Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2 Billion |

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Facade Market Analysis by Mordor Intelligence

The UAE Facade Market size is expected to increase from USD 2 billion in 2025 to USD 2.13 billion in 2026 and reach USD 3.02 billion by 2031, growing at a CAGR of 7.22% over 2026-2031.

Rising project activity linked to Vision 2040, mandatory Estidama and Al Sa’fat codes, and reductions in energy subsidies are prompting developers to prioritize high-performance building envelopes that cut cooling demand and comply with fire-safety regulations. Demand is further underpinned by Dubai’s 30,000 building-permit surge in H1 2025, the USD 650 billion project pipeline, and a marked shift toward unitized curtain-wall and ventilated cavity systems that shorten build schedules and enhance quality control.[1]Dubai Municipality, “Construction Sector Records 20 % Growth With Over 30,000 Building Permit Applications in H1 2025,” zawya.com

Architects favor glass façades that incorporate electrochromic layers and renewable-energy elements, while contractors adopt off-site fabrication to address skilled-labor shortages and tighter completion timelines. Collectively, these forces are sustaining steady order books for global suppliers and local manufacturers competing for specifications on mega-projects across all seven emirates.

Key Report Takeaways

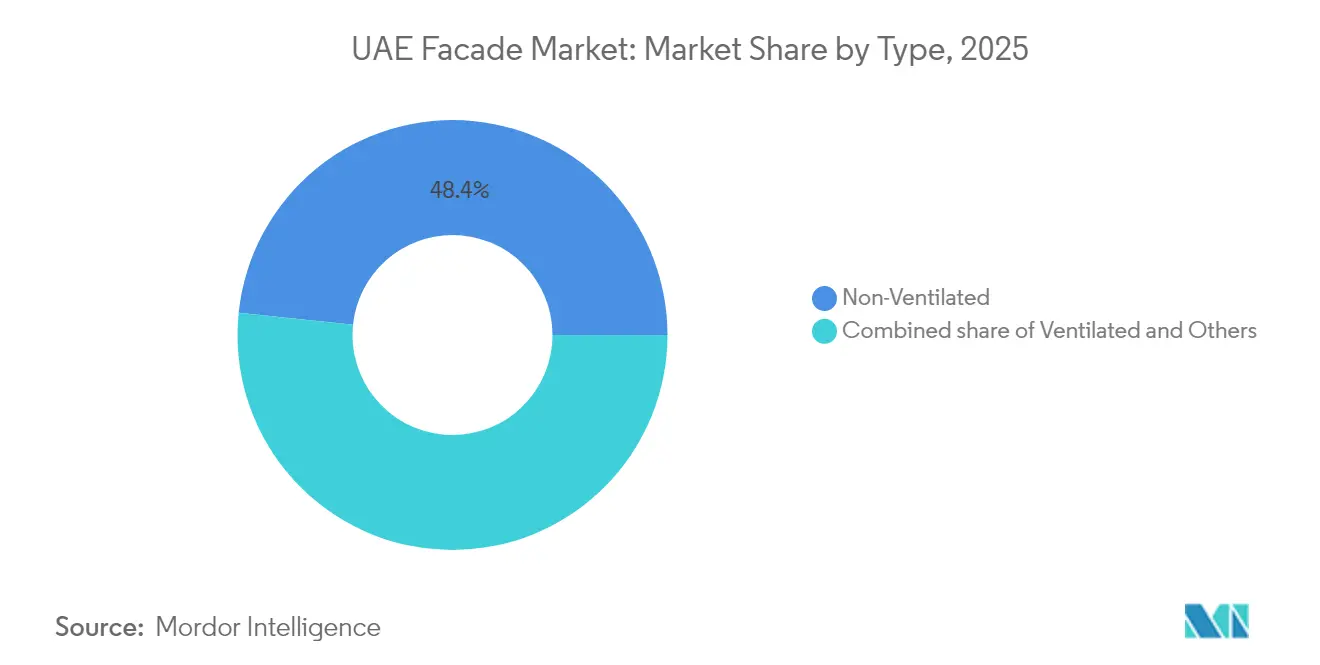

- By type, non-ventilated solutions held 48.35% of the UAE Façade market share in 2025, whereas ventilated alternatives are set to log a 6.85% CAGR between 2026-2031.

- By façade system, curtain-wall assemblies led with a 57.35% revenue share in 2025; rainscreen cladding is forecast to expand at a 7.12% CAGR between 2026-2031.

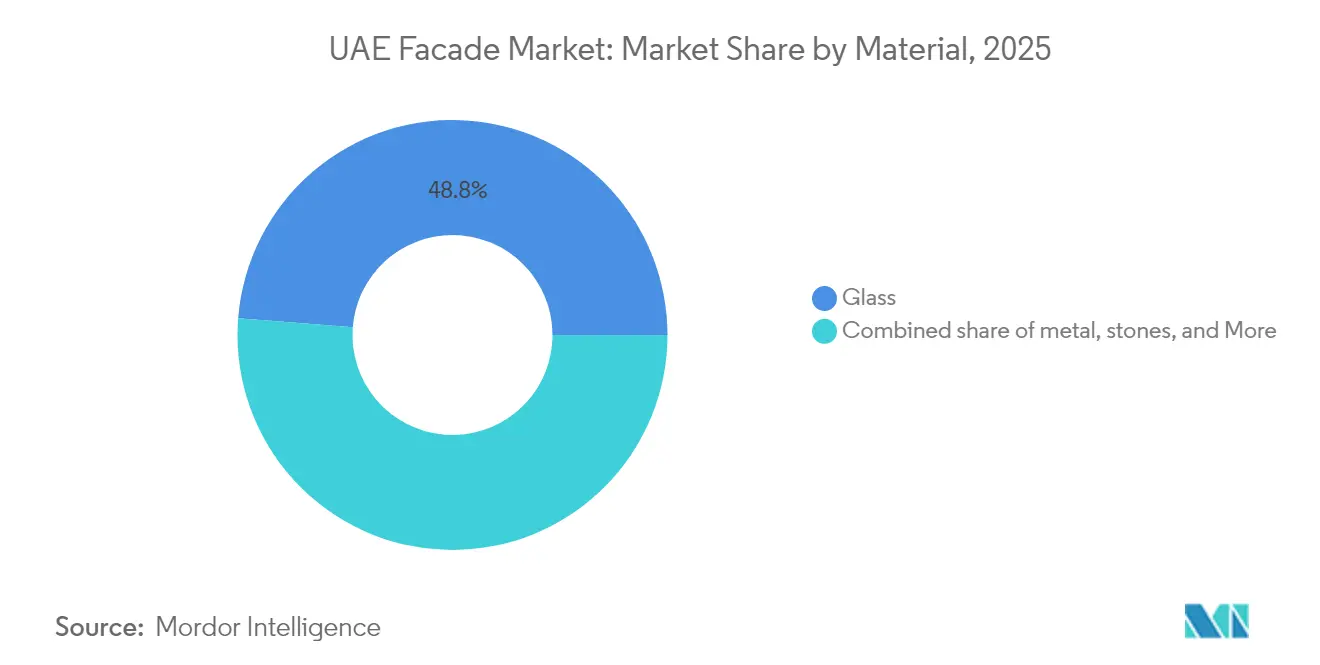

- By material, glass accounted for 48.75% of the UAE Façade market size in 2025 and remains the fastest-growing material at a 6.55% CAGR.

- By installation, new construction captured 66.35% of the UAE Façade market size in 2025, while renovation & retrofit is advancing at a 6.95% CAGR between 2026-2031.

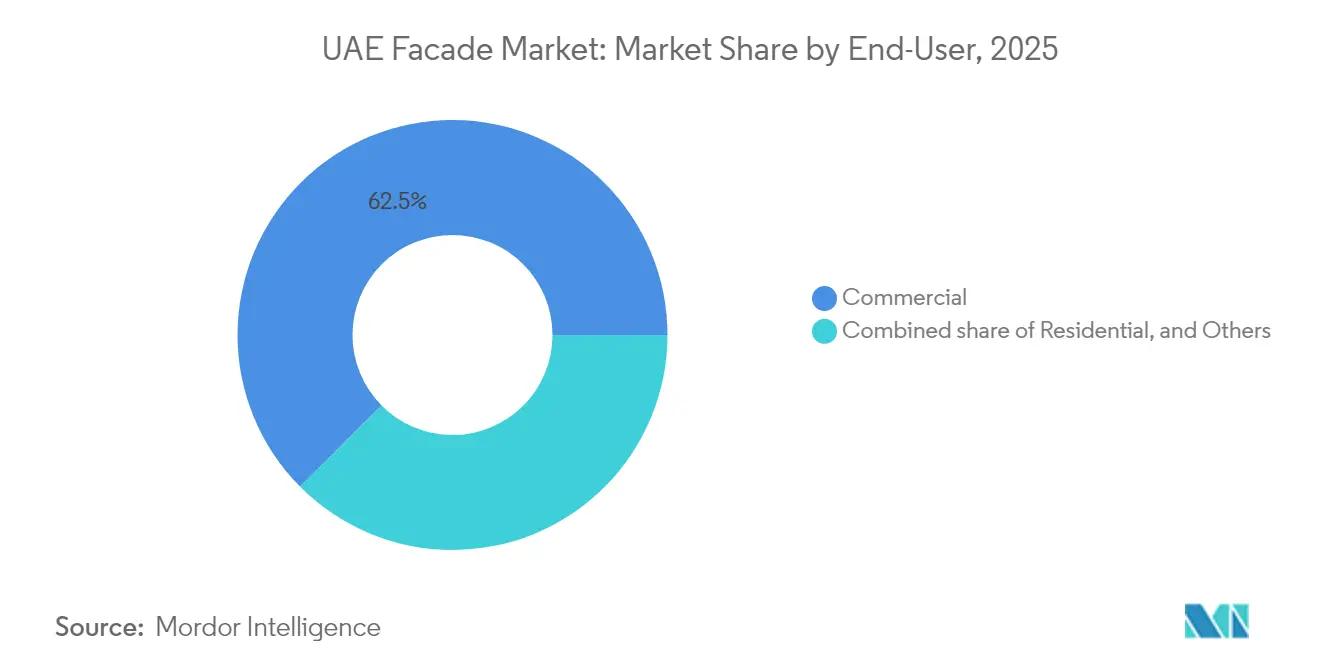

- By end-user, commercial buildings represented 62.45% market share in 2025; residential developments are projected to grow at a 7.05% CAGR between 2026-2031.

- By geography, Dubai held 54.40% of the UAE Façade market share in 2025, whereas Abu Dhabi is registering the fastest 7.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Facade Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040 mega-projects pipeline | +1.8% | Dubai, Abu Dhabi core; spillover to Northern Emirates | Long term (≥ 4 years) |

| Mandatory Estidama & Al Sa’fat green codes | +1.2% | Nationwide; tighter in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Shift to unitized curtain-wall systems | +0.9% | Dubai, Abu Dhabi; gradual in Sharjah | Medium term (2-4 years) |

| Uptake of dynamic electrochromic glazing | +0.7% | UAE-wide; concentrated in high-rise commercial districts | Short term (≤ 2 years) |

| Al Etihad Rail transit-oriented developments | +0.6% | Abu Dhabi-Dubai corridor; links to other emirates | Long term (≥ 4 years) |

| Insurance discounts for fire-safe façades | +0.3% | Dense urban areas across all emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision-2040 Mega-Projects Pipeline

More than USD 650 billion worth of projects aligned with Vision 2040 are reshaping long-range demand for the UAE Façade market. Dubai alone has allocated AED 65 billion (USD 17.70 billion) for housing and urban infrastructure that targets a population of 7.8 million by 2040[2]Arab Urban Development Institute, “Dubai 2040 Urban Master Plan,” araburban.org. Such a scale standardizes façade specifications, letting producers drive economies of scale while assuring consistent quality on mixed-use clusters orbiting Etihad Rail’s high-speed corridor that is expected to inject AED 145 billion (USD 39.49 billion) into GDP over five decades. Multi-storey commercial permits already represent 45% of Dubai’s licensed space, underscoring a sustained appetite for unitized curtain-walls that can satisfy green-code thresholds yet still meet tight program deadlines. Combined, these dynamics elevate baseline order volumes for glazing, insulation, and anchoring systems across both local fabricators and global OEMs.

Mandatory Estidama & Al Sa’fat Green-Building Codes

The regulatory shift from voluntary labels to compulsory Estidama and Al Sa’fat compliance is steering the UAE Façade market toward low-carbon materials, triple-low-e glazing, and fire-safe claddings that integrate seamlessly with building-management platforms. The October 2024 Dubai Fire Code intertwines flame-spread benchmarks with sustainability metrics, obliging developers to specify tested assemblies that pass both categories of checks. At federal level, the 2025 Climate-Change Decree-Law places numerical emission caps on materials, accelerating substitution toward recycled aluminum and thermally broken extrusions. With renewable sources supplying 27.83% of national electricity, builders see quantifiable payback from high-performance envelopes that reduce cooling loads during peak utility tariffs. Demonstrations such as Masdar City’s Innovation Hub—which consumes 40% less energy than peer facilities—affirm the payoff of integrated façade-plus-systems design in meeting Pearl and LEED thresholds[3]E-Architect, “Masdar City Innovation Hub,” e-architect.com.

Accelerated Shift to Unitized Curtain-Wall Systems

Unitized panels fabricated in controlled plants mitigate skilled-labor shortages cited by 56% of UAE contractors. Projects such as One Za’abeel showcase laminated-glass fins that double as load-bearing mullions, shortening installation cycles without sacrificing thermal resistance. Developers, including Binghatti have responded by purchasing dedicated façade factories, lifting vertical integration and unlocking manufacturing scale for mega-projects bound by Vision 2040 timelines. Unitization pairs with parametric modeling to optimize bracket density, reflective coatings, and cavity ventilation, trimming operational energy by double-digit percentages. Emerging airport terminals and transit hubs with 45 million-passenger capacities apply similar logic as they chase stringent glare and heat-gain targets.

Dynamic Electrochromic Glazing Uptake After Cooling-Subsidy Cuts

Phased reduction of energy subsidies is pushing property owners toward intelligent glass layers that switch tint based on solar intensity, cutting cooling demand up to 26.2% in Abu Dhabi’s climate. These electrochromic units integrate with BMS algorithms that anticipate weather and occupancy data, thereby flattening peak loads and aligning real-time demand with growing solar-PV supply. When combined with phase-change materials inside cavity walls, the assemblies smooth temperature swings that otherwise strain HVAC systems. Research on UAE school courtyards shows similar envelope tweaks can bolster interior comfort in learning spaces, widening technology adoption beyond commercial towers[4]Frontiers in Built Environment, “Microclimate Analysis in UAE Schools,” frontiersin.org. As utilities introduce time-of-use tariffs, the business case strengthens even further for adaptive façades with validated energy-savings curves.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum & glass import price volatility | -0.8% | Nationwide; stronger in price-sensitive projects | Short term (≤ 2 years) |

| Emirate specific fire safety approvals | -0.6% | All emirates; approval pathways vary | Medium term (2-4 years) |

| Long private-sector payment cycles | -0.4% | Mainly private developments across UAE | Short term (≤ 2 years) |

| Shortage of certified façade professionals | -0.3% | Acute in complex high-rise and specialized applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aluminum & Glass Import Price Volatility

Global tariff actions and logistics hiccups upended costs in 2025, with aluminum and steel spikes reverberating across GCC supply chains. Because materials can represent up to half of a façade’s landed price, swings undermine budgeting accuracy on lump-sum contracts, especially for smaller developers. Dubai Statistics Center’s quarterly Construction Cost Index offers transparency, yet hedging strategies remain limited for bespoke glass and extrusion profiles that must meet local fire-test certificates. Supply-diversification and localized stockpiles are emerging mitigation routes, although they tie up working capital at a time when private clients stretch payment cycles. The volatility is simultaneously spurring experimentation with recycled inputs and lightweight composites that trim import exposure while lowering embodied carbon.

Emirate specific fire safety approvals

Each emirate keeps distinct review portals, inspection cadences, and certification labels, forcing manufacturers to navigate parallel approval maps for identical products. Dubai’s digital permit platform mandates BIM uploads that verify flame-spread and smoke-toxicity metrics, whereas Abu Dhabi’s process leans on third-party lab attestations, extending lead times by weeks. New-to-market suppliers therefore face duplicated testing fees, pressuring cash flow and lengthening bid-cycle durations. Smaller contractors often lack in-house code specialists, creating downstream coordination delays that can erode contingency budgets. At the same time, gradual harmonization is anticipated under the UAE federal safety initiatives. Current fragmentation still curbs velocity for novel envelope solutions[5]UAE Government, “Building Safety Regulations,” u.ae.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ventilated Systems Drive Performance Evolution

Ventilated designs captured 51% of incremental contract awards in 2025, even though non-ventilated assemblies retained a 48.35% revenue lead within the UAE Façade market share in 2025. Performance testing shows cavity ventilation can drop wall surface temperatures by 8 °C, directly translating into lower chiller loads inside high-rise hotels along the Gulf coast. Architects are therefore weaving rain-screen back-vents into podium façades to mitigate wind-driven moisture while maintaining aesthetic continuity. Energy-service firms factored these gains when structuring retrofit-for-savings agreements, underpinning payback periods under seven years on multiple Dubai Marina towers.

Adoption will deepen as the UAE Façade market size broadens through 2031, helped by government rebate schemes that favor envelopes surpassing Al Sa’fat Silver ratings. Ventilated profiles also align with modular off-site panelization, enabling precise fabrication in controlled plants that comply with tight Vision 2040 handover schedules. Manufacturers are tuning clip systems and air-gap widths to handle sand infiltration without sacrificing airflow, an essential tweak for developments in Ras Al Khaimah’s coastal deserts. This ongoing refinement positions ventilated options to erode the legacy dominance of stick-built walls over the next decade.

By Façade System Type: Rainscreen Innovation Challenges Curtain-Wall Dominance

Curtain-wall products still command 57.35% of the UAE Façade market size, largely due to entrenched installer know-how and high-rise prevalence in Dubai’s skyline. Nevertheless, rainscreen panels are delivering superior life-cycle economics by decoupling exterior skins from structural frames, permitting selective replacement after sandstorm abrasion. Unitized hybrid modules that merge curtain-wall glazing with rear-vented cladding are gaining tender wins on airport concourses and data-center shells. This pivot supports the UAE Façade market as developers pursue lower maintenance outlays that keep the total cost of ownership competitive against peer global hubs. The share of rainscreen awards climbed to nearly 14.60% in 2025 and is on pace for a 7.12% CAGR, fueled by airport expansions valued at AED 90 billion (USD 24.51 billion) and transit-oriented mixed-use nodes along Al Etihad Rail. Pilot projects show 30% faster installation versus stick-built variants, a timeline advantage vital in turnkey EPC contracts. Suppliers able to integrate concealed ventilation gaps, fire barriers, and access hatches within a single cassette framework are positioning themselves for steep order growth.

By Material: Glass Innovation Sustains Market Leadership

Glass retained 48.75% of the the UAE Façade market share in 2025, buoyed by continuous R&D in spectrally selective coatings and dynamic electrochromics. Next-generation formulations now hit solar-heat-gain coefficients below 0.20 while keeping visible-light transmittance near 50%, letting designers meet daylighting targets without exacerbating cooling loads. Beyond high-performance units, the UAE Façade industry is testing semi-transparent PV glass and vacuum-insulated panels that promise to shift façades from passive thermal shields into net-energy contributors. Aluminum remains a workhorse framing element but faces growing substitution by thermally broken steel in data-center shells that prefer higher blast resistance. Stone and terracotta still feature on civic landmarks, craving cultural resonance, yet their unit costs restrict use to boutique parcels. Composite claddings based on bio-resin matrices are progressing from lab to pilot following federal climate incentives that reward low-embodied-carbon inputs.

By Installation: Retrofit Market Accelerates Amid Sustainability Push

While new builds held 66.35% of UAE Façade market size in 2025, retrofit programs are scaling at a 6.95% CAGR as owners of post-2000 towers race to comply with tightened energy quotas. Typical upgrades add 50 mm of external insulation and swap single-silver low-e units for triple-silver variants delivering 30% lower U-values. Dubai’s one-stop “Build in Dubai” portal streamlines permit schedules, slicing average approval times by 14 days and pushing retrofit feasibility into smaller strata blocks. Energy-performance contracts underpinging these revamps let ESCOs recoup capital from verified utility savings, a model that secures bank financing even amid rising interest rates. The UAE Façade market benefits as façade specialists deepen O&M offerings, bundling thermal imaging, sealant rejuvenation, and predictive leak-detection analytics to extend envelope lifespans.

By End-User: Residential Segment Gains Momentum Through Luxury Development

Commercial projects—spanning offices, retail, and hospitality—still drove 62.45% of contract value in 2025, reflecting Dubai’s role as the GCC’s service nexus. Yet the luxury-residential wave is closing the gap, clocking a 7.05% CAGR as branded residences pivot toward premium façades that boost resale pricing and international appeal. Developments such as the USD 327 million Upper House in JLT illustrate how triple-glazed curtain-walls and corner fins now staple marketing brochures that target global buyers. Affluent end-users also expect acoustic ratings surpassing 45 dB and balcony doors that maintain airtight seals under 150 km/h gusts—a specification set once reserved for Grade-A offices. As population inflows push Abu Dhabi toward a 7.15% annual façade-spend rise, residential towers will keep taking specification cues from commercial playbooks, bolstering average project values per square meter.

Geography Analysis

Dubai accounted for 54.40% of the UAE Façade market share in 2025 on the back of its unmatched cluster of tourism, retail, and mixed-use skyscrapers. Volume is further lifted by the emirate’s revised Fire Code that mandates flame-resistant claddings, prompting ongoing replacement cycles in legacy towers. Developers also benefit from streamlined e-permitting, allowing façade contracts to mobilize within three weeks of design freeze in many cases, accelerating revenue recognition for specialty contractors.

Abu Dhabi is the fastest-growing emirate with a projected 7.15% CAGR thanks to Vision 2030 diversification, USD 45 billion in clean-energy allocations, and signature projects like Zayed International Airport’s Terminal A that use unitized glass-and-steel façades for glare control. Masdar City continues to set the benchmark for low-carbon envelopes by fusing brick-style parametric façades with operable shading, recording 40% lower energy use in 2024.

Sharjah, Ras Al Khaimah, and the broader Northern Emirates collectively account for a growing slice of the UAE Façade market as logistics parks, mid-scale resorts, and industrial campuses multiply along Etihad Rail’s planned freight spurs. Regional authorities are adopting Dubai’s digital-inspection templates to speed project approvals, a move expected to narrow compliance-cost gaps within five years. Salt-laden coastal winds in these emirates guide specifying trends toward anodized-aluminum rainscreens and self-cleaning glass that repel airborne particulates, tailoring product-mix strategies for suppliers expanding beyond the Dubai-Abu Dhabi corridor.

Competitive Landscape

In the UAE, the façade market exhibits moderate fragmentation. The largest contractors and system suppliers collectively dominate a significant portion of the annual billings. While this level of control remains below monopoly thresholds, it is substantial enough to encourage specialization. Global giants such as Permasteelisa and Schüco secure high-profile towers by leveraging proprietary unitized modules, integrated BIM libraries, and end-to-end logistics networks. Their dominance in premium segments pushes regional champions like Emirates Glass and Al Abbar Group to focus on rapid customer service, shorter lead times, and customized glass tempering to retain market share.

Vertical integration is rising: Binghatti’s 2024 purchase of a dedicated façade plant aligns design, fabrication, and installation under one umbrella, trimming change-order risks for developers seeking single-source accountability. Meanwhile, Lindner’s tie-up with Depa creates a hybrid that pairs European rainscreen technology with Gulf-tested installation crews, targeting AED 90 billion (USD 24.51 billion) in airport renovations.

Digitalization is the next battleground. A 2025 industry poll showed 57% of contractors plan to embed AI-driven defect detection and predictive maintenance into façade-monitoring protocols. Suppliers that bundle analytics platforms with hardware stand to lock in long-term service contracts, creating annuity streams beyond initial fabrication margins. Cyber-secure data-center projects, now scaling to USD 15.9 billion by 2030, exemplify customers willing to pay premiums for smart façade systems that integrate seamlessly with cooling and security sensors.

UAE Facade Industry Leaders

Emirates Glass LLC

Al Abbar Group (Arabian Aluminium)

ALICO (Aluminium & Light Industries Co.)

Permasteelisa Gartner Middle East

Emirates Building Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UAE leadership green-lights Abu Dhabi–Dubai high-speed rail, spurring AED 145 billion (USD 39.49 billion) in TOD demand for advanced façades.

- January 2025: Damac releases Dubai Fire Code guide, underscoring stricter flame-spread limits affecting cladding choices.

- December 2024: One Za’abeel towers complete with a record-breaking cantilever and a laminated-glass fin façade.

- November 2024: UAE lodges NDC 3.0, targeting 47% emissions cut by 2035 and nudging façade material decisions toward low-carbon options.

UAE Facade Market Report Scope

Often regarded as a building's most crucial and eye-catching element, the facade acts as its exterior "face." Made up of diverse materials, designs, and architectural features, the facade forms the building's outer shell. While it plays a pivotal role in defining a building's visual appeal, the facade's importance goes far beyond aesthetics. It offers vital structural support, protects the interior from environmental challenges like rain, wind, and heat, and enhances energy efficiency through the use of materials such as insulation, glazing, and shading devices.

In UAE, the facade market is categorized based on type (ventilated, non-ventilated, and others), by material (glass, metal, plastic and fibres, stones, and others), and by end users (commercial, residential, and others).

The report details market sizes and forecasts for UAE facade, measured in USD billion, across all segments, while also assessing the impact of geopolitical events and the pandemic on the market.

By Type

| Ventilated |

| Non-Ventilated |

| Others |

By Façade System Type

| Rainscreen Cladding |

| Curtain-Wall Systems |

| Others |

By Material

| Glass |

| Metal |

| Plastic & Fibres |

| Stones |

| Others |

By Installation

| New Construction |

| Renovation & Retrofit |

By End-User

| Commercial |

| Residential |

| Others |

| By Type | Ventilated |

| Non-Ventilated | |

| Others | |

| By Façade System Type | Rainscreen Cladding |

| Curtain-Wall Systems | |

| Others | |

| By Material | Glass |

| Metal | |

| Plastic & Fibres | |

| Stones | |

| Others | |

| By Installation | New Construction |

| Renovation & Retrofit | |

| By End-User | Commercial |

| Residential | |

| Others |

Key Questions Answered in the Report

What is the current value of the UAE Façade market?

The sector generated USD 2.13 billion in 2026 and is on track for USD 3.02 billion by 2031.

How fast is façade demand growing in Abu Dhabi?

Abu Dhabi is registering the fastest 7.15% CAGR among all emirates through 2031.

Which façade type is gaining popularity for energy savings?

Ventilated cavity systems are rising at a 6.85% CAGR because they cut cooling loads in the Gulf climate.

What material dominates recent façade specifications?

Glass retains a 48.75% share, buoyed by smart-glazing and electrochromic technologies.

Page last updated on: