France Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 26.03 Billion |

| Market Size (2026) | USD 27.37 Billion |

| Market Size (2031) | USD 34.81 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

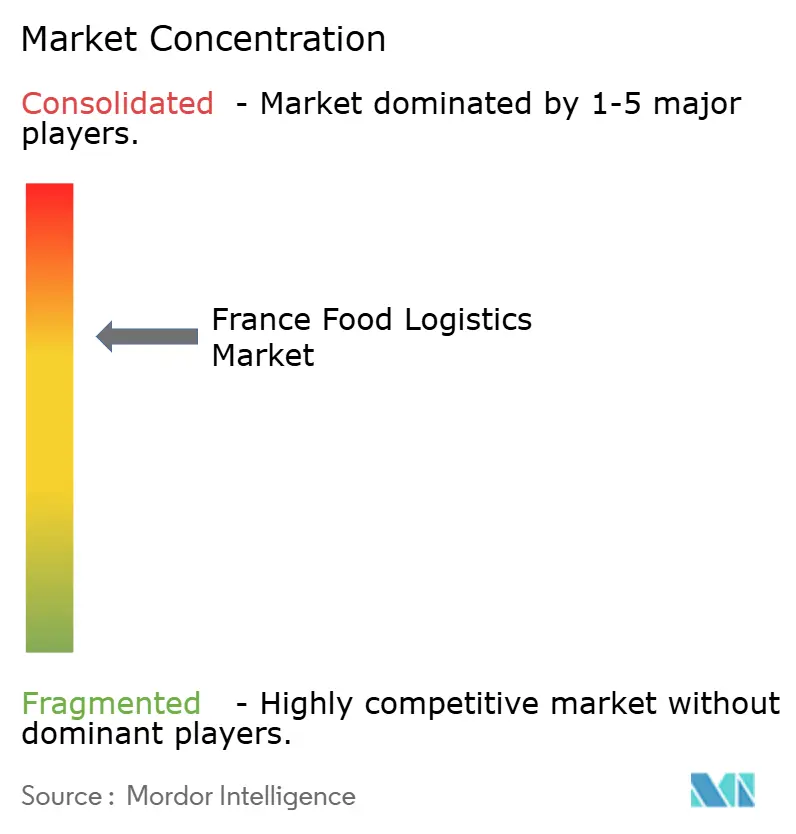

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Food Logistics Market Analysis by Mordor Intelligence

The France food logistics market size is expected to increase from USD 26.03 billion in 2025 to USD 27.37 billion in 2026 and reach USD 34.81 billion by 2031, growing at a CAGR of 4.93% over 2026-2031.

Strong demand for certified-organic products, stricter HACCP and ISO 22000 audits, and on-farm cold-storage modernization funded under the Common Agricultural Policy are reshaping facility standards and route design. Retailers are steering volumes toward third-party providers that can guarantee temperature integrity, blockchain traceability, and ammonia-based refrigeration, redirecting investment away from legacy ambient warehouses. The reopening of the Perpignan–Rungis refrigerated rail corridor is accelerating a pivot to multimodal flows that bypass congested north-south road arteries and cut diesel exposure. Meanwhile, renewable-energy ammonia hubs in rural regions are lowering per-pallet cooling costs, helping small producers move perishables competitively into national networks. Competitive pressure is therefore shifting from simple line-haul capacity to compliance infrastructure, green refrigeration, and digital visibility capabilities that determine which operators secure long-term contracts with French food manufacturers and retailers.

Key Report Takeaways

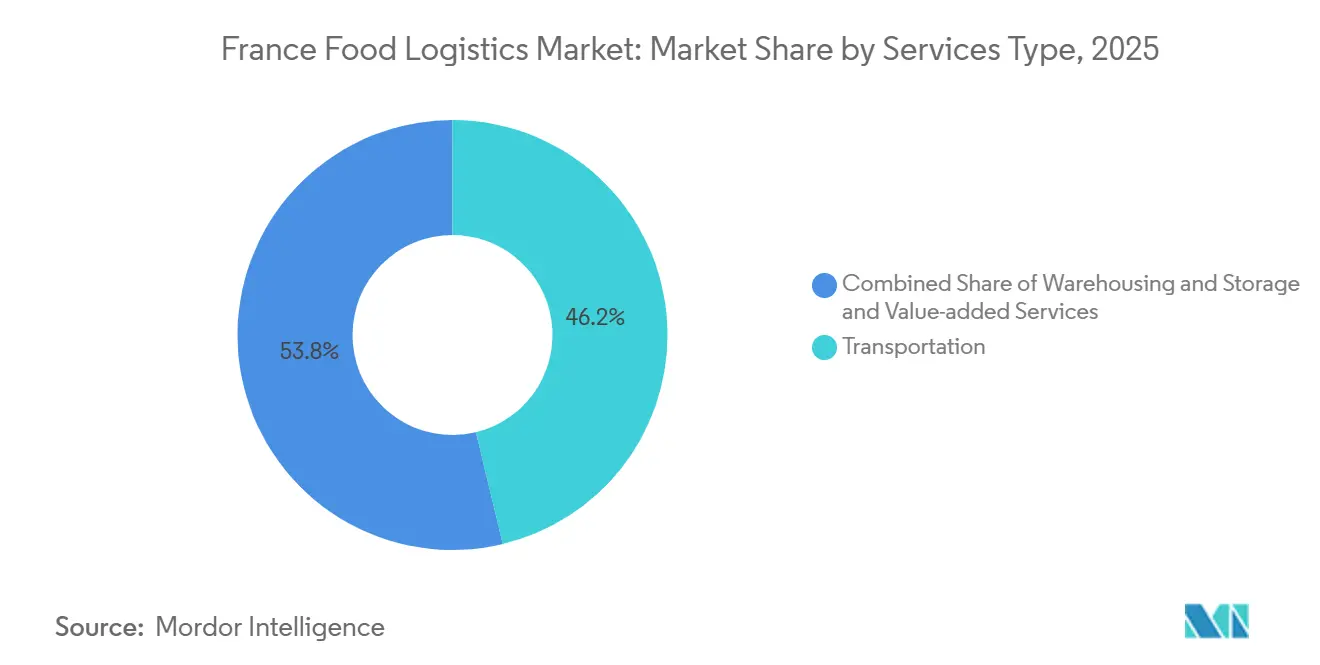

- By service type, transportation captured 46.24% of the France food logistics market share in 2025, while value-added services are advancing at a 7.49% CAGR through 2031.

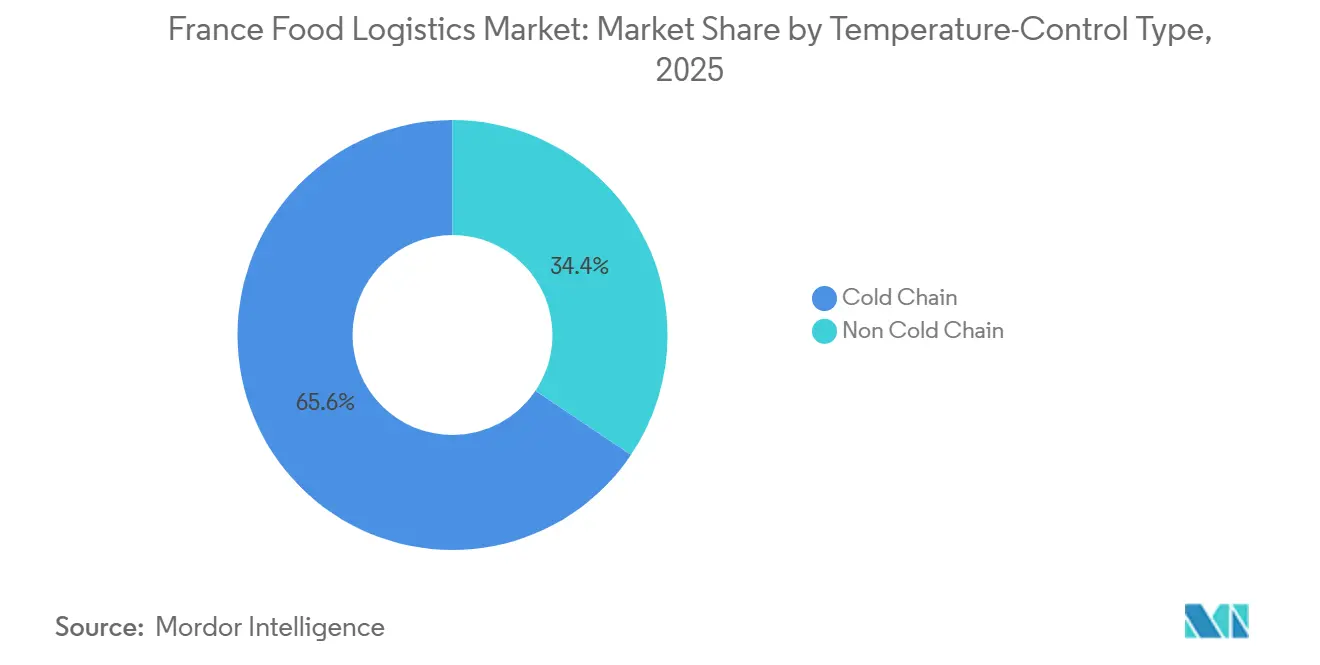

- By temperature-control type, the cold-chain segment accounted for 65.59% of the France food logistics market size in 2025 and is projected to grow at a 6.35% CAGR to 2031.

- By end-product category, dairy products and frozen desserts led with 27.26% of the France food logistics market size in 2025, whereas pet food throughput is forecast to expand at a 7.78% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Certified-Organic Food Volumes | +1.1% | National, focused on Occitanie, Nouvelle-Aquitaine, Pays de la Loire | Short term (≤ 2 years) |

| Tightening HACCP / ISO 22000 Audits | +0.9% | National, most acute in export-oriented regions | Medium term (2-4 years) |

| Seafood Nearshoring to Brittany & Normandy | +0.7% | Brittany, Normandy, corridors to Paris and Lyon | Short term (≤ 2 years) |

| CAP Grants for On-Farm Cold Storage | +0.8% | National, prioritizing small fruit and vegetable growers | Medium term (2-4 years) |

| Reopening of Perpignan–Rungis Rail Corridor | +0.5% | Southern France to Île-de-France, spillover into Benelux | Long term (≥ 4 years) |

| Renewable-Energy Ammonia Refrigeration Hubs | +0.6% | Auvergne-Rhone-Alpes, Grand Est, and other rural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Certified-Organic Food Volumes Requiring Dedicated Cold Logistics

Logistics providers are segmenting warehouses to eliminate cross-contamination and deploying dual-temperature vehicles with Ecocert-approved sanitation regimes, raising fixed costs but unlocking premium contractual yields. Organic dairy lines move faster than conventional SKUs, forcing more frequent route turns, while premium price points 30-50% above conventional support investment in blockchain lot traceability. Niche carriers specializing in organics are capturing business from national retailers who want suppliers that already satisfy audit checklists. Consequently, demand for certified capacity is outstripping supply in high-growth regions such as Occitanie, reinforcing upward pressure on dedicated cold-chain rates.

Tightening HACCP / ISO 22000 Audits Raising Demand for Compliant 3PL Warehouses

Carrefour, Auchan, and other majors now restrict tenders to ISO 22000-accredited depots, compressing the addressable market for non-certified operators. Certification requires documented critical-control protocols and continuous employee training that smaller fleets struggle to finance, accelerating consolidation within the France food logistics market. High-end infant-formula and functional-food shippers are importing GDP standards from pharma, spurring investment in redundant refrigeration and remote-temperature telemetry. As a result, compliant 3PLs can command 8-12% rate premiums, offsetting certification expenses and improving margin resilience[1]Agence Bio, “Les chiffres 2024 du bio en France,” agencebio.org.

Seafood Nearshoring to Brittany & Normandy Boosting Domestic Reefer Mileage

Average reefer hauls of 400-600 km from coastal plants to inland DCs lengthen domestic lane kilometers, lifting demand for multi-compartment trailers that sustain 0-2 °C and -18 °C zones in the same run. Labor shortages of 15-20% in processing plants are pushing automation, which in turn raises throughput predictability and heightens the need for scheduled outbound capacity. EU traceability rules that favor shorter supply chains reinforce the nearshoring logic, while the “Choisir la France” initiative supplies tax credits that defray capital outlays. Together these forces enlarge the refrigerated transport segment of the France food logistics market.

Common Agricultural Policy Grants Driving On-Farm Cold-Storage Modernization

In Provence-Alpes-Cote d’Azur and Pays de la Loire, growers that once rushed produce to city depots are now consolidating loads for weekly rather than daily dispatch, improving vehicle utilization and smoothing demand curves for regional carriers. Cold-storage decentralization reduces spoilage while allowing farmers to negotiate better contract terms because they are no longer price-takers during harvest peaks. Regional chambers of agriculture supply energy-audit toolkits that help farmers right-size ammonia or CO₂ systems for minimal kWh per pallet. These upgrades enlarge the rural node count inside the France food logistics market, widening the addressable customer base for mid-scale reefer fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Natural-Refrigerant Equipment | −0.8% | National, most acute in older depots | Short term (≤ 2 years) |

| Municipal Axle-Weight Limits | −0.4% | Rural wine-producing areas and agricultural secondary roads | Medium term (2-4 years) |

| Escalating Insurance Premiums | −0.5% | National, the highest for high-value perishables | Short term (≤ 2 years) |

| Data Fragmentation Among SMEs | −0.6% | National, severe for small producers and regional wholesalers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Natural-Refrigerant Equipment Delaying Fleet & Warehouse Upgrades

Transport units suitable for -25 °C frozen lanes come from only three global OEMs, adding 35-45% to purchase prices. French carriers face a dilemma: pay burgeoning HFC refill costs up 180% since 2022 or wait for back-ordered natural-refrigerant gear and risk service gaps. The talent deficit compounds the bottleneck; an extra 2,500 certified technicians are required by 2027 to install and maintain natural systems. As large 3PLs pre-book factory slots, smaller fleets are left to operate aging kit, tempering modernization across the France food logistics market[2]European Commission, “Common Agricultural Policy at a glance,” europa.eu .

Escalating Insurance Premiums Linked to Temperature-Excursion Liability

Premiums for temperature-excursion coverage jumped 22-28% in 2025 after a string of high-profile spoilage recalls pegged average claim costs at EUR 0.5-2 million (USD 2.31million). Underwriters now tier pricing by telemetry adoption; fleets with real-time IoT sensors enjoy 15-20% discounts, whereas paper-log operators absorb the full hike. DGCCRF can fine violators up to 4% of turnover, an exposure that insurers embed into their models, pushing some regional haulers to exit temperature-controlled lanes. Deductibles that scale with excursion duration motivate investment in backup gensets and SMS alert protocols, but the new cost burden still compresses EBIT margins by 150-250 bps for smaller operators in the France food logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Compliance-Driven Outsourcing Alters the Mix

Transportation retained a 46.24% grip on France food logistics market share in 2025, yet its growth is muted by driver shortages and volatile diesel prices, whereas value-added services are climbing at 7.49% CAGR. This shift shows that shippers prefer single-invoice partners who can handle blast freezing, kitting, and lot-traceability under one food-safety umbrella. The France food logistics market size attached to co-packing lines is rising as retailers launch ready-meal bundles that require synchronized portioning and cold assembly. Robotics adoption inside value-added facilities improves accuracy to ±0.5 °C in blast-freeze cycles, reducing cell damage in high-moisture SKUs and strengthening contractual KPIs.

Spot trucking rates fell 8-12% in 2024-2025, forcing pure haulers to explore intermodal offerings or cede share to integrated 3PLs. Rail’s subsidy-backed advance adds resilience, yet scheduling rigidity still caps its share below 8% of cold volumes. Several 3PLs are therefore bundling road-rail packages that guarantee next-day Paris arrival while cutting CO₂ per pallet by 70%. Across the France food logistics industry, service diversification is the main hedge against input-price swings and capacity overhangs.

By Temperature-Control Type: Cold Chain Extends Its Lead

The cold-chain controlled 65.59% of France's food logistics market size in 2025 and is growing at 6.35% CAGR as French consumers pivot toward fresh convenience foods. Frozen SKUs deliver a 7.2% growth tailwind by using blast-freeze to lock nutrients, while chilled dairy retains dominance in absolute tonnage. Digital sensors appear on 68% of reefer assets, up from 42% in 2023, slashing undetected excursion events by 55%. Energy-efficient composite panels and variable-speed compressors cut kWh usage per pallet by 20-30%, bolstering competitiveness against ambient rivals.

Ambient-sensitive goods such as chocolate and wine rely on passive insulation rather than active cooling, yet still stack up 9-11% of freight value. Regulatory moves extend mandatory digital logging to any refrigerated haul beyond 100 km, lifting compliance data volumes for analytics firms. The France food logistics market share commanded by cold-chain providers is therefore likely to inch upward as non-temperature-controlled players either retrofit fleets or lose tenders.

By End-Product Category: Premium Pet Food Accelerates, Dairy Holds Volume Crown

Dairy and frozen desserts supplied 27.26% of France food logistics market share in 2025, underpinned by cheese consumption of 24 kg per capita. Yet plant-based rivals are nibbling at case counts, requiring allergen-segregated bays that raise facility complexity. Meanwhile, pet-food logistics is scaling at 7.78% CAGR as fresh and raw frozen recipes mimic human-grade supply chains. Royal Canin and Hill’s now stipulate 2-4 °C end-to-end for chilled lines, persuading carriers to carve out species-specific compartments in mixed loads.

Meat, seafood, and poultry lanes emphasize blockchain batch IDs to satisfy EU farm-to-fork rules, pushing platform adoption from 18% in 2023 to an estimated 46% by 2026. Horticulture peaks compress network capacity by up to 60% in July-August, requiring dynamic load balancing among regional cross-docks. The France food logistics market size attributable to these surge windows is drawing venture-funded platforms that auction spare reefer slots in real time, trimming empty backhauls by 12-15%.

Geography Analysis

The southern arc Occitanie and Provence-Alpes-Cote d’Azur yields 2.4 million tons of fruit and vegetables each year and funnels them north via reefer corridors that average 10-12 hours in transit. The renovated Perpignan-Rungis rail service is expected to absorb 12,000 TEU annually by 2027, bringing a greener backbone to the France food logistics market[3]Marché International de Rungis, “Le Marché en chiffres,” rungisinternational.com.

Western territories, including Brittany and Pays de la Loire, supply 55% of national milk output and operate Europe’s densest seafood landing network outside Spain. Ports such as Lorient move 180,000 tons of fish annually, requiring -1 °C dockside holding rooms and -18 °C freezer tunnels before inland dispatch. The rise of seafood nearshoring boosts regional reefer mileage, with carriers adding Brittany-based micro-hubs to shorten first-mile legs. Grand Est and Bourgogne-Franche-Comté in the east serve as cereal and wine basins; their outbound flows lean on cross-border lanes into Germany and Switzerland. Long-term rail-freight modernization, budgeted at EUR 4.7 billion (USD 5.49 billion) to 2030, will add electrified sidings that accommodate refrigerated wagons, curtailing diesel drayage in export corridors.

Seasonal imbalances persist: summer horticulture surges cause a 40-60% capacity spike on northbound lanes, whereas winter dairy peaks drive southbound reefer deficits. Operators combat these swings by triangulating loads, wine barrels north, dairy south, produce east-west, boosting average asset utilization to 82%. That geographic choreography underscores why route optimization algorithms now embedded in 70% of large-fleet TMS platforms have become a decisive profit lever within the France food logistics market.

Competitive Landscape

The France food logistics market is moderately fragmented; the top five providers collectively command roughly 35-40% revenue share, leaving ample territory for regional specialists. STEF heads the league with EUR 4.8 billion (USD 5.61 billion) sales and 260 facilities, leveraging AI-driven route optimization and real-time telemetry to reduce temperature deviations by 38% year on year. GEODIS’ 2024 acquisition of trans-o-flex imports pharma-grade cold-chain know-how into premium food segments, while DSV’s 2025 purchase of DB Schenker adds scale for end-to-end continental coverage. Vertical integration is rife: top players are buying renewable-energy farms to power ammonia chillers and investing in last-mile startups to secure doorstep freshness for e-grocery clients[4]DSV A/S, “DSV completes the acquisition of Schenker,” dsv.com.

Technology serves as both a barrier and a wedge. Blockchain traceability rolled out by Chronofresh in 2024 wins insurer discounts and retailer preference, prompting copycat deployments across tier-one fleets. Robotics suppliers Exotec and E80 formed a 2025 alliance to offer multi-temperature automation, lifting picker productivity by 3-4× in new DCs. Meanwhile, compliance mandates such as ISO 22000 are prompting consolidation, as sub-scale depots either exit or sell to networks that can amortize audit costs across wider volumes. Competition, therefore, pivots on the ability to finance green refrigeration, secure certified labor, and integrate software layers that satisfy both regulators and brand-owner ESG scorecards.

White-space opportunity persists in organics, pet-food cold chain, and micro-fulfillment for rapid grocery. Parcel carriers are dipping toes by retrofitting vans with eutectic plates to serve under-30-minute e-grocery promises in Paris, but temperature-integrity lapses threaten brand equity, giving incumbent cold-specialists an edge. Market participants that marry renewable energy, digital provenance, and agile vehicle fleets will consolidate share as French retailers intensify sustainability and food-safety scrutiny across the France food logistics market.

France Food Logistics Industry Leaders

DHL Group

Kuehne + Nagel

STEF

GEODIS

FM Logistic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GEODIS completed the acquisition of Transports Malherbe to strengthen domestic road freight, especially in agri-food distribution, improving nationwide coverage and reducing reliance on subcontractors in France.

- November 2025: DHL invested in AI, automation, and sustainable warehousing to optimize cold-chain and perishable logistics.

- April 2025: DSV completed its EUR 14.3 billion (USD 16.7 billion) acquisition of DB Schenker, creating the world’s largest logistics group and extending multimodal cold-chain reach across Europe.

- February 2025: CEVA Logistics deployed 23 electric trucks in France, Belgium, and the Netherlands, taking its low-carbon fleet above 1,100 vehicles and trimming 984 tons of CO₂ annually.

France Food Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Water | |

| Air | |

| Warehousing and Storage | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat, Seafood, and Poultry |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) |

| Horticulture (Fresh Fruits & Vegetables) |

| Processed Food Products |

| Pet Food |

| Others (Spreads, Seasoning, dressing, Specialty & Functional Foods, etc.) |

| By Services | Transportation | Road |

| Rail | ||

| Sea and Inland Water | ||

| Air | ||

| Warehousing and Storage | ||

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat, Seafood, and Poultry | |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) | ||

| Horticulture (Fresh Fruits & Vegetables) | ||

| Processed Food Products | ||

| Pet Food | ||

| Others (Spreads, Seasoning, dressing, Specialty & Functional Foods, etc.) | ||

Key Questions Answered in the Report

What is the current size of the France food logistics market?

The France food logistics market size stood at USD 26.03 billion in 2025 and is projected to reach USD 34.81 billion by 2031.

How fast is cold-chain demand growing in France?

Cold-chain revenues are rising at a 6.35% CAGR through 2031 as consumers favor fresh and frozen foods and regulations tighten digital temperature logging.

Which service segment is expanding the quickest?

Value-added services such as blast freezing and kitting are advancing at 7.49% CAGR because shippers outsource compliance-heavy functions.

Why are insurance premiums increasing for food logistics operators?

Temperature-excursion liability claims have driven a 22-28% premium surge, especially for carriers lacking real-time IoT monitoring.

How is the Perpignan–Rungis rail corridor influencing logistics flows?

The restored refrigerated rail link removes 18-24 hours from Mediterranean produce transit times and lowers CO₂ emissions by 75% per ton-kilometer.

What technology trends are shaping competitive advantage?

Blockchain traceability, renewable-energy ammonia refrigeration, and warehouse robotics are becoming decisive differentiators for securing long-term retail contracts.

Page last updated on: