Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.05 Billion |

| Market Size (2026) | USD 7.27 Billion |

| Market Size (2031) | USD 8.46 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

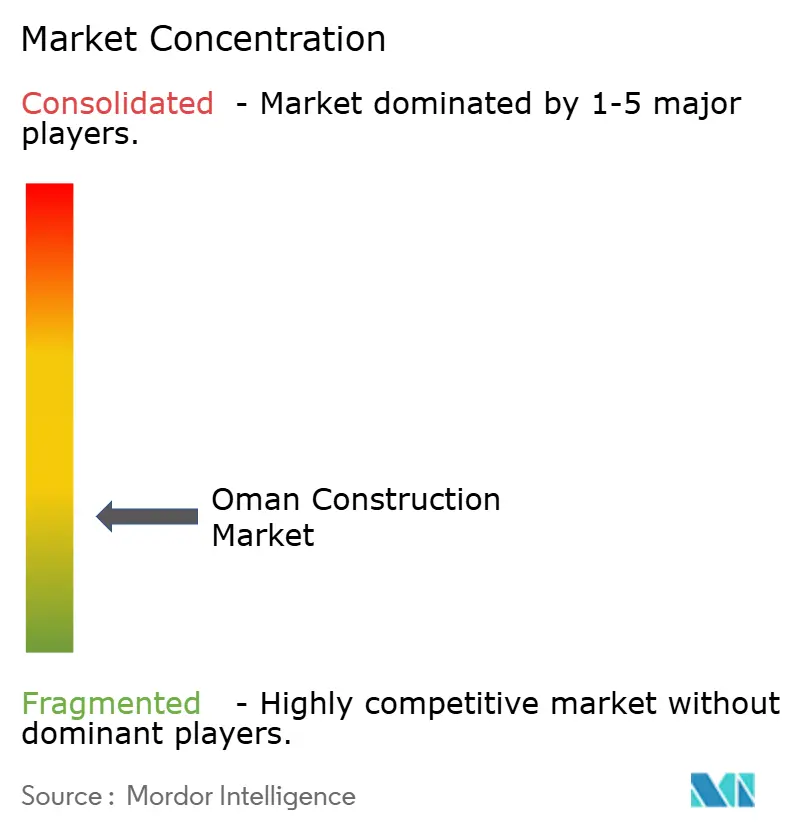

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Construction Market Analysis by Mordor Intelligence

Oman Construction Market size in 2026 is estimated at USD 7.27 billion, growing from 2025 value of USD 7.05 billion with 2031 projections showing USD 8.46 billion, growing at 3.08% CAGR over 2026-2031. Robust Vision 2040 spending, population-led housing demand, and a USD 11 billion green-hydrogen pipeline in Dhofar anchor steady growth, while modern building methods gain currency as labor rules tighten. Public funding continues to dominate large projects, but public-private partnerships and foreign capital inflows are rising as the state trims oil-linked expenditure. Rapid roll-out of the 2,224-kilometer national railway, coupled with tourism infrastructure for a tripling of annual visitors by 2040, broadens the order book for contractors. However, volatile material prices and water scarcity compliance costs temper near-term profit margins.

Key Report Takeaways

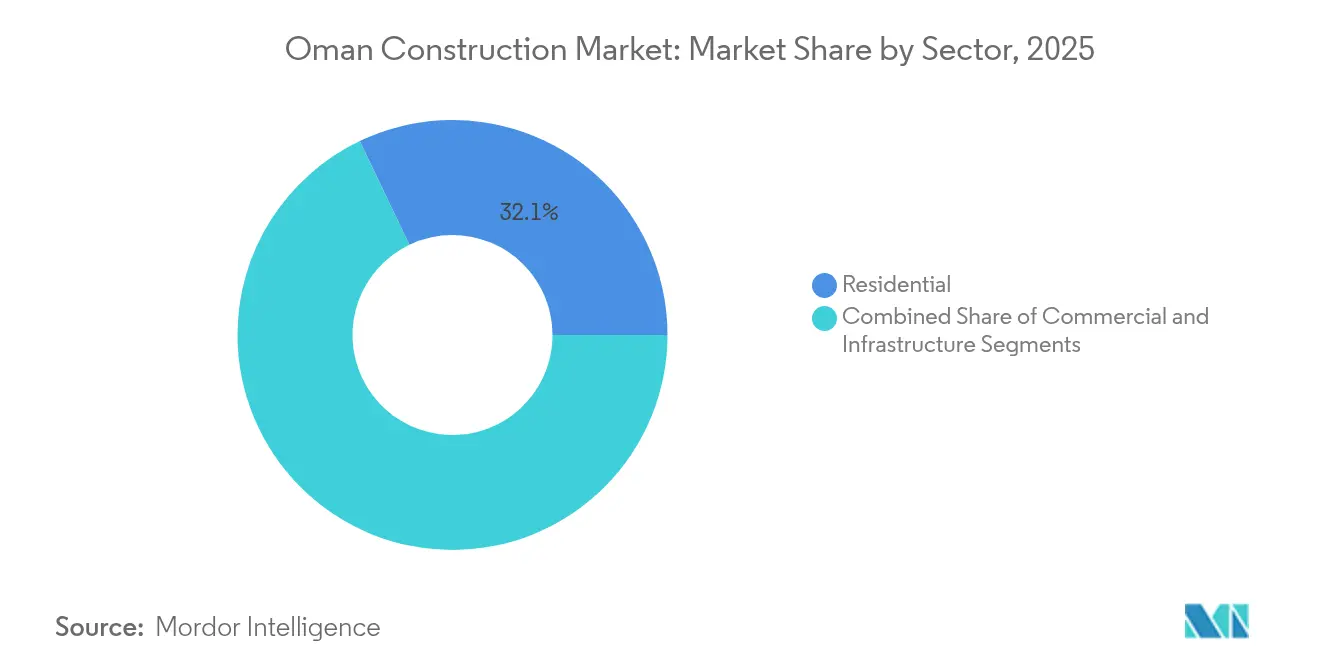

- By sector, the residential segment led with 32.10% of the Oman construction market share in 2025, while infrastructure is advancing at a 5.18% CAGR to 2031.

- By construction type, new builds accounted for 79.68% of the Oman construction market size in 2025; renovation work is projected to expand at a 4.29% CAGR.

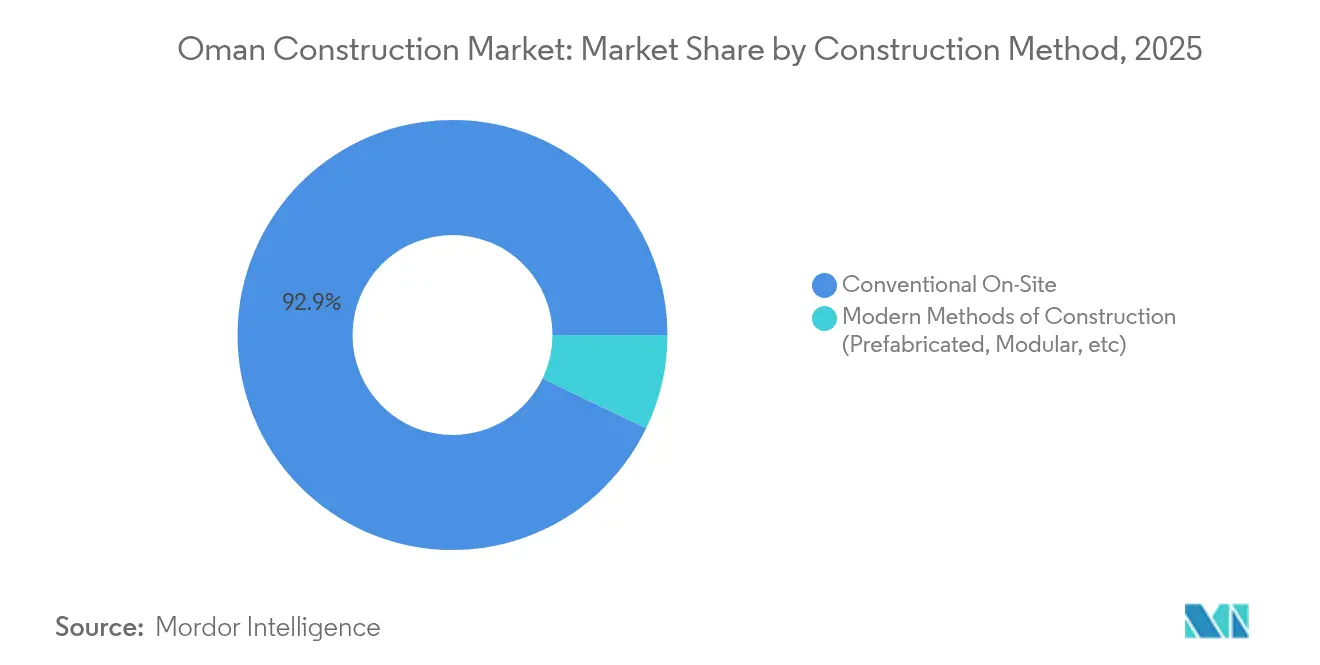

- By construction method, conventional on-site techniques held 92.85% share of the Oman construction market size in 2025, yet prefabricated and modular systems are growing at a 5.74% CAGR.

- By investment source, public spending represented 83.70% of the Oman construction market share in 2025, but private funding shows the fastest 5.03% CAGR through 2031.

- By geography, Muscat captured 40.92% of the Oman construction market share in 2025, whereas the “Rest of Oman” governorate group is forecast to grow at a 4.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government investments in Vision 2040 megaprojects | +1.2% | National — Muscat, Duqm, Sohar | Long term (≥ 4 years) |

| Green hydrogen EPC pipeline | +0.9% | Dhofar, SEZAD | Long term (≥ 4 years) |

| Rapid urbanisation & housing demand | +0.8% | Muscat, Al Batinah, emerging hubs | Medium term (2-4 years) |

| GCC rail/road connectivity programmes | +0.7% | Sohar–Salalah corridor | Long term (≥ 4 years) |

| Tourism-focused infrastructure push | +0.6% | Dhofar, Muscat, coastal corridors | Medium term (2-4 years) |

| Modular construction to offset labor shortages | +0.4% | Major urban job sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Investments in Vision 2040 Megaprojects

Large-scale public spending under Vision 2040 reshapes the Oman construction market by bankrolling entire economic districts. Duqm’s 150 km² renewable-energy zone and Sultan Haitham City’s first phase 5.5 million m² hosting 7,000 homes illustrate deep, multi-year order visibility. State debt fell to OMR 14.5 billion (USD 37.8 billion), giving room for sustained capital deployment. Contractors able to navigate In-Country Value rules and Omanisation targets secure repeat awards. Long-dated projects create stable workloads even when oil receipts fluctuate[1]Public Authority for Special Economic Zones and Free Zones, “Duqm Renewable Masterplan,” opaz.gov.om.

Green Hydrogen EPC Pipeline

Dhofar hosts USD 11 billion in signed hydrogen deals, targeting 1.38 million tonnes per year from 4.5 GW renewable supply. EPC demand spans solar fields, electrolysers, ammonia storage, and export jetties. Early packages favor global energy majors paired with local JV partners to meet Omanisation quotas. Long tenors and joint sovereign-investor funding reduce credit risk, encouraging equipment suppliers to localize production. Successful delivery positions Oman as a regional decarbonized-fuel exporter.

Rapid Urbanisation & Housing Demand

A 5.27 million population with 43% expatriates pushes annual real-estate deals to OMR 3.13 billion (USD 8.1 billion). Urban land covers only 2% of the national territory, driving higher-density housing typologies such as twin villas and row houses. Affordable housing programs add 425 social units per year, yet leave a wide supply gap. The National Spatial Strategy designates all 11 governorates as micro-hubs, multiplying residential project sites. Builders integrating compact designs and cost-efficient materials gain a pricing advantage.

GCC Rail/Road Connectivity Programs

The 2,224-kilometer national railway budgeted at USD 15 billion links Sohar to Salalah in four phases and plugs into Etihad Rail, boosting mineral freight and passenger mobility. Regional rail outlays exceed USD 100 billion, meaning design standards follow GCC-wide norms. High-speed alignment, customs nodes, and electrification works attract international EPC consortia with turnkey rail expertise. Local civil firms benefit through sub-contracts on embankments, stations, and maintenance depots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices | -0.6% | Remote projects | Short term (≤ 2 years) |

| Slow municipal permit approvals | -0.5% | Dense urban zones | Short term (≤ 2 years) |

| Fiscal tightening & capex cuts | -0.4% | Oil-dependent regions | Medium term (2-4 years) |

| Water-scarcity-related compliance costs | -0.3% | Desalination-reliant coasts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices

Cement output reached 5.2 million t, while gypsum hit 10.7 million t, yet global freight and energy swings drive unpredictable input bills. Import reliance for structural steel and specialty finishes exposes projects to currency moves. Studies rank price hikes as the top cause of cost overruns in Omani housing schemes. Government reverse-auction bulk buys partially hedge spikes, but adoption remains patchy. Contractors add escalation clauses, shifting some volatility to clients.

Slow Municipal Permit Approvals

Complex zoning in Muscat and heritage-rich interiors prolong approval cycles. E-permitting reforms are underway, but offline processes persist for multi-story or mixed-use sites. Delay risk prompts developers to front-load design documentation and stakeholder consultations. Small local builders often face higher relative costs due to limited administrative bandwidth. Streamlined digital portals promise relief yet need cross-agency integration to show full benefit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Acceleration Outpaces Residential Dominance

The residential segment held 32.10% of the Oman construction market size in 2025, reflecting deep housing demand in Muscat and fast-growing coastal towns. Vision 2040’s expansive public-housing pipeline keeps volume steady, yet tight land parcels spur a shift toward compact row-house designs. Banks offer preferential mortgages for first-time buyers, sustaining private developer margins. Meanwhile, infrastructure’s 5.18% CAGR positions it as the breakout growth engine, thanks to the USD 15 billion railway, port expansions at Sohar, and Dhofar’s hydrogen projects. International EPC firms are teaming with Galfar Engineering on rail packages, signaling technology transfer opportunities.

Sustained infrastructure roll-outs attract long-lead equipment suppliers, while housing builders adopt modular shells to mitigate skilled-labor shortfalls. Regulatory authorities mandate BIM submittals for projects over 4 stories beginning in 2026, nudging both segments toward digital workflows. As the national spatial plan seeds new economic hubs, demand arcs from core urban centers to secondary cities, offering residential contractors a broader geographic spread. Infrastructure wins continue to set location precedents that later unlock mixed-use residential clusters, further linking the two segments’ growth paths.

By Construction Type: New-Build Dominance, Renovation Revival

New construction captured 79.68% of the Oman construction market share in 2025, driven by greenfield megaprojects across Duqm, Sohar, and Salalah. Government tender boards favor turnkey packages, creating scale for tier-one contractors. Renovation, although smaller, advances at a 4.29% CAGR as facilities built in the early 2000s require energy-efficiency retrofits. Public agencies earmark grants for HVAC upgrades in schools and hospitals, opening scope for specialist subcontractors. Insurance firms also link premiums to compliance with updated seismic and fire codes, accelerating retrofit spending.

The Oman construction market share of renovation activity rises as existing office stock undergoes space re-configuration to cater to flexible-working trends. Digital twins enhance lifecycle cost calculations, reducing change-order disputes. For new builds, stricter sustainability criteria point to higher adoption of low-carbon cement and recycled aggregates. Contractors balancing both pipelines cushion cyclicality; renovation margins outstrip greenfield averages by 200-300 basis points due to lower material exposure. Market watchers expect renovation share to approach 24.60% by 2031 as asset-management maturity grows.

By Construction Method: Conventional Supremacy Meets Modular Growth

Traditional on-site methods held a 92.85% share of the Oman construction market size in 2025. Familiar workflows, ample lay-down space, and entrenched supplier networks sustain the preference. However, modular solutions sprint ahead at a 5.74% CAGR, boosted by labor quotas and timeline pressure on publicly funded schools and clinics. Pilot modular dormitories at Duqm reduced project schedules by 28%, winning praise from the Ministry of Housing. Regulatory bodies now offer fast-track permits for factory-finished units, providing a non-price competitive lever.

International players supply volumetric apartment modules, while local steel fabricators pivot to light-gauge frames for hybrid systems. Training academies backed by the Supreme Council for Planning roll out skilling programs in off-site assembly, underpinning workforce readiness. As cost curves fall, commercial developers targeting mid-market tenants embrace modular façades for repeatable room layouts. The pivot gradually erodes conventional share, but coexistence prevails as bespoke luxury builds and complex civil works still rely on labor-intensive approaches.

By Investment Source: Public Funding Dominates, Private Pulse Strengthens

Public expenditure owned 83.70% of the Oman construction market share in 2025, reflecting the state’s pivotal role in Vision 2040 execution. Ministries bundle housing, roads, and energy projects into multi-year frameworks, providing long-term demand visibility. Still, private capital climbs at a 5.03% CAGR as foreign-investment law changes grant 100% ownership in strategic sectors. PPP-style school and desalination projects move to financial close, demonstrating bankability. Islamic-finance instruments such as sukuk offer alternative funding routes for mixed-use schemes.

Developers, including Majid Al Futtaim and Shumookh Investments, accelerate mall and logistics park builds, diversifying beyond Muscat. The sovereign wealth fund’s co-investment model helps de-risk private participation in large ports and industrial estates. Over time, a rising private contribution eases fiscal pressure and injects global know-how. Early movers secure land at preferential lease rates inside free zones, setting the stage for competitive advantages as market liberalization deepens.

Geography Analysis

Muscat preserves leadership at 40.92% of the 2025 project value, leveraging administrative centrality, high population density, and ongoing airport and urban-rail works. Landmark projects such as Sultan Haitham City and the airport’s Terminal 2 elevate demand for high-spec commercial and residential towers. Contractors with proven track records in congested inner-city sites win the majority of Muscat bids, where stringent green-building codes mandate energy-saving façades and smart-metering systems. Muscati developers also pilot net-zero office retrofits, signaling a pivot to sustainability-driven demand.

Dhofar’s USD 11 billion hydrogen cluster propels the southern governorate into the fast-growth tier with a 4.93% forecast CAGR. Megawatt-scale electrolysers, wind farms along the coastal ridge, and supporting export terminals command multidisciplinary EPC expertise. The national railway’s final leg into Salalah port further crowds in ancillary warehousing and workforce housing needs. Local SMEs benefit from procurement rules that allocate 10% of package value to domestic suppliers, catalyzing industrial-base diversification. Authorities clear fast-track environmental approvals for renewable projects, shortening start-up cycles.

The remaining nine governorates collectively mirror the push for balanced regional development under the National Spatial Strategy. Al Batinah North courts logistics and light industry tied to Sohar Port’s USD 4 billion 2024 expansion. Al Dakhiliya’s cultural corridors spark boutique hotel and heritage-rehab ventures, while Al Wusta’s 150 km² renewable zone invites solar EPC packages. Rail corridors and new ring roads integrate these regions into national freight networks, tightening delivery times and lowering project logistics costs. The broadening map of active sites encourages contractors to build decentralized material depots and mobile workforce hubs.

Competitive Landscape

Domestic majors Galfar Engineering, Bahwan Engineering, and Al Turki Enterprises anchor the market, leveraging historic ties with tender boards and deep project portfolios. International heavyweights Bechtel, Larsen & Toubro, Samsung Engineering enter via joint ventures to satisfy Omanisation quotas that now mandate 35% national labor on new federal contracts. Alliance structures blend local network strengths with global technical credentials, crucial for complex rail and hydrogen jobs. Contractors that invest in BIM Level 2 capability differentiate on clash-detection efficiency, winning design-build packages at tighter margins.

Competition intensity sharpens in the mid-tier as private mixed-use and hospitality schemes balloon. Developers favor firms demonstrating modular prowess and guaranteed schedule adherence. Newcomers from the European market are offering carbon-neutral construction solutions, banking on the Ministry of Environment’s tighter emissions rules. Meanwhile, the expatriate visa cap pushes firms to launch upskilling academies for citizens, aligning with national employment plans. Companies meeting In-Country Value thresholds gain bid-score advantages, influencing procurement outcomes more than headline price alone[3]MDPI, M. Al-Balushi, “Digital Maturity of Omani Builders,” mdpi.com.

Technology adoption is a rising battleground. BIM-to-field platforms cut rework by 25% on recent school builds, prompting the Ministry of Education to stipulate digital-first workflows on its 2025 tender for 12 schools. Firms integrating drone progress tracking and AI-driven safety analytics reduce insurance premiums, further improving bid competitiveness. With green hydrogen and rail contracts demanding stringent HSE protocols, safety-performance metrics become tender differentiators. As such, market leaders refine integrated digital and sustainability value propositions to shield market share against agile entrants.

Oman Construction Industry Leaders

Galfar Engineering & Contracting SAOG

Bahwan Engineering Group

Bechtel

Larsen & Toubro Oman

Consolidated Contractors Company (CCC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: KCA Deutag Energy won a 10-year, USD 550 million drill-rig build for Petroleum Development Oman, reserving 40% spend for domestic suppliers and creating 190 local jobs.

- June 2024: Hydrom closed two Dhofar green-hydrogen EPCs worth USD 11 billion with EDF, J-POWER, Yamna, Actis, and Fortescue, slated for 1.38 million t annual output by 2030.

- June 2024: Ministry of Housing inked 35 contracts for Sultan Haitham City totaling OMR 1 billion (USD 2.6 billion) to deliver 7,000 homes over 5 million m².

- May 2024: Education Ministry issued design-and-build tender for 12 schools, targeting October 2025 awards and March 2028 completion.

Oman Construction Market Report Scope

A structure's erection, cladding, external finish, formwork, fixture, fitting of a service installation, and unloading equipment, machinery, materials, or similar tasks are all considered part of building construction.

A complete background analysis of the Omani construction market, including the assessment of the economy and contribution of sectors in it, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, geographical trends, and the impact of COVID-19 impact are included in the report.

The Omani construction market is segmented by sector (commercial, residential, industrial, infrastructure (transportation), and energy and utilities). The report offers market size and forecasts in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Muscat |

| Dhofar |

| Rest of Oman |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Muscat | |

| Dhofar | ||

| Rest of Oman | ||

Key Questions Answered in the Report

How big is the Oman Construction Market?

The Oman Construction Market size is expected to reach USD 7.27 billion in 2026 and grow at a CAGR of 3.08% to reach USD 8.46 billion by 2031.

What is the current Oman Construction Market size?

In 2026, the Oman Construction Market size is expected to reach USD 7.27 billion.

Who are the key players in Oman Construction Market?

Bechtel, Bouygues, McDermott, Daewoo Engineering & Construction Co. Ltd and Hyundai Engineering & Construction Co. Ltd are the major companies operating in the Oman Construction Market.

What years does this Oman Construction Market cover, and what was the market size in 2025?

In 2025, the Oman Construction Market size was estimated at USD 7.05 billion. The report covers the Oman Construction Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Oman Construction Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: