United Arab Emirates Structural Steel Fabrication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

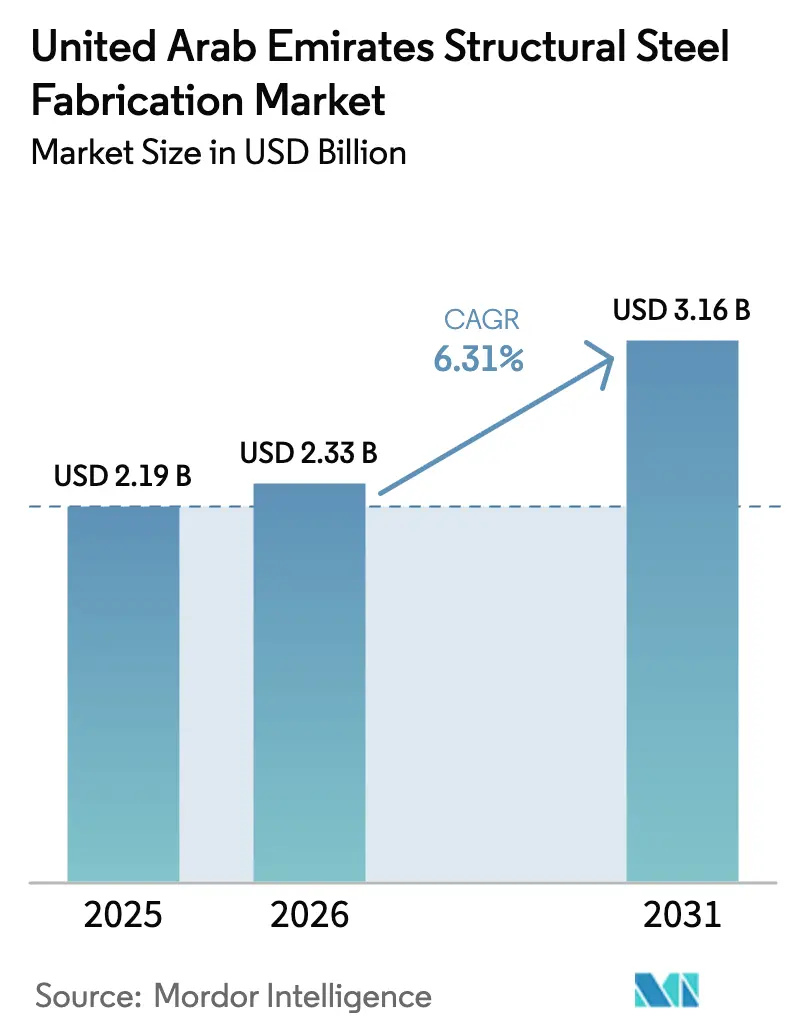

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 3.16 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

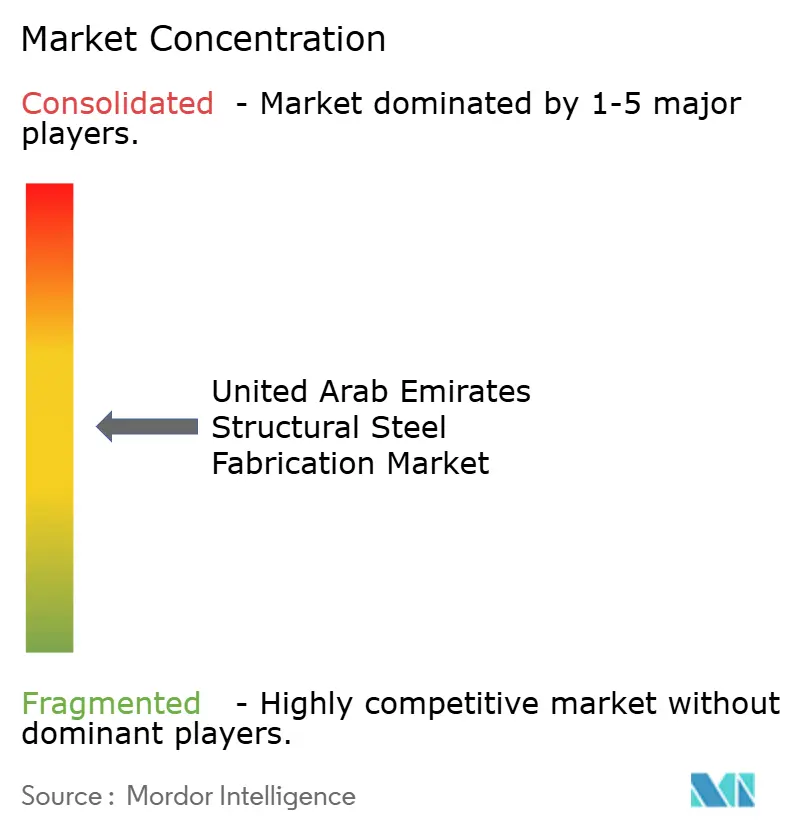

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Structural Steel Fabrication Market Analysis by Mordor Intelligence

The UAE structural steel fabrication market size is expected to grow from USD 2.19 billion in 2025 to USD 2.33 billion in 2026 and is forecast to reach USD 3.16 billion by 2031 at 6.31% CAGR over 2026-2031. This growth aligns with the UAE's "Operation 300 billion" initiative, driven by investments in infrastructure and industrial zones. Projects like the Etihad Rail's high-speed network are boosting demand for beams, columns, and bridge components. Emirates Steel, Arkan, and Masdar's renewable hydrogen-based green steel production is creating new opportunities. Heavy sections dominate sales, while plate-worked girders and custom modules are expected to grow rapidly. The construction sector holds the largest end-user share, with the power and energy segment expanding swiftly. Abu Dhabi leads in revenue, while other emirates show stronger growth. Welding remains significant, but automated cutting lines are gaining traction. The market faces challenges such as steel price volatility, a late-2024 rebar price hike, and a shortage of certified welders. Federal subsidies and recycled-content mandates under Estidama and Dubai Green Building codes are mitigating these issues and supporting growth.

Key Report Takeaways

- By product type, heavy sections led with 38.52% UAE structural steel fabrication market share in 2025, while the Other Product Types segment is projected to expand to a 8.92% CAGR through 2026-2031.

- By End-User Industry, construction contributed 46.12% of 2025 revenue, while the Power & Energy segment is projected to expand at a 9.18% CAGR through 2026-2031.

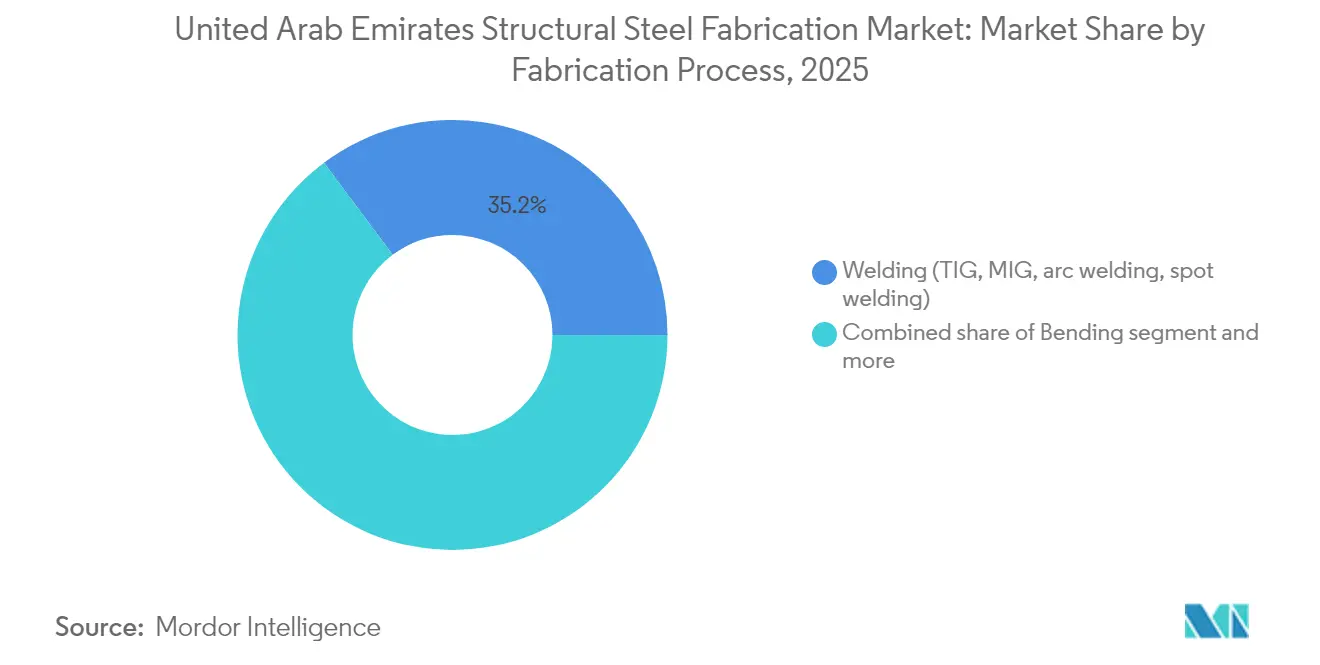

- By Fabrication Process, welding accounted for 35.20% of 2025 revenue, while cutting technologies are expected to advance at an 8.55% CAGR through 2026-2031.

- By Geography, Abu Dhabi held 38.21% of market revenue in 2025, while the Rest of the UAE region is forecast to grow at an 8.43% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mega-projects pipeline (Etihad Rail, Hyperloop, Expo legacy) | 2.1% | National, with concentration in Abu Dhabi-Dubai corridor | Long term (≥ 4 years) |

| Diversification into renewable energy & green hydrogen hubs | 1.5% | Abu Dhabi (Al Dhafra, Masdar City), Dubai (Mohammed bin Rashid Al Maktoum Solar Park) | Long term (≥ 4 years) |

| Adoption of BIM-mandated public projects | 1.2% | Dubai, Abu Dhabi, with spillover to Northern Emirates | Medium term (2-4 years) |

| Tourism-led demand for mixed-use high-rise steel structures | 0.9% | Dubai, Abu Dhabi, Ras Al-Khaimah coastal zones | Medium term (2-4 years) |

| Federal subsidies for automated/robotic fabrication lines | 0.8% | National, early adoption in Abu Dhabi and Dubai industrial zones | Short term (≤ 2 years) |

| Mandatory recycled-content targets under Estidama & Dubai Green Building codes | 0.5% | Abu Dhabi (Estidama), Dubai (Al Sa'fat), expanding to other Emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Mega-Projects Pipeline

The USD 39.44 billion (AED 145 billion) GDP contribution expected from Etihad Rail’s high-speed network illustrates the structural steel intensity of transport infrastructure. Station concourses, depot buildings, and bridge girders collectively require hundreds of thousands of tons of fabricated components. Dubai’s exploratory agreement with The Boring Company for the Dubai Loop and the next phase of Al Maktoum International Airport’s 70 square-kilometer expansion add parallel demand tracks. Each mega-project follows a phased schedule that offers fabricators multi-year revenue visibility, justifying investment in automated beam lines and robotic fitting cells that sharpen competitiveness in the UAE structural steel fabrication market[1]Shadi Malak, “Etihad Rail Stage 2 Project Brief,” Etihad Rail, etihadrail.ae.

Diversification into Renewable Energy & Green Hydrogen Hubs

EMSTEEL’s 31.5 MWp rooftop solar facility and Fertiglobe’s 1 million-ton low-carbon ammonia plant epitomize the emerging steel intensity of renewable assets. The USD 31.82 billion (AED 117 billion) UAE-Oman green metals investment package elevates trans-GCC fabrication collaboration. Structures compatible with hydrogen embrittlement requirements and cryogenic storage impose higher metallurgical standards, favoring incumbents with advanced welding qualifications. Federal programs under Operation 300 billion escalate local value-addition targets, further anchoring renewable energy steel demand inside the UAE structural steel fabrication market.

Adoption of BIM-Mandated Public Projects

Dubai’s decision to lower its BIM threshold to buildings over 20 floors and facilities exceeding 200,000 square feet rewired project workflows. Early movers that align fabrication data directly with BIM models reduce material waste by up to 15% and shorten lead times, providing owners with tangible cost savings. The launch of BuildingSMART International’s first Middle East chapter in the UAE cements the national intent to standardize digital collaboration protocols. ISO-certified contractors already capture preferential tender status, and fabricators outfitted with cloud-integrated cutting and welding robots enjoy seamless model-to-shop interoperability. These advantages are increasingly decisive as contractors pursue supertall towers and intricate mixed-use complexes in Dubai's growth corridors[2]Dawoud Al-Hajri, “Revised BIM Requirements for Building Permits 2024,” Dubai Municipality, dm.gov.ae.

Tourism-Led Demand for Mixed-Use High-Rise Steel Structures

Sphere Abu Dhabi’s 20,000-seat immersive arena and a pipeline of supertall residential towers exceeding 450 meters require bespoke steel framing with stringent tolerance control. Developers are pivoting to off-site modular production to compress schedules; consequently, the prefabricated construction market is projected to hit USD 10.01 billion (AED 36.8 billion) by 2028. Fabricators providing corrosion-resistant coatings and green-certified alloys command premium pricing on coastal projects in Ras Al-Khaimah and Fujairah. The trend broadens the UAE structural steel fabrication market beyond core metro regions and allows capacity optimization across multiple emirates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global steel price volatility & logistics shocks | -1.8% | National, with higher impact on import-dependent Northern Emirates | Short term (≤ 2 years) |

| Shortage of certified welders & fabricators | -1.1% | National, acute in Abu Dhabi and Dubai industrial zones | Medium term (2-4 years) |

| EU-style carbon border adjustment on embedded CO₂ | -0.9% | National, primarily affecting export-oriented fabricators | Medium term (2-4 years) |

| Price-led competition from KSA & Indian fabricators | -0.7% | National, with higher impact on commodity-grade fabrication segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Steel Price Volatility & Logistics Shocks

Rebar prices climbed USD 25–29.9 per ton in late 2024 as global freight bottlenecks squeezed raw-material inflows. Although 25% U.S. tariffs diverted surplus steel to the Gulf, aggressive price competition from Turkish and Chinese mills pressured local margins. Congestion at Jebel Ali and specialty grade lead-time spikes forced fabricators to raise inventory buffers, inflating working capital. EU carbon border certificates starting in 2026 add cost to export-oriented producers, prompting accelerated investment in lower-carbon EAF routes and recycled scrap uptake as hedging mechanisms[3]Andrew Griffiths, “EU Carbon Border Adjustment Mechanism: Implications for GCC Steel,” Carbon Trust, carbontrust.com.

Shortage of Certified Welders & Fabricators

The UAE imported 25% more skilled workers from India in 2024, yet vacancy rates remain high in advanced welding disciplines, especially for hydrogen and offshore wind projects. Wage premiums, schedule risk, and quality concerns follow. The Industrialists Program is rolling out accredited training, but tangible supply-side relief is not expected before 2027. Consequently, fabricators pivot to collaborative welding cobots and augmented-reality training platforms that standardize quality and partly mitigate labor scarcity in the UAE structural steel fabrication market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Anchor Mega-Project Demand

In 2025, heavy sections, including beams and columns, hold a 38.52% market share, driven by the UAE's focus on infrastructure and high-rise projects. The Etihad Rail network's need for heavy structural components supports this segment's dominance. Other product types, such as plate-worked girders, trusses, custom-built modules, and skids, are growing at a 8.92% CAGR through 2031, supported by renewable energy and modular construction applications.

The UAE's shift toward advanced engineering solutions is evident in projects like Fertiglobe's 1 million ton per year low-carbon ammonia facility, which drives demand for custom-built modules. Tubular and hollow sections are used in Dubai's mixed-use developments, while light sectional and cold-formed members support the prefabricated construction market, projected to reach AED 36.8 billion by 2028. ISO 9001 and EN 1090 certifications are increasingly vital for fabricators, with companies like Automech Steel focusing on compliance to capitalize on the growing specialized components market

By End-User Industry: Construction Leads Amid Energy Upswing

The construction sector contributed 46.12% to overall revenue in 2025, underpinned by Dubai’s 2040 Urban Master Plan and Abu Dhabi’s USD 2.72 billion (AED 10 billion) industrial strategy. Skyscrapers, theme parks, and entertainment venues drive continuous orders for floor beams, composite decks, and long-span roof trusses. Infrastructure transport is set to record a 9.18% CAGR through 2031 as the Dubai Metro Blue Line and Etihad Rail consume fabricated bridge arches, tunnel liners, and station envelopes. Renewable power plants, including the Mohammed bin Rashid Solar Park and Al Dhafra wind complex, accelerate energy-sector demand at a 9.18% clip, demanding corrosion-resistant alloys and precision-cut stiffeners.

Commercial hospitality expansions, such as Sphere Abu Dhabi, force fabricators to integrate acoustic isolation and vibration control hardware into assemblies. Industrial facilities, buoyed by customs exemptions worth USD 1.06 billion (AED 3.9 billion), underpin a steady stream of warehouse, logistics, and light-manufacturing buildings. ADNOC’s blue hydrogen build-out adds process equipment skids, pipe racks, and pressure vessel shells, reinforcing segment diversity. Together, these shifts reinforce the UAE structural steel fabrication market’s balanced sectoral exposure and limit downside risk linked to any single demand vertical.

By Fabrication Process: Welding Holds Lead While Cutting Surges

Welding preserved 35.20% of revenue in 2025 due to its ubiquity in beams, columns, and box-girder assembly. Hydrogencapable weld procedures, dual-shielded flux-core wires, and robotic fillet stations gain traction as owners tighten performance criteria. Meanwhile, advanced cutting posted the fastest 8.55% CAGR forecast, propelled by fiber-laser adoption that delivers kerf accuracy below 0.1 millimeter, essential for turbine towers and prefabricated façade kits. CNC plasma tables integrate with BIM shops, transmitting nesting files directly from design to torch and minimizing scrap.

Bending and forming processes scale alongside light-gage modular volumes, feeding panelized hotel rooms and bathroom pods. Machining services grow as renewable energy projects specify tighter tolerance flanges and pin connections. Surface treatment capacity follows suit, shifting to eco-friendly coatings that satisfy Estidama emissions limits. Government subsidies covering 15% of automation costs shorten return periods for integrated beam lines and collaborative welding cells, making capital investment in Industry 4.0 technology financially viable across the UAE structural steel fabrication market size spectrum.

Geography Analysis

Abu Dhabi retained 38.21% of the UAE structural steel fabrication market size in 2025, reflecting deep industrial roots anchored by oil and gas, petrochemicals, and state-backed renewable energy ventures. The emirate’s plan to double manufacturing output to USD 46.78 billion (AED 172 billion) by 2031 assures fabricators of sustained baseline demand. Energy-price incentives and long-term industrial land leases enhance cost competitiveness. Masdar City’s green hydrogen pilots and Al Dhafra’s utility-scale solar arrays generate large-tonnage orders for corrosion-resistant beams, lattice towers, and equipment skids.

Dubai remains a construction powerhouse, fueling demand through supertall towers and the preliminary Dubai Loop dig. BIM mandates reward digitally mature suppliers capable of model-driven production. Modular hotel chains expanding under the city’s tourism strategy prefer factory-finished steel pods that minimize site disruption. Free-zone import-duty exemptions and stable power tariffs further cultivate a receptive environment for fabricators seeking export staging points, reinforcing Dubai’s share of the UAE structural steel fabrication market.

Sharjah, Ras Al-Khaimah, Fujairah, and Ajman collectively map the fastest 8.43% CAGR through 2031. Hamriyah Free Zone’s 6,500 companies drive multiproduct demand, from conveyor galleries to port cranes. Ras Al-Khaimah’s 35% manufacturing GDP share encourages specialized structural steel orders for cement and ceramics plants. Fujairah’s multipurpose ports shorten lead times to India and East Africa, offering export-oriented fabricators logistically efficient bases. Local governments provide discounted utility packages and ready-built industrial shells, reducing entry hurdles and spreading the UAE structural steel fabrication market footprint across all seven emirates.

Competitive Landscape

The UAE structural steel fabrication market shows moderate concentration with technology adoption as the primary differentiator. EMSTEEL redirected USD 204 million toward Industry 4.0 upgrades, installing robotic beam welding lines, AI-enabled defect detection, and digital twin platforms that cut rework by 20%. The company’s partnership with Masdar to produce green steel via renewable hydrogen secures a first-mover premium in projects with strict embodied-carbon benchmarks. Emirates Global Aluminium, named a World Economic Forum Lighthouse, achieved 50% downtime reduction through advanced analytics, validating the ROI case for data-driven operations.

Competitors increasingly vertically integrate, securing coil supply, in-house galvanizing, and logistics fleets to hedge raw-material volatility. Mid-tier fabricators adopt collaborative welding cobots displayed at SteelFab 2025 to offset labor shortages and ensure consistent quality. Niche players differentiate through EN 1090 execution class 4 certification, targeting nuclear and offshore wind projects, while others cultivate expertise in prefabricated volumetric modules for hotel operators. Overall, sustaining relevance in the UAE structural steel fabrication market requires digital maturity, ESG compliance, and rapid response capability supported by predictive scheduling tools.

United Arab Emirates Structural Steel Fabrication Industry Leaders

Arabian International Company Ras Al Khaimah

Mabani Steel LLC

IMCC

Standard Steel Fabrication Co LLC

Techno Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EMSTEEL joined Make it in the Emirates 2025 as Metals & Fabrications sector partner, reinforcing its zero-carbon production roadmap and export reach to 72 countries.

- March 2025: EMSTEEL partnered with Yellow Door Energy on a 31.5 MWp rooftop solar system across 40 roofs in ICAD 1, Abu Dhabi, cutting 16,000 tonnes CO₂e annually.

- February 2025: Dubai signed a preliminary agreement with The Boring Company to study the Dubai Loop high-speed underground system, signaling potential steel demand for tunnel liners and station structures.

- April 2024: UAE and Oman firms closed a USD 31.82 billion renewable energy and green metals package that positions Emirates Steel Arkan and Emirates Global Aluminium at the heart of GCC green-steel trade.

United Arab Emirates Structural Steel Fabrication Market Report Scope

Structural steel fabrication is the process of bending, cutting, and modeling steel to create a structure. For structural steel fabrication, steel parts are often put together to create different structures of predefined sizes and shapes.

The UAE structural steel fabrication market is segmented by end-user industry (manufacturing, power and energy, construction, oil and gas, and other end-user industries) and product type (heavy sectional steel, light sectional steel, and other product types). The report offers market sizes and forecasts for the UAE structural steel fabrication market in value (USD) for all the above segments.

The report offers the market sizes and forecasts for the UAE structural steel fabrication market in value (USD) for all the above segments.

| Heavy Section(Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrastructure (Transport) | |

| Power & Energy (include utilities and renewable energy) | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation (railways systems, metro components, etc.) | |

| Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) |

| Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) |

| Bending (Press brakes, roll bending, rotary bending) |

| Welding (TIG, MIG, arc welding, spot welding) |

| Machining (Milling, turning, drilling, grinding, CNC machining) |

| Forming (Stamping, forging, rolling, hydroforming) |

| Casting (Sand casting, die casting, investment casting) |

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) |

| Abu Dhabi |

| Dubai |

| Sharjah |

| Ras Al-Khaimah |

| Rest of UAE |

| By Product Type | Heavy Section(Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-user Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrastructure (Transport) | ||

| Power & Energy (include utilities and renewable energy) | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation (railways systems, metro components, etc.) | ||

| Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) | ||

| By Fabrication Process | Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) | |

| Bending (Press brakes, roll bending, rotary bending) | ||

| Welding (TIG, MIG, arc welding, spot welding) | ||

| Machining (Milling, turning, drilling, grinding, CNC machining) | ||

| Forming (Stamping, forging, rolling, hydroforming) | ||

| Casting (Sand casting, die casting, investment casting) | ||

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) | ||

| By Geography | Abu Dhabi | |

| Dubai | ||

| Sharjah | ||

| Ras Al-Khaimah | ||

| Rest of UAE | ||

Key Questions Answered in the Report

What is the 2026 value of the UAE structural steel fabrication market?

The UAE structural steel fabrication market stands at USD 2.33 billion in 2026.

How fast is the market expected to grow by 2031?

It is projected to reach USD 3.16 billion, registering a 6.31% CAGR through 2031.

Which product type leads the market?

Heavy sections hold the top position with 38.52% market share in 2025.

Which end-user segment will expand the quickest?

Power and energy applications are forecast to grow at a 9.18% CAGR to 2031.

Page last updated on: