Middle East Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

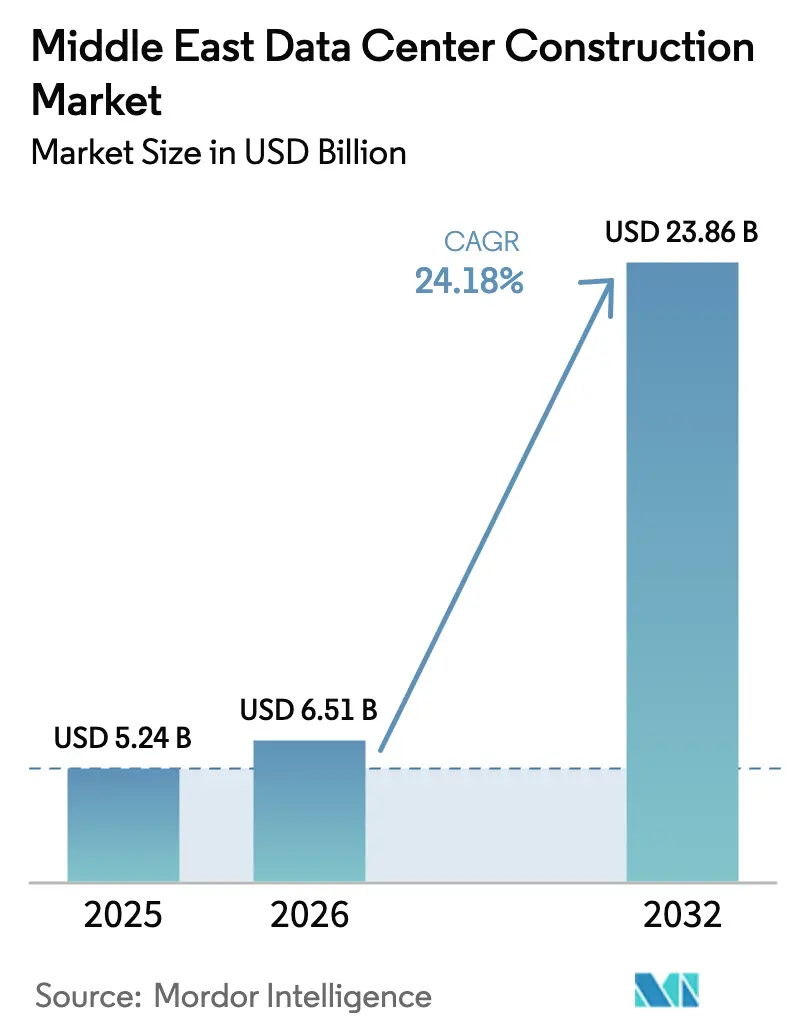

| Base Year Market Size (2025) | USD 5.24 Billion |

| Market Size (2026) | USD 6.51 Billion |

| Market Size (2032) | USD 23.86 Billion |

| Growth Rate (2026 - 2032) | 24.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Data Center Construction Market Analysis by Mordor Intelligence

The Middle East data center construction market size was valued at USD 5.24 billion in 2025 and estimated to grow from USD 6.51 billion in 2026 to reach USD 23.86 billion by 2032, at a CAGR of 24.18% during the forecast period (2026-2032). Accelerated investment from sovereign wealth funds, hyperscale cloud build-outs, and government digital-economy programs underpin the region’s rapid capacity expansion. Mechanical infrastructure keeps a lead position thanks to cooling needs in desert climates, while electrical systems record the fastest spend growth as operators chase high-density AI workloads. The United Arab Emirates (UAE) anchors the Middle East data center construction market with mature connectivity and renewable power options, yet Saudi Arabia’s Vision 2030 pipeline turns the Kingdom into the highest-growth arena. Supply chain bottlenecks in steel and specialty cooling gear tighten project schedules, but long-term power-purchase agreements (PPAs) built on solar and nuclear assets help offset operating costs and carbon liabilities.

Key Report Takeaways

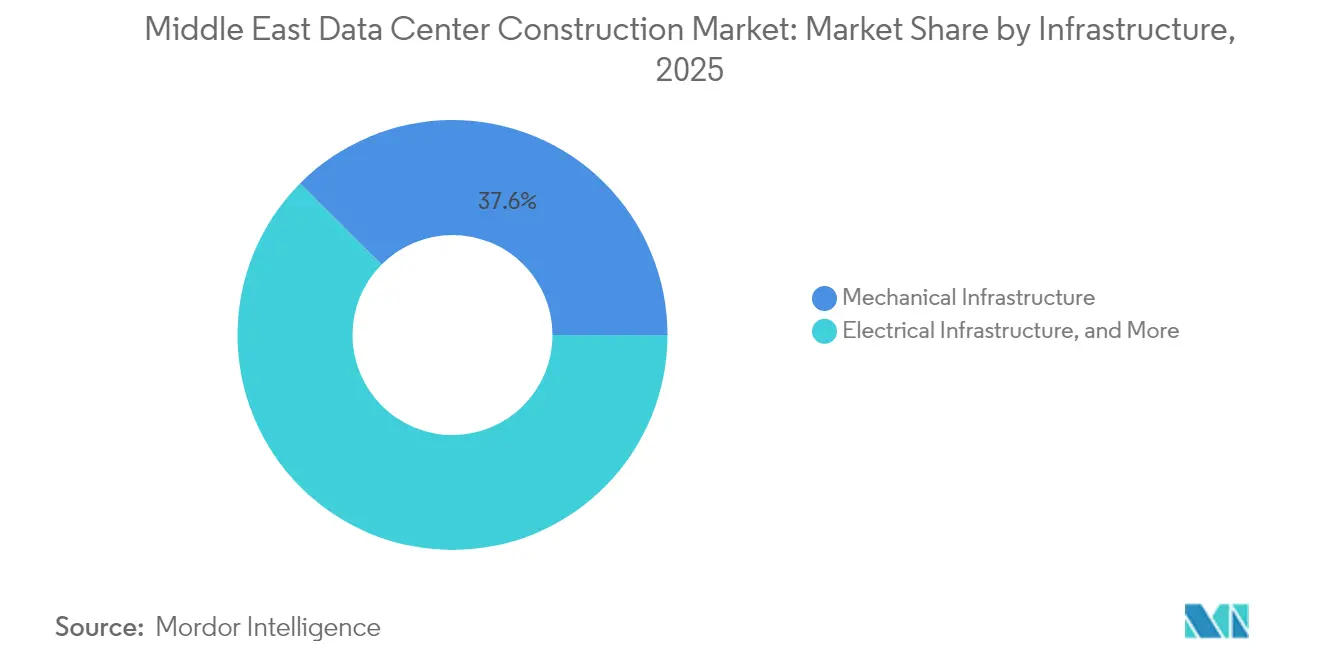

- By infrastructure, mechanical systems held 37.55% of the Middle East data center construction market share in 2025. And, electrical systems are projected to advance at a 27.84% CAGR through 2032.

- By tier type, Tier III installations commanded 53.65% revenue in 2025. And, Tier IV facilities are set to expand at a 21.72% CAGR to 2032.

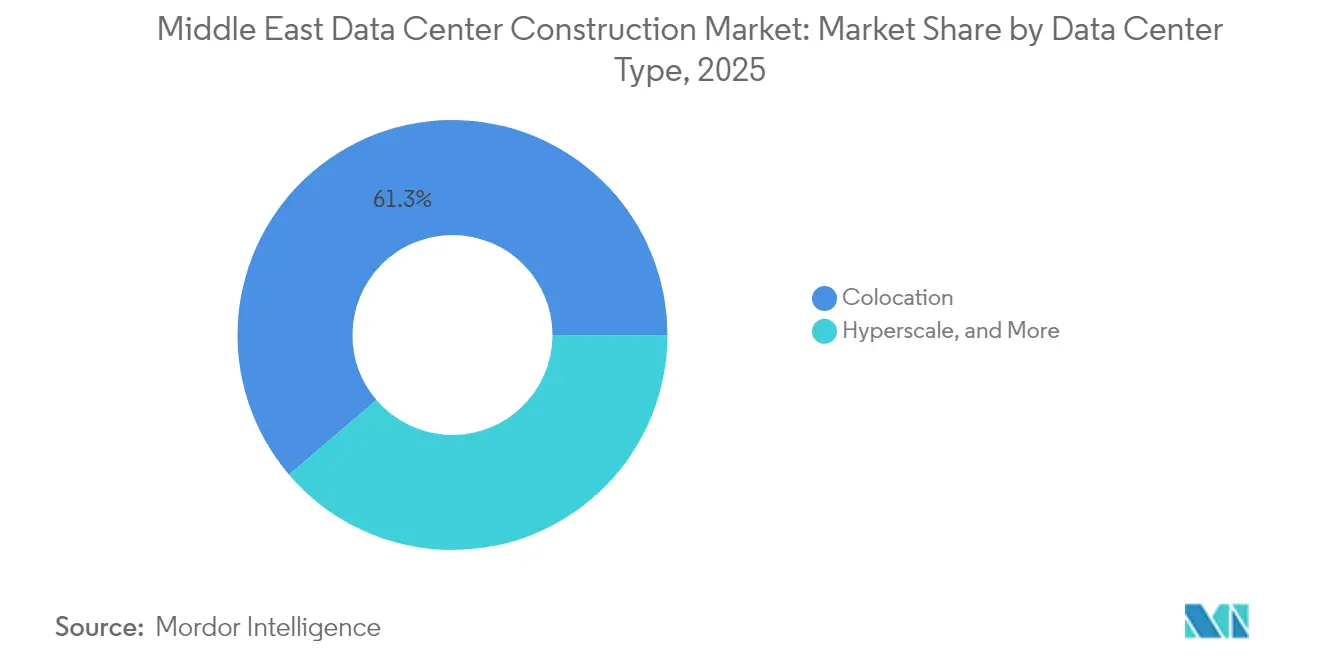

- By data center type, colocation led with a 61.25% share of the Middle East data center construction market size in 2025. By data center type, hyperscale deployments are forecast to rise at a 28.85% CAGR through 2032.

- By end-user industry, IT and Telecommunications led with a 40.35% share of the Middle East data center construction market size in 2025, and is forecast to rise at a 20.98% CAGR through 2032.

- By geography, the UAE captured 32.60% of 2025 revenue, while Saudi Arabia is growing at 20.83% through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud and AI build-outs | +8.20% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Government digital-economy and Vision programs | +6.10% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| 5G-edge latency requirements | +3.80% | GCC-wide, UAE lead | Short term (≤ 2 years) |

| Utility-scale solar and nuclear PPAs | +2.90% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Sovereign-wealth build-to-suit funding | +2.10% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Red Sea/Gulf cable landings | +1.40% | Saudi–Egypt corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud and AI Build-outs Accelerate Regional Infrastructure Transformation

OpenAI’s partnership with G42 on the 5 GW “Stargate UAE” campus pushes rack power densities toward 80 kW and makes liquid cooling a baseline design. Microsoft’s zero-water technologies further widen mechanical complexity in desert settings [1]HPCwire, “Microsoft to Open ‘Zero Water’ Data Centers in 2026,” hpcwire.com. These deployments raise electrical subsystem demand and anchor the Middle East data center construction market as a testbed for next-generation high-density designs.

Government Digital-Economy and Vision Programs Drive Sovereign Infrastructure Development

Saudi Arabia’s draft Global AI Hub Law introduces data-embassy provisions favoring in-country build-outs [2]CMS LawNow, “Shaping the future of data sovereignty: Saudi Arabia issues new draft Global AI Hub Law,” cms-lawnow.com. Parallel moves in the UAE and Oman embed local-content thresholds in procurement rules. The resulting predictable demand stream underwrites long-horizon capital spending and cements the Middle East data center construction market as the core platform for digital-government strategies.

5G-Edge Latency Requirements Spur Distributed Site Development

Etisalat’s 5G-edge-in-a-box roll-out embeds micro data centers inside cellular nodes, trimming latency to sub-10 ms for AR and IoT workloads [3].Intel, “Etisalat Harnesses 5G Edge Computing,” intel.com These projects rely on prefabricated modules and favor local builders capable of rapid site activation, widening participation in the Middle East data center construction market.

Utility-Scale Solar and Nuclear PPAs Transform Energy Economics

The UAE’s 5.3 GW Barakah reactors provide carbon-free baseload that aligns with corporate net-zero targets. Saudi solar auctions settle below USD 0.02 per kWh, locking in thirty-year power cost visibility. Developers now synchronize PPA signing with early design, firmly linking energy strategy to construction phasing across the Middle East data center construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power bottlenecks and diesel inflation | −4.3% | Saudi Arabia, Kuwait, Oman | Short term (≤ 2 years) |

| Cooling-water scarcity and wastewater fees | −3.1% | GCC-wide; acute in UAE and Qatar | Medium term (2-4 years) |

| Shortfall of Tier III/IV certified staff | −2.8% | Regional; highest in Saudi Arabia | Long term (≥ 4 years) |

| Local-content and data-sovereignty hurdles | −1.9% | Saudi and UAE regulatory zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Power Bottlenecks and Diesel Capex Inflation Constrain Rapid Deployment

Transmission upgrades trail demand, postponing energization by up to 18 months in Saudi growth corridors. Diesel backup systems cost 35-40% more than in 2024 due to steel and transport premiums [4]Steel Radar, “Rebar prices surge as Saudi Arabia’s mega projects drive market demand,” steelradar.com. These factors slow near-term project starts inside the Middle East data center construction market.

Cooling-Water Scarcity and Wastewater Fees Drive Innovation Requirements

Desalination fees send operating water costs to 15-20% of OPEX, prompting operators to adopt air-cooled or zero-water designs that raise energy draw by 20-30%. Approval cycles lengthen as authorities scrutinize wastewater plans, stretching construction schedules in the Middle East data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Electrical Systems Scale for High-Density Loads

Electrical equipment revenue rose behind growing GPU clusters, and electrical subsystems are on pace for a 27.84% CAGR. Switchgear, PDUs, and UPS units capable of 40-80 kW per rack reshape room layouts and lift structural loads. The Middle East data center construction market size for electrical systems is projected to reach USD 6.72 billion by 2032. Integration of liquid cooling pumps raises facility electrical consumption by 15-25%, blurring boundaries between mechanical and electrical trades. Service providers therefore bundle design, integration, and renewable-energy consulting into turnkey offers, deepening specialization inside the Middle East data center construction market.

Mechanical systems still absorb the largest spend because desert locations demand robust cooling. Rapid adoption of rear-door heat exchangers and direct-to-chip loops keeps mechanical share at 37.55% in 2025. Project designs now allocate extra white-space height for manifold routing and heavier chillers, increasing civil costs. Electrical and mechanical coordination thus defines project critical path and shapes competitive positioning throughout the Middle East data center construction market.

By Tier Type: Reliability Preferences Diversify Capex Profiles

Tier III accounted for a 53.65% stake in 2025 by balancing 99.982% uptime with cost control. Banking and public-sector clients, however, push Tier IV uptake to a 21.72% CAGR to 2032 as they adopt active-active architectures. Tier IV’s higher sealing and dual-bus electrical schemes uplift capex by 25-30% yet unlock premium pricing. The Middle East data center construction market share for Tier IV is poised to hit 17.45% by 2032 as regulatory and fintech workloads climb.

Edge deployments generally favor Tier II shells to speed roll-out. Modular vendors certify components in-factory, cutting site work by half and enabling 12-week go-live cycles. Uptime Institute certificates remain a procurement prerequisite, compelling smaller builders to partner with global assessors. Certification backlogs, however, accentuate the regional skills deficit and slow some Tier III upgrades inside the Middle East data center construction market.

By Data Center Type: Hyperscale Momentum Redefines Scale Economics

Colocation keeps the largest revenue slice at 61.25%, supported by enterprise outsourcing and cross-connect density. Yet hyperscale builds log a 28.85% CAGR as cloud giants chase in-country zones for AI and sovereign workloads. The Stargate UAE 5 GW campus alone will lift the Middle East data center construction market size by USD 2.5 billion between 2025-2028. Hyperscale contracts demand 50–100 MW blocks, shifting procurement toward mega-packages for electrical skids and liquid-cooling manifolds.

Enterprise, edge, and modular footprints address latency-sensitive use cases. Telecom operators co-locate edge pods in 5G towers, compressing build cycles to weeks. This distributed layer funnels traffic back to core hyperscale sites, forming a hybrid topology that broadens revenue channels across the Middle East data center construction market.

By End-User Industry: I IT and Telecommunications Sustain Structural Demand

IT and telecommunications firms generated 40.35% of 2025 construction value and maintain a 20.98% CAGR through 2032. Network transformation, content delivery, and AI platform roll-outs keep these buyers on multi-year capex plans. Financial-services clients implement Tier IV private clouds to satisfy instant-payment regulations, lifting high-availability demand. Healthcare accelerates on telemedicine adoption and mandates for secure patient data hosting, intensifying requirements for ISO 27001 and HIPAA-aligned builds. Government and defense entities reserve isolated halls or standalone compounds with air-gapped networks, raising physical-security specifications and pushing specialized contractors deeper into the Middle East data center construction market.

Geography Analysis

The UAE controls 32.60% of 2025 spending thanks to Dubai’s carrier-dense hubs and Abu Dhabi’s AI initiatives. Nuclear baseload and 2 GW of rooftop solar PPAs anchor power resilience, and submarine-cable aggregation cements Dubai as the principal interconnect gateway. The Middle East data center construction market size attached to UAE projects is projected to hit USD 7.79 billion by 2032.

Saudi Arabia enjoys the fastest trajectory at 20.83% CAGR, underwritten by Vision 2030 projects such as NEOM and smart-city corridors. The Kingdom’s Center3 plans 1 GW of capacity by 2030 while Alfanar and DataVolt announce multi-hundred-MW sites. Regulatory innovation, including data-embassy clauses, attracts foreign capital, and local energy mix diversification lessens fossil dependence.

Qatar, Kuwait, Oman, and Bahrain form the emerging cluster. Qatar’s LEED Platinum MEEZA build set a new sustainability benchmark. Oman Data Park’s USD 450 million Egypt partnership highlights regional spillover. Submarine-cable routes via the Red Sea and Gulf of Aqaba strengthen cross-market latency positions, unlocking edge-node opportunities and distributing work across the wider Middle East data center construction market.

Competitive Landscape

Regional champions and global incumbents vie for land, power, and clients. Khazna commands 300 MW and pushes diesel-free design, pairing solar PPAs with battery storage to secure OPEX gains. Digital Realty and Equinix scale through joint ventures, leveraging brand trust and global reach to land hyperscale anchor tenants. Construction contractors form tri-partite alliances with OEMs and utilities to guarantee equipment supply and grid interconnection, a tactic that mitigates steel volatility and generator delays.

Supply-chain strategies differentiate operators. Bechtel’s joint fabrication unit with Unger Steel shores up structural steel availability inside the UAE. Schneider Electric’s USD 700 million U.S. expansion adds switchgear headroom for GCC projects. Liquid-cooling specialist partnerships surface as a new competitive lever, with vendors offering custom manifold kits bundled with thermal-management control software. Market incumbents that master cross-disciplinary coordination retain pricing power in the Middle East data center construction market.

Middle East Data Center Construction Industry Leaders

Laing O’Rourke

McLaren Construction Group PLC

Turner & Townsend

James L Williams Middle East.

Alfanar Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Cisco joins the Stargate UAE consortium as a technology partner.

- July 2025: Temasek, Microsoft, and BlackRock launch Project MGX, a USD 30 billion multi-region hyperscale initiative targeting Riyadh.

- May 2025: The White House and UAE unveil a 5 GW AI campus in Abu Dhabi.

- April 2025: du and Microsoft close a USD 2 billion hyperscaler facility deal.

- March 2025: Schneider Electric commits USD 700 million to expand switchgear output, assisting Middle Eastern builds.

Middle East Data Center Construction Market Report Scope

Data center construction combines physical processes used to construct a data center facility. It chains construction standards with data center operational environment requirements.

The Middle East data center construction market is segmented by infrastructure (electrical infrastructure (power distribution solution (PDU, transfer switches, switchgear, power panels and components, and other power distribution solutions)), power backup solution (UPS, generators), service – design & consulting, integration, support & maintenance)), mechanical infrastructure (cooling systems (immersion cooling, direct-to-chip cooling, rear door heat exchanger, in-row and in-rack cooling)), racks, and other mechanical infrastructure)), and general construction)), tier type (tier 1 and 2, tier 3, and tier 4), end user (banking, financial services and insurance, IT and telecommunications, government and defense, healthcare, and other end user), and geography. The market sizes and forecasts are provided in USD value for all the above segments.

| Electrical Infrastructure | Power Distribution Solutions | Power Distribution Units |

| Switchgears | ||

| Others | ||

| Power Backup Solutions | UPS | |

| Generators | ||

| Mechanical Infrastructure | Cooling Systems | Liquid-based Cooling |

| Air-based Cooling | ||

| Racks and Cabinets | ||

| Other Mechanical Infrastructure | ||

| IT Infrastructure | Servers | |

| Storage | ||

| Other IT Infrastructure | ||

| General Construction | ||

| Services (Design and Consulting, Integration, Support and Maintenance) | ||

| Tier I and Tier II |

| Tier III |

| Tier IV |

| Colocation |

| Hyperscale / Self-built |

| Enterprise / Edge / Modular |

| Banking, Financial Services and Insurance |

| IT and Telecommunications |

| Government and Defense |

| Healthcare |

| Other End Users |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Rest of Middle East |

| By Infrastructure | Electrical Infrastructure | Power Distribution Solutions | Power Distribution Units |

| Switchgears | |||

| Others | |||

| Power Backup Solutions | UPS | ||

| Generators | |||

| Mechanical Infrastructure | Cooling Systems | Liquid-based Cooling | |

| Air-based Cooling | |||

| Racks and Cabinets | |||

| Other Mechanical Infrastructure | |||

| IT Infrastructure | Servers | ||

| Storage | |||

| Other IT Infrastructure | |||

| General Construction | |||

| Services (Design and Consulting, Integration, Support and Maintenance) | |||

| By Tier Type | Tier I and Tier II | ||

| Tier III | |||

| Tier IV | |||

| By Data Center Type | Colocation | ||

| Hyperscale / Self-built | |||

| Enterprise / Edge / Modular | |||

| By End-User Industry | Banking, Financial Services and Insurance | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare | |||

| Other End Users | |||

| By Geography | United Arab Emirates | ||

| Saudi Arabia | |||

| Qatar | |||

| Kuwait | |||

| Rest of Middle East | |||

Key Questions Answered in the Report

How fast is construction spending growing in the Middle East data center construction market?

Outlays are rising at a 24.18% CAGR and are on pace to reach USD 23.86 billion by 2032.

Which country generates the largest revenue today?

The UAE holds 32.60% of 2025 spending, driven by strong connectivity and renewable power access.

What segment is expanding the quickest?

Hyperscale builds show a 28.85% CAGR as cloud providers deploy AI-optimized campuses.

Why are Tier IV facilities gaining traction?

Financial-services and public-sector clients need 99.995% uptime, lifting Tier IV demand at a 21.72% CAGR.

How are developers managing high energy use?

Long-term solar and nuclear PPAs secure low-cost, carbon-free baseload power and improve sustainability.

What is the biggest near-term obstacle to new projects?

Grid interconnection delays and diesel backup inflation add up to 18 months to many project timelines.

Page last updated on: