Asia-Pacific Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 315.5 Billion |

| Market Size (2026) | USD 328.60 Billion |

| Market Size (2031) | USD 397.5 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

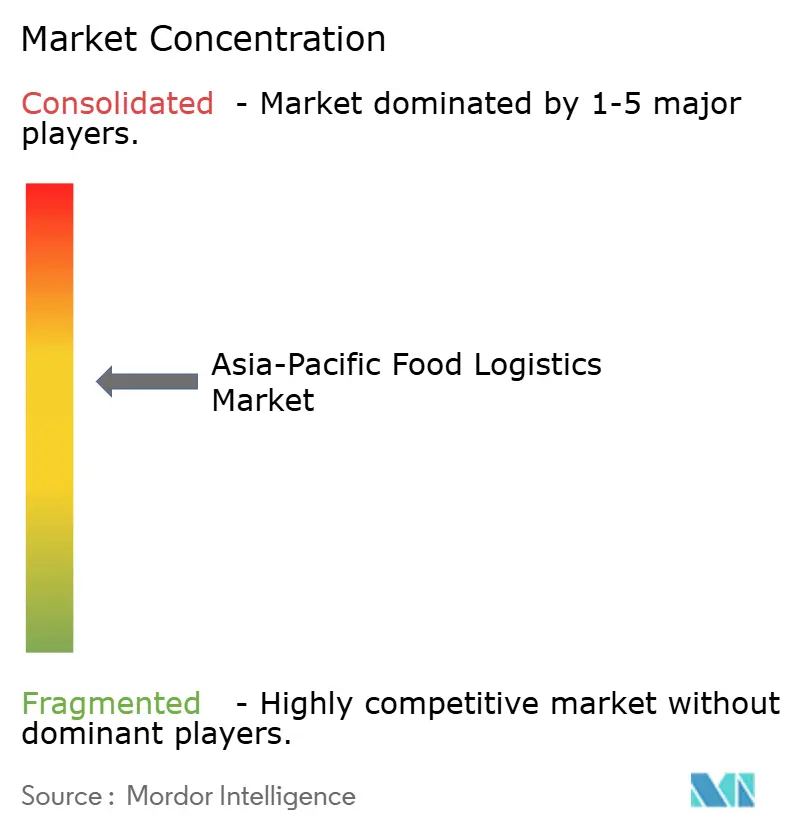

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Food Logistics Market Analysis by Mordor Intelligence

The Asia-Pacific Food Logistics Market size is expected to increase from USD 315.5 billion in 2025 to USD 328.60 billion in 2026 and reach USD 397.5 billion by 2031, growing at a CAGR of 3.88% over 2026-2031.

Regional distribution is shifting from legacy wholesale routes to digitally orchestrated cold chain corridors that position fresh produce, chilled dairy, and frozen proteins close to demand. Evolving food safety frameworks are pushing standardized temperature control and traceability, which is lifting telemetry and quality management adoption in the Asia-Pacific food logistics market. E-commerce and quick commerce are compressing delivery windows and expanding micro-fulfillment footprints with chilled and frozen capacity near urban cores. Governments are pairing digital trade facilitation with targeted logistics investments, including cold storage priorities in long-term roadmaps that reinforce producer margins and lower post-harvest losses. Heightened attention to regional foodborne illness risks is accelerating common temperature protocols and inspection standards that reshape services across the Asia-Pacific food logistics market.

Key Report Takeaways

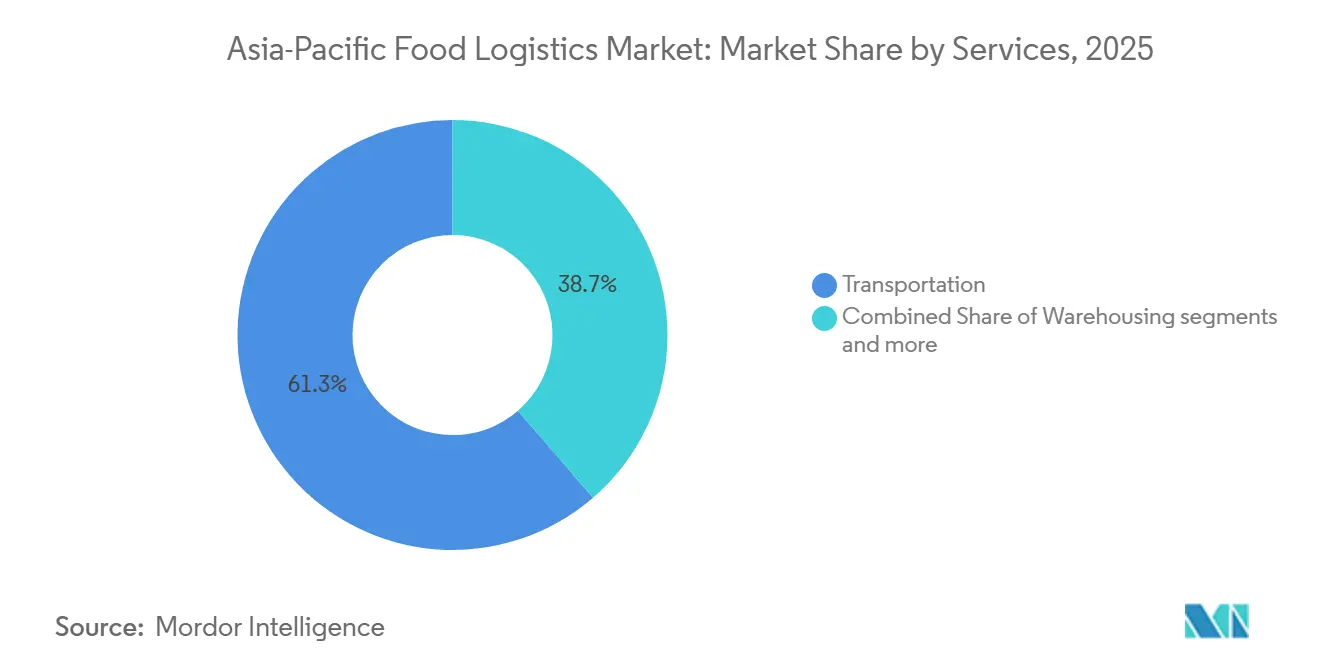

- By services, transportation held 61.34% of the Asia-Pacific food logistics market share in 2025, while value-added services and other logistics solutions are projected to expand at a 5.41% CAGR through 2031.

- By temperature-control type, cold chain accounted for 64.31% of the Asia-Pacific food logistics market size in 2025 and is projected to grow at a 4.67% CAGR through 2031.

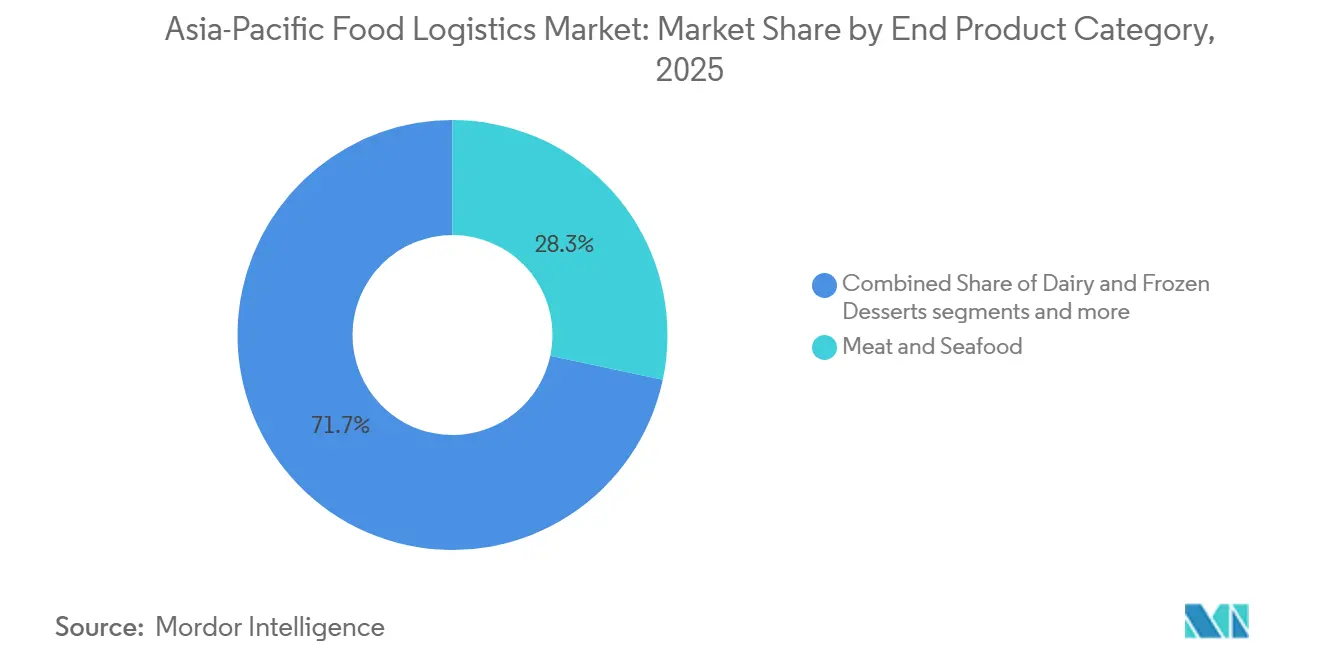

- By end-product category, meat and seafood led with 28.34% share in 2025, and dairy and frozen desserts are projected to be the fastest growing at a 5.89% CAGR through 2031.

- By geography, China accounted for 39.12% share in 2025, while India is projected to grow at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign Investment and Logistics Modernization | +0.8% | Vietnam, Philippines, Singapore, India | Medium term (2-4 years) |

| E-commerce and Quick Commerce Boom | +1.1% | China, Singapore, Indonesia | Short term (≤ 2 years) |

| Cold Chain Infrastructure Development | +1.0% | Philippines, India, Vietnam with spillover to Thailand, Malaysia | Medium term (2-4 years) |

| Organized Retail and Modern Trade Growth | +0.6% | Vietnam and core ASEAN markets | Medium term (2-4 years) |

| Cross-Border Food Trade Expansion | +0.7% | China, ASEAN, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Food Safety and Quality Standards | +0.5% | China, Japan, Singapore, Malaysia with gradual ASEAN-wide lift | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Foreign Investment and Logistics Modernization

Vietnam’s national roadmap elevates logistics to a foundational economic sector and prioritizes cold storage for agricultural outputs, with a long-term focus on green logistics that uses clean energy to support the agri-food value chain. Singapore’s Food Services Industry Digital Plan provides adoption tracks for AI-enabled document reconciliation and logistics control towers that help SMEs manage temperature-controlled flows with higher visibility and security, while aligning skills and cybersecurity needs for the sector. China’s cross-ministry plan targets 80% digitalization for business management and 75% digital control over key processes in large food enterprises by 2027, backed by demonstration projects and typical application scenarios that cascade into logistics operations. These national programs set a consistent direction for investment in temperature telemetry, secure data exchanges, and warehouse automation across the Asia-Pacific food logistics market. The push to modernize also narrows capability gaps between advanced hubs and emerging corridors where smaller operators face financing constraints. As uptake increases, service expectations now include auditable cold chain records and integrated exception handling that reinforce buyer confidence in temperature-sensitive movements across borders.

E-commerce and Quick Commerce Boom

Rapid adoption of online grocery and meal platforms is compressing delivery windows and placing a premium on short-radius cold distribution. In Singapore, e-commerce is projected to double between 2023 and 2030, and the cold chain perishables market is expected to double by 2034, reinforcing the need for robust chilled and frozen capacity in importer hubs with significant re-export activity. Digital control towers and automated ordering are improving coordination between procurement, production, and distribution to support reliability at narrow delivery intervals across the Asia-Pacific food logistics market. Cross-border e-commerce growth also benefits from rising air cargo capacity and expanded cool-chain capability at regional gateways through 2028, helping time-sensitive food products reach consumers with higher service levels. Quick commerce models are changing network design as operators pre-position chilled and frozen inventory in micro-fulfillment centers to meet three-kilometer delivery radii in dense urban areas. These shifts reward integrated providers that can orchestrate temperature, visibility, and last-mile handoffs in one service layer across the Asia-Pacific food logistics market.

Cold Chain Infrastructure Development

Targeted investment is reducing spoilage and improving farmer margins by expanding access to reliable temperature-controlled facilities. India projects 436.5 lakh metric tonnes of cold storage capacity and more than 33,000 reefer vehicles by 2031, while energy transition measures could save 876 GWh annually and reduce emissions by 785 ktCO2 through efficiency upgrades that lower cost to serve. Indonesia is prioritizing inter-island cold packages, port-based cold chain, and solar-enabled warehouses to bring down logistics costs over time, supported by digital warehouse management for better flow control. Japan faces redevelopment needs where cold storage usage neared full capacity in key ports by late 2024, and a significant portion of floor space is at least 40 years old, prompting upgrades that favor energy efficiency and temperature fidelity. China’s trajectory includes 277 million cubic meters of cold storage in 2025 and a larger refrigerated truck fleet, with strong growth for new energy refrigerated trucks that align with low-carbon policy objectives. These investments reduce bottlenecks and help standardize temperature assurance at scale in the Asia-Pacific food logistics market.

Organized Retail and Modern Trade Growth

Modern trade formats are expanding in urban and peri-urban areas and are altering replenishment patterns from bulk shipments to segmented, frequent deliveries with precise temperature control. Vietnam’s retail sales in 2025 reached VND 7,008.9 trillion, with goods retail at VND 5,391 trillion, and strong store network growth planned in 2026 to extend access to chilled and frozen categories in underserved areas, equal to about USD 205 billion for goods retail using the local reference conversion provided in 2025 (USD 205 billion). Retailers are compressing order cycles and increasing route density across store clusters, which raises the value of route planning, fleet readiness, and quality documentation in the Asia-Pacific food logistics market. Digital adoption in manufacturing and distribution also supports coordinated flows, with broad uptake of at least one sector-specific digital solution in Singapore by 2025 that helps align inventory with cold chain capacity. ASEAN’s regional food safety policy sets direction for harmonized controls and stronger national systems, which help cross-border operators align with shared expectations for labeling, handling, and traceability over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Cold Chain Infrastructure | -0.6% | India, Indonesia, Thailand, Philippines | Short term (≤ 2 years) |

| High Capital and Operating Costs | -0.8% | Thailand, India, ASEAN-wide, with acute effects in tier-two cities | Medium term (2-4 years) |

| Regulatory Complexity and Inconsistency | -0.4% | ASEAN members with transitional frameworks in China | Long term (≥ 4 years) |

| Infrastructure and Connectivity Challenges | -1.0% | South Asia, Southeast Asia, rural Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Cold Chain Infrastructure

India’s cold chain supports only a small portion of the fresh produce needs, and roughly three-quarters of the bulk storage capacity is concentrated in single-commodity potato facilities that cannot flex for diversified horticulture. Sparse assets at the farmgate, such as pre-cooling units and packhouses, increase thermal stress before produce enters formal networks and raise the risk of losses during peak seasons. Many older facilities rely on inefficient systems and poor insulation, which heighten energy intensity in power-constrained regions and limit the ability to maintain precise temperature controls. In Thailand, agricultural freight remains dominated by road, while rail and inland water transport options are underused, which keeps logistics costs elevated relative to international benchmarks and increases exposure to temperature excursions on longer routes. The lack of integrated networks and uneven capacity distribution forces exporters to stitch together multiple providers across the first mile, line-haul, storage, and border processes. These handoffs increase both dwell time and temperature risk, which limits quality outcomes in the Asia-Pacific food logistics market.

High Capital and Operating Costs

Upgrading to efficient refrigeration, renewable power, and automation requires significant upfront investment that is harder to justify outside large volume nodes. In India, older cold stores account for a large share of sector energy consumption while reefer fleets add another significant share, which amplifies sensitivity to tariffs and diesel prices. Grid instability in rural areas often necessitates diesel generators, which raises per-unit energy cost and complicates low-emission targets across the Asia-Pacific food logistics market. Transport infrastructure demand across Asia-Pacific is set to be heavy through 2035, as projected by the Asian Transport Observatory, which stretches public budgets and lengthens timelines for the supportive road and rail assets that reduce costly road reliance. Operators in mature markets also face persistent labor constraints and thin transport margins, which lower appetite for speculative cold store expansions even as exports remain resilient. These constraints slow the shift to highly automated, energy-efficient facilities outside primary hubs and keep manual processes in place, which can limit temperature precision during high-volume periods in the Asia-Pacific food logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Roads Dominate, Value-Added Solutions Accelerate

Transportation commanded 61.34% of the Asia-Pacific food logistics market share in 2025, and value-added services and other logistics solutions are projected to expand at 5.41% CAGR through 2031 for the Asia-Pacific food logistics market size. Road carries the majority of agricultural loads in Thailand, where rail is underused despite per-ton-kilometer advantages, which sustains reliance on flexible last-mile assets for frequent, small-batch replenishment. India’s dedicated Reefer Express service connecting ICD Kanpur and Mundra Port was launched in March 2026 to provide a rail corridor with tighter temperature controls and fuel savings on long domestic legs with reliable export handoffs. Warehousing footprints are growing to support omnichannel fulfillment, including temperature-controlled space in regional hubs that can scale multi-category flows for regional and cross-border distribution. Value-added solutions now bundle pre-cooling, portioning, labeling, and automated document checks to reduce handoffs and increase visibility, which aligns with buyer expectations for integrated cold chain orchestration in the Asia-Pacific food logistics market. Certifications such as ISO 9001 and ISO 22000 are becoming common prerequisites for multinational buyers, which push providers to formalize quality procedures and maintain robust documentation across all service lines.

Air freight supports high-value perishables that require rapid international connections, and network upgrades like DHL’s expanded Airfreight Cold Chain Network connect more than 30 GDP-compliant hubs with additional routes targeted in Asia. Regional air cargo volumes are projected to rise through 2028, which supports shorter cycles for cross-border shipments of fresh and chilled products. Maritime routes remain central for bulk commodity movements, and Hong Kong’s inbound food and beverage volumes in early 2025 confirm stable demand for seaborne distribution. Cross-border trucking is improving under the ASEAN Customs Transit System, and Kuehne+Nagel has added prime movers and containers in Thailand to meet e-commerce and high-tech demand while lowering cost and dwell time at borders. Digital control towers promoted in Singapore enable real-time management of routes and temperature performance, which reduces exception handling and strengthens compliance readiness for shippers across the Asia-Pacific food logistics market.

By Temperature-Control Type: Cold Chain Expansion Leads Market

Cold chain logistics represented 64.31% of the market in 2025 and are projected to expand at 4.67% CAGR through 2031 for the Asia-Pacific food logistics market size. Within cold chain flows, chilled categories dominate for dairy, ready-to-eat meals, fresh meat, and seafood, while frozen categories are scaling faster as processors extend shelf life to reach tier-two and tier-three cities at a sustainable cost to serve. China’s prepared meat products standard requires refrigerated storage and transport at 0-4°C and frozen at -18°C or below, with pre-cooled vehicles and clear limits on temperature rise during loading and unloading operations, which formalizes operating protocols for carriers and depots. Japan’s FY2025 Imported Foods Monitoring Plan intensifies audits for pathogenic microbes in frozen aquatic products and vegetables, including sampling programs for Salmonella spp. and Listeria monocytogenes in frozen unheated vegetables, which strengthens oversight of cold chain integrity on inbound flows. Non-cold chain logistics serve processed and shelf-stable categories that rely less on temperature controls, but consumer preference for fresh and ready-to-cook items keeps growth momentum centered on chilled and frozen segments in the Asia-Pacific food logistics market.

Technological progress supports multi-temperature trailers that partition chilled and frozen zones within a single vehicle to optimize route density for mixed loads. China reported 277 million cubic meters of cold storage capacity in 2025, along with a larger refrigerated truck fleet and strong growth in new energy refrigerated trucks aligned with national measures for a lower-carbon cold chain. South Korea is phasing in refrigerant limits for industrial systems and reefer trucks from 2028, tightening further by 2030, which is prompting a shift to natural refrigerants and compliant equipment among operators and OEMs. These standards and capacity additions lift the baseline for reliability across storage and line-haul, which strengthens buyer confidence in sensitive flows and reduces spoilage across the Asia-Pacific food logistics market. India’s installed capacity remains concentrated in single-commodity bulk storage, which underscores the need to diversify temperature-controlled infrastructure to support horticulture, dairy, meat, and ready-to-eat channels at a national scale.

By End-Product Category: Meat Leads, Dairy Fastest

Meat and seafood led with 28.34% share in 2025, while dairy and frozen desserts are projected to be the fastest growing at 5.89% CAGR through 2031 for the Asia-Pacific food logistics market size. China’s three-year country-specific beef tariff rate quota from 2026 influences allocation decisions and routing strategies for importers by applying a 55% additional tariff beyond national thresholds, which creates new constraints and rebalancing needs in import corridors. India’s National Program for Dairy Development allocated INR 2,790 crore through 2026 to scale milk procurement, expand bulk cooling at the village level, and strengthen laboratory testing for quality control, equal to USD 336.1 million at an assumed 2025 average exchange of INR 83 per USD (USD 336.1 million). Australia’s dairy exports rose in value to AUD 3.7 billion in 2025 over the last reported year on robust demand in Asian markets, which supports stable cold storage and reefer capacity dedicated to outbound flows. Processed foods, condiments, and packaged goods maintain a steady draw on temperature-controlled handling where quality or shelf life requires thermal control, while specialty ingredients with strict ranges expand opportunities for value-added services in the Asia-Pacific food logistics market.

Regulatory oversight on meat imports continues to tighten, with China’s registration and administration rules requiring overseas manufacturers and storage facilities to maintain reliable traceability systems from origin through processing for shipments to China. ASEAN’s Food Safety Policy directs member states to harmonize measures and strengthen national food control systems, which supports safer movement of temperature-sensitive products within the region, even as enforcement remains uneven by market. Rising cold chain investments and digital documentation expectations are reinforcing product integrity in transit, which favors providers that can combine compliance, visibility, and responsive service in the Asia-Pacific food logistics market. Public and private programs in dairy and protein supply chains are also raising baseline requirements for time, temperature, and testing, which advances operating norms across regional corridors.

Geography Analysis

China anchored regional demand with 39.12% share in 2025, while India is projected to expand at 6.12% CAGR through 2031 in the Asia-Pacific food logistics market. China reached 277 million cubic meters of cold storage capacity in 2025 and recorded rapid growth in refrigerated truck deployments, including new energy refrigerated trucks that align with national decarbonization measures and lift last-mile cold coverage. A cross-ministry program set digitalization targets for large food enterprises by 2027, including typical application scenarios and demonstration projects that extend to logistics operations and documentation standards. China’s tariff rate quota rules for beef assign country-specific thresholds and add a significant surcharge for volumes beyond allocation, which is reshaping import routing to designated gateways and compliant inland hubs.

Japan faces tight cold storage utilization in key port cities where long-standing facilities need redevelopment to meet energy and efficiency standards, while a strong inbound inspection regime continues to shape handling protocols for sensitive categories. South Korea is working through a near-term adjustment in space and rents, but has firm long-term fundamentals supported by refrigerant phase-down milestones in 2028 and 2030 that will drive equipment upgrades and modernized cold infrastructure. India is scaling cold store capacity and reefer fleets and outlining energy transition strategies to reduce losses and power intensity, though installed infrastructure remains concentrated in single-commodity storage that constrains multi-category flows in key producing states. Program support for processing and cold chain projects continues to expand preservation, quality control, and throughput along food corridors that link to export gateways.

Australia benefits from diversified exports and steady demand in Asian markets for beef and dairy, which sustains cold storage commitments despite persistent operating cost pressures in transport and labor markets. Indonesia is prioritizing inter-island cold packages, port-based capacity, and solar-enabled facilities with digital warehouse systems to cut logistics costs toward national targets over time. Malaysia serves regional flows in life sciences and food with temperature-controlled infrastructure near Kuala Lumpur’s aviation hub that reduces handling time for sensitive cargo through GDP-compliant facilities.

The Philippines is pursuing a national cold storage buildout to extend shelf life for high-value crops and support urban demand as consumption patterns evolve, a priority consistent with multi-year infrastructure and food security programs. Singapore’s cold chain perishables market is expected to double by 2034 as e-commerce scales, which increases the need for reliable chilled and frozen capacity near major gateways and accelerates the adoption of solar and electric equipment in warehouses. Thailand operates as a cross-border hub in the ASEAN Customs Transit System and is adding equipment to serve e-commerce and industrial flows, even as rail and water remain underutilized across agricultural freight. Vietnam is targeting double-digit retail growth and maintains a strong seafood export performance with frozen categories that support long-haul shipments and resilient factory utilization. In the rest of Asia-Pacific, logistics firms are building domestic networks in emerging markets with multi-site cold storage and temperature-controlled fleets to serve expanding urban nodes.

Regulatory frameworks differ across markets, and central agencies in China plan to speed revisions to food safety standards for premade dishes, residue testing, and cold chain transportation with stronger cross-department enforcement. Japan also streamlined electronic submissions for repeated import notifications following system upgrades to improve monitoring and control of inbound food items within its oversight framework. ASEAN’s food safety policy outlines coordination mechanisms for implementing regional measures along the supply chain, which will support safer, more predictable cross-border movements over time as member ratifications progress.

Competitive Landscape

The Asia-Pacific food logistics market shows moderate competition in Southeast Asia and more concentrated structures in Northeast Asia, with differentiation moving toward digital visibility, greener fleets, and consistent temperature assurance. Global integrators like DHL, Kuehne+Nagel, and DSV leverage multimodal assets and proprietary IT to win high-value contracts from food brands and fast fulfillment platforms that demand end-to-end visibility and documented controls. DHL is scaling temperature-compliant air freight networks and investing in dedicated aircraft for regulated health logistics, which also provides capabilities applicable to premium food categories and sensitive perishables that depend on strict time and temperature controls. Kuehne+Nagel expanded cross-border capacity across the Mekong and Malaysia corridors under the ASEAN Customs Transit System, adding prime movers and containers to lower costs and improve reliability for e-commerce and high-tech flows. DSV accelerated integration of acquired operations and announced large synergy targets for 2026, which can fund further service upgrades and network densification over time.

Regional leaders like Nippon Express deploy cross-border trucking and specialized cold chain handling for fresh produce and seafood to serve hotels and restaurants, while also expanding temperature-controlled storage footprints at regional hubs. Facility investments in Singapore’s Tuas area added capacity, worker-safety technology, and advanced storage systems to raise throughput and reduce emissions by replacing diesel forklifts with electric models. These moves indicate a steady shift toward higher-density networks with more precise temperature zones supported by IoT monitoring and automated quality checks in the Asia-Pacific food logistics market. The Asia-Pacific food logistics industry is also seeing a rise in control tower deployments that integrate order and inventory data to orchestrate routes and cooling profiles in real time.

Green logistics programs are reshaping procurement. China expanded the refrigerated truck fleet and saw sharp gains in sales of new energy refrigerated trucks in 2025, aligned with national measures for low-carbon cold chain logistics. South Korea’s refrigerant phase-down targets for industrial systems and reefer trucks are prompting investments in natural refrigerants and compliant equipment. Operators are adopting solar generation on warehouse rooftops and switching to electric material handling equipment to trim emissions in core nodes, as seen in Singapore’s Tuas expansion. As these capabilities spread, contracts in the Asia-Pacific food logistics market place more value on documented emissions reductions alongside delivery performance and food safety compliance.

Asia-Pacific Food Logistics Industry Leaders

DHL Supply Chain

Nippon Express Holdings

Kerry Logistics Network

Yusen Logistics (Part of NYK Line)

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: India’s Container Corporation of India launched the first dedicated Reefer Express train service from ICD Kanpur to Mundra Port, establishing a direct, temperature-controlled rail corridor that offers superior temperature consistency for the approximately 1,200 km journey, reduces carbon emissions and fuel consumption, and integrates with a global export network through collaborators.

- February 2026: DHL Group expanded its dedicated Airfreight Cold Chain Network as part of a EUR 2 billion strategic program, introducing a dedicated Boeing 777 freighter and planning additional routes across Asia with over 30 GDP-compliant aviation hubs and gateways connected.

- February 2026: China’s State Council Food Safety Office announced plans to accelerate revisions to food safety standards for premade dishes, residue testing, and cold chain transportation, strengthening regulatory frameworks and cross-departmental enforcement.

- February 2026: Singapore’s Infocomm Media Development Authority and Enterprise Singapore launched a refreshed Food Manufacturing Industry Digital Plan that guides over 1,500 food manufacturers and introduces a Logistics Control Tower solution, AI-enabled automated ordering, and manufacturing analytics, with more than 90% sector adoption of at least one digital solution by 2025.

Asia-Pacific Food Logistics Market Report Scope

The Asia-Pacific Food Logistics Market is Segmented by Services (Transportation, Warehousing, and Value-Added Services), by Temperature-Control Type (Cold Chain, Non Cold Chain), by End-Product Category (Meat & Seafood, Dairy, Fruits & Vegetables, Food and Beverages, and Others), and by Geography (China, Japan, India, South Korea, Australia, Southeast Asia, and Rest of Asia-Pacific). Market Forecasts are Provided in Value (USD).

| Transportation | Road |

| Rail | |

| Water | |

| Air | |

| Warehousing | |

| Value-Added Services and Others |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat & Seafood |

| Dairy & Frozen Desserts |

| Fruits & Vegetables |

| Food and Beverages |

| Others |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Services | Transportation | Road |

| Rail | ||

| Water | ||

| Air | ||

| Warehousing | ||

| Value-Added Services and Others | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat & Seafood | |

| Dairy & Frozen Desserts | ||

| Fruits & Vegetables | ||

| Food and Beverages | ||

| Others | ||

| By Country (Value, USD) | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Malaysia | ||

| Philippines | ||

| Singapore | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current size and outlook for the Asia-Pacific food logistics market?

The Asia-Pacific food logistics market size is expected to grow from USD 315.5 billion in 2025 to USD 328.6 billion in 2026 and reach USD 397.5 billion by 2031 at 3.88% CAGR.

Which service area leads and which is growing fastest in the region?

Transportation led with 61.34% share in 2025, while value-added services and other logistics solutions are projected to grow fastest at 5.41% CAGR through 2031.

Which product categories matter most for capacity planning?

Meat and seafood led with 28.34% share in 2025, while dairy and frozen desserts are projected to grow fastest at 5.89% CAGR to 2031, increasing chilled and frozen handling needs.

Which markets are pivotal for near-term expansion?

China held 39.12% share in 2025, and India is projected to grow at 6.12% CAGR to 2031, which will drive scale-up in storage, reefer fleets, and last-mile coverage.

What are the main forces reshaping operations and contracts?

Digitalization, stricter food safety standards, quick commerce, and green logistics are raising expectations for visibility, compliance, and energy efficiency across networks.

Page last updated on: