Saudi Arabia Structural Steel Fabrication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

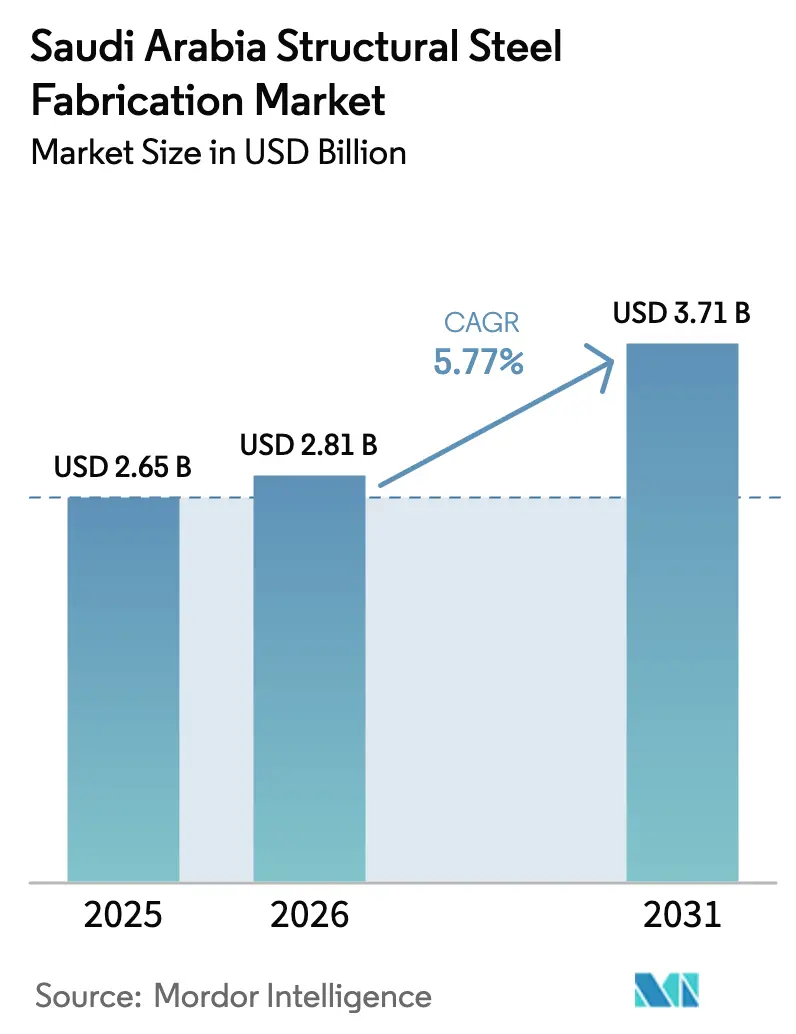

| Base Year Market Size (2025) | USD 2.65 Billion |

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Structural Steel Fabrication Market Analysis by Mordor Intelligence

The Saudi Arabia structural steel fabrication market size was valued at USD 2.65 billion in 2025 and estimated to grow from USD 2.81 billion in 2026 to reach USD 3.71 billion by 2031, at a CAGR of 5.77% during the forecast period (2026-2031). Persistent backlog from Vision 2030 projects, the downstream petrochemical build-out, and a 15 gigawatt renewables pipeline together keep workshop utilization high. Fabricators are accelerating the shift to BIM-enabled modular construction, investing in robotic welding and precision laser-cutting to meet compressed delivery windows and stringent In-Kingdom Total Value Add (IKTVA) quotas. The Eastern Province remains the revenue anchor thanks to Jubail’s petrochemical corridor, yet Riyadh is now the epicenter for fast-growing entertainment, cultural, and transport builds. Currency-hedged, long-term supply contracts are helping large yards absorb billet and scrap price spikes triggered by Red Sea logistics disruptions.

Key Report Takeaways

- By product type, heavy sections led with 38% of the Saudi Arabia structural steel fabrication market size in 2025, and custom-built modules & skids are projected to expand at a 7.11% CAGR through 2031.

- By end-user industry, oil & gas accounted for 32.1% of the Saudi Arabia structural steel fabrication market share in 2025, and power & energy (utilities and renewables) is projected to grow at an 8.4% CAGR through 2031.

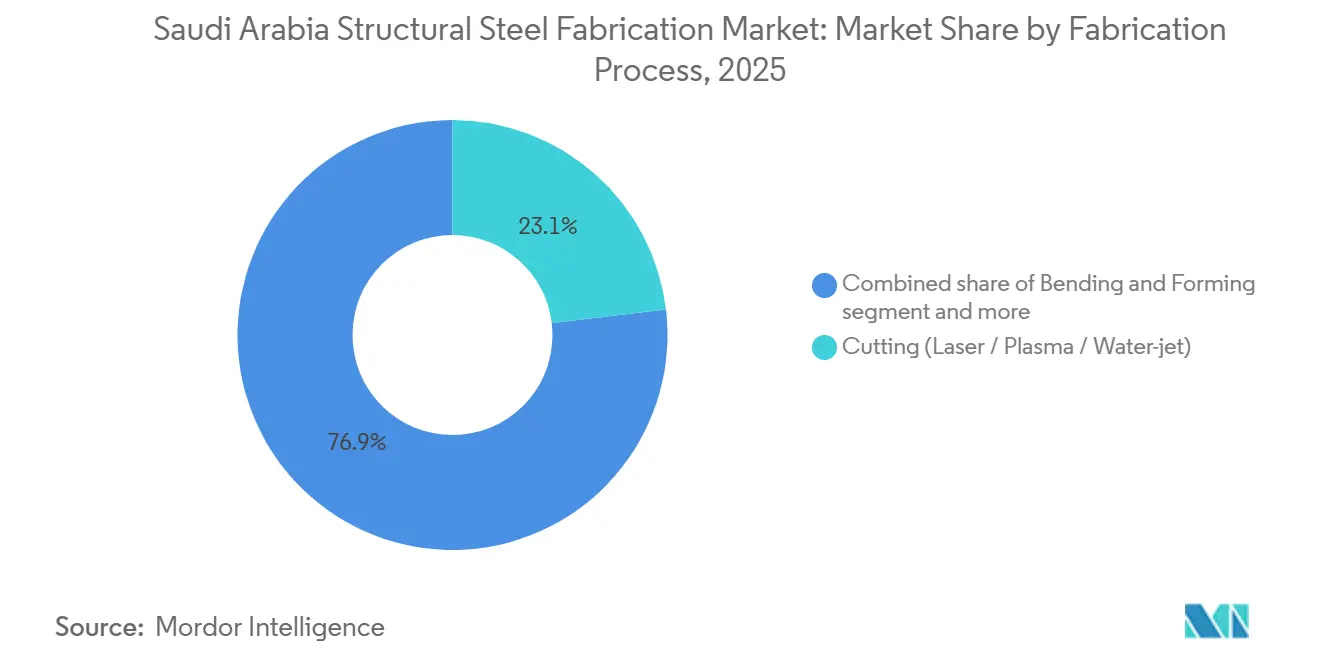

- By fabrication process, cutting held 23.1% of the Saudi Arabia structural steel fabrication market share in 2025, and assembly & modular integration is projected to grow at a 6.93% CAGR between 2026 and 2031.

- By geography, the Eastern Province captured 36.88% of the Saudi Arabia structural steel fabrication market size in 2025, and Riyadh Province is projected to expand at a 7.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding multibillion-dollar infrastructure pipeline under Vision 2030 funding acceleration | 1.8% | National, with concentration in Riyadh, Makkah, and Eastern Province | Medium term (2-4 years) |

| Fast-track execution of giga-projects (NEOM, Red Sea, Qiddiya) reaching full construction phase | 1.5% | Western Region (NEOM, Red Sea), Riyadh Province (Qiddiya) | Short term (≤ 2 years) |

| Boom in downstream oil-&-gas and petrochemical capacity additions linked to Aramco decarbonization | 1.2% | Eastern Province (Jubail, Ras Al Khair) | Medium term (2-4 years) |

| Stricter IKTVA and "Made-in-Saudi" local-content quotas stimulating domestic fabrication demand | 1.0% | National, with strongest enforcement in energy and defense sectors | Long term (≥ 4 years) |

| Uptake of BIM-enabled modular construction and automated shop-floor robotics to cut project lead-times | 0.8% | National, early adoption in Riyadh and NEOM | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Multibillion-Dollar Infrastructure Pipeline Under Vision 2030 Funding Acceleration

Saudi Arabia’s public-sector megaproject pipeline has moved from design desks to job sites, with the Riyadh Metro, Diriyah Gate, and the 1,500-kilometer Land Bridge now soaking up above-ground steel. Metro extensions alone will need more than 100,000 tonnes of beams and plate-worked girders for viaducts and stations. The USD 9.9 billion allocation to NEOM infrastructure through 2026 secures a multi-year order book for fabricators able to supply seismic-rated members on tight schedules. Large yards are responding by adding CNC bending and rotary drilling cells that can machine custom trusses without subcontracting. These capital upgrades improve first-pass yield and shorten shop cycles, reinforcing domestic capacity at a time when import routes face geopolitical risk.

Fast-Track Execution of Giga-Projects Reaching Full Construction Phase

NEOM, Qiddiya, and the Red Sea Project have entered full vertical construction, driving a synchronized demand surge for repetitive modular frames that favor robotic welding over manual stick-built assembly. Samsung C&T’s on-site prefabrication plants at NEOM cut field welding hours by roughly 40%, demonstrating the productivity upside of automation. Qiddiya’s retractable-roof stadium needs 15,000 tonnes of tubular hollow sections and pin-jointed trusses, volumes that only large, highly automated Saudi yards can deliver domestically. Contractors now stockpile cut-to-length beams and pre-drilled plates to avoid schedule penalties, even though this practice ties up working capital. Repeat orders from prime contractors that prize reliability more than lowest cost are rewarding fabricators that invest in digital workflows and capacity buffers.

Boom in downstream oil-&-gas and petrochemical capacity additions linked to Aramco decarbonization

Aramco-led downstream diversification is anchoring a petrochemical megacycle that will add over 5 million tpa of ethylene by 2030. The Amiral complex alone requires 80,000 tonnes of structural steel across its cracker and derivative units, with delivery windows locked to a 2027 first-production date. Feedstock allocations granted in 2025 to Tasnee and Sipchem-LyondellBasell triggered EPC tenders specifying ASME-certified supports and seismic-rated pipe racks, raising the bar on quality systems. Fabricators that already hold ASME and AWS stamps are in pole position to land these contracts, and several have upgraded NDT labs to secure long-term framework deals. Petrochemical work also supports turnkey skid demand, letting yards move upstream into higher-margin mechanical integration.

Stricter IKTVA and "Made-in-Saudi" local-content quotas stimulating domestic fabrication demand

The In-Kingdom Total Value Add Program reached 70 percent achievement in February 2026, contributing USD 280 billion to GDP and creating over 500,000 jobs, yet enforcement is tightening as Aramco and the Ministry of Investment mandate 75 percent local content for new energy and infrastructure contracts by 2028[1] "IKTVA Programme Contributes $280bn to Saudi GDP." MEED, February 2026. . Zamil Steel's November 2024 joint venture with Germany's Wolffkran to manufacture tower cranes domestically exemplifies the strategic response, converting a previously imported product line into a local supply chain that qualifies for IKTVA credits and shortens delivery lead-times from 16 weeks to 8 weeks. AIC Steel's partnership with Lockheed Martin to localize defense-system fabrication, announced in 2024, leverages IKTVA incentives to capture a share of the Kingdom's USD 10 billion annual defense procurement budget, diversifying revenue beyond traditional construction and oil-and-gas segments. The program's cascading effect is evident in Zamil Steel's USD 153.3 million industrial complex in Al-Kharj, developed with SAMI Land for defense manufacturing, which will house laser-cutting, CNC machining, and automated welding bays designed to meet NATO and Saudi military specifications. IKTVA's requirement that suppliers demonstrate 30 percent Saudi employment in engineering roles and 70 percent in procurement roles by 2026 is accelerating training partnerships with the Technical and Vocational Training Corporation, though the pace of skill development lags the surge in contract awards.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spike-and-dip volatility in billet & scrap import costs amid Red Sea and Black Sea logistics disruptions | -0.6% | Western Region (Jeddah, NEOM, Red Sea Project) with spillover to national pricing | Short term (≤ 2 years) |

| Ongoing shortage of certified welders/fabricators as Saudization drains expatriate labor pool | -0.5% | National, acute in Riyadh and Eastern Province | Medium term (2-4 years) |

| Prolonged payment cycles and retentions on public megaprojects straining fabricator working capital | -0.4% | National, concentrated in government-funded infrastructure and defense contracts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spike-and-Dip Volatility in Billet & Scrap Import Costs Amid Red Sea and Black Sea Logistics Disruptions

Houthi attacks in the Red Sea pushed war-risk premiums to ten times pre-crisis norms, lifting spot freight from Asia to Jeddah from USD 500 to USD 2,500 per TEU and adding roughly USD 75 per tonne to landed steel costs. Re-routing via Dammam port avoids the hot zone but adds inland trucking expense and three days to delivery, a drag on fixed-price contracts. Fabricators now negotiate inflation-index clauses and hold larger safety stocks, increasing working capital needs but safeguarding delivery reputations.

Ongoing Shortage of Certified Welders/Fabricators as Saudization Drains Expatriate Labor Pool

Mandates for 30% Saudi engineers and 70% Saudi procurement staff by 2026 have accelerated expatriate outflows, leaving an estimated shortfall of 10,000 to 15,000 certified welders. Industry-backed academies graduate fewer than 2,000 welders per year, forcing firms to automate or pay wage premia for scarce skills. Riyadh and Eastern Province projects compete for the same talent pool, inflating labor costs and stretching schedules on specialized assemblies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Dominate, Modular Skids Expand

Heavy sections carried 38% of 2025 revenue for the Saudi Arabia structural steel fabrication market share, underscoring their role as primary load-bearing elements across towers, bridges, and industrial halls. Demand is entrenched in projects like the Riyadh Metro viaducts and petrochemical pipe racks that cannot substitute lighter gauges. Conversely, custom-built modules and skids post the fastest expansion, growing at a 7.11% CAGR as giga-projects specify off-site assemblies to counter onsite labor constraints. Samsung C&T’s NEOM prefabrication lines illustrate how turnkey skid packages integrate structural frames, piping, and electricals, reducing field hours and guaranteeing dimensional accuracy. Yards equipped with robotic welding and CNC machining cells position themselves to capture this premium segment, leveraging BIM to synchronize once-siloed disciplines.

The tilt toward modularization also lifts ancillary demand for precision plate-work used in reactor supports and large trusses. Tubular and hollow structural sections gain importance in seismic-rated frames like Qiddiya’s retractable roof, while light sections sustain residential and low-rise retail builds where speed trumps capacity. The Saudi Arabia structural steel fabrication market size associated with plate-worked girders is poised to track infrastructure spend on long-span bridges, with the Land Bridge rail project alone forecast to absorb 200,000 tonnes of girders and gantry structures by 2029. As yards diversify into multiple product lines, advanced nesting software helps optimize cut plans, minimizing scrap and lifting overall yield.

By End-User Industry: Oil & Gas Leads, Renewables Accelerate

Oil & gas retained a commanding 32.1% share of the 2025 Saudi Arabia structural steel fabrication market, fueled by downstream expansions such as the USD 11 billion Amiral cracker and support infrastructure at Jubail. These projects order large-volume, ASME-certified supports and heavy plate, locking in shop capacity well into 2027. Yet power & energy utilities and renewables are the breakout segment, forecast to grow at an 8.4% CAGR to 2031 as ACWA Power, Masdar, and TotalEnergies build out a 15 gigawatt pipeline of solar and wind farms. Tracker structures, wind-tower sections, and grid-interconnect steel form a rising share of order books, diversifying revenue away from hydrocarbons.

Construction end-users remain sizeable, drawing from ongoing metro extensions, heritage venues, and large retail districts that rely heavily on beams and cold-formed members. Manufacturing and industrial equipment orders, including tower cranes birthed by the Zamil-Wolffkran JV, reinforce a gradual climb in capital-goods fabrication inside the Kingdom. Niche demand surfaces in defense, mining, and shipbuilding as IKTVA rules open doors for localized high-spec assemblies. The Saudi Arabia structural steel fabrication industry is adapting by enhancing certification portfolios, AWS, ISO 9001, and, increasingly, ISO 3834, to serve multiple end-markets without compromising compliance.

By Fabrication Process: Cutting Retains Scale, Assembly & Integration Surges

Cutting processes supplied 23.1% of 2025 revenue, making them the largest contributor to the Saudi Arabia structural steel fabrication market size at the process level. Multi-axis laser, plasma, and water-jet lines supply precise blanks that drive downstream productivity, exemplified by MS-Metals’ ±0.5 mm laser setup in Tabuk. However, the assembly and modular integration cluster is on track for the highest growth, at a 6.93% CAGR to 2031, as EPC contractors increasingly award turnkey skid packages instead of line-item steel tonnage. Fabricators therefore bundle cutting, forming, welding, and even electrical fit-out inside single contracts that promise single-point accountability.

Bending and forming keep pace where architectural curves and tapered beams are required, notably in Diriyah’s column-free opera house and Qiddiya’s stadium roof. Welding, whether TIG, MIG, or SMAW, remains the critical value-adding step, but labor scarcity spurs robotics adoption across routine joints, reserving certified human welders for pressure-vessel and seismic applications. Machining and surface treatment round out the flow, with growing in-house capacity at Doosan’s Tuwaiq factory linking forging, CNC machining, and finishing under one roof. The integrated model reduces logistic hand-offs and fits the fast-track ethos now prevalent across public-sector builds.

Geography Analysis

The Eastern Province contributed 36.88% of 2025 revenue, anchored by Jubail’s petrochemical expansions and Ras Al Khair’s emerging heavy-industry hub. Projects like the Amiral complex, Tasnee’s 3.3 million tpa facility, and Advanced Petrochemical’s propane dehydrogenation unit collectively lock in more than 150,000 tonnes of future steel demand. Dammam’s deep-water port has become the detour of choice whenever Red Sea lanes flare, giving local yards a logistical edge in raw-material intake. Ras Al Khair’s USD 834 million Tuwaiq Casting & Forging plant and NMDC Energy’s 40,000 tpa fabrication yard strengthen a vertically integrated corridor capable of supplying both domestic and export markets[2]"NMDC Energy Fabrication Yard at Ras Al Khair." MEED, January 2025. .

Riyadh Province, although smaller in base, is the fastest-growing geography with a 7.01% CAGR to 2031. The metro Red Line extension, Diriyah’s SAR 5.1 billion (USD 1.36 billion) opera house, and Qiddiya’s entertainment complex collectively require specialized trusses, tubular sections, and architectural steel. Fabricators are setting up satellite yards in Al-Kharj and Sudair Industrial City to reduce haulage times and position closer to end-sites. Arabian Pipes’ OCTG coupling plant and Benaa’s new rebar mill broaden the industrial footprint beyond construction alone, reflecting the capital’s shift toward diversified manufacturing.

Makkah Province hosts iconic giga-projects such as NEOM, Oxagon, and the Red Sea resorts, each presenting sustained demand for modular frames, desalination plant steel, and airport terminals. While Houthi-related freight surcharges initially inflated west-coast project costs, contractors mitigated exposure by routing via Dammam and trucking. Al Yamama’s wind-tower factory in Yanbu positions the western region as a supply center for the 3 gigawatt national wind pipeline. Peripheral regions like Tabuk and Hail are no longer backwaters; MS-Metals’ automated Tabuk facility and TotalEnergies-AEW’s As Sufun solar project show Vision 2030 money now reaches secondary provinces, broadening the customer base for fabricators willing to mobilize.

Competitive Landscape

Saudi Arabia’s structural steel fabrication sector is moderately competitive. Zamil Steel pushes vertical integration, from heavy sections to tower cranes and defense modules, enabling it to pitch cradle-to-deployment solutions that meet strict IKTVA credit requirements. MS-Metals leverages robotic welding and BIM interoperability to undercut rivals on schedule, a decisive advantage on fast-track NEOM packages. AIC Steel’s defense pivot via Lockheed Martin diversifies revenue and captures higher margins tied to NATO-grade specifications.

State-driven consolidation is underway. PIF’s 2025 purchase of Hadeed and the follow-on acquisition of Rajhi Steel signal an ambition to create a national champion with in-house billet, plate, and rebar rolling lines. The integrated steelmaker could internalize raw-material supply and set domestic benchmark pricing, pressuring independent fabricators to specialize or seek joint ventures. Foreign entrants such as Buhur-Jindal SAW’s USD 100 million pipe mill leverage parent-company technology and local financing incentives, intensifying rivalry in commodity pipe and HSS segments[3]"Buhur-Jindal SAW Pipe Plant Joint Venture." MEED, February 2026..

Strategic playbooks now emphasize long-term framework agreements with Aramco, SEC, and PIF portfolio companies, locking in baseline tonnage and smoothing order volatility. Technology spending centers on automated cutting and welding cells that raise throughput per square meter, allowing yards near metropolitan zones to compete despite higher land costs. Certification upgrades, from ASME to ISO 3834, enable access to petrochemical, power, and defense tenders that carry thicker margins than price-sensitive commercial building work.

Saudi Arabia Structural Steel Fabrication Industry Leaders

-

Attieh Steel

-

Gulf Specialized Works

-

Zamil Steel

-

Saudi Building Systems Mfg. Co.

-

International Building Systems Factory Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Buhur Group and Jindal SAW formed a joint venture to build a 350,000 tpa carbon steel pipe plant in Sudair Industrial City, with first output slated for Q4 2027.

- January 2026: East Pipes Integrated awarded a USD 20.9 million contract to double coating-line capacity in Dammam, aligning with Land Bridge rail demand.

- December 2025: Arabian Pipes announced a USD 8 million OCTG coupling factory in Riyadh, aiming for Q2 2027 commissioning.

- November 2025: Al Yamama Iron & Steel won a USD 47.1 million contract to supply 380 kV transmission towers in the Western Region.

Saudi Arabia Structural Steel Fabrication Market Report Scope

Structural steel fabrication is the process of bending, cutting, and modeling steel to create a structure. For structural steel fabrication, steel parts are often put together to create different structures of predefined sizes and shapes.

The Saudi Arabia structural steel fabrication market is segmented by end-user industry (manufacturing, power and energy, construction, oil and gas, and other end-user industries) and product type (heavy sectional steel, light sectional steel, and other product types).

The report offers the market sizes and forecasts for the Saudi Arabia structural steel fabrication market in value (USD) for all the above segments.

| Heavy Sections (Beams & Columns) |

| Light Section & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Plate-worked Girders & Trusses |

| Custom-built Modules & Skids |

| Construction | Commercial Buildings |

| Residential Buildings | |

| Industrial Buildings | |

| Transport Infrastructure (roads, bridges, metro) | |

| Power & Energy (utilities & renewables) | |

| Oil & Gas | |

| Manufacturing & Industrial Equipment | |

| Automotive & Rail Systems | |

| Other Industries (Mining, Shipbuilding, Defense, Agri-food, Telecom) |

| Cutting (laser, plasma, water-jet, saw, shear) |

| Bending & Forming (press-brake, roll, rotary) |

| Welding (TIG, MIG, SMAW, spot) |

| Machining (milling, turning, drilling, CNC) |

| Casting & Forging |

| Surface Treatment & Finishing |

| Assembly & Modular Integration |

| Riyadh Province |

| Makkah Province (Jeddah, Mecca) |

| Eastern Province (Dammam, Jubail) |

| Rest of Saudi Arabia |

| By Product Type | Heavy Sections (Beams & Columns) | |

| Light Section & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Plate-worked Girders & Trusses | ||

| Custom-built Modules & Skids | ||

| By End-user Industry | Construction | Commercial Buildings |

| Residential Buildings | ||

| Industrial Buildings | ||

| Transport Infrastructure (roads, bridges, metro) | ||

| Power & Energy (utilities & renewables) | ||

| Oil & Gas | ||

| Manufacturing & Industrial Equipment | ||

| Automotive & Rail Systems | ||

| Other Industries (Mining, Shipbuilding, Defense, Agri-food, Telecom) | ||

| By Fabrication Process | Cutting (laser, plasma, water-jet, saw, shear) | |

| Bending & Forming (press-brake, roll, rotary) | ||

| Welding (TIG, MIG, SMAW, spot) | ||

| Machining (milling, turning, drilling, CNC) | ||

| Casting & Forging | ||

| Surface Treatment & Finishing | ||

| Assembly & Modular Integration | ||

| By Geography | Riyadh Province | |

| Makkah Province (Jeddah, Mecca) | ||

| Eastern Province (Dammam, Jubail) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

What is the forecast value of structural steel fabrication demand in Saudi Arabia by 2031?

The Saudi Arabia structural steel fabrication market is projected to reach USD 3.71 billion by 2031.

Which province is growing fastest for fabrication demand?

Riyadh Province is expected to post a 7.01% CAGR through 2031, the highest among all regions.

Which end-user sector will expand most rapidly?

Power & energy utilities and renewables are forecast to grow at an 8.4% CAGR through 2031.

How are IKTVA rules shaping the sector?

Stricter IKTVA quotas now demand 75% local content by 2028, prompting joint ventures and new domestic production lines.

Page last updated on: