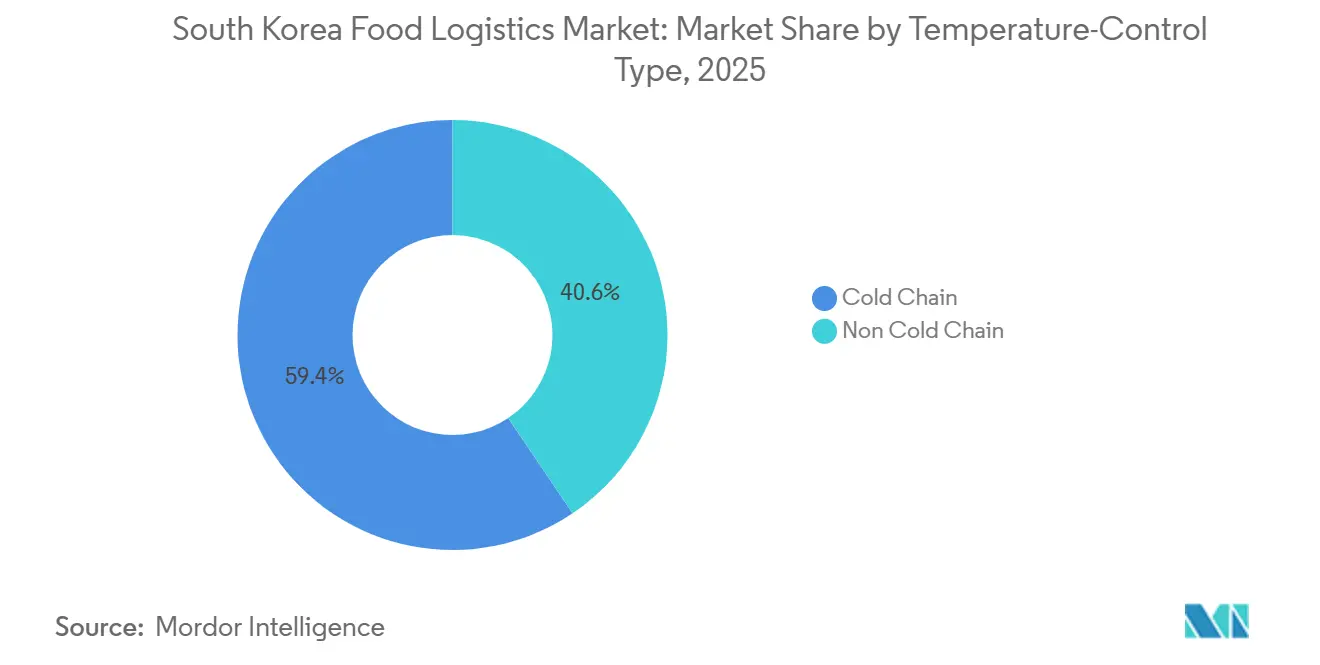

- By temperature-control type, cold chain operations commanded 59.43% of the South Korea food logistics market size in 2025 and are advancing at a 6.68% CAGR through 2031.

- By end-product category, meat, seafood, and poultry led with 26.42% of volumes in 2025, while pet food logistics posted the fastest 8.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Blockchain-Based Cold-Chain Documentation | +0.9% | National, early adoption in pharma-food zones | Medium term (2-4 years) |

| Growth of Pharma-Grade Storage Standards Influencing Food Logistics | +1.1% | Seoul, Busan, and Incheon metropolitan areas | Long term (≥ 4 years) |

| Rising Energy-Efficiency Retrofits in Refrigerated Fleets & Warehouses | +0.7% | National, focused on industrial complexes | Medium term (2-4 years) |

| Urban Brownfield Redevelopment Unlocking Sites for Logistics Hubs | +0.6% | Seoul, Incheon, Daegu urban cores | Long term (≥ 4 years) |

| Expansion of Intermodal Rail Refrigerated Services | +0.5% | Busan–Seoul corridor, secondary city links | Long term (≥ 4 years) |

| Insurance-Driven Upgrades from Heightened Consumer Litigation Risk | +0.8% | National, high-value food segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration of Blockchain-Based Cold-Chain Documentation

Distributed ledger platforms record immutable temperature and location data that satisfy audits and liability insurance conditions. The Ministry of Food and Drug Safety encourages blockchain for high-risk categories, replacing vulnerable paper logs and cutting insurance premiums by 30-40% for compliant operators. CJ Logistics links blockchain modules to its warehouse management system, creating a unified traceability layer from farm to retailer. Importers of premium seafood and organic produce benefit most because provenance verification commands shelf-price uplifts that offset hardware and integration costs. Smaller carriers struggle with legacy IT stacks that lack open APIs, widening the capability gap and prompting consolidation. Over the medium term, real-time ledger data is expected to become a prerequisite for high-value contract renewals, embedding blockchain deep into the South Korea food logistics market[1]Ministry of Food and Drug Safety, “Blockchain Traceability Pilot,” mfds.go.kr.

Growth of Pharma-Grade Storage Standards Influencing Food Logistics

Good Distribution Practice protocols migrate from pharmaceuticals into premium foods as nutraceuticals blur category lines. GDP-compliant warehouses require temperature mapping, validated transport lanes, and deviation management, adding 15-20% to operating costs yet enabling 25-30% price premiums. DHL leverages its GDP infrastructure to secure ultra-low-temperature food contracts, extending pharma skill sets to functional foods. Domestic providers retrofit sensors and automated alerts to match multinational benchmarks and avoid customer defection. Certified capacity remains undersupplied, allowing early movers to lock in multi-year agreements. Over the long term, GDP standards will likely delineate a premium tier within the South Korea food logistics market, concentrating margins among compliant players.

Rising Energy-Efficiency Retrofits in Refrigerated Fleets & Warehouses

Industrial electricity prices rose 18% between 2024 and 2025, making energy the second-largest expense after labor for cold storage facilities. Operators install ammonia-based natural refrigerants, LED lighting, and AI-guided compressor controls that trim consumption by up to 35% without product risk. Variable-speed drives deliver paybacks within 18 months at current tariffs, prompting national-scale rollout aided by government subsidies covering 20-30% of capital outlay. Energy passports have emerged as tender prerequisites, making retrofits a revenue enabler rather than a cost center. Medium-term gains include lower carbon taxes and improved ESG rankings, elements that sway multinational food manufacturers when awarding South Korea food logistics market contracts[2]Korea Energy Economics Institute, “Industrial Electricity Rate Analysis 2024-2025,” keei.re.k.

Urban Brownfield Redevelopment Unlocking Sites for Logistics Hubs

Municipal authorities fast-track permits and offer tax credits for converting dormant industrial parcels into multistory cold stores, easing inner-city land shortages. Land acquisition costs fall 30-40% versus greenfield, though remediation adds complexity and raises financing hurdles. LX Pantos’ New Port Eco Logistics Center exemplifies the model with a vertical design that triples cubic utilization on a restricted footprint. Automated storage and retrieval systems compensate for height-induced handling challenges and support 24/7 fulfillment. Long-term impact will be measured in reduced last-mile mileage and faster e-grocery delivery, two decisive KPIs for the South Korea food logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile LNG and Electricity Prices Escalating Cold-Storage OPEX | -1.2% | National, energy-intensive facilities | Short term (≤ 2 years) |

| Heightened Customs Inspection Delays for Animal-Origin Goods | -0.7% | Busan, Incheon ports, and air cargo terminals | Medium term (2-4 years) |

| Limited Availability of Urban Land Zoned for Refrigerated Facilities | -0.9% | Seoul, Busan, and Incheon metropolitan areas | Long term (≥ 4 years) |

| Aging Refrigeration Infrastructure Causing High Maintenance Downtime | -0.6% | National, facilities over 15 years old | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile LNG and Electricity Prices Escalating Cold-Storage OPEX

South Korea’s heavy reliance on imported LNG exposes domestic electricity tariffs to global spot price shocks, with 2024-2025 fluctuations reaching 300-400%. A 5,000 m² cold store consuming 10 MWh daily experiences monthly bill swings of USD 50,000-80,000, complicating contract pricing and cash-flow planning. Operators resort to temporary energy surcharges that erode customer loyalty, while fixed-price contracts compress margins during spikes. On-site solar and battery systems mitigate volatility but require 5-7 year paybacks that strain smaller balance sheets. Persistent price swings may accelerate consolidation as undercapitalized firms exit the South Korea food logistics market.

Heightened Customs Inspection Delays for Animal-Origin Goods

To guard against zoonotic outbreaks, the Animal and Plant Quarantine Agency increased physical inspection rates for meat and seafood shipments to 40-50%, extending dwell times by 18-24 hours. Importers absorb higher spoilage risks and expand safety stocks, lifting total landed costs 8-12%. Logistics providers build chilled holding zones at ports to preserve cargo quality during the wait, yet those assets generate no revenue. Air-freighted tuna and chilled pork suffer disproportionate quality decay, prompting some shippers to re-route through alternative gateways, which diffuses but does not eliminate the bottleneck. Medium-term, digital pre-clearance programs may shorten queues, although full deployment lies beyond the current forecast window[3]Animal and Plant Quarantine Agency, “Inspection Procedures for Animal Products,” qia.go.kr.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Value-Added Expertise Redefines Profit Pools

Value-added services are projected to expand at a 7.81% CAGR, while transportation accounted for 48.77% of South Korea food logistics market share, though its dominance is gradually being eroded. Shippers increasingly pay premiums for services such as blast freezing, relabeling, and inventory visibility, as these deliver significantly higher margins than core transport. Road freight continues to dominate short-distance, intra-provincial distribution, while rail gains traction on longer routes where cost efficiencies offset scheduling rigidity. Sea freight remains the backbone for bulk imports through major ports, supported by specialized cold-chain vessels serving regional trade lanes. Air freight remains a niche option for high-value perishables, justified by substantially higher pricing.

Meanwhile, warehousing is evolving through automation technologies like AS/RS, improving efficiency, accuracy, and scalability in line with e-grocery demands. As logistics providers bundle multimodal transport with packaging and quality control, competition is shifting from price-driven models to reliability and integrated service delivery. This transformation is expanding the high-value segment of the South Korea food logistics market, raising entry barriers due to the need for both infrastructure and advanced data capabilities.

By Temperature-Control Type: Cold Chain Captures Premium Volume

Cold chain services controlled 59.43% of South Korea food logistics market size and will compound at 6.68% through 2031 as consumer preference shifts toward fresh, functional, and minimally processed foods. Frozen storage below 0 °C grows fastest thanks to rising imported seafood and processed meat volumes that demand ultra-low temperatures. Chilled zones between 2-8 °C handle dairy and fresh produce, with GDP-compliant sites fetching 25-30% rate premiums, thereby expanding the South Korea food logistics market size for certified capacity. Ambient temperature-controlled ranges (15-25 °C) remain important for confectionery and beverages but gradually concede share to chilled categories as retailers elevate quality standards. Blockchain-verified temperature logs become table stakes in premium segments, locking out firms without sensor-rich fleets. Operators differentiate via redundant power, validated mapping, and rapid deviation response, elements that influence insurer assessments and contract renewals. Non-cold chain lanes still move shelf-stable staples; however, margin potential concentrates in high-spec cold chain corridors.

As nutraceuticals and functional beverages proliferate, hybrid storage zones capable of frequent temperature set-point changes gain favor. Facility design thus prioritizes modularity and energy efficiency to manage mix volatility. Over time, integrated cold chain networks will constitute the backbone of South Korea's food logistics market infrastructure, leaving ambient carriers vulnerable unless they invest in refrigeration retrofits.

By End-Product Category: Pet Food Outpaces Core Protein Segments

Meat, seafood, and poultry captured 26.42% of 2025 tonnage, reflecting Korea’s protein-rich diet and high import dependency. Nonetheless, pet food is the fastest mover, expanding at 8.10% CAGR as ownership rates climb and regulatory bans on dog-meat consumption redirect spending toward premium kibble. Import volumes of North American and European brands surged 45% in 2025, requiring allergen-segregated storage and lot-level traceability, services that command fees above human-food equivalents. Dairy logistics ride increased cheese and ice-cream popularity among millennials, while horticulture chains rely on sophisticated ripening and humidity controls to satisfy year-round fruit availability. Processed staples remain stable beneficiaries of long shelf life and ambient lanes that cut logistics cost per kilogram[4]United States Department of Agriculture Foreign Agricultural Service, “Korea Pet Food Market Update,” fas.usda.gov.

“Others,” encompassing sauces, condiments, and functional powders, gain traction as Korean cuisine globalizes and domestic palates diversify. Providers capable of multi-temperature handling and rapid SKU switching edge as product variety balloons. Pet food’s rise spotlights a broader premiumization wave that feeds directly into demand for certified cold chain services, reinforcing the value-added narrative within the South Korea food logistics market.

Geography Analysis

South Korea’s compact landmass channels 85% of reefer imports through Busan and Incheon, creating dominant coastal nodes that feed national distribution. The Seoul metro region absorbs roughly half of imported perishables despite encompassing only a quarter of the land, elevating urban congestion and heightening the value of inner-city cold space. Brownfield conversions in Seoul and Incheon mitigate land scarcity, yet capacity still lags demand, prompting secondary hubs in Daegu, Gwangju, and Daejeon. These inland centers shorten lead times to provincial retailers and relieve pressure on the capital’s highways, though volume thresholds must be met to justify dedicated cold investment.

Gangwon Province emerges as a lower-cost alternative with upgraded highway links to Seoul, drawing developers attracted by 30% cheaper land and municipal tax incentives. Jeju’s insular location necessitates multimodal air-sea chains that inflate logistics costs and dampen consumption unless high tourist flows warrant the premium. Busan’s customs infrastructure processes reefer cargo faster than smaller ports; however, policy harmonization underway at the Korea Customs Service aims to equalize dwell times nationwide by 2028. Urban emissions caps phase out older diesel trucks, compelling operators to adopt electric vans and night deliveries that raise operating costs but cut congestion.

Mountainous terrain funnels freight along limited arterial highways, making any incident a national bottleneck. The 2024 port strike that sidelined 40% of reefer capacity underscored the concentration risk within the South Korea food logistics market. Consequently, public policy now encourages rail and coastal shipping diversification to buffer future shocks. Regional investment incentives tilt fresh capital toward undeveloped provinces, yet talent shortages and lower shipment density remain practical hurdles. Overall, geography dictates that resilient, multimodal networks are indispensable for nationwide cold chain integrity.

Competitive Landscape

The South Korea food logistics market is moderately fragmented, with domestic chaebols and global specialists carving out distinct niches. CJ Logistics leads through nationwide infrastructure and in-house AI that optimizes inventory placement and robot pick sequences. LX Pantos expands intermodal breadth via alliances with ocean carriers and Korail, knitting sea-rail-road flows that lower emissions and cost. International players DHL, Kuehne + Nagel, and Nippon Express focus on cross-border pharmaceutical and premium food lanes, where GDP credentials and global reach justify premium fees.

Technology acts as the critical differentiator. Predictive analytics pre-empt temperature excursions, while blockchain platforms provide audit-grade traceability, both prerequisites for high-value contracts. Energy-efficient retrofits also shape competitiveness, because lower kilowatt-hours per pallet allow providers to offer longer fixed-price agreements in an era of tariff volatility. Smaller family-owned warehouses grapple with the capital burden of modern refrigeration and cyber-secure IT, making them acquisition targets for deep-pocketed players seeking city-center footprints.

Strategic moves include CJ Logistics’ rollout of a cube-based AS/RS at Incheon that handles 650 bins per hour and Boxlinks’ investment in reefer containers that underpin rail corridor expansion. On the service side, subscription-based everyday delivery models test micro-fulfillment viability for chilled groceries. ESG pressures encourage partnerships with renewable-energy developers to cut scope 2 emissions, another emerging tender criterion. Over the forecast period, competitive advantage will spring from the ability to fuse physical assets with digital orchestration, guaranteeing transparency, compliance, and sustainability for multinational food and pet-nutrition brands active in the South Korea food logistics market.

South Korea Food Logistics Industry Leaders

CJ Logistics Co., Ltd.

Lotte Global Logistics

Hyundai Glovis

Hanjin Transportation

Coupang Fulfilment & Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LX Pantos acquired a large logistics center in Katowice, Poland (109,000 m²), aimed at supporting European operations and Korean exporters.

- October 2025: CJ Logistics signed a win win financial partnership with Hyundai Commercial to develop exclusive financial products for vehicle owners and logistics partners, including support for the logistics broker platform “The Unban.”

- April 2025: CJ Logistics launch of “THE FULFILL”: Introduced a unified fulfillment solution covering inbound to outbound logistics, including tailored structures for fresh food and cold chain segments as part of broader service enhancements.

- February 2025: LX Pantos secured a massive logistics facility (~142,852 m²) in Incheon to strengthen e commerce logistics footprint.

South Korea Food Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Water | |

| Air | |

| Warehousing and Storage | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat, Seafood, and Poultry |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) |

| Horticulture (Fresh Fruits and Vegetables) |

| Processed Food Products |

| Pet Food |

| Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.) |

| By Services | Transportation | Road |

| Rail | ||

| Sea and Inland Water | ||

| Air | ||

| Warehousing and Storage | ||

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat, Seafood, and Poultry | |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) | ||

| Horticulture (Fresh Fruits and Vegetables) | ||

| Processed Food Products | ||

| Pet Food | ||

| Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.) | ||

Key Questions Answered in the Report

What CAGR is projected for South Korea food logistics during 2026-2031?

The sector is forecast to grow at a 5.25% CAGR, with value rising from USD 15.97 billion in 2026 to USD 20.62 billion by 2031.

Which service category is expanding fastest in South Korea food logistics?

Value-added offerings such as blast freezing, relabeling, and inventory management post the highest growth at a 7.81% CAGR through 2031.

Why are GDP storage standards gaining traction in Korean cold chains?

Functional foods and nutraceuticals blur lines with pharmaceuticals, so shippers now pay 25-30% price premiums for GDP-compliant temperature control and traceability.

How do rising energy costs affect investment decisions for cold storage operators?

An 18% jump in industrial power tariffs between 2024 and 2025 accelerates retrofits AI-managed compressors, natural refrigerants, and LED lighting, that cut electricity use up to 35%.

Which regions beyond Seoul present viable expansion sites for refrigerated warehousing?

Provinces such as Gangwon and inland cities like Daegu and Daejeon offer lower land costs and new tax incentives, though they require sufficient shipment density to justify builds.

Which technology investments most strengthen competitive positions today?

Blockchain traceability, warehouse AI, and IoT temperature sensors allow providers to secure insurer approvals, command premium rates, and win long-term contracts from high-value food brands.

Page last updated on: