UAE Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

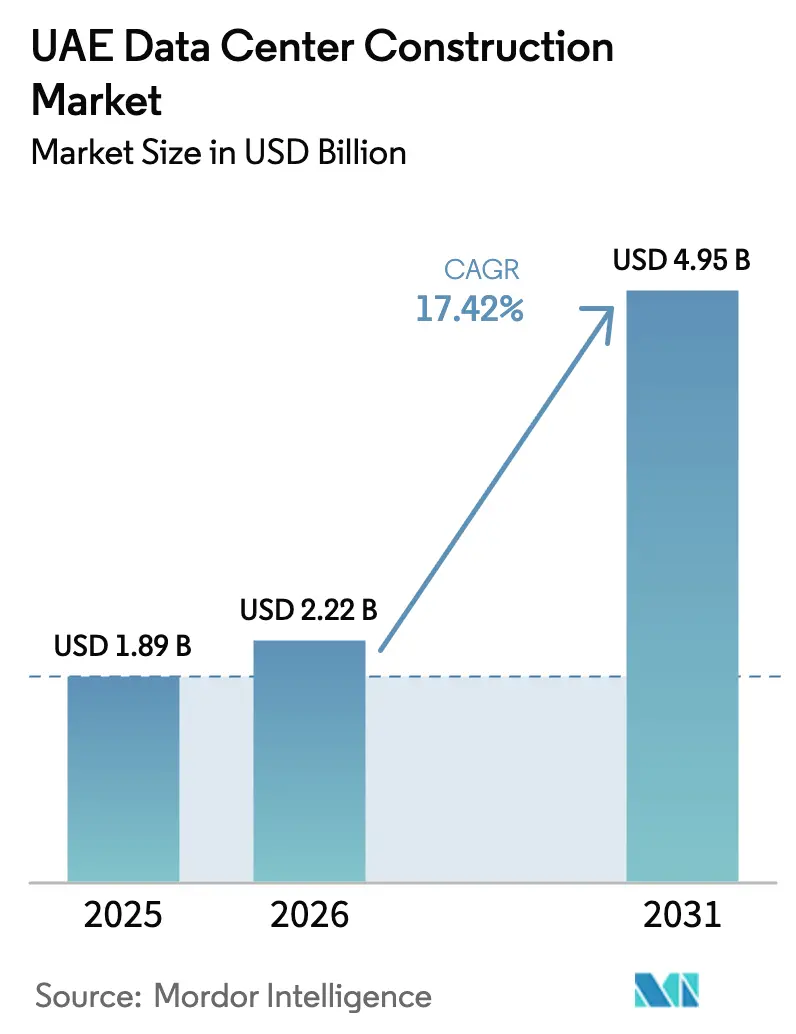

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 4.95 Billion |

| Growth Rate (2026 - 2031) | 17.42% CAGR |

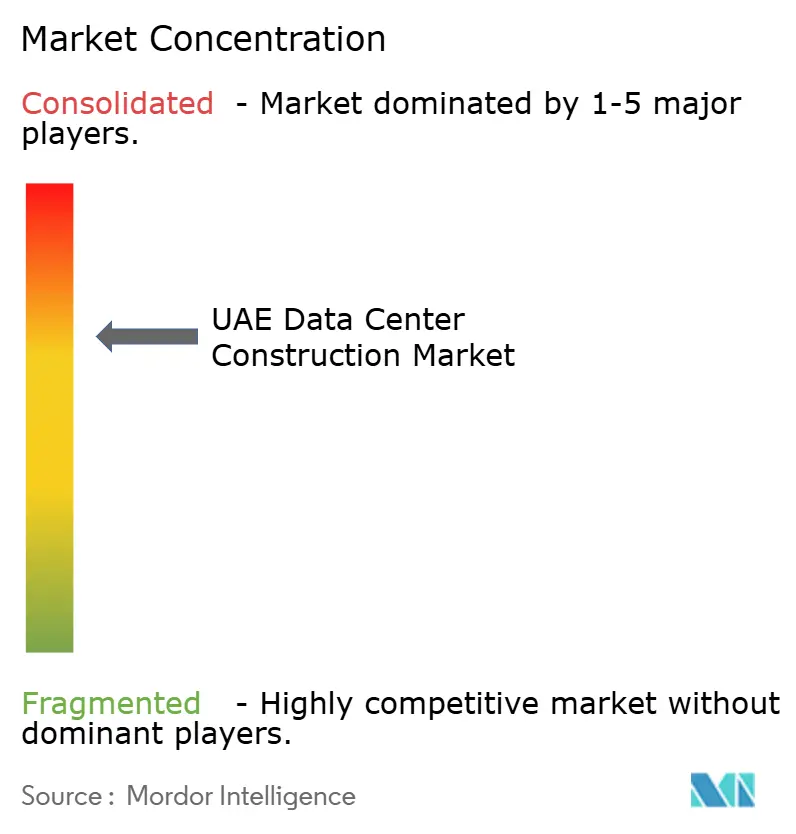

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Data Center Construction Market Analysis by Mordor Intelligence

The UAE data center construction market size in 2026 is estimated at USD 2.22 billion, growing from 2025 value of USD 1.89 billion with 2031 projections showing USD 4.95 billion, growing at 17.42% CAGR over 2026-2031. The UAE data center construction market is expanding because hyperscalers are building sovereign-cloud regions that comply with local data-residency rules while supporting artificial-intelligence (AI) workloads at unprecedented power densities. Government programs such as Abu Dhabi’s AED 13 billion Digital Strategy 2025-2027 are catalyzing large-scale public-sector demand for Tier IV-certified capacity, which in turn is attracting private enterprises seeking hybrid deployment options. Strategic partnerships—exemplified by Microsoft’s AED 2 billion alliance with du—are steering the UAE data center construction market toward purpose-built hyperscale campuses engineered for GPU-rich computing. Parallel green-finance incentives introduced around COP28 are prompting operators to integrate on-site renewables and innovative cooling technologies. At the same time, supply-chain constraints, material inflation and shortages of Tier III/IV-qualified labor threaten to temper the near-term build-out curve.

Key Report Takeaways

- By tier type, Tier 3 facilities held 48.25% of the UAE data center construction market share in 2025; Tier 4 facilities record the fastest growth at 19.86% CAGR through 2031.

- By data-center type, colocation services led with 70.55% revenue share in 2025, while self-build hyperscaler projects are expanding at a 22.45% CAGR to 2031.

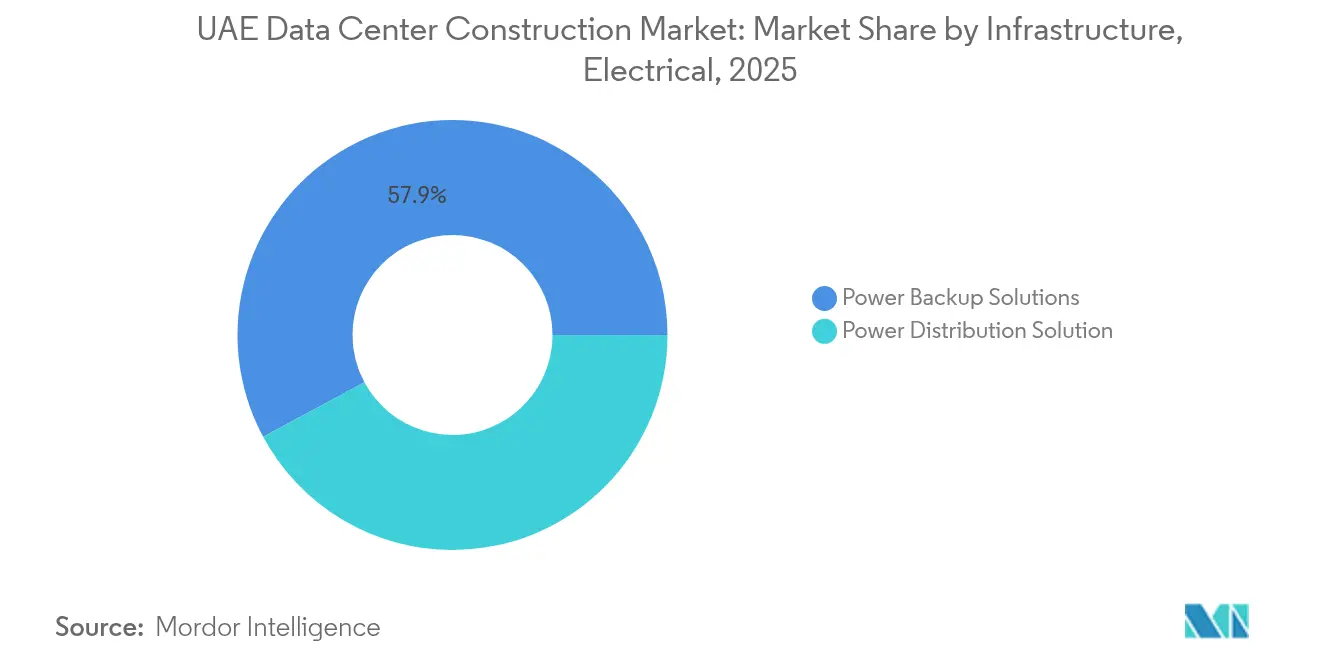

- By electrical infrastructure, power-backup systems accounted for 57.85% share of the UAE data center construction market size in 2025, with power-distribution solutions growing at 21.05% CAGR over 2026-2031.

- By mechanical infrastructure, cooling systems captured 55.9% of the UAE data center construction market size in 2025; servers and storage post the highest CAGR at 20.25% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing investments in cloud and AI workloads | +4.2% | UAE-wide, focused on Dubai and Abu Dhabi | Medium term (2-4 years) |

| Government-led digital-transformation programs | +3.8% | National, Abu Dhabi spearheading | Long term (≥ 4 years) |

| 5G- and IoT-fuelled edge-computing demand | +2.9% | Urban and industrial zones | Medium term (2-4 years) |

| Arrival of hyperscale cloud availability zones | +3.5% | Dubai and Abu Dhabi | Short term (≤ 2 years) |

| COP28-aligned green-finance incentives | +1.8% | Solar-rich regions | Long term (≥ 4 years) |

| Free-zone land-lease and tax holidays | +2.1% | Free zones across UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Investments in Cloud and AI Workloads

Rising AI demand is reconfiguring facility design, pushing power densities up to five times traditional levels as projects such as the planned 5 GW Abu Dhabi AI campus gain momentum. Khazna’s 100 MW AI-optimised complex in Ajman, which dedicates 20 halls to GPU clusters, illustrates how local operators are pivoting toward purpose-built layouts that favor liquid cooling and dense power distribution G42. This evolution is widening the competitive gap between legacy colocation halls and AI-native builds. The Microsoft-du alliance earmarks AED 2 billion to expand sovereign AI capacity in Dubai,[1]William Turton — “Microsoft, du Sign AED2 Billion Hyperscale Deal,” reuters.com signaling enterprise preference for infrastructure that is “future-proof” for upcoming AI migrations. As AI capability becomes a baseline expectation, even non-AI workloads are being contracted on AI-ready floors.

Government-Led Digital Transformation Programs

Abu Dhabi’s Digital Strategy 2025-2027 mandates 100 % adoption of sovereign cloud across all ministries, immediately enlarging addressable demand for domestic data-center space. The Federal Digital Network (FEDnet) extension calls for distributed nodes to back real-time e-government services, effectively guaranteeing multi-availability-zone capacity reservations. Abu Dhabi Municipality is already rolling out a Tier IV disaster-recovery site with Huawei to safeguard smart-city data.[2]Staff Writer — “Abu Dhabi Digital Strategy 2025-2027 Detailed,” zawya.com Once public-sector workloads migrate, private enterprises are expected to follow suit to preserve interoperability with government systems and secure B2G contracts. The job-creation target of 5,000 digital roles is spurring ancillary edge-facility builds near population centers to ensure low-latency service delivery.

5G- and IoT-Fuelled Edge-Computing Demand

Nation-wide 5G coverage combined with surging IoT device counts is moving compute closer to the user. Qualcomm’s Abu Dhabi Engineering Center is prototyping 5G edge-AI gateways that depend on micro-data-centers situated at base-station level. du is complementing macro-hyperscale projects by trialing 5G-Advanced cells capable of hosting micro-edge nodes on-site.[3]Staff Writer — “Qualcomm Opens Abu Dhabi Engineering Center,” qualcomm.com Utilities and energy producers are adopting localized compute for real-time grid optimisation, prompting a wave of containerised edge builds around industrial zones. These deployments boost overall utilisation of the UAE data center construction market by adding incremental capacity orders across secondary emirates.

Arrival of Hyperscale Cloud Availability-Zones

Dedicated cloud regions from Microsoft Azure, among others, are redefining baseline redundancy expectations in the UAE data center construction market . The G42-led campus plans illustrate the next iteration: integrated AI super-clusters embedded within sovereign-cloud frameworks. Contracting models increasingly require multi-phase buildouts that guarantee live power during construction, pressuring contractors to adopt modular “live-site” practices. Regional incumbents like Khazna are widening their footprint abroad to retain share as global hyperscalers land; their local regulatory knowledge remains a core selling point. Standardised hyperscale specifications are also opening doors for niche EPCs with repeatable, factory-built designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and licensing complexities | -2.3% | Nationwide, variable by free zone | Medium term (2-4 years) |

| High electricity tariffs and grid constraints | -1.9% | UAE-wide, dense sites hit hardest | Short term (≤ 2 years) |

| Scarcity of Tier III/IV skilled labour | -1.6% | National, specialists in short supply | Long term (≥ 4 years) |

| Water-scarcity cooling surcharges | -1.2% | Desert regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Licensing Complexities

The Federal Personal Data-Protection Law imposes overlapping obligations for operators serving multiple customer cohorts, requiring bespoke compliance protocols across federal, DIFC and ADGM regimes. Unresolved implementing regulations leave ambiguity on cross-border transfer conditions, delaying green-light decisions for new builds. Hyperscalers often duplicate workloads across two UAE zones to satisfy residency clauses, inflating capex and complicating traffic engineering. The new UAE Data Office introduces another checkpoint in project-approval workflows, compelling operators to widen legal and compliance budgets.

High Electricity Tariffs and Grid Constraints

Dubai’s tiered tariff—20 to 33 fils per kWh—creates a steep marginal-cost curve at power footprints above 50 MW. Intermittent renewables integration complicates grid-stability forecasts, especially outside Dubai and Abu Dhabi where utility upgrades lag. Operators are therefore investing in behind-the-fence solar arrays and battery farms, driving up initial capex even as long-term opex falls. Mega-projects must also coordinate with Emirates Water and Electricity Company to reserve dedicated feeders, elongating permitting timelines and amplifying the restraint on the UAE data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Drives Premium Infrastructure Demand

The UAE data center construction market size allocated to Tier-certified facilities favored Tier 3 with 48.25% share in 2025. Growing hyperscale presence, however, is pushing Tier 4 capacity at a 19.86% CAGR through 2031 because machine-learning services require 99.995% uptime for regulated workloads. Abu Dhabi Municipality’s Tier IV disaster-recovery site illustrates the public-sector appetite for premium resilience

Tier 1 and Tier 2 footprints are receding as enterprise digitalisation programs pivot toward cloud-first architectures that assume higher service-level agreements. Operators use Tier 4 branding to justify premium pricing, which helps amortise step-ups in power-distribution gear and advanced cooling. The segment’s expansion concentrates skilled-labour shortages in commissioning and QA roles, reinforcing one of the market’s key restraints.

By Data Center Type: Hyperscaler Self-Build Reshapes Market Dynamics

Colocation retained 70.55% of the UAE data center construction market share in 2025, but self-build hyperscaler footprints are growing 22.45% annually, signalling a structural pivot. Microsoft’s decision to develop a dedicated du-operated campus rather than lease space in existing colocation halls confirms hyperscalers’ preference for bespoke specifications reuters.com. The UAE data center construction market size attached to self-builds is therefore on track to overtake retail colocation floors by the decade’s end.

Edge and enterprise builds continue to proliferate, mainly to satisfy data-sovereignty needs in healthcare and energy verticals. Qualcomm’s gateway initiative demonstrates corporate willingness to sponsor ultra-compact nodes when latency or data-protection requirements dictate local processing. These diversified build types distribute revenue streams across contractors while reducing single-customer concentration risk for landlords.

By Electrical Infrastructure: Power Backup Dominates Amid Grid Modernisation

Power-backup equipment such as rotary UPS and diesel-replacement flywheels captured 57.85% of electrical revenue in 2025. As AI clusters ramp, sophisticated bus-ducts and intelligent PDUs are forecast to record 21.05% CAGR through 2031, elevating their contribution to the UAE data center construction market size. Operators favour resilient designs that can absorb grid shocks without battery drain, reflecting lessons learned from intermittent renewables.

Khazna’s diesel-free operational concept uses grid plus battery-storage orchestration to align with national decarbonisation goals . These solutions raise up-front costs but lower lifecycle emissions and fuel logistics. Suppliers capable of integrating renewables into static-switch architectures are likely to win disproportionately as green-finance covenants tighten.

By Mechanical Infrastructure: Server and Storage Expansion Mirrors AI Pivot

Cooling remained the largest mechanical category at 55.9% share in 2025, reflecting the desert climate’s thermal-management challenges. Yet servers and storage hardware will expand 20.25% per year as hyperscalers install GPU-dense racks entering the UAE data center construction market. Vertiv’s MegaMod CoolChip modules, designed for 75 kW-per-rack deployments, highlight how suppliers are packaging prefabricated white space that can be commissioned in 12 weeks.

Racks, containment aisles and busways are being redesigned to facilitate liquid-coolant loops and rear-door heat exchangers. These mechanical upgrades ripple through to construction sequencing, as slabs must now accommodate heavier rack loads and embedded piping. The transition underscores how AI compute requirements drive capex distribution away from shell-and-core toward IT-and-cooling-heavy bill-of-materials.

Geography Analysis

Dubai and Abu Dhabi dominate the UAE data center construction market given their connectivity, policy support and concentration of enterprise headquarters. Dubai’s cluster benefits from omnidirectional subsea-cable ingress, enabling both Gulf and East-African traffic to interconnect at minimal latency. Free-zone frameworks grant 100 % foreign ownership, which accelerates permitting for newcomers. Azure’s forthcoming availability zone and Equinix’s continuous expansions reinforce Dubai’s status as the default on-ramp for multinational cloud services.

Abu Dhabi’s AED 13 billion sovereign-AI program positions the capital as a governmental and research nucleus, fuelling demand for Tier IV and GPU-optimised halls. The emirate’s G42-anchored 5 GW campus will become the largest single allocation of the UAE data center construction market size once energised, drawing a global ecosystem of AI chipmakers, software firms and academic partners zawya.com. Edge-node work packages are concurrently proliferating around government precincts to guarantee sub-5 millisecond round-trip for smart-city control loops.

Secondary emirates are absorbing spill-over builds as operators chase lower land prices and redundant power feeds. Ajman’s 100 MW Khazna project illustrates how cost-efficient plots can host AI mega-farms while still interconnecting via dark-fiber backbones to Dubai hubs. Fujairah leverages direct Arabian Sea cable landings for disaster-recovery footprints that avoid Strait of Hormuz choke points. Collectively, these satellite zones diversify risk and unlock incremental capacity without overburdening Dubai and Abu Dhabi grids.

Competitive Landscape

Competition is moderate, with a handful of regional specialists and several inbound global players. Khazna, Moro Hub and Gulf Data Hub collectively command a sizable share, yet no single operator exceeds half of installed capacity. International brands such as Equinix and Digital Realty leverage global design templates to accelerate time-to-market. The UAE data center construction market thus rewards firms that can localise global best practices within the UAE’s regulatory and climatic context.

Strategic focus centers on sustainability and localisation. Khazna’s diesel-free blueprint and Moro Hub’s solar-powered campus set new performance benchmarks that attract capital eligible for ESG frameworks. Concurrently, developers are rolling out Emiratisation programs to groom local engineers for Tier III/IV commissioning roles, helping mitigate labour bottlenecks.

MandA activity is heating up: the USD 5.5 billion valuation attached to Khazna after Silver Lake and MGX’s 40 % stake signals strong investor confidence in home-grown platforms. Cross-border outreach is rising too; Khazna’s Turkey expansion reveals a bid to export regulatory know-how while capturing emerging-market upside. Technology partnerships—like Vertiv’s modular-cooling alliance with Gulf Data Hub—illustrate how OEMs co-innovate with local builders to compress deployment timelines and cut PUE.

UAE Data Center Construction Industry Leaders

Khazna Data Centers

Equinix

Moro Hub (DEWA)

Amazon Web Services

Microsoft Azure

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OpenAI partnered with UAE authorities to anchor a hyperscale facility in the 5 GW Abu Dhabi AI campus, positioning the site among the world’s largest AI data centers.

- May 2025: G42 announced a UAE-US consortium to build the 5 GW AI Campus, aiming to supply sovereign AI compute to nearly half the world’s population.

- April 2025: Microsoft and du signed an AED 2 billion agreement to develop a hyperscale data center in Dubai, designated for AI and cloud workloads.

- March 2025: ADQ teamed with ECP on a USD 25 billion energy-infrastructure fund to finance power assets serving future hyperscale builds.

- February 2025: Khazna began constructing a 100 MW AI-optimised data center in Ajman, scheduled for commissioning in Q3 2025.

- January 2025: Abu Dhabi Government unveiled its Digital Strategy 2025-2027, allocating AED 13 billion toward a fully AI-native public-sector cloud.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates data center construction market as all spending on design, civil works, electrical-mechanical systems, and software integration required to deliver new, expanded, or fully refurbished carrier-neutral, enterprise, edge, and hyperscale facilities across the country.

We exclude minor maintenance projects below 1 MW IT load and temporary modular container rentals.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with general contractors, MEP engineers, and colocation planners in Dubai, Abu Dhabi, and Sharjah. They then ran short surveys with cloud tenants to confirm utilization ramps and Tier IV demand.

Desk Research

We consulted open datasets from the Federal Competitiveness & Statistics Center, Dubai Municipality building permits, DEWA high-voltage connections, and TeleGeography cable maps to size capacity pipelines. Extra color came from company filings, Volza trade records for switchgear imports, Emirates Green Building Council efficiency guidelines, and patent analytics via Questel. These illustrate the breadth of sources, and many more were checked for validation.

Market-Sizing & Forecasting

A top-down model converts announced megawatts and typical cost per MW into a spending pool, which is subsequently cross-checked through sampled equipment bills, channel checks, and selective bottom-up roll-ups. Key inputs include land-ready megawatts, blended cost per MW, foreign contractor share, green-energy premium, and exchange rate-adjusted material inflation. We forecast through 2030 using multivariate regression tied to GDP, cloud outlay, and fiber route kilometers, supported by scenario analysis for hyperscale campus timing. Gaps in supplier data are bridged by power-to-area ratios that our fieldwork has already vetted. This is where Mordor Intelligence applies experience gained from similar GCC models.

Data Validation & Update Cycle

Outputs face variance checks against utilities' connection data and customs entries. Senior reviewers inspect anomalies before sign-off. We refresh annually and trigger mid-cycle updates when projects above 10 MW reach final investment decision. An analyst reruns every calculation before delivery.

Why Our UAE Data Center Construction Baseline Commands Reliability

Published estimates often diverge, and we frequently find that firms mix IT equipment with shell costs, adopt differing Tier scopes, or lock currency at separate dates.

Key Gap Drivers: some track only hyperscale shells, others apply a uniform $/MW, while a few roll forward five-year budgets without confirming ground-break.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.55 B | Mordor Intelligence | - |

| USD 1.26 B | Global Consultancy A | Omits tenant-supplied electrical racks, single exchange rate |

| USD 0.80 B | Regional Consultancy B | Models Tier I-II sites only |

| USD 3.50 B | Industry Journal C | Adds equipment refresh and unfunded announcements |

These contrasts show how Mordor's disciplined scope selection, dual-source cost inputs, and yearly refresh give decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

How big is the UAE Data Center Construction Market?

The UAE Data Center Construction Market size is expected to reach USD 2.22 billion in 2026 and grow at a CAGR of 17.42% to reach USD 4.95 billion by 2031.

What is the current UAE Data Center Construction Market size?

In 2026, the UAE Data Center Construction Market size is expected to reach USD 2.22 billion.

Who are the key players in UAE Data Center Construction Market?

Jacobs Engineering Group, Arup Gulf Limited, AECOM., Turner & Townsend and Aurecon Group Pty. Ltd. are the major companies operating in the UAE Data Center Construction Market.

What years does this UAE Data Center Construction Market cover, and what was the market size in 2025?

In 2025, the UAE Data Center Construction Market size was estimated at USD 2.22 billion. The report covers the UAE Data Center Construction Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the UAE Data Center Construction Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: