Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

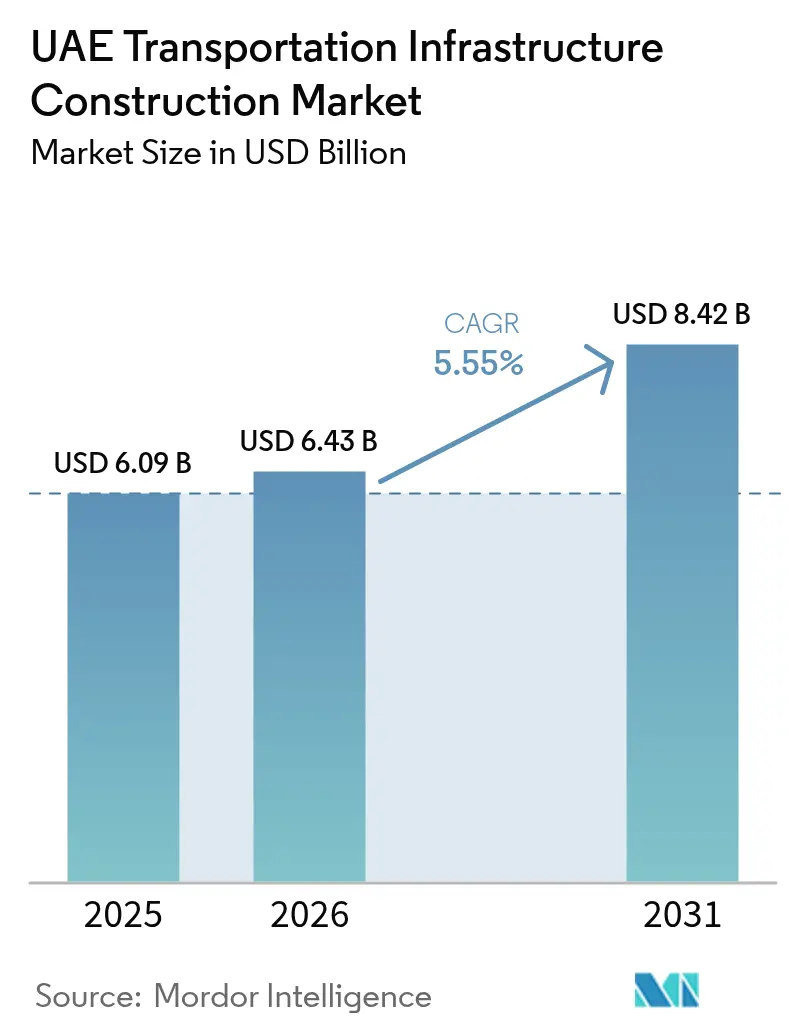

| Base Year Market Size (2025) | USD 6.09 Billion |

| Market Size (2026) | USD 6.43 Billion |

| Market Size (2031) | USD 8.42 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

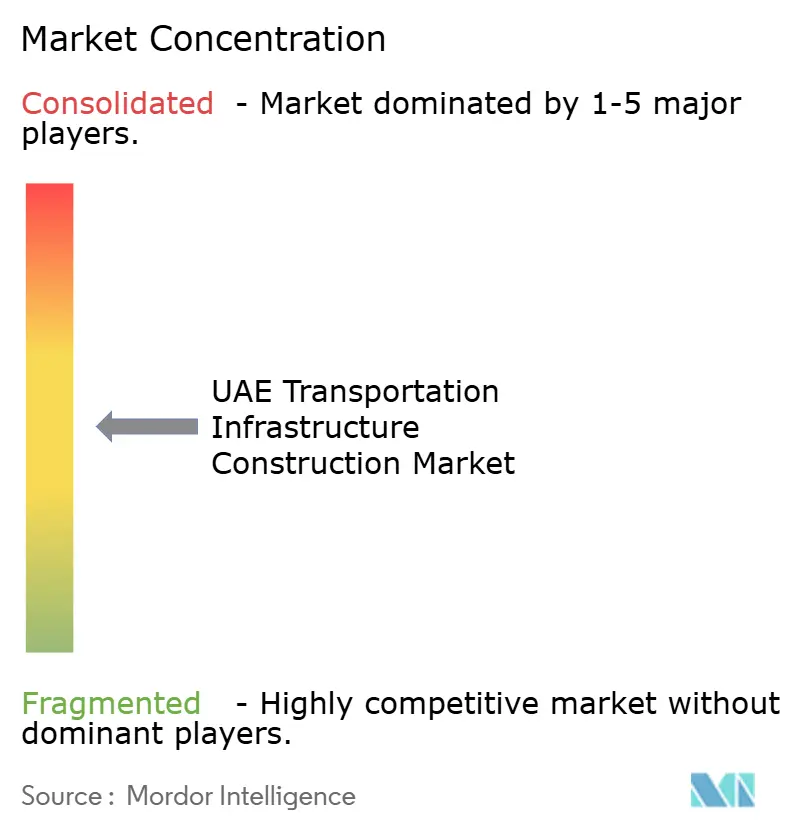

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

The UAE transportation infrastructure construction market size was valued at USD 6.09 billion in 2025 and estimated to grow from USD 6.43 billion in 2026 to reach USD 8.42 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031).

Sustained public-sector spending, the rapid rollout of Etihad Rail Phase 2, and a pipeline of post-Expo 2020 legacy projects continue to anchor headline growth. Government budgets are rising even as oil prices fluctuate, confirming long-term policy commitment to diversified, world-class connectivity. Intensifying aviation traffic, industrial diversification under Operation 300bn, and a widening portfolio of public-private partnerships jointly reinforce demand for multimodal capacity.

Competitive intensity is growing as global EPC majors and fast-scaling domestic contractors deploy digital twins, AI-enabled maintenance, and green hydrogen pilots to secure new contracts and enhance project margins. Emerging opportunities span smart-road upgrades, autonomous-ready corridors, and greenfield aviation links that tie seamlessly into rail freight routes, positioning the UAE transportation infrastructure construction market for resilient medium-term expansion.

Key Report Takeaways

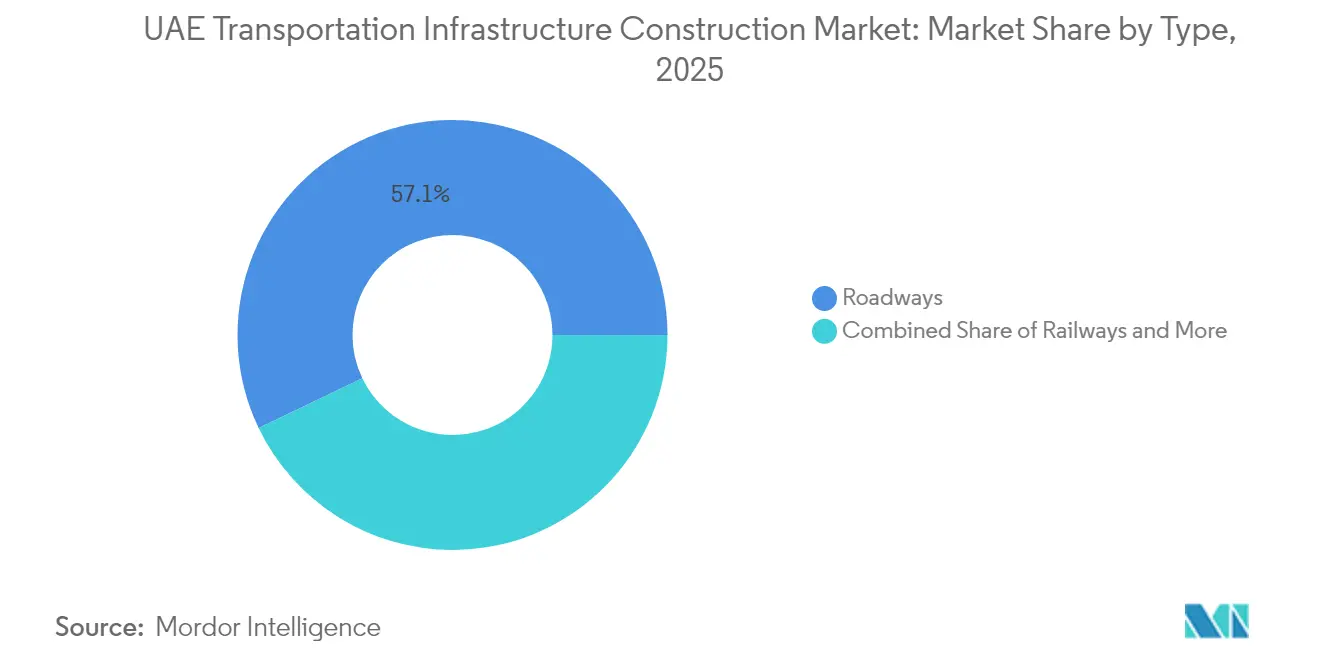

- By type, roadways held 57.12% of UAE transport infrastructure market share in 2025, while railways are projected to record the fastest 6.75% CAGR through 2031.

- By construction type, new construction commanded 75.10% share of the UAE transport infrastructure market size in 2025 and is set to grow at 6.58% CAGR between 2026-2031.

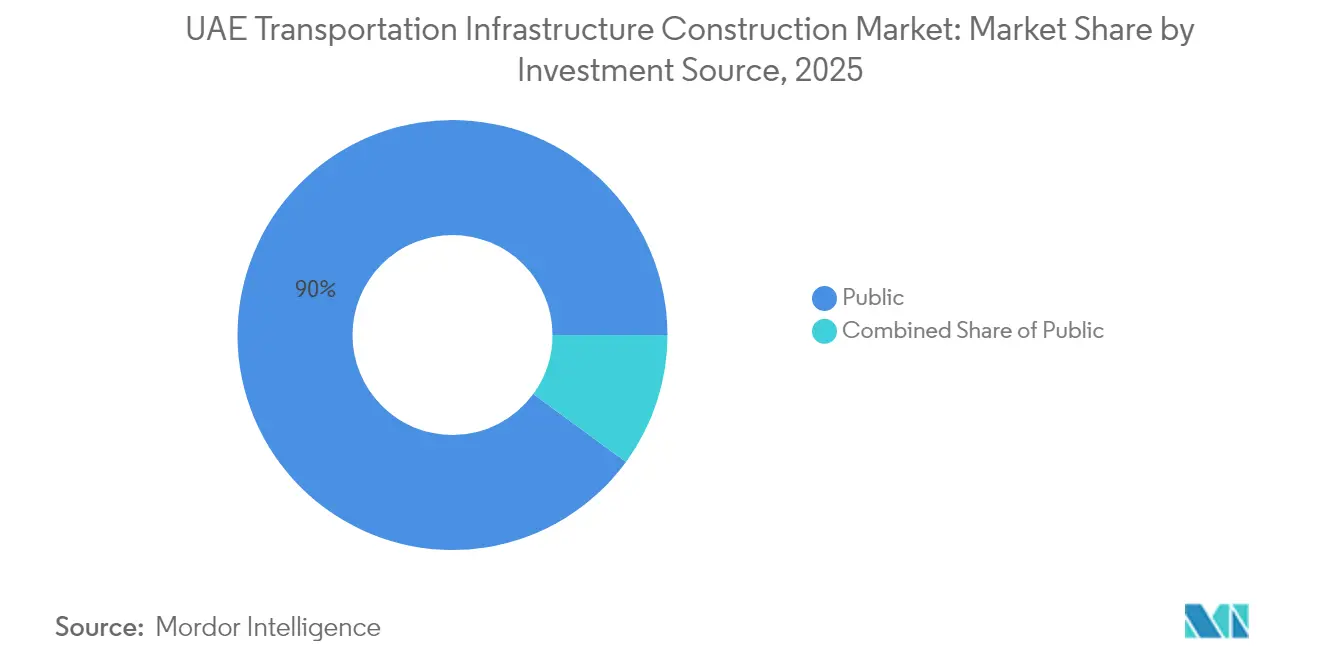

- By investment source, the public segment controlled 89.95% revenue share in 2025; private investment is forecast to rise at 7.12% CAGR to 2031.

- By geography, Abu Dhabi led with 41.05% UAE transport infrastructure market share in 2025, while the rest of UAE is advancing at a 7.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Rail Project capital injection | +1.2% | Nationwide; early gains in Abu Dhabi, Dubai, Sharjah | Long term (≥ 4 years) |

| Economic-diversification agenda | +1.0% | Abu Dhabi & Dubai industrial zones | Long term (≥ 4 years) |

| Growing air-passenger hub status | +0.9% | Dubai airport catchment | Medium term (2-4 years) |

| Expo 2020 legacy boosts tourism-linked transport demand | +0.8% | Dubai core; Northern Emirates spillover | Medium term (2-4 years) |

| AI-driven highway maintenance programs | +0.3% | Federal road networks | Short term (≤ 2 years) |

| Green-hydrogen freight corridor pilots | +0.4% | Abu Dhabi industrial corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Rail Project Transforms Inter-Emirate Connectivity

Etihad Rail Phase 2 injects AED 40 billion of capital and lays 900 kilometers of dual-use track designed for 60 million tonnes of freight and 36.5 million passengers per year by 2030. High-speed services promise a 30-minute Abu Dhabi-Dubai ride at 350 km/h, spurring modal shift from road to rail and easing highway congestion. Freight operators anticipate 30% logistics cost savings once direct port-to-hub rail corridors bypass urban chokepoints. Compliance with European Train Control System standards and ISO 14001 certifications positions the network for interoperable GCC expansion and sustainable operations. Long-term spillovers include land-use densification around planned passenger stations and fresh real-estate demand in satellite towns.

Economic-diversification Agenda Drives Industrial Transport Demand

Operation 300bn aims to lift industrial GDP contribution to AED 300 billion by 2031, backed by AED 30 billion in Emirates Development Bank financing. New factories within KEZAD and Dubai Industrial City require dependable freight corridors to ports and airports, inflating demand for last-mile roads, on-site rail spurs, and temperature-controlled warehousing[1]UAE Government, “Operation 300bn Industrial Strategy,” u.ae. Government-led “Make it in the Emirates” incentives fast-track customs and documentation, creating predictable lead times that attract export-oriented manufacturers. As production capacity scales, the UAE transport infrastructure market sees rising orders for specialized heavy-haul rolling stock and automated container-handling systems.

Aviation Hub Status Creates Multimodal Transport Pressure

Dubai International processed 92.3 million passengers in 2024, and capacity is set to exceed 100 million by 2027. The AED 128 billion Al Maktoum International Airport mega-expansion will accommodate 260 million passengers, requiring express rail links, upgraded freeways and dedicated cargo zones. Strategic eight-hour flight-time access to two-thirds of the global population magnifies ground-network stress: authorities are adding reversible freeway lanes, remote baggage drop-off points and AV-ready feeder lines. The planned DXB-to-DWC traffic handover by 2032 further accelerates investment in south-Dubai road rings and automated people-mover systems.

Expo 2020 Legacy Amplifies Tourism-Transport Integration

Enhanced metro links, upgraded arterial roads, and purpose-built transit hubs created for Expo 2020 now service more than 850,000 daily riders, underpinning year-round tourist mobility. The Dubai Metro Blue Line, an AED 20.5 billion extension, will knit emerging residential clusters into the central network while supporting Dubai’s 2040 “20-minute city” vision[2]Dubai Government Media Office, "RTA Awards Dubai Metro Blue Line Contract," mediaoffice.ae. Permanent improvements in airport-exhibition-hotel connectivity shorten journey times, improve visitor satisfaction, and lift the UAE transport infrastructure market’s attractiveness to hospitality investors. Regulatory enablers, including frictionless e-visa systems and integrated ticketing, encourage repeat visits and higher on-arrival spending, reinforcing transport throughput. Spillover benefits filter into Sharjah and Ajman as day-trip excursions rise, prompting inter-emirate bus frequency upgrades and additional smart-parking facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile oil revenue constrains federal CAPEX | -1.1% | All emirates | Short term (≤ 2 years) |

| Skilled-labor shortage inflates civil-works cost | -0.7% | Major construction zones | Medium term (2-4 years) |

| Environmental-approval delays on coastal dredging | -0.4% | Coastal emirates | Medium term (2-4 years) |

| Low-carbon steel supply disruptions | -0.3% | National projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil-Revenue Volatility Constrains Federal Infrastructure Spending

Brent swings squeeze fiscal buffers and can postpone non-critical highway or port upgrades despite multi-year plans. The 2025 federal budget earmarks AED 71.5 billion overall expenditure with only 3.6% reserved for infrastructure, heightening competition among ministries for limited allocations. When prices dip below budget assumptions, some tendered projects face phased execution or scope minimization. Contingency arrangements involve emirate-level financing or PPP models to sidestep federal pauses, but these require additional due-diligence cycles that elongate procurement timelines.

Skilled-Labor Shortages Inflate Construction Costs

A tight talent pool of BIM engineers, tunneling technicians and rail-signal specialists pushes average wage premiums above GCC peers. Surveyed contractors reported labor-linked cost inflation on 51% of ongoing projects in 2024. Firms respond by importing expertise, investing in training academies and piloting on-site robotics to automate repetitive tasks. Yet visa caps and housing costs constrain foreign recruitment, while automation adoption remains uneven, jointly tempering the UAE transport infrastructure market’s delivery speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Railways Drive Modal-Shift Revolution

Roadways continue to anchor 57.12% of the UAE transport infrastructure market value in 2025, owing to a 4,000-kilometer federal network that supports daily freight movement. Nevertheless, railways, supported by Etihad Rail’s national rollout, are growing at a 6.75% CAGR, the fastest among modes. Rail freight corridors are projected to handle 60 million tonnes annually by 2030, diverting an estimated 300,000 truck trips per year and cutting logistics costs by up to 30%.

Aviation infrastructure advances include the AED 128 billion Al Maktoum expansion, cementing Dubai’s global hub status and attracting airport-city logistics developers. Ports and inland waterways benefit from AD Ports Group’s AED 12-15 billion capex program through 2028, part of efforts that lifted Khalifa Port into the global top-five for efficiency. Across modes, smart-infrastructure adoption, exemplified by Dubai RTA’s AI-controlled traffic signals, signals a shift from capacity-building to technology-enabled performance gains. This trend underpins recurring O&M contracts within the UAE transport infrastructure market.

By Construction Type: Greenfield Projects Dominate Expansion

New construction absorbed 75.10% of 2025 spending and is forecast to maintain a 6.58% CAGR to 2031. Flagship projects range from the 30-kilometer Dubai Metro Blue Line to the 1,200-kilometer GCC rail link stretching into Oman. The UAE transport infrastructure market size for renovation remains meaningful at 24.90% yet sees slower momentum because most core assets were built post-2005 and still operate within lifecycle tolerances.

Building-permit issuance surged 20% in H1 2025, reflecting robust greenfield momentum under Dubai’s 2040 master plan. Updated Dubai Building Code provisions oblige developers to complete traffic-impact studies, spurring complementary roadworks around mixed-use districts. Meanwhile, the renovation segment prioritizes digital retrofits, IoT sensors, EV-charging lanes, and smart-bridge monitoring over large-scale reconstruction, providing specialized opportunities for advanced technology vendors.

By Investment Source: Public Sector Leads While PPPs Accelerate

The public sector financed 89.95% of projects in 2025, typified by federal allocations, emirate-level budgets and strategic entity capex such as ADNOC and AD Ports. Yet private capital is expanding at 7.12% CAGR as PPP frameworks mature. The Dubai RTA’s AED 2.5 billion PPP pipeline covering parking, marine transport and automated fare collection showcases widening roles for concessionaires.

Keolis’s nine-year O&M contract for Dubai Metro and Tram points to operational outsourcing trends. DP World’s USD 2.5 billion logistics infrastructure plan further illustrates the shift toward specialized private investment in hinterland connectivity. Clear procurement guidelines and transparent risk-sharing models reduce investor uncertainty and sustain capital inflows into the UAE transport infrastructure market.

Geography Analysis

Abu Dhabi leads while the northern emirates accelerate. Abu Dhabi’s sizable industrial base, spearheaded by KEZAD’s expanding warehousing footprint, anchors consistent freight throughput and justifies ongoing highway and port channel deepening efforts. Khalifa Port handled 1.37 million TEUs in Q1 2024, up 26% year on year, confirming capacity-driven growth. Green-hydrogen pilots at Al Dhafra foster prospects for low-carbon maritime and rail traction fuels, feeding demand for new storage tanks, pipeline links and bunkering berths.

Dubai’s growth narrative hinges on international aviation and trade. The 92.3 million-passenger tally at DXB in 2024 supported record duty-free sales and rising air-to-road cargo transfers. The Dubai Metro Blue Line will knit low-income suburbs into the economic core, easing labor mobility. AI-powered traffic management curbs congestion by up to 20%, freeing latent road capacity and delaying costly motorway expansions.

Northern emirates receive catalytic impetus from Etihad Rail and Hafeet Rail, which together will thread Ras Al Khaimah quarries and Fujairah oil storage directly into GCC markets. Sharjah’s Khor Fakkan natural deep-water port anchors a logistics cluster targeting India-East Africa trade lanes. Federal grants earmarked for feeder-road widening and last-mile rail terminals reinforce balanced national development and sustain expansion in the UAE transport infrastructure market.

Competitive Landscape

International EPC leaders such as Bechtel, Vinci and China Railway Construction Corporation compete head-to-head with UAE-grown champions including ALEC Engineering, Dutco and Al-Futtaim Construction. Market share shifts favor firms demonstrating digital-delivery prowess: ALEC’s 29% revenue jump in 2024 coincided with expanded modular-build portfolios and rollout of site robotics. Siemens Mobility clinched signaling contracts by pairing ETCS expertise with local partner Hassan Allam’s project-execution record, illustrating the advantage of blended consortia.

Demand for sustainability credentials encourages contractors to showcase ISO 14001 certification, low-carbon concrete mixes and waste-heat recovery during asphalt production. R&D spend channels into predictive-maintenance platforms that combine LiDAR inspections, drone surveys and AI-assisted defect analytics, elevating service revenues within the UAE transport infrastructure market. Transparent tender portals, price-discovery tools and electronic bid bonds enhance market fluidity while preserving competitive parity.

Innovation, rather than low bid price alone, increasingly dictates award decisions. Contracts now weight 30-40% of evaluation score on lifecycle value, O&M cost minimization and carbon-footprint reduction commitments. Companies unable to demonstrate credible decarbonization roadmaps risk losing ground as authorities pursue Net Zero 2050. Consequently, alliances between energy majors, equipment OEMs and civil contractors multiply, pooling expertise to deliver turnkey, sustainability-led transport solutions.

UAE Transportation Infrastructure Construction Industry Leaders

-

Al-Futtaim Group

-

ALEC Engineering & Contracting LLC

-

Consolidated Contractors Company

-

National Contracting and Transport CO

-

Khansaheb

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Etihad Rail unveiled a high-speed Abu Dhabi–Dubai passenger service cutting travel time to 30 minutes, projected to add AED 145 billion to GDP over 50 years

- December 2024: Dubai RTA awarded the AED 20.5 billion Dubai Metro Blue Line contract to a Turkish-Chinese consortium for a 30-kilometer extension with 14 stations

- May 2025: AD Ports Group signed a 50-year USD 120 million agreement to develop the KEZAD East Port Said Zone in Egypt, enhancing Red Sea–Gulf logistics

- April 2024: Dubai approved an AED 128 billion expansion of Al Maktoum International Airport to host 260 million passengers

UAE Transportation Infrastructure Construction Market Report Scope

Transportation Infrastructure refers to the framework that supports the transport system. It consists of fixed installations including roads, railways, airways, waterways, canals, and pipelines, and terminals such as airports, railway stations, bus stations, and trucking terminals.

The UAE Transportation Infrastructure Construction report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation, its impact, porter's five forces analysis, and the impact of COVID-19 on the market. In addition, the report also provides company profiles to understand the competitive landscape of the market.

The UAE Transportation Infrastructure Construction Market is segmented by Transport Mode (Railways, Roadways, Airports, and Waterways). The report offers the market sizes and forecast for the UAE transportation infrastructure construction market in value (USD billion) for all the above segments.

By Type

| Roadways |

| Railways |

| Airways |

| Ports and Inland Waterways |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Geography

| Abu Dhabi |

| Dubai |

| Sharjah |

| Rest of UAE |

| By Type | Roadways |

| Railways | |

| Airways | |

| Ports and Inland Waterways | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Geography | Abu Dhabi |

| Dubai | |

| Sharjah | |

| Rest of UAE |

Key Questions Answered in the Report

How large is the UAE transport infrastructure market in 2026?

The UAE transport infrastructure market size is USD 6.43 billion in 2026.

What is the expected CAGR for UAE transport infrastructure through 2031?

The market is forecast to grow at a 5.55% CAGR between 2026 and 2031.

Which mode is expanding fastest inside UAE transport infrastructure?

Railways are the fastest-growing segment with a projected 6.75% CAGR through 2031.

Page last updated on: