Japan Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 31.69 Billion |

| Market Size (2025) | USD 32.99 Billion |

| Market Size (2030) | USD 40.11 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

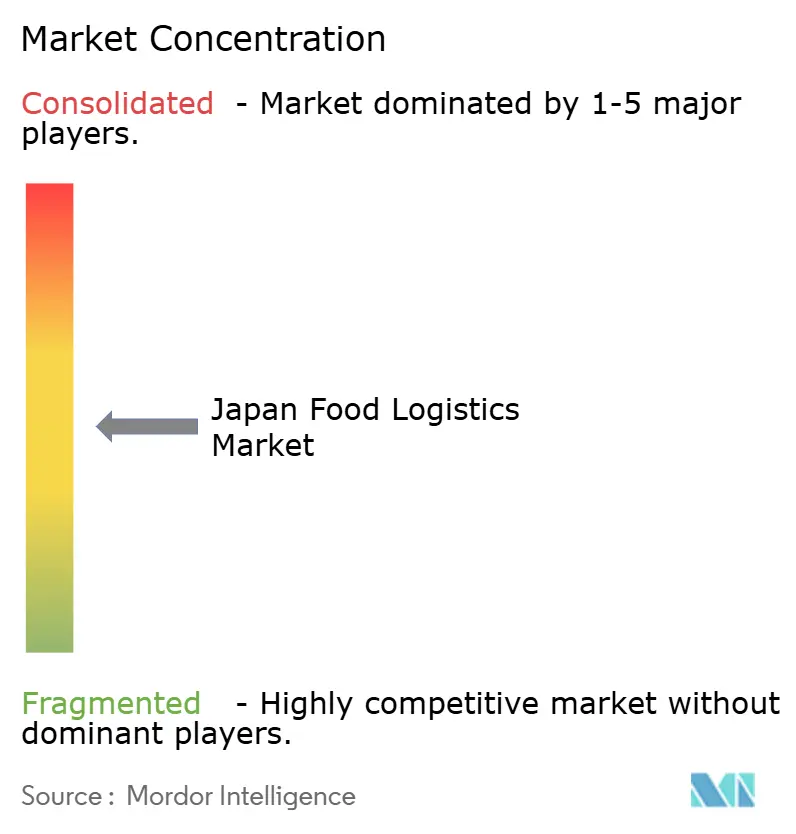

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Food Logistics Market Analysis by Mordor Intelligence

The Japan food logistics market size is projected to be USD 31.69 billion in 2025, USD 32.99 billion in 2026, and reach USD 40.11 billion by 2031, growing at a CAGR of 3.99% from 2026 to 2031.

A measured headline growth rate conceals big structural change. Pharmaceutical cold-chain operators now dedicate slack capacity to grocery movements, boosting average asset utilization to 85% versus the historical 68% baseline, while giving fresh food shippers access to pharmaceutical-grade monitoring that cuts spoilage by as much as 45%. Parallel corporate Scope-3 audits have led multinationals to trim carrier rosters by 30-40% since 2024, channeling volume toward providers able to supply audited carbon data and invest in low-emission fleets. Elderly single-person households already place 2.3 grocery orders each week, more than double the family average, forcing route planners to orchestrate high-frequency, low-volume chilled deliveries that challenge classic hub-and-spoke.

Key Report Takeaways

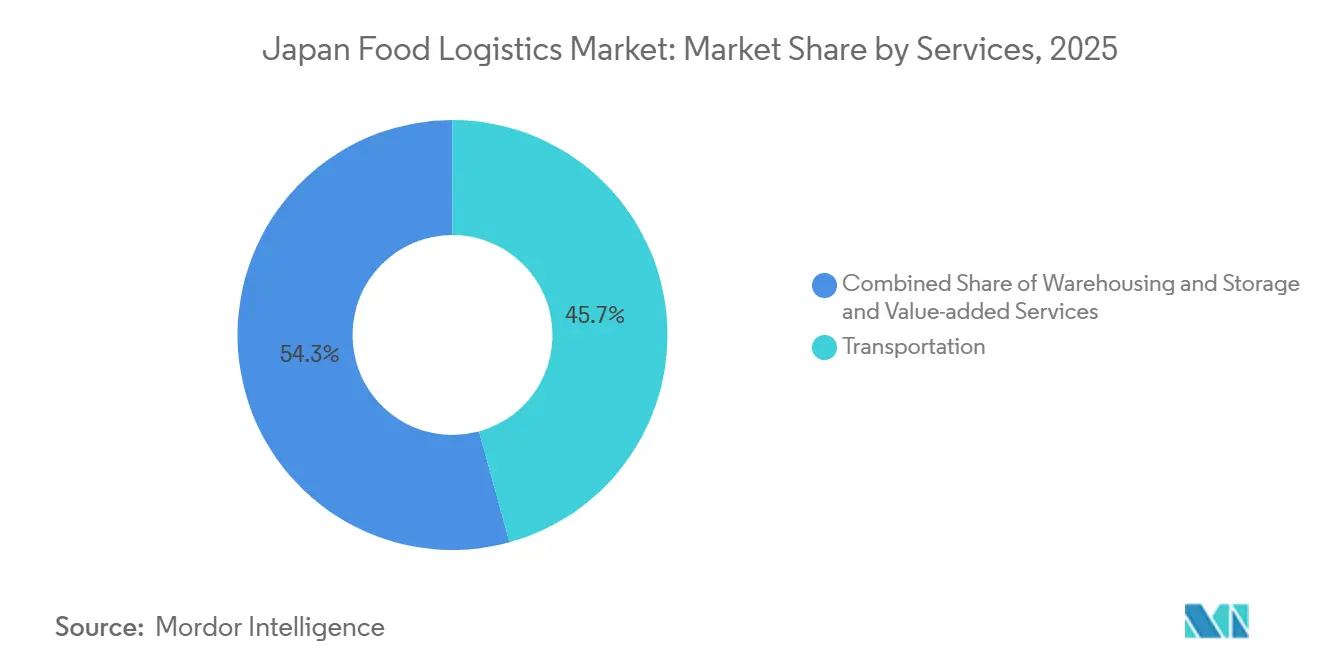

- By services, transportation commanded 45.72% of the Japan food logistics market share in 2025, whereas value-added services are forecast to advance at 6.55% CAGR through 2031.

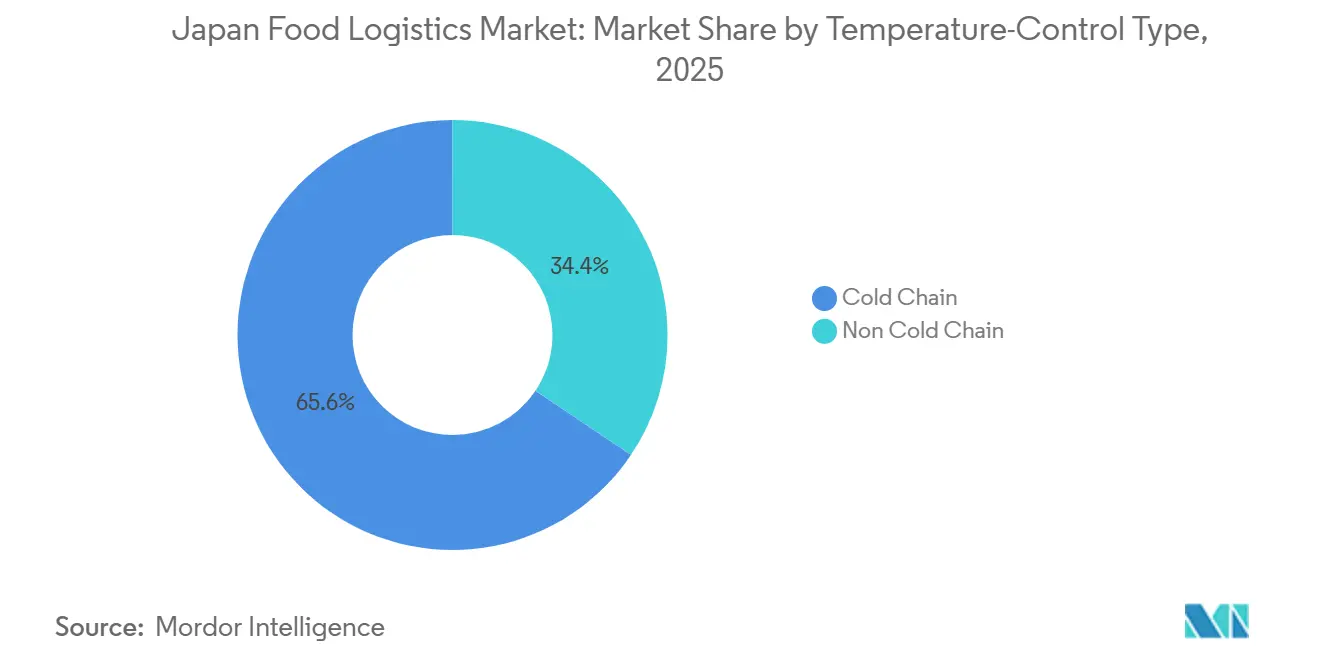

- By temperature-control type, Cold chain held 65.59% of the Japan food logistics market size in 2025 and is expanding at a 5.41% CAGR to 2031.

- By end-product category, meat, seafood, and poultry captured 32.26% share of the Japan food logistics market size in 2025; pet food is the fastest-growing end-product category at 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Pharmaceutical Cold-Chain Cross-Utilisation | +0.9% | National, with concentration in Greater Tokyo, Osaka, and Nagoya pharmaceutical hubs | Medium term (2-4 years) |

| Corporate Scope-3 Emission Audits Prompting Supplier Consolidation | +0.7% | National, led by multinational food manufacturers and major retailers | Short term (≤ 2 years) |

| Ageing Population Driving High-Frequency Small-Lot Chilled Runs | +1.1% | National, with acute impact in rural prefectures and metropolitan suburbs | Long term (≥ 4 years) |

| National Food-Security Stock Freezer Initiatives | +0.5% | Regional, targeting port cities and inland distribution centers | Medium term (2-4 years) |

| Port Digitalisation Slashing Reefer Dwell Times | +0.6% | Coastal, focused on Tokyo, Yokohama, Osaka, Kobe, and Nagoya port complexes | Short term (≤ 2 years) |

| Urban Tax Breaks for Automated Vertical Cold-Storage Sites | +0.8% | Metropolitan, prioritizing Tokyo, Osaka, and secondary city industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Pharmaceutical Cold-Chain Cross-Utilization

Hybrid networks now shift refrigerated trucks from morning drug deliveries to afternoon fresh-food runs, aligning 2-8 °C requirements across both cargo types and lifting food volumes to 15-22% of pharmaceutical fleet capacity[1]“Food Security Initiatives,” Ministry of Agriculture, Forestry and Fisheries, maff.go.jp . Higher specification control trims waste, extends shelf life, and supports premium pricing for imports such as Norwegian salmon and Australian chilled beef. Operators capture new revenue without major capital outlay, so hybrid services should keep widening until dedicated food-only fleets lose cost competitiveness.

Corporate Scope-3 Emission Audits Prompting Supplier Consolidation

Nestle Japan, Unilever, and peer producers have cut carrier counts from 15-20 to as few as five strategic partners, achieving 12-18% carbon-intensity improvement per ton-kilometer. Carriers offering real-time CO₂ dashboards, electric trucks, and LNG tractors win multi-year contracts that guarantee baseline volumes and co-fund decarbonization pilots. The trend erects entry barriers for small regional haulers lacking measurement capacity and accelerates roll-up activity as larger 3PLs buy route density.

Ageing Population Driving High-Frequency Small-Lot Chilled Runs

Japan’s over-65 cohort reached 29.1% of the population in 2025, and their e-grocery baskets are 60% smaller yet ordered more than twice as often. Providers respond with micro-fulfillment centers inside five-kilometer radii of high-density elderly neighborhoods, temperature-controlled lockers, and AI route engines that remix stops hourly. Success hinges on balancing delivery frequency with chilled load consolidation, an area where algorithmic dispatch and pharmaceutical-grade multipoint tracking deliver measurable fuel and labor savings.

National Food-Security Stock Freezer Initiatives

The 2024 food-security program funds 180,000 pallet positions at -25 °C across 12 regional reserve hubs, underwriting 50% of capex and 30% of annual opex, provided operators rotate inventory through commercial channels before sell-by dates[2]“Cold Chain Infrastructure Development and Food Supply Systems,” Ministry of Agriculture, Forestry and Fisheries (MAFF), maff.go.jp . Cold-store providers gain long-term occupancy guarantees that stabilize revenue while delivering overflow capacity for private customers during seasonal peaks. Government rotation rules also create predictable outbound flows into retail and food-service channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Insurance Premiums Covering Temperature Excursions | -0.5% | National, with higher impact on long-haul refrigerated transport | Short term (≤ 2 years) |

| Constrained Grid Connections for High-Power Refrigeration | -0.7% | Metropolitan and industrial zones with aging electrical infrastructure | Medium term (2-4 years) |

| Night-Time Delivery Noise Ordinance Constraints | -0.4% | Urban residential areas and mixed-use districts | Long term (≥ 4 years) |

| Delayed Certification Pipeline for HFC-Free Cooling Systems | -0.3% | National, affecting new facility construction and equipment replacement cycles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Insurance Premiums Covering Temperature Excursions

Premiums for cold-chain cargo jumped 35-50% between 2024 and 2025, with underwriters insisting on continuous IoT monitoring and documented contingency plans. Claims now average USD 180,000 per incident, prompting small fleets either to absorb margin-sapping policy costs or risk operating uninsured. Large 3PLs respond with predictive maintenance and dual-compressor trailers that satisfy insurer checklists and wave through at lower rates.

Constrained Grid Connections for High-Power Refrigeration

Connecting a new automated freezer can take 8-14 months and cost USD 1.5-3.5 million in transformer upgrades because 1970s-era substations sit near load limits around Tokyo Bay, Osaka Bay, and Nagoya corridors[3]“Energy and Infrastructure Policy,” Ministry of Economy, Trade and Industry, meti.go.jp. Project delays erode IRR and trigger developer hesitancy despite soaring demand. On-site solar and battery storage help, but cannot yet substitute a full grid supply at the required megawatt scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Value-Added Operations Command Premium Growth

Transportation retained 45.72% of the Japan food logistics market share in 2025, anchored by the country’s intricate road network that supports the daily replenishment of thousands of convenience stores. Yet value-added services are the clear pace-setter, growing at 6.55% CAGR as manufacturers push postponement to the edge of consumption and outsource blast freezing, labeling, and kitting to logistics specialists. The Japan food logistics market size tied to warehousing also rises as automated multi-temperature DCs blend storage with light processing, enabling next-day ecommerce grocery fulfillment in megacities.

Rail freight’s renaissance on the Hokkaido-Honshu corridor now shaves 15-25% off unit cost versus trucking for bulk frozen cargo, while sea transport covers inter-island lanes and bulk imports. Air remains a boutique channel for premium perishables such as uni and Pacific bluefin tuna, where shelf-life economics justify charter rates. Together, multimodal options give shippers flexibility to match speed, cost, and carbon objectives without compromising cold-chain integrity.

By Temperature-Control Type: Cold Chain Dominance Intensifies

Cold chain already accounts for 65.59% of the Japan food logistics market size in 2025 and is adding value at a 5.41% CAGR, proving that chilled and frozen categories underpin both current scale and incremental growth. Frozen storage below 0 °C is the largest node, reflecting Japan’s established frozen-food culture, but chilled services at 2-8 °C now outpace in growth thanks to meal-kit platforms and same-day grocery apps. Unified multi-temperature DCs let operators co-locate frozen shrimp, chilled yogurt, and ambient rice crackers, maximizing cube utilization and route density while simplifying compliance under the Food Sanitation Act[4]“Industry Overview,” Japan Frozen Food Association, reishokukyo.or.jp.

Ambient logistics remains indispensable for shelf-stable sauces and ready-to-drink tea, though brand owners increasingly book climate-controlled space to extend shelf life and guard against summer heat spikes. Digital thermologgers embedded across fleets generate granular audit trails that regulators and brand QA teams now expect as standard.

By End-Product Category: Pet Food Premiumization Reshapes Handling Requirements

Meat, seafood, and poultry retained 32.26% of 2025 volumes, powered by national protein preferences and tight safety regulations that lock in refrigerated flows. However, pet food outpaces every other category, expanding at a 6.84% CAGR as owners embrace chilled fresh meals and raw frozen diets. These SKUs demand segregation from human food, different HACCP documentation, and sometimes species-specific pathogen testing, prompting logistics providers to build dedicated chambers and color-coded workflow protocols.

Dairy and frozen desserts post steady gains on the back of premium cheese imports and health-oriented yogurt launches, while horticulture flows grapple with ethylene sensitivity that forces separated loading plans. Processed foods maintain scale but face margin pressure as consumers gravitate toward “fresh chilled” alternatives, nudging manufacturers to tender new cold-chain lanes that raise overall demand for refrigerated space across the Japan food logistics market.

Geography Analysis

Greater Tokyo, Osaka-Kobe, and Nagoya collectively absorb nearly 65% of national food demand, anchoring the densest concentration of refrigerated warehouses and cross-docks along coastal arterial highways. The Tokyo Bay cluster hosts massive import flows of frozen seafood and fresh produce, leveraging nearby Chiba and Kanagawa freezer complexes for immediate customs clearance and same-day store replenishment. Osaka Bay mirrors that model for western Honshu, while simultaneously channeling transshipment traffic linking South Korea and eastern China feeders.

Hokkaido supplies dairy, grains, and seafood to the mainland, relying on ferry and dedicated reefer rail services that maintain 18-24-hour door-to-door integrity from Sapporo farms to Tokyo depots. Kyushu ports specialize in Asian import consolidation and livestock outbound flows, underpinned by new cold-stores in Fukuoka and Kagoshima that shorten pick-to-ship cycles for pork exporters.

Secondary cities Sendai, Hiroshima, Sapporo, and Fukuoka use municipal incentives to develop regional temperature-controlled hubs. These platforms support direct-to-consumer channels outside megacity catchments, reduce empty backhauls, and serve as disaster-resilience nodes under national food-security doctrine. Such geographic diversification disperses capacity stress away from the traditional Tokaido corridor and broadens the operational footprint of the Japan food logistics market.

Competitive Landscape

The Japan food logistics market displays moderate concentration: the top five operators Yamato Transport, Nippon Express, Nichirei Logistics, Senko Group, and Konoike Transport collectively control about 40-45% of revenue, leaving ample headroom for regional specialists and technology-led entrants. Incumbents wield end-to-end service portfolios spanning road, rail, sea, and air, plus automated DC networks that enable one-invoice solutions attractive to brand owners slimming their carrier lists.

Digital capability and sustainability differentiation now trump simple scale. CargoWise adoption by major forwarders standardizes workflow, improves customs cycle times, and opens APIs for CO₂ tracking dashboards that feed directly into shippers’ Scope-3 reports. Electric light-commercial vehicle pilots in Tokyo suburbs cut noise and emissions for last-mile chilled drops, while LNG-powered tractors serve trunk lanes between Tokyo, Nagoya, and Osaka.

Strategic maneuvers include Mitsui’s buy-out of HAVI Supply Chain to penetrate the quick-service restaurant vertical, Yamato’s dedicated cargo plane launch for overnight fresh-food e-commerce, and DHL’s partnership with Temu to tie cross-border grocery sellers into its cold-chain network. M&A remains active as well-capitalized players scoop up family-owned cold-stores in Kyushu and Tohoku, raising the Japan food logistics market entry hurdle for newcomers without established infrastructure.

Japan Food Logistics Industry Leaders

Yamato Transport Co., Ltd.

Nippon Express Holdings Inc.

Nichirei Logistics Group Inc.

Konoike Transport Co., Ltd.

Senko Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group and Temu formed a strategic alliance to fast-track cross-border e-grocery fulfillment into Japan, integrating temperature-controlled air and road legs for specialty foods.

- December 2024: Nippon Express introduced Protect Box Global, a real-time monitored insulated packaging solution aimed at premium food and pharmaceutical exporters.

- October 2024: Mitsui acquired HAVI Supply Chain Solutions for USD 180 million, adding nationwide quick-service restaurant logistics expertise to its portfolio.

- June 2024: Yamato Transport deployed its own cargo aircraft to accelerate overnight delivery of premium fresh foods across Japan.

Japan Food Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Water | |

| Air | |

| Warehousing and Storage | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat, Seafood, and Poultry |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) |

| Horticulture (Fresh Fruits and Vegetables) |

| Processed Food Products |

| Pet Food |

| Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.) |

| By Services | Transportation | Road |

| Rail | ||

| Sea and Inland Water | ||

| Air | ||

| Warehousing and Storage | ||

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat, Seafood, and Poultry | |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) | ||

| Horticulture (Fresh Fruits and Vegetables) | ||

| Processed Food Products | ||

| Pet Food | ||

| Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.) | ||

Key Questions Answered in the Report

How big will the Japan food logistics market be by 2031?

Forecasts indicate the Japan food logistics market size will reach USD 40.11 billion by 2031 under a 3.99% CAGR.

Which service category grows fastest through 2031?

Value-added operations such as blast freezing and labeling are projected to rise at 6.55% CAGR as manufacturers adopt postponement models.

What share does cold chain hold today?

Cold chain services covered 65.59% of 2025 revenue, confirming their central role in food safety and premiumization.

Why are insurance costs rising for refrigerated cargo?

Temperature-excursion claims have pushed insurers to lift premiums 35-50% and require real-time IoT monitoring before underwriting policies.

Which end-product category is the new growth hotspot?

Pet food logistics is expanding at 6.84% CAGR as owners shift to refrigerated fresh meals and frozen raw diets.

How are ports cutting dwell times for reefer boxes?

Digital customs pre-clearance, IoT temperature tracking, and truck slot-booking systems have reduced average reefer dwell time to 3.4 days, saving both energy and demurrage.

Page last updated on: