Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

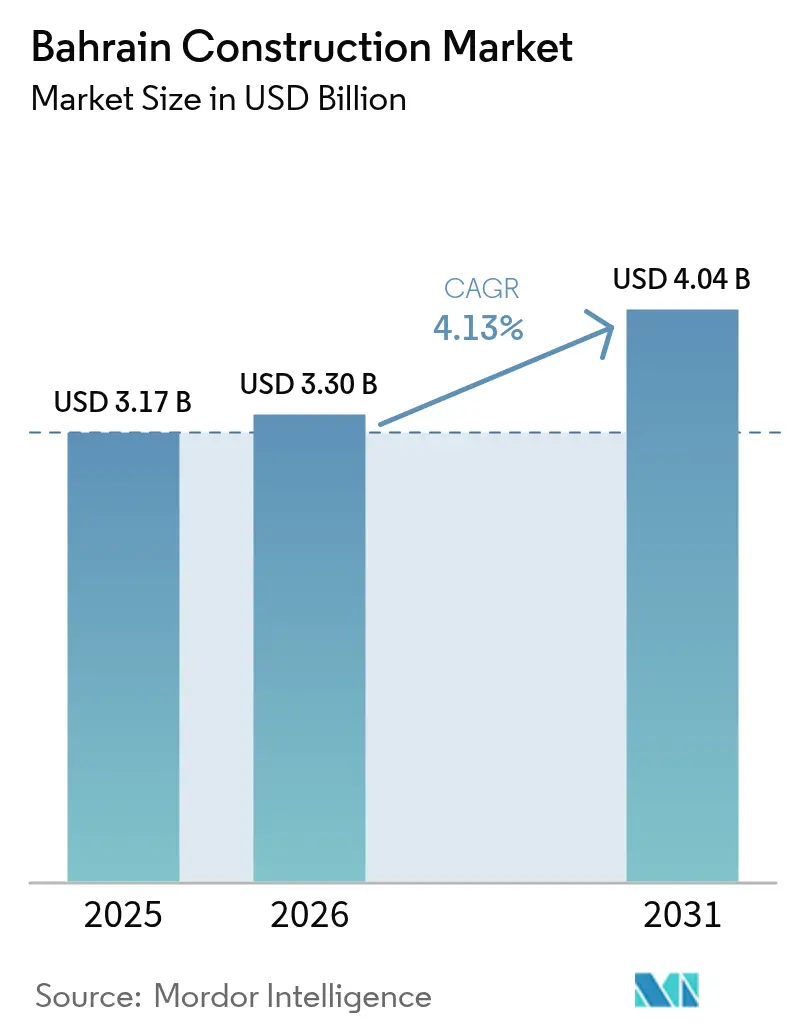

| Base Year Market Size (2025) | USD 3.17 Billion |

| Market Size (2026) | USD 3.3 Billion |

| Market Size (2031) | USD 4.04 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

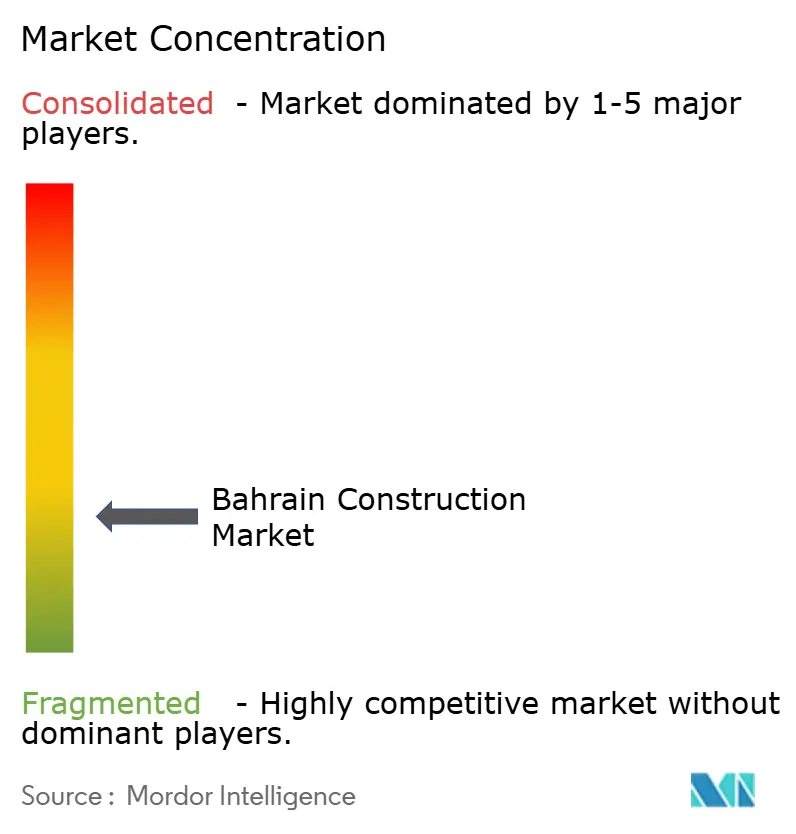

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Construction Market Analysis by Mordor Intelligence

The Bahrain Construction market size is expected to grow from USD 3.17 billion in 2025 to USD 3.3 billion in 2026 and is forecast to reach USD 4.04 billion by 2031 at 4.13% CAGR over 2026-2031. This steady expansion is anchored in Vision 2030, which channels public-private capital into large infrastructure corridors while maintaining fiscal discipline. Government-backed outlays for the USD 2 billion metro system, the USD 3.5 billion King Hamad Causeway, and a USD 30 billion multi-year infrastructure pipeline keep order books healthy even as material costs and skilled-labor shortages squeeze contractor margins. Rising green-building mandates, modular construction pilots, and digital-twin rollouts indicate that technology adoption is moving from proof-of-concept to mainstream application. These shifts position the Bahrain construction market as a regional test bed for advanced project-delivery methods, offering foreign contractors a gateway to the wider GCC.

Key Report Takeaways

- By sector, infrastructure led with 37.42% of Bahrain's construction market share in 2025, while residential projects are forecast to post the fastest 5.98% CAGR through 2031.

- By construction type, new-build activity accounted for 59.88% of the Bahrain construction market in 2025, whereas renovation is projected to expand at a 5.12% CAGR over the same period.

- By construction method, conventional on-site techniques held 91.67% of 2025 revenue; prefabricated and modular solutions are advancing at a 6.52% CAGR to 2031.

- By investment source, public funding secured 67.05% of 2025 spending, but private-sector flows are climbing at a 5.79% CAGR as PPP rules mature.

- By geography, Manama commanded 34.10% of 2025 activity, while Muharraq is poised for the quickest expansion at a 5.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased investment in infrastructure | +1.2% | National, concentrated in Manama and Muharraq | Long term (≥ 4 years) |

| Housing demand under Vision 2030 | +1.0% | National, with emphasis on Northern Governorate | Long term (≥ 4 years) |

| Focus on green buildings | +0.8% | National, with early adoption in commercial districts | Medium term (2-4 years) |

| Bahrain Metro PPP pipeline | +0.6% | Manama-Muharraq corridor | Medium term (2-4 years) |

| Liberalised free-hold laws for expatriates | +0.4% | Designated investment zones | Short term (≤ 2 years) |

| Digital-twin adoption cuts project delays | +0.2% | Major infrastructure projects nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Investment in Infrastructure

A USD 30 billion portfolio earmarked through 2030 is transforming Bahrain from a maintenance-focused builder into a network-centric economy. Flagship projects such as the USD 2 billion metro and the USD 7 billion BAPCO refinery upgrade demonstrate how long-dated PPP concessions can mobilize global contractors while shielding the treasury. Construction subsidies, sovereign guarantees, and streamlined tender rules shorten financial close and keep bid volumes high. Downstream, the surge lifts demand for steel fabrication, rail systems, and specialized engineering, creating a multiplier across the Bahrain construction market. With transport, energy, and digital grids moving in lockstep, infrastructure will remain the backbone of new contract awards over the next decade.

Housing Demand Under Vision 2030

The state plans to deliver 40,000 new dwellings by 2030, responding to population growth toward 2.3 million and chronic waiting lists for subsidized homes. Mixed-income master plans near planned metro stops improve land-use efficiency and support transit-oriented growth. PPP-financed communities like Al Madina Al Shamaliya signal how private capital can meet social targets without straining the budget. Liberalized foreign-ownership rules extend demand to long-term expatriates, broadening the buyer pool. These factors lift the residential slice of the Bahrain construction market and diversify revenue away from cyclical commercial towers.

Focus on Green Buildings

Mandatory LEED-aligned guidelines now apply to all public projects, turning sustainability from a niche add-on into a baseline specification. Developers weigh higher upfront costs against lower life-cycle energy bills and stronger tenant appeal, especially from multinationals with ESG mandates. Solar PV integration, water-saving fixtures, and recycled aggregates are becoming standard clauses in design briefs. Financial sweeteners—such as fast-track permits and reduced utility fees—further accelerate adoption. As a result, the Bahrain construction market is carving out a green-certified segment that attracts equipment suppliers and consultants specializing in low-carbon design[1]Ministry of Municipalities Affairs, “National Green-Building Guidelines,” municipality.gov.bh.

Bahrain Metro PPP Pipeline

The 35-year concession covering design, build, finance, operate, and maintain sets a new benchmark for risk allocation in the GCC. Automated trains, elevated viaducts, and integrated ticketing require specialist know-how, favoring consortia that blend civil works with rolling-stock technology. Successful delivery will cut road congestion and anchor new real-estate clusters around station nodes. Spin-off contracts for depots, utilities, and transit-oriented developments offer additional upside to contractors. The metro, therefore, links mobility gains with construction growth, reinforcing the Bahrain construction market’s momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction-material costs | -0.9% | National, with acute impact on large projects | Short term (≤ 2 years) |

| Skilled-labour shortages | -0.7% | National, particularly affecting specialized trades | Medium term (2-4 years) |

| Rising public-debt limits capital spending | -0.5% | National government projects | Long term (≥ 4 years) |

| Slow BIM uptake among SME contractors | -0.3% | National, concentrated among smaller contractors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Construction-Material Costs

Global steel and cement volatility has inflated tender prices by up to 20%, eroding contractor margins and prompting renegotiation of fixed-price deals. Bahrain’s heavy reliance on imports magnifies currency and freight swings despite local aluminum smelter capacity. To hedge risk, builders adopt escalation clauses, bulk-buying pools, and early procurement strategies. Authorities have eased customs processes for essential inputs, yet price uncertainty still deters smaller firms from bidding on large packages. If volatility persists, the Bahrain construction market could see project postponements until cost curves stabilize.

Skilled-Labour Shortages

Bahrainization quotas cap foreign labor at 70%, tightening access to experienced tradespeople just as mega-projects ramp up. Domestic training pipelines have yet to produce sufficient crane operators, welders, and MEP technicians, forcing contractors to recruit costlier specialists from abroad. A compulsory end-of-service fund adds to payroll expenses, further squeezing budgets. Companies respond by digitizing site workflows and piloting modular fabrication to cut labor intensity. Unless vocational programs pivot toward construction skills, the Bahrain construction market may face timeline slippage and higher delivery risk[2]Labour Market Regulatory Authority, “Expatriate Workforce Statistics 2024,” lmra.bh.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Retains the Lead While Housing Accelerates

Infrastructure contributed 37.42% of Bahrain's construction market revenue in 2025, underscoring its status as the kingdom’s primary growth engine. The residential slice, though smaller, is forecast to record a 5.98% CAGR through 2031, lifted by social-housing quotas and expatriate demand. Mega-links such as the metro and King Hamad Causeway dominate order books and channel procurement toward heavy-civil specialists. Meanwhile, commercial and industrial projects circle financial districts and free-trade zones, supporting diversification beyond oil. Vision 2030’s blended financing model keeps the pipeline robust even under fiscal ceilings.

Developers in Manama Bay are coupling mixed-use towers with green-building certifications to secure premium leases, while industrial players cluster near Khalifa Bin Salman Port to leverage logistics synergies. On the housing front, bundled PPPs offer off-balance-sheet solutions that align with budget rules. These dynamics ensure that both core civil works and vertical construction contribute meaningfully to the Bahrain construction market.

By Construction Type: New-Build Dominance Meets Growing Retrofit Demand

New developments captured 59.88% of 2025 turnover, reflecting the kingdom’s expansionary phase. Yet renovation is climbing at a 5.12% CAGR as aging stock faces code upgrades and energy-efficiency retrofits. Building-permit data show sustained momentum, with more than 2,600 approvals issued in Q1 2025. Government schemes offering low-interest retrofit loans and expedited green-certification pathways encourage owners to modernize. For contractors, retrofit jobs provide cash-flow smoothing between large greenfield wins.

Digital-twin models shorten survey cycles and improve cost forecasting for refurbishment packages, a capability now migrating from megaprojects to mid-rise apartments. This blended workload broadens revenue streams across the Bahrain construction market and supports the growth of specialist subcontractors focused on MEP upgrades, façade recladding, and structural reinforcement.

By Construction Method: Conventional Techniques Still Dominate but Modular Gains Traction

Traditional on-site building accounted for 91.67% of the 2025 value, mirroring entrenched contractor practices and regulatory familiarity. Prefabricated and modular systems, however, are registering a 6.52% CAGR, driven by labor scarcity and schedule compression. Early adopters in affordable-housing PPPs report 15% faster delivery and lower rework, bolstering the business case. Elevated metro corridors and airport expansions also tap modular steel assemblies for speed and safety advantages.

Government bodies now pilot factory-inspected components for social-housing pilots, signaling official support for industrialized construction. As supply chains mature and design codes adapt, modular penetration is expected to widen, diversifying delivery options within the Bahrain construction market.

By Investment Source: Public Funds Lead but Private Capital Is Catching Up

State spending delivered 67.05% of 2025 contracts, reflecting sovereign backing for transport, housing, and energy infrastructure. Private inflows are progressing at a 5.79% CAGR, enabled by 100% foreign-ownership rules and streamlined licensing. A USD 17 billion investment package unveiled with U.S. partners illustrates rising overseas appetite for Bahraini projects. Commercial landlords are also capitalizing on 7% gross rental yields, among the region’s highest, to finance office and hospitality builds.

PPP frameworks allocate construction risk to private consortia while offering availability-based returns, a structure now proven on the LNG terminal and being replicated for the metro. These models diversify funding channels and reduce reliance on the treasury, broadening the Bahrain construction market’s appeal to institutional investors.

Geography Analysis

Manama maintained 34.10% of 2025 spending, anchored by its role as the financial nucleus and by continuous upgrades to arterial roads and public-realm spaces. Projects such as the USD 107.42 million Al Fateh Highway expansion and the World Aquatics Centre highlight the city’s ability to attract sector-diverse capital. High-rise approvals around Bahrain Bay signal that prime land scarcity is channeling demand into vertical mixed-use formats. Regulatory bodies are fast-tracking permits for developments linked to metro station areas, aligning transport corridors with real-estate uplift and sustaining the Bahrain construction market in the capital.

Muharraq, though smaller, is projected to log a 5.72% CAGR to 2031, propelled by airport-adjacent logistics parks and first-phase metro stations. Residential schemes aim to capture unmet demand from aviation and tourism workers, while commercial parcels near waterfront promenades cater to SME tenants. The municipal council’s zoning revisions, which earmark transit-oriented districts for higher plot ratios, are catalyzing land trades and attracting master developers. This momentum positions Muharraq as the fastest-growing pocket within the Bahrain construction market.

Outside the northern corridor, the Southern and Central governorates host industrial estates, petrochemical expansions, and new social-housing clusters. UPDA’s land-use map shows residential footprints at 11.92% and nature reserves at 33.14%, underscoring the balancing act between growth and conservation. Public-private housing in Al Madina Al Shamaliya directs population spread away from the dense north, easing infrastructure load. Together, these regional strategies distribute construction opportunities across the kingdom and ensure that the Bahrain construction market is not overly reliant on a single urban center.

Competitive Landscape

A mid-range concentration typifies the Bahrain construction market, where local champions such as Nass Corporation and Haji Hassan Group leverage government relationships to secure civil packages, while global majors like Larsen & Toubro and Parsons target tech-heavy megaprojects. Tender frameworks prioritize track record in PPP delivery, sustainability compliance, and digital capability, steering awards toward firms with integrated design-build-operate offerings. Joint ventures blend indigenous knowledge with international best practice, mitigating execution risk on complex builds.

Technology has become a decisive battleground. Top-tier contractors deploy AI-assisted scheduling, drone site surveys, and IoT safety gear to trim overheads and win extension options. Smaller firms lag in BIM uptake, partly due to capital constraints, but government e-tender portals now require digital deliverables, nudging adoption. Sustainability credentials also sway bid evaluations; recycled-aggregate quotas and solar-ready roofing are increasingly embedded in specifications. These criteria raise entry barriers and intensify competition within the Bahrain construction market.

Strategic moves in 2024-2025 include Larsen & Toubro’s cross-country gas pipeline EPC win, which broadens its regional footprint, and Alba’s supply agreements that lock in aluminum for local curtain-wall fabricators. In parallel, Bahrain-based developers formed alliances with Gulf pension funds to seed mixed-use districts near forthcoming metro stops. Such alignments concentrate specialized skills and deep balance sheets, signaling that consortium-based models will dominate the next wave of awards.

Bahrain Construction Industry Leaders

Nass Corporation

Haji Hassan Group

Almoayyed Contracting Group

Cebarco Bahrain

Six Construct

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: A USD 17 billion investment accord was announced with U.S. firms, covering aviation, tech, and industrial assets.

- February 2025: The Ministry of Transportation and Telecommunications confirmed Phase 1 of the metro, 20 stations over 29 km under a 35-year PPP.

- January 2025: Bahrain enacted a 15% domestic minimum top-up tax for multinationals, aligning with OECD rules and prompting contractors to reassess corporate structures.

- March 2024: Larsen & Toubro won two 56-inch onshore gas pipelines, the firm’s largest Middle East EPC order.

Bahrain Construction Market Report Scope

Construction is an industry that includes the erection, maintenance, and repair of buildings and other immobile structures and the building of roads and service facilities that have become integral parts of structures and are essential to their use. The Bahraini construction market report covers a complete analysis of the industry, including current economic and market scenarios, market size estimation for key segments, and emerging trends in the market segments. The report also covers the impact of the COVID-19 pandemic on the market.

The Bahrain Construction Market is Segmented by Sector (Commercial Construction, Residential Construction, Industrial Construction, Infrastructure [Transportation] Construction, and Energy and Utilities Construction). The report offers market size and forecasts for the Bahrain Construction market in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Manama |

| Muharraq |

| Rest of Bahrain |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Manama | |

| Muharraq | ||

| Rest of Bahrain | ||

Key Questions Answered in the Report

How large is the Bahrain construction market in 2026?

It is valued at USD 3.3 billion and is forecast to reach USD 4.04 billion by 2031, growing at a 4.13% CAGR.

Which sector contributes the most to ongoing projects?

Infrastructure holds 37.42% of 2025 spending, led by the metro, causeway, and refinery upgrades.

Where is construction activity expanding the fastest geographically?

Muharraq is projected to log a 5.72% CAGR to 2031, supported by airport expansion and metro connectivity.

What is driving residential construction demand?

Government commitments to deliver 40,000 units and relaxed expatriate ownership rules are lifting housing orders.

How are rising material costs being managed?

Contractors use price-escalation clauses, early bulk procurement, and modular methods to hedge cost swings.

What role do PPPs play in new contracts?

Public-private partnerships finance large projects like the metro, shifting construction risk while ensuring long-term service delivery.

Page last updated on: