Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

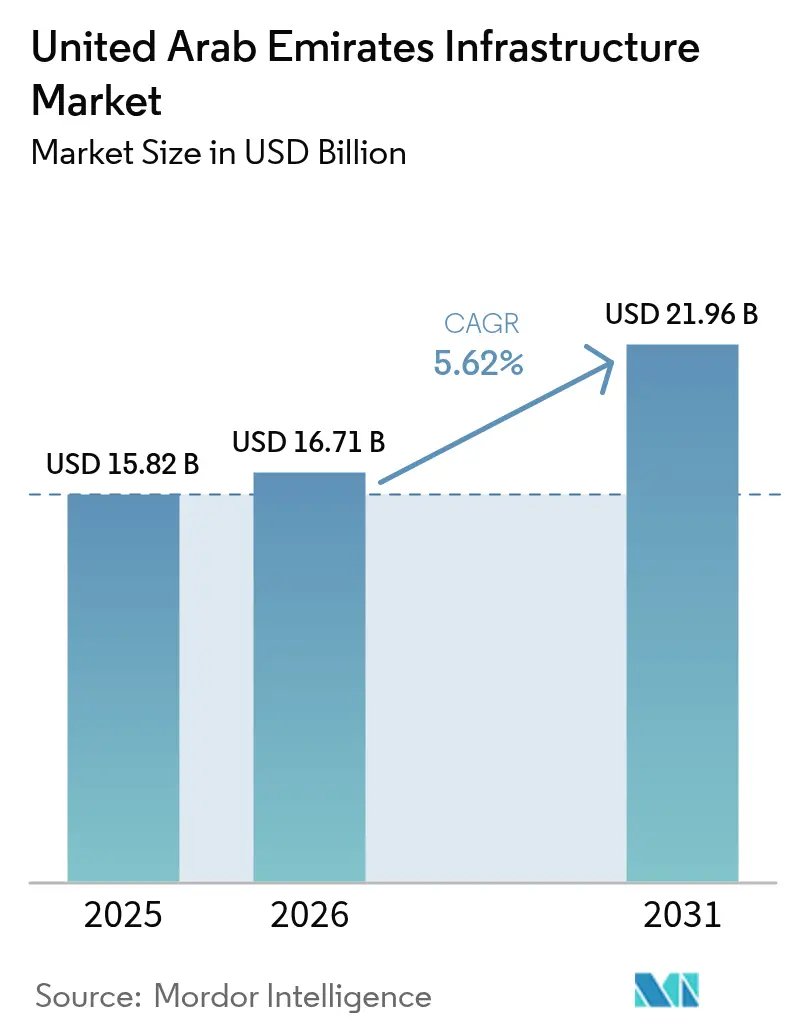

| Base Year Market Size (2025) | USD 15.82 Billion |

| Market Size (2026) | USD 16.71 Billion |

| Market Size (2031) | USD 21.96 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Infrastructure Market Analysis by Mordor Intelligence

The UAE Infrastructure Market size was valued at USD 15.82 billion in 2025 and estimated to grow from USD 16.71 billion in 2026 to reach USD 21.96 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031).

Sustained sovereign spending, rising private‐sector participation, and an economy-wide diversification agenda underpin this trajectory. Government capital outlays of AED 4.8 billion in Q1 2024 kept construction activity advancing at 6.2% even amid global macro headwinds[1]Federal Competitiveness & Statistics Centre, “UAE’s GDP hits AED430 billion in Q1 2024,” fcsc.gov.ae. Public commitment is reinforced by the “We the UAE 2031” vision that seeks to double non-oil exports and propel GDP to AED 3 trillion, shifting project pipelines toward multimodal logistics, industrial, and smart-city assets[2]UAE Government, “’We the UAE 2031’ vision,” u.ae . The UAE infrastructure market additionally gains momentum from megaprojects such as the Etihad Rail passenger service, the USD 35 billion Al Maktoum International Airport rebuild, and the USD 5.5 billion Ruwais LNG complex, each offering multi-year contract visibility. Private capital is crowding in through the National In-Country Value (ICV) program, which certified AED 205 billion of investments in 2024 and rewards firms that localize supply chains and technology.

Key risks lie in the volatile oil-price cycle that still steers fiscal space, a persistent skilled-labor shortage driving wage inflation, and intensifying cross-GCC competition for foreign direct investment. Nonetheless, the UAE infrastructure market continues to pivot toward high-value segments such as extraction, renewable utilities and AI-enabled transport systems, setting the stage for steady topline growth, improved project economics and widening opportunities for experienced EPC contractors and specialized service providers.

Key Report Takeaways

- By infrastructure category, transportation led with 38.02% revenue share in 2025, while extraction is projected to post the fastest 7.88% CAGR through 2031.

- By construction type, new builds accounted for 78.86% of the UAE infrastructure market size in 2025; renovation is set to accelerate at a 7.61% CAGR to 2031, buoyed by federal retrofit mandates.

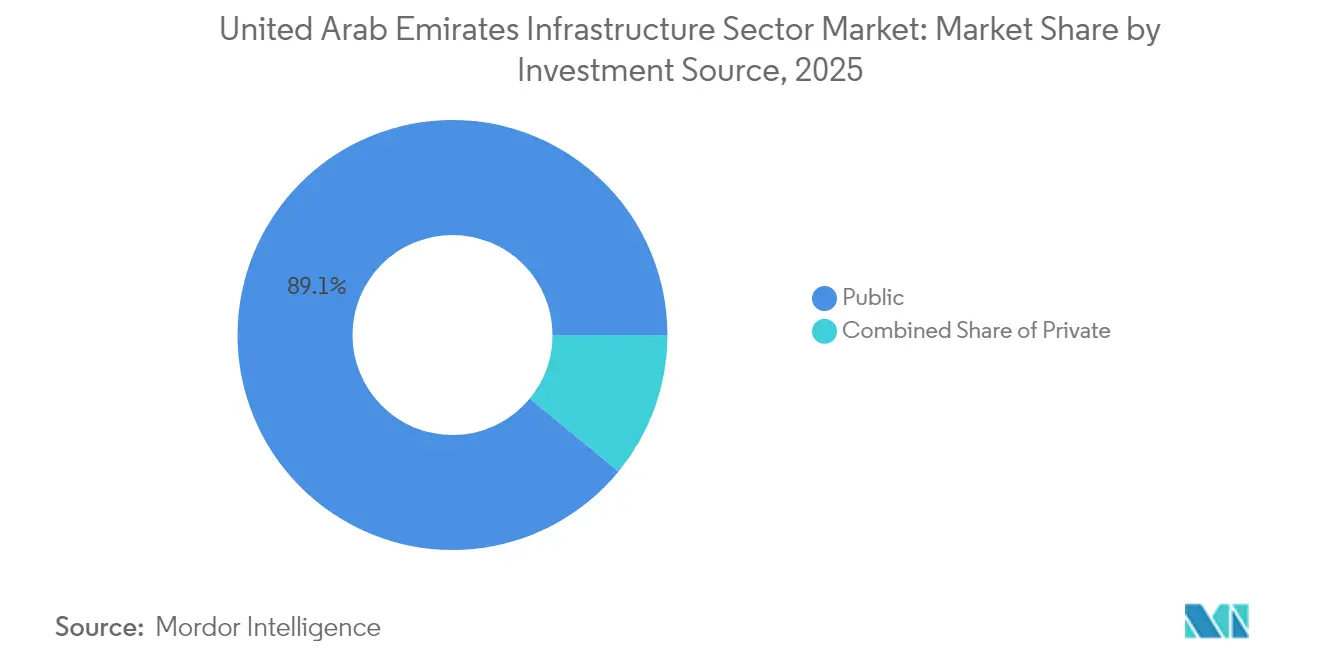

- By investment source, public funding retained 89.05% of the UAE infrastructure market share in 2025, yet private investment is forecast to grow 8.42% annually through 2031.

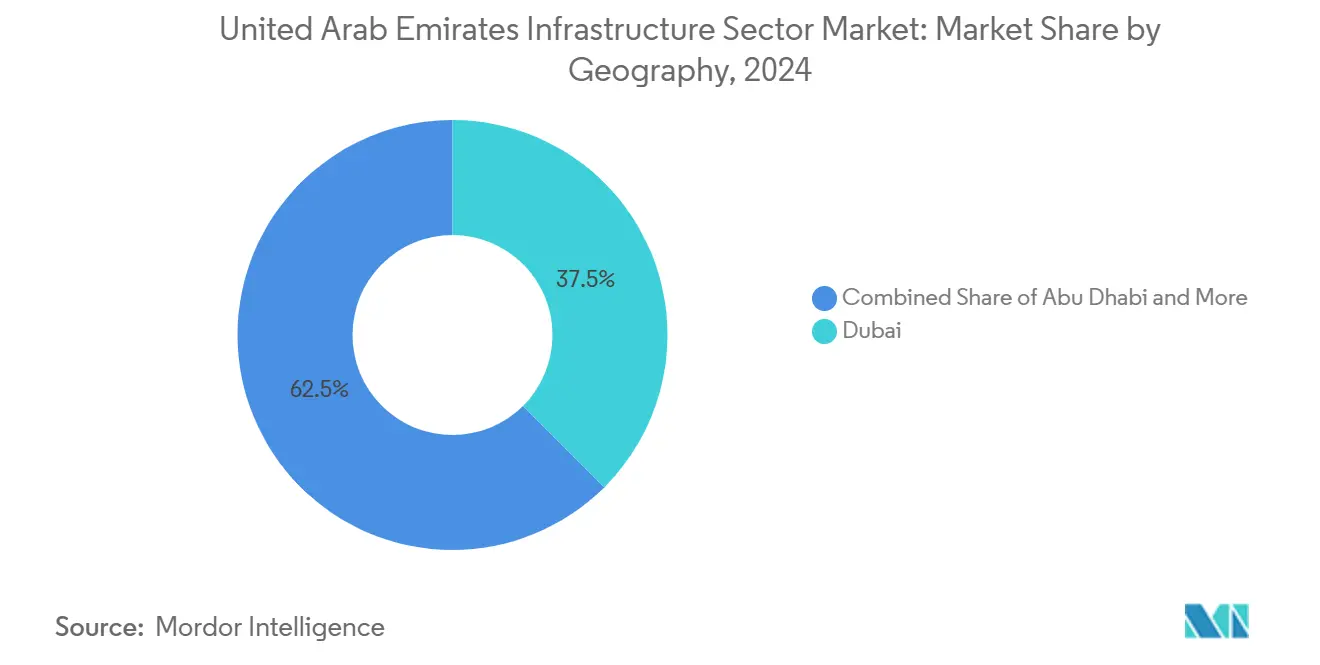

- By geography, Dubai captured 37.12% of 2025 spending, whereas Abu Dhabi is on track for the highest 7.32% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diversification under “We the UAE 2031” vision | +1.2% | National, led by Dubai & Abu Dhabi | Long term (≥ 4 years) |

| Rising green-bond issuance for sustainable assets | +0.8% | National renewables clusters | Medium term (2-4 years) |

| Tourism-oriented megaprojects after COP-28 | +0.6% | Dubai & Abu Dhabi | Short term (≤ 2 years) |

| ICV program boosting local sourcing | +0.5% | Industrial zones countrywide | Long term (≥ 4 years) |

| Mandated retrofit of federal buildings | +0.4% | Nationwide government districts | Medium term (2-4 years) |

| AI traffic-flow optimization demand | +0.3% | Smart-city corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Economic Diversification Under “We the UAE 2031” Vision

The diversification roadmap commits AED 300 billion to manufacturing and prioritizes space, clean-energy and pharmaceutical value chains, each demanding bespoke logistics hubs, utilities and testing facilities[3]Emirates News Agency, “Operation 300bn to advance UAE industrial sector,” wam.ae. Emirates Development Bank’s AED 30 billion financing window is already underwriting factory clusters and SME parks that require heavy-infrastructure tie-ins, fast-tracking tender pipelines in free zones across Abu Dhabi’s Khalifa Industrial Area and Dubai’s Jebel Ali. Non-oil export targets of AED 800 billion elevate the need for deep-water berths, bonded warehouses and multimodal connectors, pivoting the UAE infrastructure market toward outward-looking assets rather than purely domestic consumption platforms.

Sharply Rising Green-Bond Issuances Funding Sustainable Infrastructure

ALTÉRRA’s USD 30 billion catalytic commitment aims to unlock USD 250 billion for climate-aligned assets worldwide by 2030, with priority deployment into UAE solar, hydrogen and smart-grid projects. The Mohammed bin Rashid Al Maktoum Solar Park, backed by successive green-bond tranches, has already reached 5 GW of installed capacity while delivering record tariffs, illustrating how sustainable finance is lowering the weighted-average cost of capital for large-scale clean-energy infrastructure. Contractors exhibiting verifiable ESG metrics now enjoy preferred-bidder status on federal tenders, incentivizing rapid upgrading of project delivery standards.

Tourism-Led Megaprojects Ahead of COP-28 Legacy Build-Out

Dubai’s airport expansion to 260 million passengers annually and its 2040 master-plan road upgrades anchor near-term workloads for runways, interchanges and automated people movers. Abu Dhabi mirrors this push through cultural districts and cruise-terminal refurbishments that complement its LNG growth platform, signaling a broadening of the UAE infrastructure market beyond hydrocarbons toward hospitality, retail and mixed-use ecosystems[4]COP28, “UAE commits USD 30 billion in catalytic capital,” cop28.com.

Mandatory In-Country Value Program Boosting Local Sourcing

ICV scoring now weighs up to 10% of bid evaluations on federal projects, encouraging EPCs to establish fabrication yards, training academies and R&D centers inside the UAE. Certified firms secured AED 205 billion of awards in 2024, up 20% year-on-year, underscoring the materiality of localization to the UAE infrastructure market. The ripple effect is a deeper industrial base that reduces import dependency and embeds high-skill employment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile oil-price cycle curbing fiscal space | -1.1% | Hydrocarbon-heavy emirates | Short term (≤ 2 years) |

| Skilled-labor shortages inflating wages | -0.7% | Dubai & Abu Dhabi | Medium term (2-4 years) |

| Cross-GCC FDI competition | -0.5% | Region-wide | Medium term (2-4 years) |

| ESG tender pre-qualifications raising costs | -0.4% | Major government projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortages Driving Wage Inflation

Rapid project starts have stretched the skilled workforce. ALEC Engineering lifted headcount 46% to almost 40,000 in 2024 yet still flags deficits in BIM specialists and certified welders. Parallel mega-projects, including Etihad Rail, high-speed interchange upgrades and data-center campuses, compete for the same talent, pushing daily wage rates up 9-11% and tightening bid margins across the UAE infrastructure construction market.

Cross-GCC Competition for FDI Diverting Capital

Saudi Arabia’s NEOM, Qatar Energy’s LNG expansions and Oman’s port corridor initiatives collectively exceed USD 2 trillion in announced value, offering global investors multiple pathways outside the UAE. This rivalry necessitates aggressive regulatory reforms, localized incentives and superior execution records for UAE entities to retain deal flow, shaping a more competitive landscape for financing and for the UAE infrastructure construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Extraction Growth Outpaces Transportation Leadership

Extraction projects recorded the highest forecast CAGR at 7.88%, even though transportation accounted for 38.02% of 2025 revenues and retained primacy in absolute terms. Extraction momentum stems from ADNOC’s USD 15 billion 2025-2029 capex aimed at boosting gas-processing capacity 30% and lifting EBITDA 40%. Ruwais LNG’s USD 5.5 billion award spotlights rising demand for cryogenic storage, deep-water jetty work, and carbon-capture modules, all high-margin niches within the UAE infrastructure market size. Transportation continues to dominate value owing to publicly funded rail, highway, and airport schemes, with the Etihad Rail passenger service set to link 11 cities at 200 km/h and contribute AED 145 billion to GDP over a 50-year horizon.

Utilities infrastructure, led by the 5 GW Mohammed bin Rashid Al Maktoum Solar Park, persists as a strategic third pillar, attracting grid-reinforcement and battery-storage contracts. Social infrastructure is buoyed by mandatory energy retrofits, where envelope upgrades and HVAC overhauls deliver 27% consumption savings and propel specialist contractors into ascendant positions within the UAE infrastructure construction market. High-specification extraction facilities such as the USD 9 billion Hail & Ghasha gas project equipped with integrated CO₂ capture illustrate how low-carbon mandates are recasting engineering design standards across all infrastructure classes.

By Construction Type: Renovation Surges Amid New-Build Dominance

New-build assets captured 78.86% of 2025 spending, reflecting the still-expanding urban footprint; however, renovations’ 7.61% CAGR through 2031 underscores a pivot to asset-life optimization. The UAE infrastructure market share for renovation rises as federal retrofits target 60 government buildings in phase one, with studies indicating façade insulation can slash peak-summer HVAC loads 19.7%. Decree-Law No. 11 compels corporate landlords to embed emission-reduction pathways by 2025, triggering backlog conversions in offices, malls, and hotels.

While greenfield airport terminals, LNG trains, and industrial parks sustain contractor orderbooks, retrofit work is gaining profitability due to shorter cycles, lower capital intensity, and premium technology content. Smart-building retrofits integrate IoT sensors, BMS platforms, and renewable micro-grids, creating recurrent O&M revenue streams. The Dubai Universal Design Code and updated Building Code also raise specifications for accessibility and seismic resilience, reinforcing the UAE infrastructure construction industry’s transition toward performance-driven project awards.

By Investment Source: Private Momentum Narrows the Gap

Public expenditure remained dominant at 89.05% in 2025, yet private capital’s 8.42% CAGR signals a structural rebalancing of the UAE infrastructure construction market. The ALTÉRRA vehicle illustrates hybrid financing models in which government seed capital crowds in private investors for climate-aligned assets valued at USD 30 billion. Sovereign wealth funds amplify this effect; Mubadala alone oversees AED 1.1 trillion in AUM and deployed AED 89 billion toward data centers, renewables, and mobility infrastructure in 2024.

Legal reforms play a catalytic role. The new competition law mandates pre-clearance for deals above AED 300 million, offering clarity that emboldens overseas investors while encouraging domestic consolidation. Liberalized foreign-ownership rules in 2024 allowed 100% stakes in 1,000+ activities, unleashing fresh capital pools into logistics warehousing, district cooling, and telecom fiber backbones segments historically off limits to non-locals. The UAE infrastructure market, therefore, exhibits a virtuous cycle where public anchors, private follow-ons, and blended-finance structures accelerate project throughput.

Geography Analysis

Dubai, holding 37.12% of 2025 spend, sustains leadership by virtue of its role as regional trade and tourism hub and its proclivity for fast-tracked megaprojects. The USD 35 billion Al Maktoum International Airport revamp targets 260 million passengers annually and signals continued commitment to aviation supremacy. Complementary smart-traffic deployments expanded adaptive-signal coverage from 11% to 60% of arterial corridors, cutting journey times 61% and unlocking land value in peripheral districts. Dubai’s 2040 Urban Master Plan envisages the population doubling to 7.8 million, generating AED 65 billion housing and transit demand and cementing a robust pipeline for the UAE infrastructure market.

Abu Dhabi delivers the fastest 7.32% CAGR through 2031, propelled by the Ruwais LNG complex, Hail & Ghasha gas fields and federal retrofit clusters concentrated in the capital. ADNOC’s plan to double LNG capacity to 15 million tpa places Abu Dhabi at the heart of Middle Eastern gas logistics and related pipeline and berth builds. Regulatory innovation also differentiates the emirate: QR-code-enabled construction signboards now broadcast live compliance data, elevating transparency and embedding digital site management norms.

Sharjah and northern emirates capitalize on Etihad Rail’s 1,200 km network, with stations in Fujairah and Ras Al Khaimah facilitating freight diversification and tourism flows at 200 km/h service speeds. Sharjah’s 34 km² Mleiha National Park demonstrates ecotourism infrastructure’s rising prominence, while the Hafeet Rail link to Oman opens new cross-border corridors for aggregate, cement and processed-foods exports. Collectively, these developments broaden the UAE infrastructure construction market’s geographic dispersion, reducing reliance on Dubai-Abu Dhabi duopoly and enhancing inclusive growth.

Regulatory Landscape

Infrastructure construction in the UAE operates under a federal framework (including Federal Law No. 2 of 2016 governing general construction works), with day-to-day permitting, inspections, and completion certification handled at emirate level. In Dubai, the Dubai Development Authority oversees construction permitting and inspection workflows, while Dubai Municipality administers technical requirements through the Dubai Building Code. In Abu Dhabi, the Abu Dhabi International Building Code (ADIBC) is used as a core reference for building safety and performance.

Compliance requirements are widening beyond traditional HSE to include digital delivery and sustainability conditions. Dubai project submissions increasingly include BIM deliverables aligned to ISO 19650, alongside IFC-style interoperability expectations. Meanwhile, federal and emirate-level Net Zero 2050-aligned retrofit and efficiency programs embed measurable energy, water, and carbon outcomes into public procurement and approvals, which increases the burden on contractors for documentation, reporting, and as-built handover.

Value Chain Analysis

The UAE infrastructure value chain is anchored by government clients and state-linked sponsors that originate and fund large programs (federal entities such as the Ministry of Energy and Infrastructure, and emirate-level bodies such as Dubai RTA, alongside strategic asset owners like ADNOC and Etihad Rail). These clients contract master planners and design consultants for feasibility, permitting, and detailed design, then award to EPCs and specialist contractors, often through consortia that combine international engineering and technology capability with local delivery capacity and localization credentials. Downstream, operators and O&M providers monetize long-life assets (transport corridors, utilities networks, desalination and power plants), with performance-based maintenance and lifecycle upgrades becoming more prominent as retrofit mandates expand.

On the supply side, building materials and MEP equipment suppliers (steel, concrete, cables, pumps, HVAC and controls) face lead-time and price volatility, and skilled-labor shortages continue to pressure execution and margins on fast-tracked programs. Procurement is shifting toward earlier contractor involvement, negotiated packages for critical-path scopes, and longer-term supply agreements. Localization policies such as National In-Country Value (ICV) also encourage contractors to build UAE-based fabrication, warehousing, and training capacity to improve tender competitiveness and reduce import dependence.

Competitive Landscape

The market features moderate fragmentation, with the top five EPC contractors controlling a combined share comfortably below 30%. NMDC Energy tops local rankings with AED 55 billion in backlog, yet international behemoths such as Samsung E&A and Petrofac continue to clinch high-value LNG and petrochem awards, reflecting cross-GCC mobility and deep balance sheets. Regional champions like ALEC Engineering are scaling rapidly through diversification into Saudi Arabia’s Qiddiya and modular factory investments, registering 29% revenue growth and 46% workforce expansion in 2024.

Technology serves as a critical differentiator. The RTA’s 20% wait-time reduction via AI traffic-signal controls sets a precedent, pushing contractors to bolster digital engineering and cybersecurity capabilities. The ICV framework rewires competitive priorities, local fabrication yards, Emirati workforce ratios, and R&D outlays now directly influence tender scores. Consortia models gain traction, evidenced by Technip Energies-JGC-NMDC’s USD 5.5 billion Ruwais LNG win, which pooled FEED, execution, and marine-dredging expertise to satisfy aggressive schedule and localization benchmarks.

White-space opportunities emerge in data-center infrastructure, with plans for a 5 GW AI campus requiring hyperscale power, cooling and fiber routes. Modular building specialists and advanced-prefab suppliers are poised to capture share as developers pursue cost-certainty and accelerated delivery. Meanwhile, ESG reporting guidelines introduced by Dubai Financial Market compel public companies to disclose 32 metrics, a requirement that favors established contractors with mature environmental management systems, but also creates niches for boutique sustainability consultancies.

United Arab Emirates Infrastructure Industry Leaders

Aegion Corp

Bechtel

AE Arma-Electropanc

CB&I LLC

Fluor Corp

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is concentrated around large, multi-year public programs expanding essential networks such as urban road capacity, water and sewerage systems, and national transport links. Delivery is increasingly tied to structured contracting and PPP-style models, with Dubai RTA and Dubai Municipality-led packages translating master plans into sizable awards for roads and underground utilities. Abu Dhabi has also signaled an expanded PPP pipeline for transport and infrastructure, which creates entry points for developers, EPCs, operators, and financiers who can price long-duration risk and deliver performance-based O&M.

The market also presents whitespace for technology-led and sustainability-linked delivery, particularly where public clients tie procurement to measurable outcomes and digital handover. Federal retrofit initiatives targeting government buildings, alongside municipal BIM requirements in Dubai, are supporting recurring demand for energy and water efficiency upgrades, BMS/IoT integration, and data-driven asset management, which benefits specialist contractors and system integrators. On funding, the UAE Federal Budget 2026 allocates AED 2.625 billion to the Infrastructure and Economic Resources Sector, providing a near-term anchor for federally sponsored works and demand pull across materials, MEP, and construction services.

Recent Industry Developments

- July 2026: Dubai Roads and Transport Authority (RTA) awarded an AED 2 billion contract for the Latifa bint Hamdan Corridor Development Project, covering major connectivity works including bridges and tunnels. The award underpins Dubai's near-term road-capacity build-out and creates demand across civil works, traffic systems, and adjacent utilities diversions through a multi-year delivery window.

- May 2026: ALEC Engineering and Contracting received a Letter of Award from DCT Abu Dhabi for Sphere Abu Dhabi, a large venue-led project. The award expands Abu Dhabi's pipeline and reinforces the role of diversified infrastructure and cultural assets in contractor backlogs and supply packages.

- November 2024: Siemens signed a contract with the UAE Ministry of Energy and Infrastructure to retrofit 60 government buildings, targeting energy and water savings and a CO2 reduction of 15,400 metric tons annually. The program institutionalizes performance-based retrofit work under the Net Zero 2050 agenda and expands demand for MEP modernization, controls, and measurement and verification services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the UAE infrastructure sector market is defined as the value of construction activity tied to building and upgrading core physical infrastructure across the country, captured in USD and aligned to investment-led project execution.

Scope exclusions: This sizing excludes routine operations and maintenance spend that does not extend asset life or create new capacity.

Segmentation Overview

- By Infrastructure

- Transportation Infrastructure

- Utilities Infrastructure

- Social Infrastructure

- Extraction Infrastructure

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Geography

- Abu Dhabi

- Dubai

- Sharjah

- Rest of UAE

Data Sources, Market Sizing, and Validation

Desk Research

Desk research set the starting point by anchoring the model on the UAE project environment and macro signals that influence public and private capex. We relied on open sources such as UAE Federal Competitiveness and Statistics Centre releases, central bank and ministry publications, IMF and World Bank macro series, and trade and customs statistics that help explain equipment import intensity for large projects.

To make the market definition practical, we also reviewed infrastructure pipeline disclosures from government entities, publicly available procurement and tender notices, and disclosures in annual reports and investor presentations of relevant contractors and developers. Where needed, we used paid subscriptions for company financials and intelligence, news and financials, and global contracts and tenders to sanity-check project timing, award patterns, and revenue recognition behavior. The sources listed here are illustrative, and many other references were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk sources cannot fully show, especially how budgets translate into real execution and billing across emirates. We spoke with a mix of owners, consultants, EPC and contractors, and materials and equipment participants to confirm scope boundaries, typical cost splits, and how new build versus renovation is being counted in practice. For a UAE-only market, discussions were balanced across Abu Dhabi, Dubai, and the remaining emirates so assumptions reflect different procurement styles and project maturity levels.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | |

| Mid tier: 47% | Functional/Unit leaders: 31% | |

| Smaller Players: 16% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where public and private infrastructure outlays are reconstructed using budget signals, project award and execution cycles, and UAE macro context, then translated into annual market value for infrastructure construction activity. Once that total is built, it is corroborated with selective bottom-up approximations, such as sampled project cost benchmarks, contractor revenue exposure checks, and a simple value = volume x average cost logic for repeatable asset types. This step helps adjust for timing gaps.

Key inputs that shaped the model included the active and planned project pipeline by emirate, the mix of transportation, utilities, social, and extraction-linked infrastructure, new construction versus renovation shares, funding source split between public and private, and the typical lag between award, mobilization, and revenue booking. Where inputs were incomplete, we used ranges validated through interviews and then applied conservative mid-points, followed by sensitivity checks to see how totals move under faster or slower execution.

For forecasting, scenario analysis was used around project conversion rates and capex phasing, and then the chosen path was aligned to expert views on policy priorities, fiscal space, and likely tender cadence. The final forecast is therefore traceable to a small set of repeatable variables that can be refreshed as new awards, budgets, or delays become visible.

Data Validation & Update Cycle

Validation is done in layers so the totals do not rely on a single indicator. We compare the modeled market movement against independent signals such as award announcements, tender activity, large-project milestones, and reported revenue trends, and then investigate any unusual jumps before sign-off.

A second analyst review is applied to key assumptions such as execution lags, renovation shares, and currency conversion timing, followed by targeted re-contacts when a major variance shows up. Reports are refreshed annually, and interim updates are made when material events occur such as large budget changes or project rescoping. Before delivery, a final pass is completed so clients receive an updated view based on the latest public information and primary feedback.

Mordor Intelligence's UAE Infrastructure Sector Market Estimate Compared With Other Published Estimates

Published market sizes for UAE infrastructure can look far apart because the market boundary is not always handled the same way, and the timing of when projects are counted can shift totals by a lot. Differences usually come from what is treated as infrastructure versus broader construction, how renovation is counted, and whether pipeline values are confused with annual execution.

By tracking project awards, execution lags, and emirate-level phasing in the model, Mordor Intelligence keeps the UAE infrastructure total tied to what is realistically delivered in-year, rather than rolling up long pipeline values as if they were revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.82 B (2025) | |

| Regional Consultancy A | USD 22.50 B (2023) | Uses an earlier base year and a broader infrastructure definition that reads closer to overall construction-linked development, which can inflate the value when adjacent building activity is included. |

| Trade Journal B | USD 5.94 B (2025) | Anchors estimates heavily on macro and GDP-style parameters and related company revenue proxies, which can understate years where large public projects are active but revenue recognition is uneven across participants. |

The spread in the table mainly comes down to scope boundary and the timing logic used to convert pipeline and budgets into annual market value. When the definition is kept focused on infrastructure execution and the same timing rules are applied each year, the outputs become easier to compare and to refresh when new awards or delays occur.

Key Questions Answered in the Report

What is the current value of the UAE infrastructure construction market?

The UAE infrastructure market size reached USD 16.71 billion in 2026 and is projected to hit USD 21.96 billion by 2031.

Which infrastructure segment is growing the fastest in the UAE?

Extraction infrastructure leads growth with an 7.88% CAGR, bolstered by ADNOC’s multi-billion-dollar gas-expansion program.

How quickly is private investment in UAE infrastructure expanding?

Private capital is forecast to rise at an 8.42% CAGR through 2031, narrowing the gap with historically dominant public funding.

Which emirate shows the strongest growth outlook?

Abu Dhabi is expected to record the highest 7.32% CAGR to 2031 on the back of LNG, gas-processing and government retrofit projects.

What technological trends are shaping new UAE infrastructure projects?

AI-driven traffic management, digital-twin simulations and ESG-linked procurement standards are reshaping design and delivery practices.

Page last updated on: